Smartphones Enter the Knockout Stage in 2026

02/27 2026

02/27 2026

528

528

Source | Bohu Finance (bohuFN)

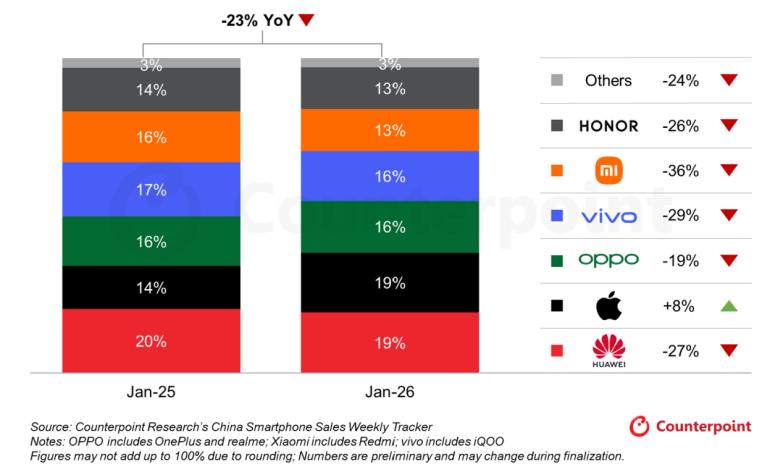

Not long ago, Counterpoint Research released a report on China's weekly smartphone sales, and the data wasn't pretty. In January this year, smartphone sales in China fell by 23% year-on-year, with most domestic brands experiencing double-digit declines. Only Apple maintained positive year-on-year growth.

This unusual decline, of course, has special reasons. Last January coincided with the Spring Festival promotional period overlapping with national subsidies, which pulled demand forward and created a high base. This year, the Lunar New Year fell at a different time, and the subsidies were less generous than last year, leading to a noticeable decline in market performance for domestic smartphone makers.

But beyond that, there's a clear difference between Apple and its peers—price. Due to pricing, most Apple models were not eligible for subsidies and were thus less affected.

Besides the fading subsidies, mid-to-low-end smartphones face an even bigger challenge—the historic price hike of memory chips. The surge in AI demand hasn't just driven up stock prices for companies like Zhipu and MINIMAX or made U.S. gas turbines scarce—it's also drained memory manufacturers' capacity. Consumer-grade memory sticks have been sidelined, causing headaches for smartphone makers.

Transsion, the “King of African Smartphones,” saw revenue growth without profit growth in the third quarter of last year, with its gross margin dropping by two percentage points. According to supply chain sources, multiple smartphone brands have reduced their 2026 device orders by 10%-20%. There are also reports that Meizu's smartphone business has effectively halted, and the planned Meizu 23 release for 2026 is no longer moving forward.

Will 2026 be a year of shakeout for smartphones?

01 The Persistent Challenge of Moving Upmarket

The push by domestic smartphone brands toward the high-end market is a long-standing issue.

According to Counterpoint, 2017 marked a turning point for smartphone shipments. Before 2017, global smartphone shipments were on the rise. From 2017 to 2020, shipments began to decline slightly, hitting a decade-low in 2023.

With market growth capped, consumer demand for upgrades is undergoing two key changes.

First, replacement cycles are lengthening. In 2020, the average replacement cycle for Chinese consumers was 24–25 months, but by 2025, it had stretched to 33–38 months.

Second, consumers are continuously upgrading to higher-priced models. Year-end holiday promotions, installment financing, and trade-in programs have all fueled the trend toward premium smartphones.

From the latest market data, growth continues to be driven by “value expansion” rather than “scale expansion.” Counterpoint shows that in Q4 2025, global smartphone market revenue grew 13% year-on-year to $143 billion, a new single-quarter record. Meanwhile, the average selling price (ASP) rose 8%, surpassing $400 for the first time in a single quarter.

IDC forecasts that by 2026, smartphones priced above $600 will account for 35.9% of China's market, up 5.4 percentage points year-on-year. Models priced between $400–$600 will make up 10.1%, down 0.8 points; $200–$400 models will account for 34.0%, down 0.3 points; and under-$200 models will shrink by 4.3 points to 20.0%.

The high-end market is no longer optional.

Although Huawei slid from the top two under U.S. sanctions in 2020, leaving room for other domestic players, most have yet to make significant progress in the premium segment.

Data shared by Weibo blogger RD Observation shows that in 2025, 56% of Huawei's sales were from models priced above 4,000 yuan, compared to just 20.5% for Xiaomi, 18.5% for Vivo, and 13% for OPPO.

Looking at recent flagship series sales, by the sixth week of 2026, Apple, Huawei, Xiaomi, Vivo, and OPPO had sold approximately 20.9327 million, 3.1105 million, 3.5046 million, 1.4544 million, and 1.1677 million units, respectively. While Xiaomi outsold Huawei, its flagship series was released earlier, and Huawei's weekly sales outperformed Xiaomi's.

The progress in premiumization also gave Huawei and Apple more flexibility during the Spring Festival promotions.

Huawei's Lunar New Year sale covered its entire product range, with the Mate 70 Pro+ (originally priced at 8,499 yuan) seeing discounts of up to 2,700 yuan. Apple offered a 2,000 yuan discount on the poorly selling iPhone Air, which, combined with national subsidies, brought the total discount to 2,900 yuan. Other domestic brands, however, did not offer impactful promotions during the holiday.

While the success of others is disheartening, what worries other smartphone brands even more is the memory supercycle.

02 The Smartphone Kill Zone

Since the second half of last year, it hasn't just been AI and gold going wild—memory has too.

TrendForce data shows that in Q1 2026, general-purpose DRAM contract prices will rise 55%–60% quarter-on-quarter, while NAND flash will increase 33%–38%. When combined with previous quarters' gains, memory prices have entered a “supercycle,” with increase even surpassing the 2018 peak.

How dramatic is this price surge?

A clear example is server-grade 64GB RDIMM memory: around $255 in Q3 2025, it jumped to $450 in Q4. According to multiple authoritative sources, contract prices have now surpassed $900, with widespread expectations of hitting $1,000 in Q2 2026. This surge is also being driven by AI.

Faced with such profit margins, suppliers didn't hesitate.

The three major memory makers—Samsung, SK Hynix, and Micron—are significantly cutting consumer-grade DDR4 and DDR5 production to prioritize HBM and server memory. As a result, consumer-grade memory supply has collapsed, driving prices sharply higher. How severe is the supply crunch? SK Hynix stated in October last year that its 2026 production capacity for DRAM, NAND Flash, and HBM was fully booked, with Samsung and Micron's HBM capacity also sold out.

To make matters worse, this price surge is unlikely to ease anytime soon. Counterpoint expects memory prices to spike 40%–50% in Q4 2025, another 40%–50% in Q1 2026, and around 20% more in Q2 2026.

This means Apple's “golden memory,” which was once a running joke, is now literally gold.

In 2020, memory accounted for about 8% of the iPhone 12 Pro Max's bill of materials (BoM). By 2025, it made up over 10% of the iPhone 17 Pro Max's BoM.

According to UBS estimates, by Q4 last year, memory could account for up to 34% of the BoM for mid-to-low-end smartphones, up from just 22% in 2024. This translates to a roughly $16 increase in per-unit cost, a nearly 37% jump.

High-end smartphones, with their fat profit margins, can weather this storm. But for manufacturers focusing on mid-to-low-end models, an awkward situation has emerged:

Memory chips are a rigid cost but not a selling point. If prices rise, price-sensitive mid-to-low-end users—accustomed to buying 512GB/1TB storage for around 1,000 yuan—will likely wait it out. But if manufacturers don't raise prices, their already thin profit margins could be wiped out by rising costs.

Transsion is a prime example. In 2025, its total revenue fell less than 5% year-on-year to 68.7 billion yuan, but profit nearly halved. Net profit attributable to shareholders was around 2.5 billion yuan, down 3 billion yuan from the previous year—a 54% drop. Transsion directly attributed this to rising memory prices in its earnings preview. In price-sensitive markets like Africa, estimates suggest that for every $5 increase in terminal pricing, sales could drop by over 10%.

According to Jiemian News, in January this year, Wan Zhiqiang, CMO of Starry Meizu Group China, admitted that the sharp rise in memory prices had dealt a severe blow to Meizu's business plans, forcing the cancellation of the Meizu 22 Air launch. Recently, there have also been reports that Meizu's smartphone business has effectively halted, with the Meizu 23 project no longer moving forward.

With costs continuing to rise, industry differentiation is almost inevitable. High-end brands can rely on scale and supply chain clout to hold the line, while low-cost, high-volume manufacturers are being forced to explore options: raising prices, reducing specs to maintain prices, or cutting production.

03 Price Hikes, New Paths, and AI

For smartphone makers, 2026 is set to be a year of divergence.

The premiumization trend, combined with the memory cycle, is giving Apple, Samsung, and Huawei a growing advantage. In Q4 last year, Apple hit record highs in both shipments and revenue, up 14% and 23% year-on-year, respectively, with new revenue records in the U.S., China, Latin America (LATAM), Western Europe, the Middle East, and South Asia.

Diversified Android manufacturers will face less impact. Xiaomi's smartphone business saw notable pressure in Q4 last year, with shipments down 11% year-on-year. The silver lining is that at the group level, Xiaomi isn't overly reliant on smartphones—its IoT and automotive businesses are showing strong momentum. In Q3 last year, Xiaomi's automotive revenue reached 29 billion yuan, up 199.2% year-on-year, achieving a quarterly operating profit of 700 million yuan and a gross margin exceeding 25% for the first time.

Other, less diversified smartphone makers, however, face greater challenges.

To navigate the crisis, manufacturers are already taking action.

First up: price hikes to protect margins.

Sina Tech reports that starting in March, smartphone price increases will accelerate, with new models seeing hikes of at least 1,000 yuan. Meanwhile, mainstream brands like OPPO, OnePlus, Vivo, iQOO, Xiaomi, and Honor are expected to raise prices on older models to cope with frequent memory cost fluctuations.

Next: exploring new businesses.

In recent years, smartphone makers have been expanding their horizons. For example, starting last year, multiple manufacturers—including OPPO, Vivo, and Honor—began developing handheld gimbal cameras similar to DJI's Pocket series, targeting a market where DJI enjoys margins over 50% and lifetime sales exceeding 10 million units.

There have also been notable executive changes. Recently, Vivo announced a leadership reshuffle: founder and CEO Shen Wei stepped down as president, with Executive Vice President Hu Baishan promoted to president while retaining his role as COO, reporting to Shen Wei. Hu, a key figure in Vivo's technological upgrades, led the establishment of Vivo's Central Research Institute and drove its global imaging partnership with Zeiss. Outsiders see this move as Vivo's shift toward multi-device ecosystems, accelerating new businesses like MR and robotics.

Finally: AI.

Since last year, on-device AI has finally shown signs of influencing consumer decisions. The Nubia M153 Doubao smartphone assistant, a collaboration between ByteDance and Nubia, can directly respond to user intent, enabling cross-platform price comparisons and voice-activated photo editing. ByteDance, Alibaba, and Tencent have also demonstrated how to better integrate AI into smartphones. Nubia CEO Ni Fei has stated that the trend toward AI smartphones is irreversible, with “open collaboration” as the path forward.

One clear trend is that as model capabilities expand, the integration of models with systems and smartphones will deepen. The manufacturer that first pioneers a mature on-device AI agent deployment strategy could spark a new wave of upgrades.

Sources:

1. GeekPark: "Smartphone Agents: The 2026 Playbook"

2. Yuanchuan Tech Review: "Memory Price Hikes Collapse the Budget Smartphone Market"

3. Multifaceted InterfaceX: "Meizu Smartphones May Become History: Business Effectively Halted, March 2026 Delisting"

4. Counterpoint Research: "Memory Prices to Surge 50%, Rally to Continue into 2026"

5. Counterpoint Research: "Global Smartphone ASP Tops $400 for First Time in a Single Quarter"

6. Dingjiao: "Spring Festival Smartphone Wars: Some Drop Prices by 4,000 Yuan, Others Hold Firm"

The cover image and accompanying photos are owned by their respective copyright holders. If the copyright owner believes their work is unsuitable for public viewing or should not be used freely, please contact us promptly, and our platform will make corrections immediately.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving