From Technology to Brand: The Sino-Korean Rivalry in the Color TV Market

06/12 2026

06/12 2026

448

448

Summary: Three World Cups, but No 'Champion' Title

Source: Chaoyang Capital Theory

As the FIFA World Cup in the United States, Canada, and Mexico approaches, Hisense's logo will appear on World Cup billboards for the third time.

From Russia to Qatar and now to North America, Hisense has become the most prominent Chinese brand in sports marketing over eight years. But has Hisense truly benefited from its consecutive World Cup investments?

Market estimates suggest that the 2026 World Cup sponsorship fee ranges between $75 million and $100 million. When combined with marketing execution costs, the comprehensive investment for a single tournament easily exceeds 1 billion RMB.

Even when spread across Hisense Visual Technology, Hisense Home Appliances, and other subsidiaries, the cost still amounts to several hundred million RMB.

According to financial reports, Hisense Visual Technology achieved a net profit attributable to shareholders of 2.454 billion RMB in 2025, up 9.24% year-on-year.

Market promotion expenses reached 1.8 billion RMB, a 33% increase year-on-year, accounting for 73% of the net profit.

However, the significant overseas exposure Hisense Visual Technology gained through heavy investment has not fully translated into brand premium.

The company's overseas gross profit margin remained at only 12.03% last year, lagging more than 11 percentage points behind the domestic margin of 23.58%.

In contrast, domestic peers like TCL gained access to high-end brands and global channels by acquiring Sony's TV business, while Skyworth secured low-cost operational rights for Panasonic and Philips in Europe and the Americas through brand licensing and agency operations. Hisense chose the most resource-intensive and slowest path: building its own brand, independently investing in events, and expanding channels.

Is this 'slow' approach the correct strategy for breaking into the high-end global market?

Can Hisense break the overseas brands' monopoly on the top share of the high-end market?

World Cup Marketing Cools Down, Hisense Doubles Down

Looking back at Chinese brands' World Cup marketing journey, a shadow seems to loom.

At the 2010 FIFA World Cup in South Africa, Yingli Green Energy became the first Chinese company to sponsor the event. However, just four years later, the global photovoltaic industry hit a low point, and Yingli suffered consecutive massive losses. The sponsorship's effectiveness diminished significantly, and the company ultimately could not renew its contract.

Following Yingli, Wanda became a FIFA top-tier sponsor in 2016, committing $850 million to cover four World Cups. As the domestic real estate cycle declined, Wanda faced financial distress, defaulted on sponsorship fees, and had its rights suspended before officially withdrawing in 2024.

Indeed, sponsoring the World Cup can boost brand exposure but cannot save a company's fundamentals.

If the industry is in a downturn, World Cup billboards become nothing more than extremely expensive backdrops for companies.

Recognizing this, Chinese companies have become more rational for the 2026 FIFA World Cup in the United States, Canada, and Mexico, with an overall 'cooling' trend.

According to Global Data, Chinese companies' total sponsorship for the 2022 Qatar World Cup reached $1.395 billion. For this edition, only four companies—Lenovo, Hisense, Mengniu, and Wuliangye—have confirmed sponsorships totaling 'over $500 million,' a significant reduction from the previous tournament.

Furthermore, considering that approximately 70% of this year's matches will kick off at 2 AM to 10 AM Beijing time, leading to a sharp decline in domestic viewership and advertising value, many brands have withdrawn.

For example, Vivo chose to exit quietly after sponsoring two consecutive tournaments.

Under these circumstances, only brands committed to overseas marketing persist.

Hisense is one such brand. With the domestic color TV market experiencing declining volumes and prices and intensifying internal competition, going global has become a necessity.

Hisense's most high-profile global move has been sports sponsorships, starting with the 2016 UEFA European Championship and continuing uninterrupted through the 2026 World Cup.

Has this investment paid off? Certainly.

According to Hisense, the group's revenue reached 224.4 billion RMB in 2025, up 4% year-on-year, with overseas revenue accounting for 110.7 billion RMB, an 11% increase.

For Hisense Visual Technology, annual revenue was 57.679 billion RMB, down 1.45% year-on-year. The bright spot was that overseas revenue accounted for over half, growing 4.57% year-on-year.

However, the quality of this growth remains questionable.

In 2025, Hisense Visual Technology's domestic gross profit margin was 23.58%, while the overseas margin was only 12.03%.

Weaker profitability in overseas markets compared to the domestic market has been a persistent challenge for Chinese brands going global.

This is not a dilemma unique to Hisense. According to TCL Electronics' financial report, its domestic color TV business had a gross profit margin of 21.7%, while its overseas large-screen display business had a margin of only 15.1%, a significant gap.

Why do Chinese brands have lower gross profit margins overseas than domestically?

The reason lies in brand recognition in the mid-to-high-end color TV market among overseas consumers.

In consumers' minds, Samsung and LG, as 'imported foreign brands,' have long occupied the high-end market niche, while Chinese brands are still perceived as offering 'high cost-effectiveness.'

To move from 'going out' to 'moving up,' Chinese brands must overcome not production capacity or channel barriers but the brand ceiling.

Hisense's consecutive sponsorship of three World Cups aims to break through the domestic brands' exposure ceiling. However, while spending money to gain exposure is easy, converting that exposure into brand recognition is another matter.

Sino-Korean Rivalry: From Technology to Brand

The color TV market has evolved through three eras marked by the rise of Japanese, Korean, and now Chinese companies.

In the 1980s and 1990s, Japanese companies such as Sony, Panasonic, Sharp, and Toshiba dominated the global TV market.

As Japan entered its 'Lost Decade,' Japanese companies gradually retreated.

South Korea's Samsung and LG took over.

To this day, Samsung has remained the global leader for 20 consecutive years.

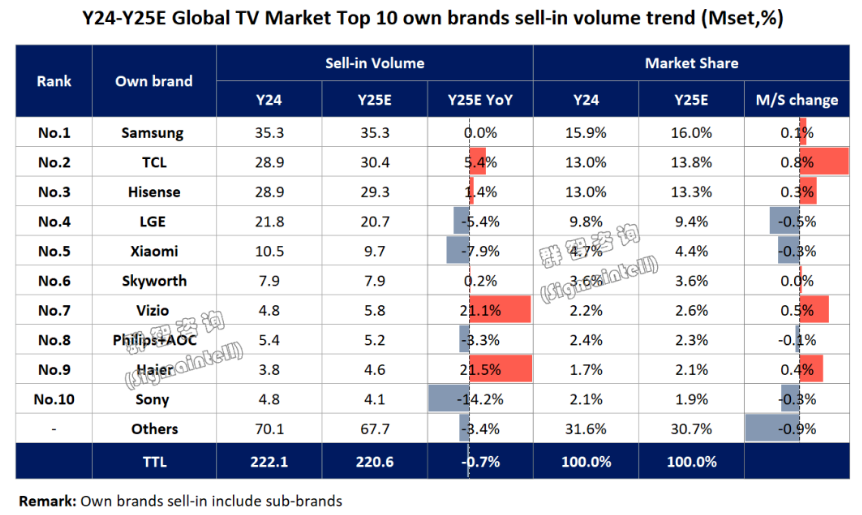

According to AVC Revo's report, Samsung shipped 35.3 million color TVs globally in 2025, down 1.5% year-on-year. However, its high-end OLED TV shipments reached 2 million units, up 39.3% year-on-year.

Figure: Samsung's Micro RGB Product Line

Then came Chinese brands.

From the 'original equipment manufacturer' model adopted by Skyworth and TCL in the 1990s to the mid-2010s, when domestic market saturation and overcapacity forced Chinese brands to truly 'go global.'

2016 marked the first turning point.

According to Huaxi Securities' research report, TCL's overseas TV sales share rose from 49% in 2016 to 76% in 2023. Hisense Visual Technology's overseas sales share increased from 51% in 2019 to 62% in 2023.

Both curves began accelerating upward around 2016.

In 2024, Chinese brands' global TV shipments surpassed those of Korean brands for the first time.

In 2025, the combined shipments of TCL and Hisense further narrowed the gap with Samsung. Among the top 10 global TV brands by shipment volume, three were Chinese brands, with Samsung and LG Electronics occupying the other two spots.

Today, the Sino-Korean rivalry has taken shape, but leading in shipments does not equate to dominating the high-end market.

According to Omdia's 2025 data, Samsung held a 52.2% share in the high-end TV market priced above $1,500 and a 54.3% share in the ultra-high-end market above $2,500.

While Chinese brands have increased their shipments, the top spot in determining brand status remains occupied by Korean companies.

Where does the gap lie?

If the answer were still core panel technology, it would indicate a lack of understanding of why China is described as the 'Industrial Cthulhu.'

According to AVC Revo's data, Chinese panel manufacturers accounted for 69.2% of the global TV panel market share in 2025. BOE, TCL CSOT, and HKC controlled the global large-screen LCD TV panel market, with many high-end models from Sony and Samsung relying on Chinese supply chains for their screens.

The real gap lies in the accumulated perception of technological pathways.

OLED has been marketed as synonymous with 'high-end' over the past decade, with Samsung and LG monopolizing this track (translation note: ' track ' means 'market segment' or 'track'). According to Omdia, LG maintained a 49.7% shipment share in the OLED market, ranking first for 13 consecutive years.

Chinese brands like TCL and Hisense did not choose to compete head-on with OLED but instead pursued Mini LED, a more cost-effective technological window.

Last year, Hisense introduced RGB-Mini LED technology, while TCL launched SQD-Mini LED technology, both representing transformative innovations.

In terms of display technology, Chinese brands are no longer lagging behind overseas brands and can even be considered leaders.

However, translating technological advantages into overall brand recognition requires a lengthy cognitive transformation process.

This may be why Hisense continues to sponsor the World Cup.

For the 2026 FIFA World Cup in the United States, Canada, and Mexico, Hisense increased its investment to approximately $150 million and became the official partner for VAR display technology for the first time, deploying its self-developed RGB-Mini LED equipment in the referee center.

Hisense aims to use the world's largest sports marketing platform—the World Cup—to repeatedly convey a message to consumers: RGB-Mini LED is the direction for the next generation of high-end TVs.

Currently, technological equality has been achieved, but brand equality is still on the way.

TCL Rides the Wave, Skyworth Rents the Boat, Hisense Builds the Ship: Is Slow and Steady the Best Approach?

Regardless, from the perspective of the overall global color TV competition landscape, the 3.0 era of Chinese advancement and Korean retreat has arrived.

Korean brands have clearly shifted toward 'maintaining volume and protecting profits,' with their core strategy for 2026 focused on value-driven replacement cycles through 'high-end + AI + sports events.'

Korean brands' strategic retreat has created a window of opportunity for Chinese brands to achieve both volume and price growth in the European and American high-end markets.

And China is indeed pressing its advantage.

In early 2026, two significant events occurred in the global color TV market: TCL formed a joint venture with Sony, and Skyworth reached a strategic cooperation agreement with Panasonic.

Combined with Hisense, which had already acquired Toshiba, China's leading color TV companies are using similar paths within the same time window to target the same goal: the overseas high-end market.

However, their approaches differ slightly.

TCL is 'riding the wave' by leveraging strong industrial chain and technological integration to take a dominant position in the new joint venture with Sony.

According to Sigmaintell's forecast, TCL's global TV market share, including the joint venture, will expand to 17% by 2027, potentially surpassing Samsung to claim the global top spot for the first time.

Skyworth Group is 'renting the boat' through brand licensing and agency operations in its cooperation with Panasonic.

Panasonic transferred its North American and European sales and marketing operations to Skyworth, which handles operations while Panasonic retains brand ownership. This is not Skyworth's first such deal; it also operates Philips TV in North America.

Skyworth's rationale is that the strategic priority of its TV business is declining, making brand licensing the lowest-cost and fastest way to expand overseas.

In contrast, Hisense invests more heavily in building its own high-end brand: front-loading R&D, optimizing overseas supply chains, and continuously sponsoring top-tier events.

This path is the most resource-intensive and slowest.

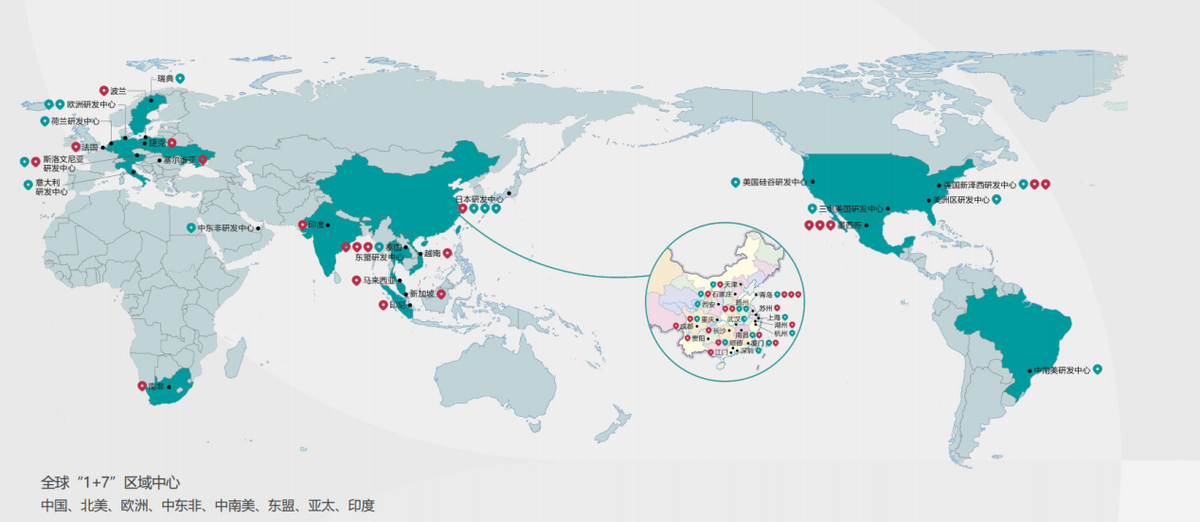

As of the end of 2025, Hisense implemented a '1+7' global regional center layout, establishing 30 R&D centers worldwide and employing over 16,000 engineering and technical personnel—all representing costs.

Not to mention the investment in top-tier event sponsorships. Hisense has consistently used event marketing to enhance its global brand awareness and high-end image.

Jia Shaoqian, Chairman of Hisense Group, said that sports marketing is a 'slow and steady' approach.

But after investing hundreds of millions of dollars, how long will it take for this slow and steady approach to bear fruit?

Diminishing marginal returns are Hisense's current dilemma.

According to Hisense's official data, its global brand awareness surged from 37% to 59% between 2016 and 2021. However, marketing costs are eating into profits.

Financial reports show that Hisense Visual Technology's selling expenses totaled over 7 billion RMB in 2024 and 2025, exceeding its combined net profit for those two years.

Sports marketing represents a long-term accumulation of psychological effects. Exposure can accelerate awareness but cannot achieve trust conversion in the short term.

Hisense is betting against time. Will a decade or more of sustained exposure change global consumer perceptions?

TCL and Skyworth are bypassing the trust accumulation stage in shorter times using different approaches.

As for Hisense, which is building its own ship, only time and consumers can provide the answer to how far it is from reaching the other shore.

-

![]()

Insta360 Leads Global Market, Yet Profit Signals Remain Subdued

-

Marketing and Transaction Growth: Entering the Age of the Agent

-

![]()

Dongfeng’s Solid-State Batteries Set for Mass Production and Vehicle Integration in H2 2026

-

Marketing and Transaction Growth: Entering the Age of Agent

-

![]()

Stock Prices Hit Rock Bottom & Regulatory Interviews Raise Dual Alarms in Auto Industry

-

![]()

Can the Hongqi G919 Surmount the Challenge Posed by the Mengshi 917?

-

![]()

AI Gaokao Evaluations Plagued by Chaos: Full Marks Awarded for Incomplete Questions

-

![]()

For Two Straight Months, No BBA Model Has Exceeded 10,000 Monthly Sales in the Chinese Market