? Let's talk about Baidu's latest AI advancements and its concerns

08/29 2024

08/29 2024

525

525

Baidu's challenges in AI reveal the common issues faced by the internet industry during the AI transformation.

Author: Lu Yao

As a company renowned for its engineering culture, Baidu's recent AI initiatives have been remarkable. From Wenxin Yiyan to the opening of Wenxin Large Model 4.0, Baidu has demonstrated a stronger willingness for all-in AI transformation than any other company, with almost all its products undergoing AI reshaping or optimized iteration.

However, in terms of market value, Baidu's performance seems to have fallen short of expectations.

We previously pointed out that over the past decade, Baidu has invested over RMB 100 billion in research and development, spanning AI, autonomous driving, and large models. The difficulties in converting these technologies into practical benefits may be related to factors such as the market's acceptance of AI technology, user adoption, and the competitive landscape.

Yet, from the current development perspective, Baidu's direction is not misguided. One thing is certain: the future belongs to AI.

Robin Li also noted in a 2021 speech that China is entering a golden decade for AI, and that the application threshold for AI technology will significantly decrease in the coming decade. Furthermore, he later mentioned that as the application threshold for AI technology continues to drop, developers and creators will have more opportunities.

To align with this trend, Baidu vigorously promotes its PaddlePaddle platform, aiming to lower the barrier to AI development and application by simplifying development processes and providing easy-to-use tools. Similarly, Tencent Cloud's Hai and Huawei's Ascend AI full-stack software platform are also aimed at facilitating AI application development. Additionally, generative AI tools like ByteDance's Coze and its domestic version aim to reduce the development threshold for AI applications based on large models.

Looking at the AI industry chain over the past two years, it becomes evident that chip companies controlling software ecosystems remain the most profitable segment, exemplified by NVIDIA with its high-performance GPUs. Driven by ChatGPT, the large model sector has attracted the most funding, with MiniMax valued at over USD 2.5 billion and Li Kaifu's AI startup 01 Life receiving hundreds of millions of dollars in funding, with some companies reaching valuations of over USD 10 billion.

Speculative booms in the tech sector are common, but it's intriguing that AI application fields, which hold great promise, have not attracted as much funding. Most AI application vendors have raised less than USD 100 million. Many investors also point out that as the market cools down, securing funding for AI projects, compared to large models or even early mobile internet startups, has become significantly more challenging.

This is primarily due to low market expectations for these companies. There are indeed few truly successful AI applications, and user growth rates are generally modest, making it difficult to find benchmarks. Companies developing products face a vastly different competitive environment from the past, where it's hard to find a niche without major players, making the landscape more treacherous for startups.

Especially after the significant withdrawal of US dollar funds, RMB funds have restrictions and preferences. In China, the value created by high-tech products like AI, compared to manufacturing and retail, is still relatively insignificant. Coupled with the rare wave of IPO withdrawals in the A-share market this year, investors have become even more cautious.

Under these circumstances, startups that rely on AI products and can satisfy the market with revenue and profits, or even complete an IPO, are virtually non-existent. As a result, some internet companies are pushing their large models, while large model companies are promoting their applications. However, due to the lack of convincing value metrics in the market, these secondary market giants find it challenging to revive their market values through AI applications.

Baidu is a prime example of this. Before the launch of Wenxin Yiyan, ChatGPT posed more of a threat to Baidu, fueled by predictions that AI search could replace traditional search.

AI search can more accurately understand users' query intent, eliminating the need to browse multiple links to find relevant information, thereby enhancing search efficiency and accuracy. Nevertheless, traditional search is not without merit. For specific keywords, it can provide more appropriate answers based on relevance and click-through rates.

In other words, the real threat to Baidu is not that AI has changed search. Baidu's turning point occurred during the mobile internet era, when traditional information distribution platforms and pay-per-click advertising were replaced by more personalized, interest-driven algorithms. Baidu missed the opportunity to maintain its user ecosystem on mobile devices, with its search share diverted by platforms like Douyin, WeChat, and Xiaohongshu that cater to different scenarios and needs.

Today, amidst the AI boom, the mission at the application layer is even more daunting and complex for Baidu. While it may not fully realize Robin Li's vision of "Box Computing," this is indeed an opportunity to rebuild business barriers.

The resurgence of Google and Microsoft in the AI era is closely tied to their strategies. Google focuses on strategic acquisitions and venture capital investments to strengthen its technological advantages and supports AI startups through cloud services. Microsoft, on the other hand, accelerates its AI technology breakthroughs and builds a robust AI ecosystem through large-scale investments and collaborative development.

In China, the dynamics of the large model market have shifted. Similar to selling shovels, chip computing power remains a rigid demand, commanding higher prices due to scarcity. However, domestic large models supporting AI applications are facing intense competition, with many enterprises still in a "shell" state, diluting their appeal.

Faced with this situation, most companies have three paths to follow: develop several C-end or B-end applications as an effective short-term solution to address the challenges of AI implementation; build their own ecosystem and incubate AI applications as investors; and focus on continuous research and development in deep learning, natural language processing, and computer vision, driving growth through technological innovation.

The pendulum of development swings both ways. These large model companies, led by Baidu, are gradually sinking into a technological quagmire due to unclear market demands and ambiguous commercialization paths.

The 'competition' among base models refers to the relentless pursuit of algorithmic, model accuracy, and performance improvements, leading to significant resource consumption and cost increases.

In generative AI applications, despite Robin Li's call for entrepreneurs to compete in AI application development, practical implementation still faces issues like high costs, large model delusions, and low user retention rates. For instance, this year's 'price war' among large models significantly reduced API call costs, but these costs are still over ten times higher than those of traditional keyword searches.

A research report by Sequoia Capital notes that while AI infrastructure investments are substantial, the actual returns generated thus far have fallen far short of expectations. There is a significant gap between the expected revenue and actual growth in the AI industry, with this 'black hole' expanding from USD 125 billion in 2023 to USD 600 billion.

Globally, AI's actual financial returns for enterprises also fall short of expectations. Microsoft performed strongly, with its Intelligent Cloud revenue growing 20% year-over-year in Q4 last year, but its overall performance missed expectations due to AI investments. In contrast, while Google saw growth in advertising revenue, significant increases in capital expenditures and underwhelming AI development led to market value fluctuations.

Undoubtedly, compared to the previous cloud computing boom, AI still holds many unknowns.

Over the past few years, a relatively comprehensive ecosystem has been established based on cloud computing, involving close collaboration among cloud service providers, software developers, integrators, and others to promote the adoption of cloud services. Cloud computing has transformed traditional software delivery models, offering more imaginative business models like SaaS, PaaS, and IaaS.

Furthermore, when discussing the transition from IBM to Salesforce and SaaS as a significant business model transformation, it's well-known that as technology advances and the market evolves, traditional databases and software face challenges like high costs, complex deployment, and difficult maintenance. Companies like Salesforce enable users to access services over the internet on a pay-as-you-go basis, revolutionizing both technology and business models to drive industry innovation and competition. Notably, AI has yet to demonstrate such transformative power.

Existing AI applications are primarily concentrated in three areas: Copilot (productivity tools), Creativity (creative assistance), and Companionship (emotional companionship). Media research into pricing strategies for dozens of AI application products reveals that AI functionality commercialization mainly involves charging directly for AI features, increasing product prices, or integrating AI features into existing bundles without price changes.

The survey found that most current AI features are incorporated into existing software packages as added value, with companies like Notion, Microsoft, and Airtable offering AI capabilities at an additional cost.

Other models involve packaging AI products into subscription bundles, with a minority adopting a hybrid pricing model combining subscription fees and pay-per-use charges. For example, the AI avatar app Talkie, which recently gained popularity, has generated nearly USD 830,000 in cumulative downloads and revenue since its launch last year, with revenues derived from subscriptions, in-app purchases, and advertising.

Currently, whether as additional features or standalone AI products, none have broken through existing business models to create new revenue streams.

Pricing AI products is a complex task, with the key being accurately measuring the practical value of features to entice users to pay. This determines whether AI applications, primarily based on SaaS subscriptions, can overcome the historical challenge of software "payment resistance" in China. Optimistically, if achieved, this would represent a significant breakthrough.

Returning to Baidu, unfortunately, a comparison of market values reveals that while companies like Google and Microsoft have reached peak valuations amidst the AI large model trend over the past year, even with some declines, they remain at high levels. In contrast, domestic internet giants like Baidu and Alibaba have not experienced similar changes, remaining at prolonged lows.

The reasons behind this are undoubtedly complex, encompassing market size, internationalization, technological innovation and R&D investment, fierce domestic competition, regulatory policies and compliance requirements, investor confidence, and market expectations. These challenges pose acute difficulties for Baidu.

This article is originally written by Xinmou

-

![]()

Domestic Pioneer: Changjin Photonics, First Listed Company Focused on Special Optical Fibers, Soars Over 15-Fold on STAR Market Debut

-

![]()

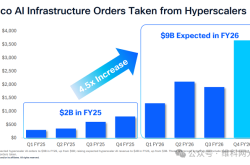

Single-Quarter Orders Break $1 Billion Barrier! Cisco’s Acacia Surfs the AI Boom

-

![]()

Consistently Propelling Technological Progress: Qualcomm’s Xu Hao Elucidates How 6G Trial Frequencies Can Optimize the Balance Between Coverage and Bandwidth

-

![]()

Liushenyu Mine Disaster Drives Industrial Innovation: Pioneering a New Era of Intelligent Mine Safety with Integrated Air-Ground Systems

-

![]()

Ant Group CEO Han Xinyi's Latest Speech: The Emergence of 'Trust Logic' in the AI Era

-

![]()

Demystifying the Rankings: Do High Scores in Robotics Competitions Equate to Real-world Implementation Strength?

-

![]()

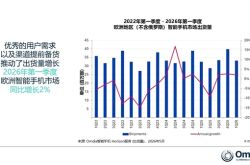

Europe's Q1 Smartphone Market Shipments Revealed: Samsung Holds Firm at First Place, Honor Surges Over 60%

-

![]()

Mixed Fortunes: The Ongoing Transformation of the Automotive Industry's Value Landscape