Stock Prices Hit Rock Bottom & Regulatory Interviews Raise Dual Alarms in Auto Industry

06/12 2026

06/12 2026

440

440

Introduction

While it's uncertain whether automotive stocks have bottomed out, what is undeniable is that confidence in the automotive sector is taking a significant hit.

On June 11, two pivotal events unfolded in the automotive industry, prompting deep introspection across the entire supply chain.

One event is the capital market's retreat from the automotive sector. Stock prices of major automakers, including SAIC Motor, GAC Group, and BAIC Group, have successively plummeted to new lows not seen in nearly a decade or even since their listings. The overall valuation of the automotive sector continues to slide, with capital risk aversion reaching a cyclical peak.

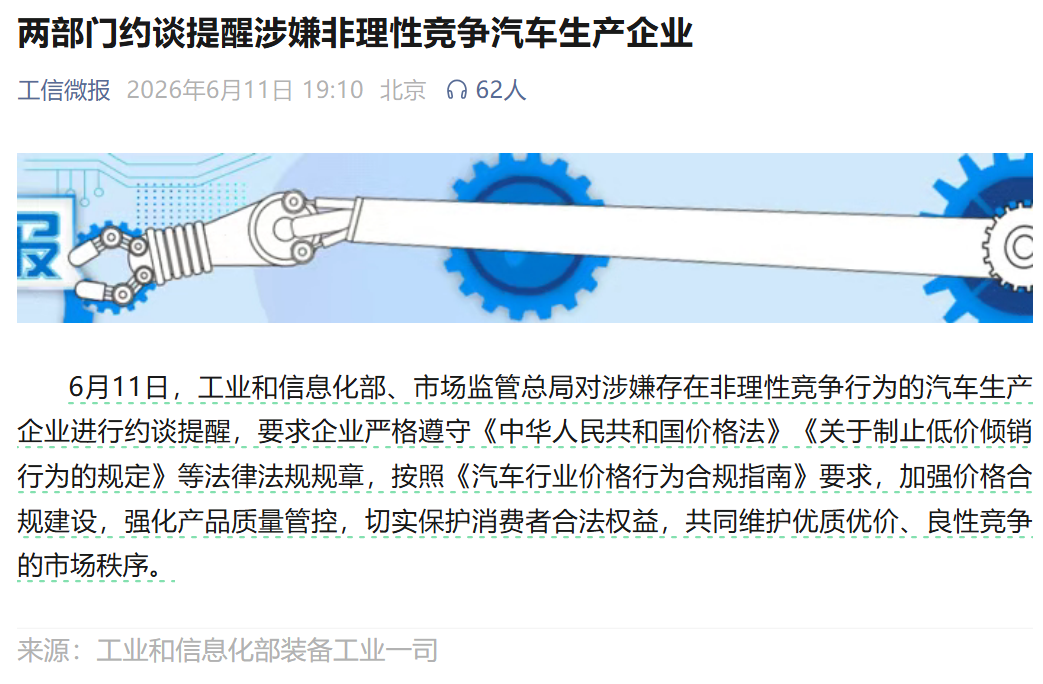

The other event is renewed regulatory scrutiny. The Ministry of Industry and Information Technology (MIIT) and the State Administration for Market Regulation jointly interviewed automakers, directly addressing irrational price cuts and disorderly internal competition within the industry.

These two significant events, though seemingly unrelated, both point directly to the most pressing issue: the automotive industry has entered a period of profound adjustment, marked by an imbalance between supply and demand, pressure on profitability, and disordered competition.

Pessimism is spreading, and the automotive industry is facing its most severe inflection point and test in history. At this critical juncture, the traditional development logic of "pursuing scale, expanding production capacity, and competing on sales volume" has become obsolete. Automakers must abandon their obsession with high-speed growth and shift towards healthy operations and steady development. This is likely the only path for the entire industry to navigate through this adjustment cycle.

01 Capital and Regulators Simultaneously Signal Risks

As of June 11, stock prices of mainstream automakers on the A-share and Hong Kong stock markets have weakened across the board, with several industry leaders hitting multi-year lows and market pessimism spreading.

GAC Group closed at RMB 5.75, with its stock price falling to a ten-year low since May 2015. SAIC Motor closed at RMB 10.87, marking its lowest stock price since June 2016. BAIC Group fell to HKD 1, hitting a record low since its listing in 2014, with a market capitalization of only HKD 8 billion, teetering on the brink of becoming a penny stock.

In addition to traditional automakers, new energy vehicle (NEV) startups have also not been spared. Take the highly talked-about Xiaomi as an example; its stock price has fallen from a peak of HKD 61.45 per share in June last year to a current low of HKD 25.58 per share, a cumulative decline of over 58%. In just one year, Xiaomi's total market capitalization has shrunk from HKD 1.48 trillion to around HKD 667.717 billion, evaporating over HKD 800 billion, with its market value more than halved.

Other NEV startups are faring no better. XPeng Motors saw a single-day decline of 5.63%, while Seres has lost approximately RMB 25 billion in market capitalization over the past ten trading days. NIO's stock price has also essentially returned to its historical lows. The entire automotive sector is characterized by low trading volumes and a lack of incremental capital, displaying typical characteristics of a zero-sum game in existing market share.

The pricing logic in the capital market has always been pragmatic. The continuous decline in stock prices essentially reflects investors' comprehensive bearish outlook on the industry's future profitability, growth potential, and competitive landscape.

On the one hand, domestic auto sales have declined by nearly 20%, and the price war rages on without end. Automakers' gross profit margins on complete vehicles continue to be compressed. In the first quarter of 2026, the overall profit margin of the automotive industry was only 3.2%, far below the average level of downstream industries, with profit margins continuously being eroded.

On the other hand, the slow transformation of joint-venture automakers and the intensifying internal competition among domestic automakers, coupled with the expanding losses of dealers and rising channel risks, have created multiple uncertainties, leading capital to choose risk aversion. Behind the decade-long cycle of stock prices lies a true reflection of the industry's fading dividends and the end of its extensive growth model.

The joint interview by the two ministries is also aimed at drawing red lines for disorderly price wars and internal competition within the industry.

On June 11, the Ministry of Industry and Information Technology and the State Administration for Market Regulation jointly conducted interviews and reminders with automotive manufacturing enterprises suspected of engaging in irrational competition. They required these enterprises to strictly abide by the "Price Law" and the "Regulations on Preventing Low-Price Dumping Behavior," strengthen price compliance and strictly control product quality in accordance with the "Compliance Guidelines for Price Behavior in the Automotive Industry," and jointly maintain a market order of high quality and fair pricing.

There is widespread speculation about which automakers were interviewed. The author believes that several leading automotive brands are highly likely to have been interviewed together due to their large scale and the significant impact any of their actions can have on the entire industry. Additionally, brands that dominate social media and public opinion may also have been targeted because, in the information age, the influence of online public opinion on consumer psychology far exceeds that of the past, necessitating stronger regulation.

In fact, this is not the first time regulators have taken action. From the tripartite symposium in January this year to address price disorder to the strengthening of cost monitoring in March, and now this centralized interview, the regulatory approach has been consistent: to resolutely curb internal competition behaviors such as "selling cars at a loss, malicious price cuts, and false advertising," attempting to use the invisible hand of the government to steer the industry towards healthy development.

It is evident that regulators have clearly recognized that endless internal competition will only destroy the industry's foundation. Currently, the industry widely experiences "price inversion," where dealers incur losses on every vehicle sold, and automakers rely on low prices and high volumes to gain market share, plunging the entire upstream and downstream industrial chain into losses. Low-price competition has not spurred positive innovation but has instead led some companies to sacrifice quality to cut costs, damaging consumer rights and undermining the industry's long-term development potential.

The combination of these two signals indicates that the automotive industry is facing its most difficult moment in history. The era of "barbaric growth" through price cuts for volume gains has come to a definitive end.

02 Multiple Factors Compound, Domestic Auto Market Falls into a Cyclical Low

The underlying causes of declining stock prices and regulatory interviews lie in the persistent weakness of the terminal market. According to the production and sales data released by the China Association of Automobile Manufacturers (CAAM) for January-May 2026, the overall downward trend in the domestic automotive market is clear, and the industry has officially entered a stage of profound competition over existing market share.

Data shows that from January to May 2026, domestic automotive production and sales reached 12.235 million and 12.207 million vehicles, respectively, down 4.6% and 4.2% year-on-year. Passenger vehicles, as the mainstay of the market, saw production and sales of 10.349 million and 10.318 million vehicles, respectively, during the same period, down 6.6% and 6.2% year-on-year, with the decline widening further.

Looking at specific segments, new energy vehicles (NEVs) continued to grow in May, with sales reaching 1.496 million vehicles, up 14.4% year-on-year. From January to May, cumulative sales reached 5.802 million vehicles, up 3.5% year-on-year, with the NEV penetration rate reaching 47.5%. This indicates that not all segments are weakening; the significant contraction in fuel vehicle sales is the core driver of the overall decline in passenger vehicles.

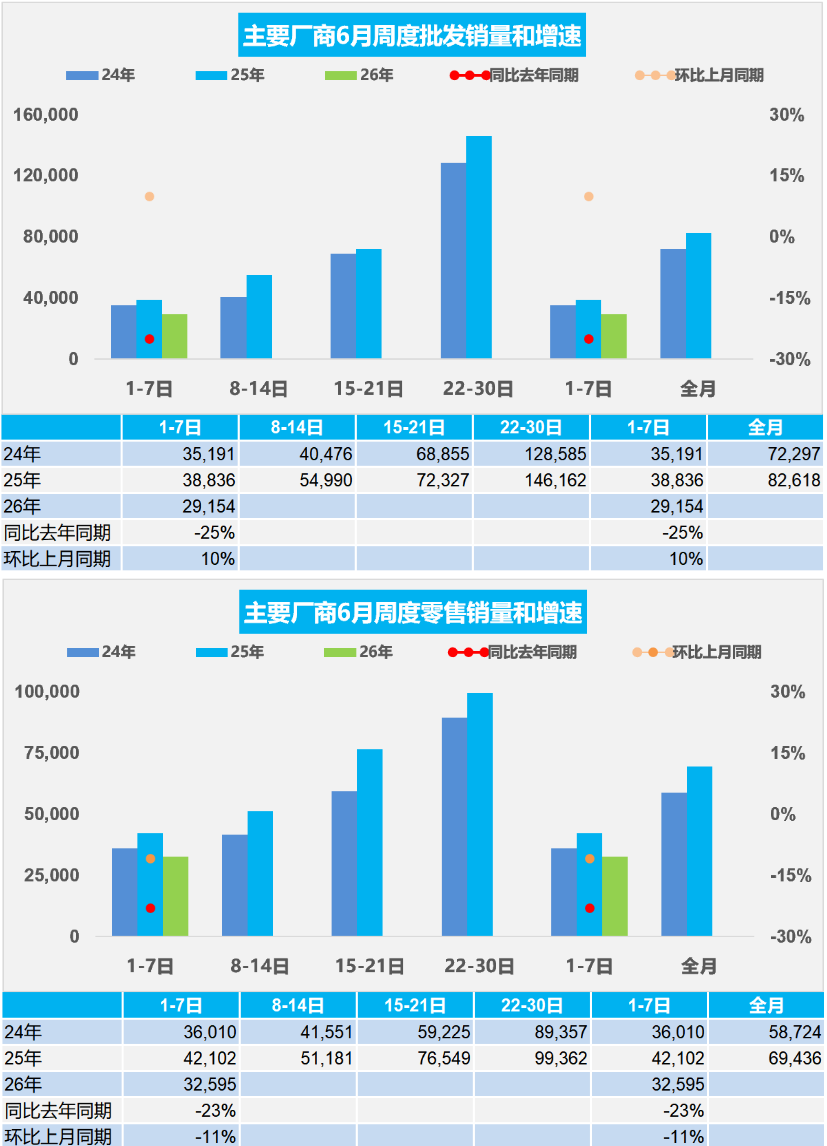

Of course, as June arrives, the entire industry is entering its slowest season of the year. Weekly data from the China Passenger Car Association for the first week of June (1-7) shows that domestic retail sales of automobiles fell by 23% year-on-year, while wholesale declines reached 25%. Dealers in some regions report high inventory pressure and have largely stopped taking delivery of new vehicles.

This aggregation of information casts an even thicker shadow over the automotive market in the second half of the year.

Analyzing the decline in domestic auto sales, there are two core reasons. The first is the overdraft of previous policy dividends, with a high base suppressing current sales. Over the past two years, policies such as local car-buying subsidies, purchase tax exemptions, and local consumption vouchers, combined with NEV replacement incentives, have significantly stimulated short-term consumption. Many users who originally planned to delay vehicle replacement or purchases completed transactions ahead of schedule during the policy window, directly overdrafting regular consumer demand in 2026.

After the policy dividends fade, the market returns to its natural consumption rhythm, and the purchasing power released earlier disappears. Coupled with the high base from the same period last year, which was itself stimulated by policies, a significant year-on-year decline becomes inevitable. This "overdraft first, then slump" trend is also a common pattern in many stimulus-driven industries.

Another crucial reason is the macroeconomic environment, which has slowed down the recovery, leading to a comprehensive slowdown in residents' consumption willingness and vehicle replacement cycles. Automobiles are big-ticket consumer goods, and their prosperity is highly tied to the macroeconomy, residents' income, and employment conditions. Currently, the pace of macroeconomic recovery has slowed, with layoffs and salary cuts occurring in many industries. Residents' precautionary savings intentions have risen, making them increasingly cautious about big-ticket purchases like automobiles, which cost tens of thousands or even hundreds of thousands of yuan.

From terminal market research, consumers' vehicle replacement cycles have lengthened from the previous 3-5 years to 5-7 years, with a wait-and-see attitude becoming mainstream. Not only is the automotive industry under pressure, but suppliers, advertising and media, automotive retail, and other upstream and downstream supporting industries are also struggling. The chain pressure from the top down further drags down terminal sales.

After decades of development, China's automotive industry ranks first globally in production and sales, boasting the world's most complete industrial chain and a vast user base. Its fundamentals remain solid. However, history has proven that no industry can remain smooth sailing indefinitely. Short-term sales declines, price fluctuations, and capital market volatility are the true state of the automotive industry and part of its self-purification and survival-of-the-fittest process.

Moving forward, automakers and everyone in the industrial chain must re-examine the logic of industry development. The era of high-speed growth dividends has ended, and steady operations, value competition, and long-termism will become the core themes in the coming years.

For some brands and manufacturers, it is time to proactively adjust their business objectives and abandon unrealistic scale pursuits. They should formulate reasonable production and sales plans based on their technological reserves, brand positioning, and channel capabilities, shut down inefficient production capacity, optimize capacity layout, and reduce operational leverage and financial risks.

More importantly, they need to actively respond to regulatory requirements, resolutely abandon the mindset of low-price internal competition, and shift towards value competition in technology, quality, and services. They should reallocate resources to research and development innovation, product iteration, and user services, using differentiated products to avoid homogeneous price wars and relying on technological and service premiums to reshape their profitability systems. At the same time, when expanding overseas markets, they should adopt a long-term perspective, reject simple low-price volume sales, build a mid-to-high-end product matrix, and uphold the global brand image of Chinese automobiles.

In the future, the automotive industry will no longer compete on who sells more or who has lower prices but on who has better products, healthier operations, and longer-term layouts. Only by abandoning the obsession with scale, adhering to compliant operations, delving deep into technology, respecting the market, and treating the industrial chain well can automakers navigate through this profound adjustment cycle and emerge into the light in two to three years.

Editor-in-Chief: Cao Jiadong Editor: He Zengrong

THE END

-

![]()

Insta360 Leads Global Market, Yet Profit Signals Remain Subdued

-

Marketing and Transaction Growth: Entering the Age of the Agent

-

![]()

Dongfeng’s Solid-State Batteries Set for Mass Production and Vehicle Integration in H2 2026

-

Marketing and Transaction Growth: Entering the Age of Agent

-

![]()

Stock Prices Hit Rock Bottom & Regulatory Interviews Raise Dual Alarms in Auto Industry

-

![]()

Can the Hongqi G919 Surmount the Challenge Posed by the Mengshi 917?

-

![]()

AI Gaokao Evaluations Plagued by Chaos: Full Marks Awarded for Incomplete Questions

-

![]()

For Two Straight Months, No BBA Model Has Exceeded 10,000 Monthly Sales in the Chinese Market