Kunlunxin’s IPO: Baidu’s Strategic Move to Forge Alliances

06/30 2026

06/30 2026

517

517

When You Can’t Outspend, Partner Strategically

Kunlunxin’s IPO journey has reached a significant milestone.

On June 29, Reuters confirmed that Kunlunxin, Baidu’s AI chip subsidiary, is advancing plans for a dual listing in Hong Kong and the United States, targeting a valuation of approximately $50 billion—40% higher than Baidu’s current $36 billion market capitalization.

More intriguingly, The Information reported that industrial investors interested in the IPO are required to purchase chips in multiples of their intended equity subscription. Caijing Magazine cited sources stating that investors must buy Kunlunxin’s products to secure shares: “To acquire a $10 million stake, you need to purchase $70 million worth of chips.”

At first glance, this arrangement seems unconventional. In a typical IPO, companies exchange equity for investor capital, and under reasonable valuations, most IPO-bound firms actively seek industrial capital participation. However, Kunlunxin appears to have added another layer: If you want to be a shareholder, you must first prove you’re also a customer.

This design suggests that Baidu isn’t merely selling chips; it’s using the IPO to screen industry allies genuinely willing to bet on Kunlunxin’s future.

01 Kunlunxin’s Triple-Win Strategy

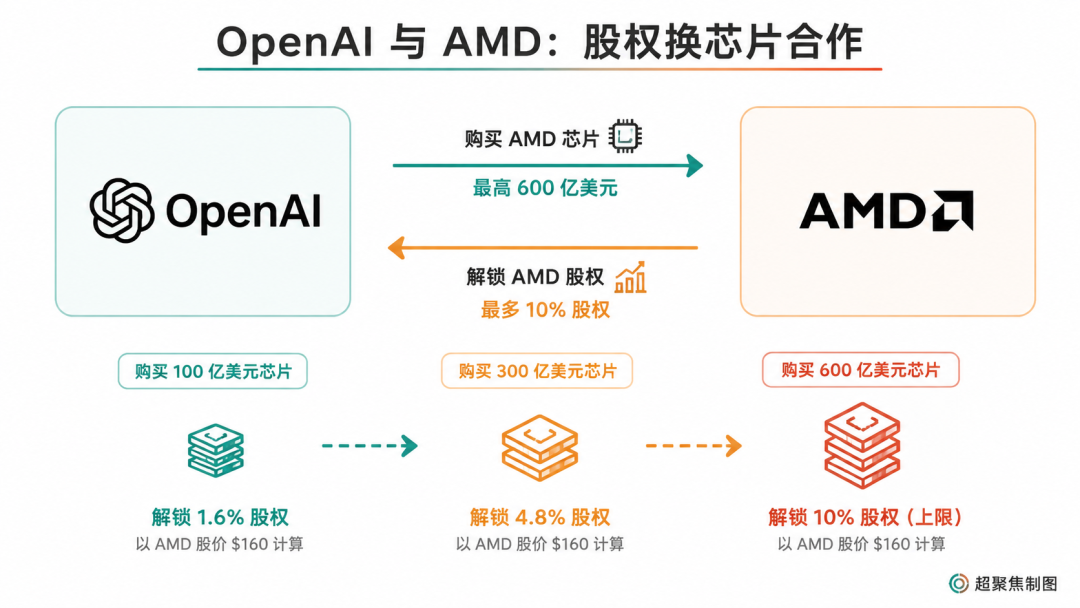

Kunlunxin’s requirement for investors to purchase chips at 3–7 times the subscription price echoes AMD’s 2025 strategic partnership with OpenAI.

In October 2025, AMD and OpenAI announced a landmark deal. OpenAI committed to deploying up to 6GW of AMD GPUs, while AMD granted OpenAI warrants for up to 160 million common shares. If deployment and stock price targets were met, OpenAI could acquire up to 10% of AMD’s equity—effectively achieving zero-cost AI chips.

This setup is clever. On the surface, AMD sells chips to OpenAI, but in reality, AMD uses equity to tightly bind OpenAI—a super-client—to its supply chain.

For AMD, OpenAI’s orders guarantee demand, revenue, and endorsement from one of the world’s most critical AI customers, diversifying beyond NVIDIA.

For OpenAI, this isn’t just about buying GPUs. Solely purchasing NVIDIA’s AI chips would funnel all profits to NVIDIA. By buying AMD’s GPUs while acquiring AMD equity, OpenAI can pressure NVIDIA on pricing while benefiting from supplier value growth—even if that growth is self-driven.

Baidu’s approach follows a similar logic.

For Kunlunxin, the IPO requirement transforms its identity. As a Baidu-incubated chip company, no matter how impressive its technology or plans, outsiders perceive it as an internal asset within Baidu’s AI ecosystem. However, if domestic CSP clients like Tencent and ByteDance formally adopt its chips, Kunlunxin becomes a verified, externally recognized AI chip company.

Thus, Kunlunxin doesn’t need financial investors like Hillhouse or Sequoia; it needs industrial clients bringing data center, model, scenario, and adaptation demands. Moreover, orders worth 3–7 times the subscription value aren’t trivial—they could secure Kunlunxin’s performance for three to five years post-IPO.

For Tencent, ByteDance, and other tech giants without in-house chips, a domestically advanced company willing to cede equity at such “low” prices is a dream scenario.

Why does ByteDance support Cambricon? Why does Alibaba develop its own PPUs? Price and business adaptability are key considerations.

Price is straightforward: AI chips are a high-margin industry. Long-term purchasers like Alibaba, Tencent, and ByteDance continuously feed profits to suppliers. For these giants, AI isn’t a one-off project but a cost center consuming ongoing compute resources. No matter how profitable their e-commerce, social, or entertainment businesses are, they still want to “eliminate” suppliers.

However, constrained by technical capabilities, only Alibaba has successfully built its own path and gained the confidence to “reject” Huawei’s Ascend chips. Tencent and ByteDance face different circumstances. More suppliers mean stronger bargaining power to lower prices. Moreover, if they truly invest in Kunlunxin, their AI chip expenditures could transform into investment gains on financial statements.

Adaptability matters even more because AI chips aren’t plug-and-play.

Models, frameworks, operators, software stacks, cluster stability, and inference efficiency all require fine-tuning. Domestic giants have vastly different business scenarios: ByteDance focuses on recommendations and content distribution, while Tencent operates social, gaming, advertising, and cloud services. They need not just generic chip specs but compute solutions that integrate into their businesses.

To address this, they could either rely on CUDA or exclusively support startups like ByteDance does with Cambricon.

But Baidu suddenly offers: “You don’t need to build chips from scratch or settle for simple procurement. Buy Kunlunxin’s AI chips, and we’ll become shareholders together.” For CSPs like Tencent and ByteDance, this is transformative. Equity becomes a rope tying procurement, adaptation, and long-term gains together—a soft pillow for sleepy CSPs.

Ultimately, Baidu may benefit the most.

For Baidu, Kunlunxin’s IPO isn’t just about raising funds; it’s a revaluation. As mentioned, Kunlunxin’s valuation could reach $50 billion, exceeding Baidu’s current $36 billion market cap. This means a spun-off AI chip asset targets a valuation higher than its parent company—a rare opportunity for any tech giant.

More importantly, if leading internet firms join, Baidu will truly align with them. Currently, Baidu holds ~58% of Kunlunxin, expected to remain above 40% post-IPO.

If successful, Baidu won’t just sell Kunlunxin; it will equip this AI giant with a newer, stronger engine while retaining control.

02 Baidu’s AI Strategy: An Hourglass Approach

While infrastructure advances rapidly, AI access points are reshuffling and contracting.

On June 25, Baidu merged its ERNIE Bot web version, ERNIE APP web version, and Baidu ERNIE Assistant web version into a unified Baidu ERNIE Assistant web platform, ending its multi-brand era for web-based AI assistants.

However, this move feels less like a prelude to a stronger offensive and more like organizing scattered battlefield equipment.

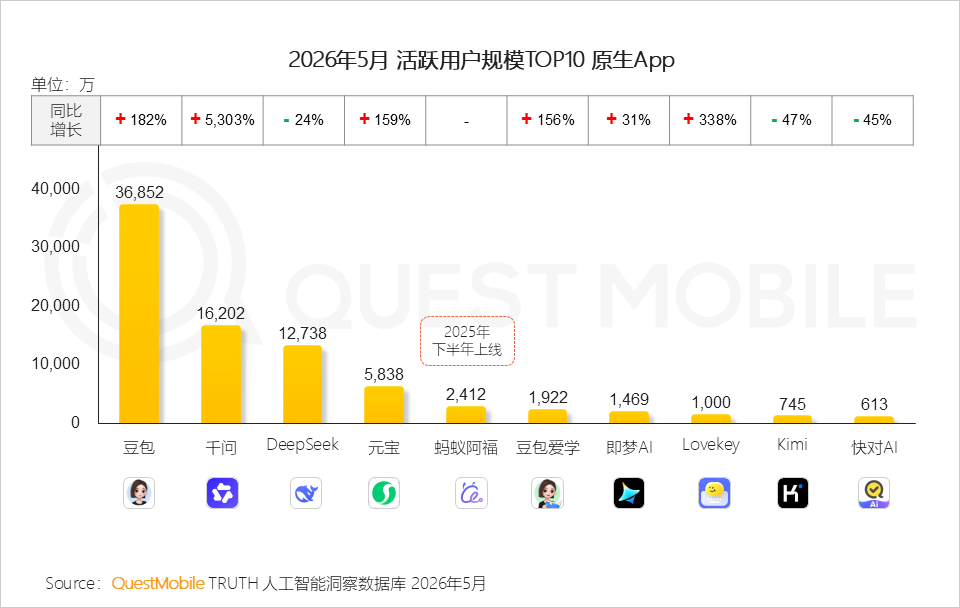

According to QuestMobile, as of May 2026, among the top 10 native AI apps by active users, Doubao led with 369 million monthly actives, followed by Qianwen (162 million) and DeepSeek (127 million). Tencent Yuanbao had 58.38 million monthly actives. Notably, Baidu ERNIE has been absent from this list for some time.

This suggests that Baidu’s ChatGPT rival has temporarily exited the stage.

However, Baidu seems to have anticipated this. ERNIE is no longer the sole protagonist in Baidu’s AI narrative:

Early this year, Baidu reorganized its Document and Cloud Drive divisions into a new Personal Super-Intelligence Business Group, reporting directly to Robin Li. In March, He Jingzhou, former head of large model algorithms, rotated to the Mobile Ecosystem Business Group to deepen integration of large models with search and recommendation services. In May, Baidu established a Model Committee to oversee foundational and applied model R&D. In June, the Digital Human Innovation Business Department upgraded to an independent unit from the existing commercial framework.

These moves, though fragmented, point to a unified strategic focus: embedding AI capabilities across Baidu’s business foundations rather than relying on a single unified access point to compete.

This strategic adjustment is already reflected in Kunlunxin’s collaboration. It’s challenging for a company to fiercely compete with all giants at AI access points while selling chips to them and expecting them to become shareholders and customers.

This is the subtlety of Baidu’s current AI strategy.

Baidu hasn’t abandoned applications, nor has it reduced itself to infrastructure alone. Instead, it’s adopting a more pragmatic hourglass structure: At the bottom lie Kunlunxin, intelligent cloud, models, and compute infrastructure; at the top sit specific businesses like Document, Cloud Drive, search, digital humans, and autonomous driving. The middle—the crowded, costly, and vulnerable general-purpose Chatbot access point—has intentionally contracted.

This may seem like a compromise, but it’s more of a strategic trade-off: If you can’t dominate access points, don’t just fight there. If application layers can’t support aggressive expansion, integrate AI into existing businesses. If infrastructure offers advantages, make it an indispensable supply chain link for others.

In other words, Baidu no longer tries to win everywhere but doubles down on areas with its deepest moats.

Fortunately, after fifteen years of development, Kunlunxin now empowers Baidu to stand tall and choose its allies wisely.

- END -

-

![]()

Luxury Lineup, Highly Anticipated! The Pioneer of Physical AI Gears Up for Hong Kong Stock Exchange Debut!

-

![]()

Mercedes-Benz Withholds Year-End Bonuses for 90,000 Staff: Germany's Industry 4.0 Aspirations in Tatters

-

![]()

Can the Hong Kong Stock Market Pay for World Models? Dissecting Momenta's Prospectus

-

![]()

Set for Secondary Listing in Hong Kong with Market Cap Exceeding 500 Billion: How Luxshare Precision Regains Investor Trust?

-

![]()

Approaching its Secondary Listing in Hong Kong with a Market Cap Exceeding 500 Billion: How Has Luxshare Precision Regained Investor Trust?

-

![]()

Real Insights from New Energy Vehicle Owners in China’s Top 30 Cities by Ownership

-

![]()

Real Thoughts of New Energy Vehicle Owners in Top 30 Cities by Car Ownership

-

![]()

Truth Revealed: Memory Prices Soar, Apple Profits Surge, Yet Memory Makers Bear the Blame