Has the new order not yet formed, and will the “price war” for new energy vehicles never end?

09/14 2024

09/14 2024

610

610

After the start of the “golden September and silver October”, will the domestic auto racing scene become more intense, or will the battles gradually die down?

The answer leans more towards the former. On the evening of September 9, BYD officially launched the 2025 Han DM-i, equipped with the all-new fifth-generation DM technology, as well as the Han EV model. This time, BYD continues to offer more features at a lower price.

Official information shows that although the 2025 Han has undergone upgrades in multiple core technologies such as design, performance, technical configuration, and intelligence, with both versions equipped with the Dynasty Network's first “Eye of Heaven” advanced intelligent driving assistance system, the price is lower than the current Han Glory Edition model.

Specifically, the starting price of the DM-i version is 4,000 yuan cheaper than the Glory Edition; while the EV version offers a maximum discount of up to 14,000 yuan compared to the Glory Edition.

As a true “king of competition” in the new energy vehicle sector, BYD has not stopped its competitive strategy in terms of model upgrade iteration speed and price advantage. Its competitors are also following suit, collectively entering an era of high cost-effectiveness.

In today's automotive market, “low prices” have become a normalized phenomenon. This is not necessarily a bad thing.

As prices drop, automakers seek new “blue oceans”

In July this year, domestic new energy passenger vehicles surpassed the market share of gasoline-powered vehicles for the first time, with a penetration rate climbing to 53.5%.

At the same time, according to the China Association of Automobile Manufacturers, the total sales target for China's new energy vehicles for the full year is expected to reach 11.5 million units, representing a year-on-year increase of over 21% compared to the actual sales of 9.495 million units in 2023. However, compared to the past four years' compound annual growth rate of 61%, the growth rate has slowed significantly.

When the penetration rate reaches a certain level, the growth rate on the demand side slows down significantly, and the bonus protection period gradually disappears. “Trading volume for price” becomes the most direct competition means for automakers.

At the beginning of 2023, Tesla took the initiative to announce price reductions of up to 36,000 yuan for its main models. During this period, the slogan “same price for gasoline and electric vehicles” was prominent. This then ignited a price war among vehicles and automakers priced above 200,000 yuan, with both new and traditional automakers such as NIO, XPeng, Li Auto, BMW, Mercedes-Benz, Audi, and BYD announcing follow-up price reductions.

Amid the “blades and swords,” the “price war” in new energy vehicles lasted throughout 2023 and intensified in 2024.

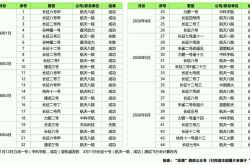

According to the China Passenger Car Association (CPCA), in the first eight months of this year alone, 173 models in the domestic market saw price reductions, exceeding 90% of the total number of price reductions for the entire year of 2023 and also surpassing the combined total of price reductions by brands before 2022. Among them, pure electric vehicles saw a larger average price reduction of 15%, while gasoline-powered vehicles saw an average reduction of 11%.

However, the difference is that this time, BYD's initiative has greatly increased.

First, after the Lunar New Year, BYD directly unveiled the “winning combination” of the 79,800 yuan Qin PLUS DM-i and the Destroyer 05 Glory Editions. Following this announcement, automakers such as Nezha, Changan Qiyuan, Wuling, and others quickly followed suit in the price range below 100,000 yuan. Models such as the Wuling Starlight PLUS, Changan Qiyuan A05, Q05, and Beijing Hyundai Elantra directly reduced their guide prices.

It is important to note that most of these vehicles are A-segment models. According to the past distribution of prices and sales volumes for traditional gasoline-powered vehicles, the 80,000-150,000 yuan price range, dominated by A-segment models, has always been the most concentrated sales segment, with a large scale.

In recent years, the share of gasoline-powered vehicles in the domestic A-segment market has been rapidly declining, falling from 97% in 2018 to 77% in 2023, while new energy vehicles have increased from 3% in 2018 to 23%. However, there is still significant room for growth.

According to China Business Network, while the new energy penetration rate in the A00-segment market reached 100%, it was only 31% in the A-segment market in the first seven months of this year, with the A0, B, and C segments reaching 61%, 46%, and 39%, respectively.

With lithium-ion battery costs continuing to decline and hit new lows in 2024, it is the perfect time for new energy automakers to enter the A-segment market. After entering the third quarter, automakers such as Chery, Wuling Starlight, and Geely's Geometry brand have again launched new A-segment new energy models. XPeng's newly launched MONA M03 is also targeting this niche segment, reportedly receiving over 30,000 orders within just 48 hours of its launch.

Moreover, competing in the 100,000 yuan price range is also a clever way to attract traffic. The A-segment market is becoming a blue ocean for automaker competition.

Secondly, the 150,000-200,000 yuan price range is a key focus for many automakers. The most typical example in this range remains BYD. From launching nearly a dozen Dynasty and Ocean Network Glory Edition models such as the Dolphin, Seal DM-i, and Han family in the first quarter, to recently unveiling the all-new 2025 Han DM-i and Han EV, these models are concentrated in this price range.

Apart from directly announcing price reductions, even new-energy automakers that have traditionally focused on the mid-to-high-end segment, such as NIO, have initiated a “dimensionality reduction” market strategy under significant performance pressure. They have launched the Ledao sub-brand with a broader audience and are about to introduce the Firefly, a third brand targeting an even lower price segment.

According to the China Association of Automobile Manufacturers, cumulative sales in the 150,000-200,000 yuan price range in the domestic market from January to August continued to lead the entire market, reaching 1.899 million units, a year-on-year increase of 16.1%. This is in line with the current per capita consumption capacity in China.

In the 100,000-500,000 yuan range, automakers' “price as a spear” strategy

Looking back at the turbulent journey of the new energy vehicle sector over the past nine months, we can see that competition in the new energy vehicle market over the past two years has been more about seizing the opportunity to rebuild the new order in the domestic and global automotive markets amidst the transition from old to new technologies and from gasoline-powered to new energy vehicles.

Against this backdrop, automakers have adopted a seemingly normalized low-price strategy.

Of course, for domestic automakers, using “price” as a spear to rebuild the new order requires certain opportunities.

Opportunity 1: The top-down full-chain scale effect begins to coalesce, releasing significant cost reduction and efficiency enhancement capabilities.

In 2023, BYD was still promoting the slogan “same price for gasoline and electric vehicles.” However, just a year later, it shifted to the slogan “electric cheaper than gasoline.” There are many key factors behind this change, such as the recent drop in battery-grade lithium carbonate prices from a peak of 600,000 yuan per ton due to a severe imbalance between supply and demand to the current level of 75,500 yuan per ton.

According to China Energy News, the current power battery accounts for about 40% of the total vehicle cost, while the cathode material also accounts for about 40% of the battery cost. The decline in lithium resource prices has paved the way for significant cost reductions in complete vehicles.

Based on this background, some automakers that have already built up their scale advantages have quickly and proactively adopted pricing strategies to seize market share in the lower penetration A-segment models and the 100,000-200,000 yuan price range, while continuously expanding their brand influence and attempting to squeeze out competitors with more extreme scale effects.

As one of the earliest domestic independent new energy brands, BYD employs a vertically integrated business model, with self-developed and produced batteries, motors, and even many chips, giving it significant advantages across the entire industry chain and making it easier to profit from scale effects.

BYD's financial reports are the best testament to these scale effects. In 2023, BYD set a new record for annual auto sales in China and became the first Chinese automaker to enter the top 10 in global sales, as well as the global leader in new energy vehicle sales. In the first half of 2024, when BYD further proactively attacked the market, it continued to achieve significant growth in performance, with the gross margin of its automotive business increasing by 3.27 percentage points.

Clearly, the coalescence of the full-chain scale effect has contributed to some companies' cost control capabilities. This is the core underpinning of the “price war” at the product level.

Opportunity 2 lies in the demand side. Although the market share of new products and stages shifts from the 0-1 phase to the 1-N growth phase, and the industrial driving force shifts from policy orientation to market orientation, it does not mean that policy support should completely withdraw.

As an industry with significant price elasticity and obvious replacement cycles, in the current consumer environment, tax exemptions, continuous trade-in incentives, and support policies are essential drivers for new energy vehicles to accelerate their penetration into the gasoline-powered vehicle market.

Therefore, when the mid-August “golden September and silver October” auto sales season approached, the Ministry of Commerce once again announced new auto trade-in incentives, undoubtedly providing another boost to automakers. In 2023, China had about 110 million passenger vehicles in the core replacement peak period, and this year, it is predicted that 40% of the incremental demand for passenger vehicles will come from trade-ins. Based on last year's sales of 26 million vehicles, about 10 million passenger vehicle sales this year are expected to come from trade-ins.

Driven by a series of internal and external factors in the industry, the market share of domestic new energy vehicles first exceeded the critical 50% threshold in July. This is actually a watershed moment, and signs of a new order in the entire industry may already be emerging.

At this point, it is crucial for automakers to “know themselves” and understand that what they should be “competing” on is not price, but differentiation, building barriers that drive out inferior products through differentiation.

Conclusion

2024 is a crucial year for new energy automakers to establish a firm foothold, and they are bound to face fiercer competition. Almost nine months have passed, and some new energy enterprises are already well-prepared. The only thing to note is that during this process, the “degree” of competition is crucial:

Simply using price reductions as a means of competing with rivals can easily become habitual, leading to deviations from a healthy competitive order. It is important to remember that simply competing to lower prices indefinitely is a dead end; instead, the path to growth and success lies in elevating brand value, quality, and experience.

Source: Songguo Finance

-

![]()

Prayer for Success, Yet China's Space Industry Must Look Beyond Mere Success

-

![]()

Can Intelligent Driving Talents Adapt to Embodied AI? A Dimensionality Reduction or a Cultural Shock?

-

![]()

Final Assessment: Unveiling the Causes of the Sluggish Domestic Auto Market in the First Half of the Year

-

![]()

Buying a Crippled FSD for 100,000 Yuan! Musk Struggles to Quell Consumer Anger, Are New Energy Vehicles 'Outdated as Soon as They Hit the Road'?

-

![]()

Over €1.15 Billion Spent, No Mass Production in Four Years! The Volkswagen-Bosch Partnership Falters, While the Chinese Market Quietly Flourishes

-

![]()

AI Carnival: Who Will Foot the Bill?

-

![]()

Who Will Foot the Bill for the AI Craze?

-

![]()

Midea’s Air Conditioners Fly Off Shelves in Europe, Boosting He Xiangjian’s 200 Billion Yuan Fortune