Overnight Vanishing Act: 1.8 Trillion Gone! Silicon Giants Are Splurging While Carbon-Based Consumers Are Priced Out

06/30 2026

06/30 2026

438

438

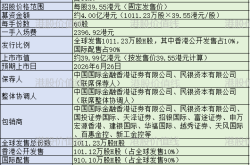

Apple's stock took a nosedive, plummeting by 6.2% in a single day, directly wiping out a staggering $263.4 billion in market value. Converted at the day's exchange rate, that's roughly 1.8 trillion yuan, marking the worst trading day of the year so far.

The catalyst was straightforward: Apple announced across-the-board price hikes for all Mac, iPad, and Vision Pro models. The culprit? Skyrocketing costs for upstream memory chips and advanced manufacturing processes, which even Apple can no longer shoulder alone.

The market's response was swift and unforgiving: Price increases are a surefire way to dampen sales, leading to a double whammy of lower volumes and prices, sparking an initial sell-off. Apple's supply chain partners, like Luxshare Precision, followed suit with steep declines, painting the market landscape in shades of green.

But Apple is merely the tip of the iceberg. What truly warrants closer examination is the taut rubber band lurking behind the scenes.

Upstream Feasts While Downstream Struggles Along the Same Supply Chain

A stark contrast emerged on the same fateful day.

While Apple's stock tumbled, memory chip behemoth Micron Technology soared by 16% in a single trading session.

On one side, sellers are reeling; on the other, suppliers are raking in massive profits. Upstream and downstream players on the same supply chain are navigating two vastly different realities.

The situation mirrors trends in the A-share and Hong Kong stock markets. A handful of leading stocks in computing power and semiconductors are enjoying an isolated bull run, while thousands of other stocks, regardless of their performance, are being collectively shunned by investors if they lack AI ties, leading to a relentless downturn.

The market has entirely shifted its focus away from profit statements, zeroing in solely on 'AI content.' This is the current K-shaped divergence in action.

The Truth Behind the Money Burn: Not for Profit, But for Survival

Many assume that the surge in tech stocks must equate to massive profits. This assumption is entirely misguided.

The driving force behind this rally isn't profitability but an arms race that shows no signs of slowing down.

In 2026, the capital expenditures of the five major cloud providers—Amazon, Microsoft, Google, Meta, and Oracle—on purchasing cards and constructing data centers are projected to reach a staggering $760 billion, marking a nearly 80% year-over-year increase.

What does $760 billion represent? It's roughly equivalent to the market value of two Apples, all invested within a single year.

These giants have no choice but to keep up. On the poker table of technology, not following suit means certain death. Whoever stops will lose their ticket to the AI era. Even if their large model businesses are still hemorrhaging money and cash flows are tight, they have no option but to continue funneling funds into NVIDIA and Micron's coffers.

This has created a self-sustaining loop that defies logic: The market spins a tale of 'eternal computing power shortage,' driving up stock prices. Giants raise funds at inflated valuations and then pour that money into hardware procurement. Upstream chip manufacturers receive a flood of orders, further validating the narrative that 'computing power is indeed scarce.'

In this loop, end consumers are nowhere to be seen.

A Computer Nearing 30,000 Yuan: Who Can Still Afford the Upgrade?

Now it's finally the turn of 'carbon-based consumers'—you and me—to take center stage.

Major memory manufacturers like Samsung and SK Hynix have shifted their most elite production capacity to manufacture HBM (high-bandwidth memory for AI). This has severely constrained the production capacity for DRAM and flash memory used in ordinary smartphones and computers. As a result, consumer chip prices have skyrocketed several times over in the past year.

These inflated costs are passed down the supply chain, ultimately slapping consumers with price hike notices.

Take the MacBook Pro, for instance. A configuration that once cost 20,000 yuan now costs 26,000 or even 30,000 yuan. A video-producing blogger who might have gritted their teeth and upgraded their productivity tools now simply closes the webpage and gives up.

That simple act of closing the webpage is the weakest link in this capital frenzy.

The infinite expansion of silicon-based computing power has finally hit the ceiling of carbon-based consumption.

At this point, some might argue: If consumer electronics aren't selling, won't that cause demand for memory chips to collapse? Can the story of chip price hikes continue?

Quite the opposite. This is where the most counterintuitive yet crucial cognitive dividing line lies.

Consumer electronics are no longer the primary battleground for memory chips. By 2026, server DRAM will account for over 50% of the market. It's estimated that 70% of globally produced DRAM chips will be consumed by data centers. HBM production capacity is already fully booked, with Micron only able to meet 50-60% of actual customer demand. NVIDIA has inked multi-year long-term agreements with SK Hynix, and North American cloud providers are willing to accept price hikes to secure supply.

In other words, selling a few tens of millions fewer smartphones has a negligible impact on overall memory chip demand. The production capacity freed up by consumer electronics is immediately snapped up by AI data centers. The chill in consumer demand won't reach chip factory floors anytime soon.

But that doesn't mean the story is risk-free.

The Real Problem Lies Not in Supply and Demand, But in Who Pays the Bill

Weak consumer electronics demand won't directly crash the chip market's prosperity, but it exposes a deeper risk: No link in the entire AI supply chain is currently supported by end-user payments.

That $760 billion in annual 'military spending' isn't profit earned by AI itself but financing raised through capital market valuation narratives. It's the liquidity generated by traditional industries, household savings, and real-world consumption that's fueling this silicon-based leap forward.

Weak consumer demand means the carbon-based real economy's ability to generate revenue is weakening. This is the true hidden danger: Once confidence in capital markets cracks, the entire financing loop could unravel.

This risk won't explode tomorrow. But the 1.8 trillion yuan evaporated by Apple is already a stark reminder—the market can ignore profit statements temporarily, but not indefinitely.

What Comes Next?

Apple's plunge isn't just a case of bad news being priced in; it's a signal worth heeding.

The supply-demand dynamics of memory chips won't be easily shaken by weak consumer electronics demand in the short term. But how this divergence resolves ultimately hinges on one thing: whether AI can truly land and start generating its own revenue.

Either AI applications genuinely penetrate the real economy, with large models and computing power services starting to generate tangible profits, using self-sufficiency to fill that $760 billion gap. This path leads to a truly closed-loop industry.

Or commercialization fails to materialize, capital market patience runs out, financing conditions tighten, and lofty computing power stocks lose their liquidity support. At that point, no amount of HBM shortage can resist the gravitational pull of valuation correction.

Epilogue

The market is currently engaged in a rather absurd act: frenziedly betting on the infinite future of silicon-based civilization while turning a deaf ear to the exhaustion of the carbon-based real economy.

It's true that the memory chip boom is currently backed by real, hard-currency orders in the short term. But no matter how powerful computing power becomes, it ultimately cannot escape the server racks. Its foundation lies in every ordinary person's wallet, in capital market confidence in the future, and in the real economy's patience for continued bloodletting.

The confidence of carbon-based consumption is the true upper limit of silicon-based expansion. Without concrete individuals, any technological revolution is just a string of money-burning code. Short-term survival may rely on financing, but long-term success must come from real payments. (Produced by Zitai)

-

![]()

Kunlunxin’s IPO: Baidu’s Strategic Move to Forge Alliances

-

![]()

AI Gives Volcano Engine a Chance to 'Change the Table'

-

![]()

AI Gives Volcano Engine a Chance to 'Change the Table'

-

![]()

A Smart Parking IPO Emerges in Xiamen with a 204% Surge on the First Day of Listing

-

![]()

Alibaba Exits Gaming Industry: A Strategic Move Forward?

-

![]()

New Car Model Faces Unprecedented Negative Campaign; Leapmotor Navigates Through Challenges Amid Profitability Concerns

-

![]()

Overnight Vanishing Act: 1.8 Trillion Gone! Silicon Giants Are Splurging While Carbon-Based Consumers Are Priced Out

-

![]()

2026 China GEO Industry Application Scenario Maturity and Supplier Selection Analysis Report (Part 1)