Trillions in Instant Retail Fall Short in Driving Midea’s Growth

06/22 2026

06/22 2026

521

521

Instant Retail Dividends Fail to Propel Midea’s Growth Ambitions

Author | Andrew Editor | Gu Nian

Amidst this year’s 618 shopping spree, instant retail has become the latest battleground for the home appliance sector.

First-quarter financial reports from Midea, Haier, and Gree paint a rather grim picture. With home appliance retail sales declining by 6.2% year-on-year, the trillion-yuan instant retail market has emerged as a highly sought-after growth avenue for brands.

Among these companies, Midea has been the earliest and most efficient in its deployment. Public data indicates that Midea has been in this race for nearly two years since its partnership with Meituan in 2024, swiftly connecting over 20,000 offline stores to various platforms.

However, beneath the surface excitement, the quality of growth remains underwhelming.

In the first quarter of 2026, Midea reported a total operating revenue of RMB 131.581 billion and a net profit attributable to shareholders of RMB 12.675 billion. After excluding non-recurring items, the net profit for the first quarter declined by 14.02% year-on-year. This indicates greater growth pressure in Midea’s core home appliance operations than the surface numbers suggest, while the much-anticipated new instant retail channel has, for the time being, failed to drive significant growth.

As the early leader in instant retail, Midea has been unable to lift its overall performance out of the low-growth territory, risking becoming a follower rather than a pioneer.

Today, numerous brands are officially doubling down on home appliance instant retail, but few have managed to break through inventory stagnation to deliver meaningful incremental growth. The trillion-yuan instant retail track has not become Midea’s breakthrough solution; instead, it has emerged as a new frontier demanding greater patience and time.

Two Years of Effort Yet to Show in Financial Reports

During this year’s 618, Midea intensified its instant retail initiatives by fully connecting brand warehouses and offline stores to flash sale platforms.

In the first phase of the campaign, the fan category saw an average of 2,600 daily orders through this channel, with refund rates 16 percentage points lower and conversion rates 2.2% higher compared to regular orders.

After May, cumulative orders via Midea’s flash sale channel surpassed 100,000, achieving a tenfold increase from January. Compared to Gree, which has not fully embraced instant retail, Midea has clearly become the first major home appliance player to capture instant retail dividends.

Being first to the table stemmed from early deployment advantages.

Going back to 2024, Midea began onboarding 25,000 proprietary retail stores onto Meituan when Meituan Flash Sales was rapidly expanding, with home appliances as its key high-value category. Midea’s full-scale entry became a benchmark event in the industry.

Subsequently partnering with Taobao Flash Sales, Midea completed deep integration with both major instant retail platforms, largely aligning online-offline inventory and pricing systems. Sources close to Midea’s operations revealed that these stores are Midea-operated, suggesting significant investment in human capital for store-level sales.

Operationally, Midea’s instant retail model makes sense. Over 20,000 offline stores and regional warehouses form the fulfillment network, platforms provide traffic, 30-60 minute deliveries meet emergency needs, and a reliable after-sales system supports instant-demand categories like small appliances and air conditioners, supplemented by targeted operations.

Two years of execution proved this broad commercial strategy correct during 618, but the channel’s growth ceiling appears far lower than expected.

Evidence lies in Midea’s decision not to separately disclose instant retail performance in financial reports nor reveal this channel’s GMV ratio. Even with May orders exceeding 100,000, this remains negligible within Midea’s annual hundred-billion-yuan revenue—currently perhaps insignificant.

Industry insiders consider this merely supplementary to traditional channels, shifting orders that would have closed in physical stores or traditional e-commerce to instant retail platforms.

Inevitably, industry cycles impact results. The home appliance sector faces constraints from real estate, consumer capacity, and price wars, with sluggish overall market growth. Instant retail optimizes channel efficiency but cannot alter fundamental industry demand.

While the sector holds hundreds of billions in prospective instant retail dividends with real growth potential, for leading brands, this translates to inventory optimization rather than explosive incremental growth.

After two years of participation, Midea proved this path viable but slow.

Midea’s all-in instant retail bet targets the trillion-yuan track’s future, yet regrettably, this game involves far more complex dynamics and obstacles than imagined. First-Mover Advantage or Headwind Challenges?

First-Mover Advantage or Headwind Challenges?

Pursuing instant retail aims to capture market dividends.

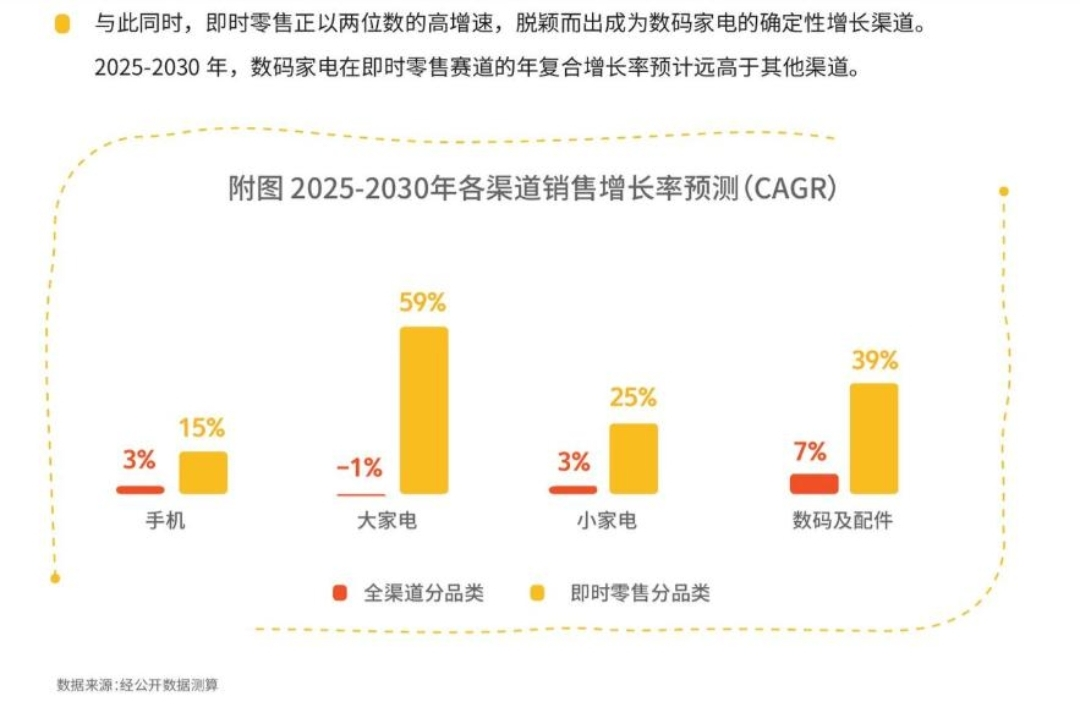

The Academy of Commerce Research forecasts China's domestic instant retail market will surpass RMB 1 trillion in 2026, with multiple authoritative institutions predicting RMB 1-1.2 trillion. For mature industries like home appliances, any trillion-yuan new channel warrants heavy investment, as missed opportunities outweigh trial costs.

Midea entered first to secure early-mover advantages and establish channel barriers. But when chasing early dividends, speed may not equate to the greatest advantage.

First, product mix distribution shows that major appliances' instant retail consumption remains an education-needed market.

CIConsulting data reveals that fresh food, beverages, and staple grains currently dominate instant retail at over 70% combined. The remaining shares are split among snacks, personal care, household items, and 3C digital products, with major appliances accounting for minimal penetration.

Consumption logic varies by scenario. A Chongqing consumer told City Image that fresh food, beverages, and daily essentials represent high-frequency needs, driving strong reliance on instant delivery and repeat purchases. Home appliances, however, are typical low-frequency, high-value purchases planned in advance with price comparisons—not impulsive buys when needs arise.

For major appliances, speed enhances but doesn't determine purchases.

Regarding true pain points—integrated delivery-installation services—instant retail hasn't fully leveraged offline stores' strengths.

Currently, riders handle deliveries while brands' after-sales teams manage installations—two systems requiring better coordination. Integrated services sound simple but demand synchronized delivery timing, installer scheduling, and parts preparation. Any hiccup disrupts experiences.

Similar challenges exist in transparent pricing, reliable after-sales, and other in-home services.

Industry analysts note that brands' control over instant retail platforms warrants scrutiny regarding pricing, gray market goods, authenticity, and SKU completeness. Consumer disputes from misinformation or defective products create headaches for manufacturers, distributors, and users alike—a balancing act involving all stakeholders' interests.

Beyond industry-wide issues, Midea faces mismatches between its strengths and instant retail advantages. Instant retail penetration remains lower in lower-tier markets where Midea traditionally excels, yet this advantage hasn't fully transferred.

In Chongqing, City Image research found significant order volume disparities between urban and rural Midea stores.

From regional food delivery data, urban areas account for ~60% vs. 40% in rural zones—one factor explaining the gap.

Moreover, remote cities may lag in installation services and comprehensive capabilities. Regional structural contradictions likely limit instant retail's incremental contribution to group performance.

Instant retail opens a new track for Midea, but whether early entry provides first-mover advantages or headwind challenges remains uncertain.

Competitors are rapidly following suit. Gree, Haier, and Xiaomi have joined major instant retail platforms. Gree partnered with Meituan Flash Sales during 618 to promote same-day air conditioner installation, directly challenging Midea's strength. Meanwhile, Xiaomi launched major appliances on instant retail, opening official Meituan stores for air conditioners and monitors in select regions.

Once markets mature, Midea’s two-year head start might shrink to months for rivals. Omnichannel Competition Demands Comprehensive Strategies

Omnichannel Competition Demands Comprehensive Strategies

Traditional home appliance channels feature strict regional divisions, with each dealer guarding its territory. Instant retail shatters physical boundaries, transforming same-street competition into global battles.

Frankly, instant retail's challenges merely reflect Midea’s broader omnichannel growth pressures. Battles rage online and offline, across premium and mid-range segments, with no easy fights elsewhere.

Online, traditional e-commerce's traffic dividends peaked long ago, with home appliances hitting penetration ceilings. Only relentless price wars remain. Midea retains scale advantages but faces squeezed margins.

Progress in premium channels also lags Haier.

In the first quarter of 2026, Casarte captured 71.1% of the RMB 15,000+ refrigerator market, 80% of same-priced washing machines, and 44.7% of premium air conditioners.

In major appliances above RMB 10,000, Casarte dominates, leaving scraps for COLMO, Siemens, and others. Midea's eight-year-old COLMO grows rapidly but started later than Casarte, with clear gaps in scale and market position.

Root causes include COLMO initially leveraging Midea's channels and setting aggressive growth targets. Under pressure, pricing drifted downward. While technically advanced, ultra-premium brands often lack mindshare.

Premium markets offer rich profits but remain elusive, while Midea's mid-low-end scale battles leave it vulnerable to price wars and industry cycles.

Offline, Midea leads with tens of thousands of outlets but loses growth momentum. Gree leverages Dong Mingzhu's personal IP for digital flagship stores, with over 10,000 Healthy Home series gaining traction through agile online-offline tactics.

The industry seeks new channels and models relentlessly. Once the most aggressive channel innovator, Midea now appears conventional.

Facing channel pressures, Midea hasn't stood still.

Instant retail represents one initiative. In premium segments, COLMO and Toshiba operate in parallel, establishing over 1,600 COLMO stores covering ~280 cities by end-2025, along with 650+ Toshiba stores and 1,200+ Toshiba showrooms domestically.

For private domain operations, Midea launched its own mini-program and user system, reaching 5.15 million daily page views (PV) last year to retain users.

Yet online battles rage over traffic and pricing, offline over experience and services, while instant retail demands speed, fulfillment, and platform resources—no second growth curve has emerged yet.

With first-quarter net profit growth around 2%, Midea faces no easy channels for effortless wins or single-move breakthroughs.

This omnichannel war demands sustained effort from Midea.

-

![]()

Insta360’s Post-Lockup Period Begins: Employees Suspected of Selling Shares, Institutions Biding Their Time—Is a Major Storm on the Horizon?

-

![]()

Are Houses Getting 'ID Cards' Now? In the Future, House Decorating, Renting, and Buying Will All Be Possible with a Simple Scan!

-

![]()

Where Should the Senior Citizens in County Towns Go?

-

![]()

【OFweek Weike Cup】Santec Officially Enters for the 2026 Optical Industry Annual Innovation Product Award

-

![]()

Anhui’s Taihu County Establishes a Project with an Impressive Annual Production Capacity of 850 Million Square Meters of Optical Film, Along with Supporting Rollers!

-

![]()

The AI Unicorn Valued at 960 Billion is Raising Funds Again

-

![]()

Unveiling the Strategy: The RMB 11.5 Million Deal of MLOptics

-

![]()

Qingtian Lease Hits 7 Billion Valuation in Six Months, Coexistence of Robot Leasing Bubble and Reality