Why Am I Bullish on Uber Despite Its Downward Trend?

07/15 2026

07/15 2026

459

459

Autonomous Driving: A Benefit or a Disruption?

Produced by | Meigang Investigation

Assessing Uber's development through valuation, business metrics, membership plans, advertising, and autonomous driving.

At the time of writing, Uber's stock price had fallen to around 70.

After further reading and research, we are even more bullish on Uber.

I. Valuation and Key Financial Ratios

Since last October, Uber's stock price has been declining, dropping from 100 to around 74.

What does a stock price of 74 signify?

Reaching a multi-support level: The stock price has fallen to the support levels seen in February and April this year, as shown in the figure below.

Valuation compressed to historic lows: TTM P/E ratio of 17, P/S ratio of 2.68, and stock price to cash flow ratio of 14.

From the perspective of compound interest's key indicators, Uber's ROA is 15%, ROE is 37%, and ROIC is 25%. What does this mean? Microsoft's respective figures are 20%, 34%, and 27%.

Buying a compound interest machine at a low price is a possibility. However, a low price does not equal an opportunity, and current compound interest does not guarantee sustained compound interest.

What is the market currently worried about? Is business growth slowing down? What catalysts exist for the stock price? What opportunities is the market overlooking? These are the questions that need answers.

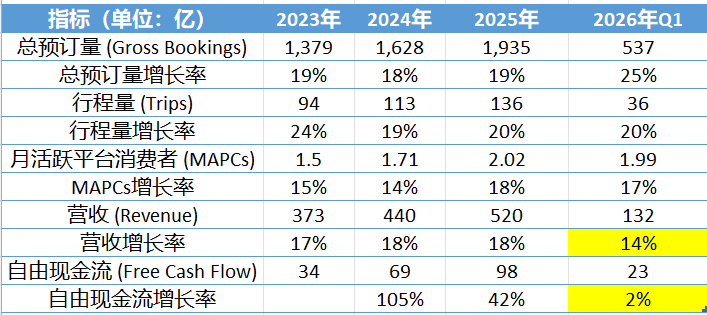

II. Core Business Metrics - Is Growth Slowing?

Analyze the following table compiled by the Chief Inspector item by item.

Total bookings have grown steadily over the past three years, with acceleration observed in Q1 2026.

Trip volume maintains steady growth without signs of deceleration.

The number of monthly active platform consumers continues to grow steadily.

Revenue growth rate for Q1 2026 declined from the usual 18% to 14%:

This is not actually a slowdown in growth but rather a bookkeeping impact due to a change in business model in the UK market.

Under the new accounting method, Uber's payments to drivers in the UK are no longer recorded as operating costs but are directly treated as revenue deductions.

This change in accounting treatment resulted in a $1 billion reduction in book revenue.

Adding this $1 billion back, the revenue growth rate is 23%.

Revenue growth is actually accelerating, not decelerating.

In terms of free cash flow, Q1 2026 was affected by fluctuations in working capital, leading to significant cash outflows. However, looking at just one quarter is not very meaningful; tracking at the end of the year will provide a clearer picture.

Therefore, from the perspective of key business metrics, business growth has not slowed down; instead, it has accelerated in terms of total bookings and adjusted revenue.

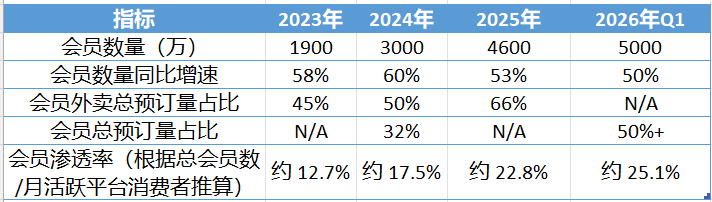

III. Uber One Membership System - An Often Overlooked Revenue Converter

Why look at the progress of the Uber One membership plan? Because this membership system significantly optimizes Uber's overall revenue conversion capability in several ways:

Membership fees are directly included in the revenue base. The subscription fees paid by users for Uber One are directly counted as revenue, improving revenue stability and increasing gross profit margins. With 50 million members in Q1 2026 and an annual membership subscription fee of $100, the annual revenue from subscriptions alone would be $5 billion.

Significantly increases average order value and consumer spending. Management indicates that members' average monthly spending is 3-3.4 times that of non-members, thereby diluting fixed costs.

Cross-platform traffic guidance and ultra-high retention rates. Members exhibit high loyalty, with cross-platform (ride-hailing + food delivery) consumer retention rates 35% higher than those of single-service consumers. Cross-selling significantly reduces additional marketing costs for acquiring new customers.

I summarize the important indicators for tracking Uber One in the table below:

The logic behind Uber One is relatively clear: it employs a combined strategy of "subscription fees + high average order value + high-frequency cross-platform repurchases."

IV. Advertising Business - Not Yet Fully Unleashed but Holds Immense Potential

At the end of 2022, Uber established an advertising department. A year later, the advertising ARR reached $900 million, growing to $2 billion by the end of 2025/early 2026.

On the ride-hailing platform, Uber has not set advertising targets because management believes that the travel experience should take priority, and travel advertising should focus on "quality" over "quantity."

The food delivery platform advertising is the main battlefield. Management set a long-term goal in 2024 for advertising revenue to account for more than 2% of total food delivery bookings. Based on total food delivery bookings of $90.9 billion for the whole year of 2025, the 2% target corresponds to $1.8 billion.

Although Uber has not disclosed the exact gross profit margin of its advertising business, management has repeatedly pointed out that the advertising business has an extremely high gross profit margin and provides excellent operational leverage for boosting profits.

Management clearly recognizes the potential of advertising but has been restrained. This indirectly shows that they prioritize long-term interests over short-term performance spikes. It's a balancing act.

From another perspective, if management decides to loosen this valve, even slightly, it could significantly boost Uber's overall profits and serve as a strong catalyst for the stock price.

V. Autonomous Driving - A Benefit or a Disruption?

Will Uber benefit from the autonomous driving wave or be disrupted by it? This is the most crucial question in this article and the core of whether Uber will be re-priced.

Currently, the market's pricing is caught in the middle, with bullish and bearish forces vying, and no definitive conclusion has been reached yet.

To answer this question, we need to examine from an industry perspective where Uber currently stands and where it will stand after autonomous driving becomes widespread. There are also several sub-questions to consider and organize.

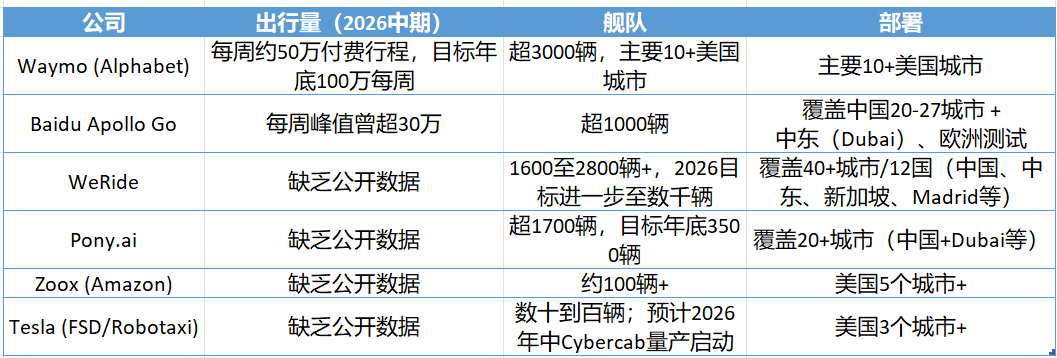

Question 1: Who are the leading companies in autonomous driving? Is there a possibility of one company dominating in the future?

Currently, the leading global autonomous driving companies mainly include Waymo, Baidu Apollo Go, WeRide, Pony.ai, Zoox, and Tesla. I have compiled information gathered online into the following table.

Among these, the first four companies—Waymo, Apollo, WeRide, and Pony—have achieved commercial operation of Robotaxi services without safety drivers.

While we focus on the US autonomous driving market, Chinese autonomous driving companies have already fully rolled out in multiple cities and are quickly approaching the inflection point of overall profitability. This is important because we can refer to the US market based on this.

Among the companies listed above, only a few have achieved a high degree of autonomous manufacturing (such as Apollo, Zoox, and Tesla). Other companies do not manufacture their own vehicles but rely on partner vehicle platforms or joint production.

Take Waymo as an example. It collaborates with automakers such as Hyundai, Volvo, and Toyota to provide basic vehicle platforms. Through integration partners like Magna, Waymo Driver's autonomous system is assembled and integrated in US factories. The focus is on the integration of software and hardware rather than building entire vehicles from scratch.

Tesla is a unique case. Musk's vision is that as autonomous driving technology evolves, Tesla owners can rent out their cars to become part of the AV ride-hailing network. If this happens as he envisions, a large number of driverless Teslas will flood the market and capture significant market share. However, the question remains: not everyone is willing to rent out their car to earn extra money. Isn't buying a car for personal ownership rather than for earning extra income the primary motivation?

Based on the above, my inference is that the barrier to entry for autonomous driving is not insurmountably high. As technologies become standardized, the future autonomous driving market is likely to have multiple providers, resulting in a competitive landscape with many players.

Question 2: What changes will the widespread adoption of autonomous driving bring to transportation?

I would like to use Jevons Paradox to answer this question.

Jevons' core viewpoint: When technological progress improves resource utilization efficiency, the total consumption of that resource may increase rather than decrease.

The underlying mechanism: Technological progress makes resource production more efficient, thereby reducing costs. Due to lower costs, the total consumption of the resource will increase.

Extending this to autonomous driving, we can infer the following:

Autonomous driving increases vehicle utilization. In Uber's collaboration with Waymo, it was found that, on average, a Waymo autonomous vehicle is busier than 99% of local human drivers. Humans get tired and need rest, while autonomous vehicles can work continuously except for charging.

Autonomous driving significantly reduces transportation costs. Increased vehicle utilization, elimination of human driver salaries, and continuous technological iterations will gradually reduce the cost of autonomous driving.

Due to the decrease in ride costs, more people will choose to take rides. On the one hand, the capacity of the ride-hailing market will explode; on the other hand, people's willingness to buy cars may decrease.

Question 3: Where does Uber currently stand in the hybrid network of human drivers and autonomous vehicles?

Uber does not heavily invest in vehicle manufacturing or exclusively rely on a single autonomous driving company. Instead, it serves as a demand-side entry point, integrating human drivers and multiple AV suppliers. Users can match the optimal vehicle (human-driven or autonomous) with a single tap through the Uber App, and Uber takes a commission.

The biggest challenge for ride-hailing is the volatility of demand, such as differences in peak and off-peak hours, locations, and weather conditions. A pure AV fleet can easily fall into a utilization dilemma, with either excess capacity during off-peak hours or insufficient capacity to meet peak demand.

Uber's hybrid network advantage lies in the fact that, on the one hand, human drivers provide flexibility and full geographical coverage, while on the other hand, AVs offer high utilization and 24-hour operation, thereby maximizing vehicle utilization.

Autonomous vehicles are extremely expensive assets, and the key to their commercial success lies in vehicle utilization. Currently, Uber's average commission is around 20%. For autonomous driving companies, the increase in vehicle utilization must be able to cover this 20% commission for them to be willing to partner with Uber.

According to Uber management, mathematically, the utilization rate of autonomous vehicles on the Uber platform must be 25% higher than that on a 1P (first-party) independent network for autonomous driving companies to break even. They believe that the additional utilization rate brought by the Uber platform to autonomous vehicles can easily exceed this 25% incremental threshold.

Currently, except for Tesla, Uber has partnerships with major AV providers. This indicates that Uber indeed provides a vehicle utilization increase of over 25% for them.

In Q1 2026, the volume of autonomous rides increased more than tenfold year-on-year, with over 15 cities expected to be launched by the end of this year—see the figure below.

In markets where Uber collaborates with AV providers, there is currently no data to prove that AV providers are taking away Uber's market share. Management also pointed out that in San Francisco and Los Angeles, where Waymo has been operating for a longer time, Uber's market share is even higher than it was six months ago.

In summary, within the current hybrid network of "humans + AVs," Uber holds the entry point to demand through its platform. Since autonomous driving is still in its early stages, Uber's advantage is unlikely to be disrupted in the short to medium term.

Question 4: Where does Uber's advantage lie after the full adoption of autonomous driving?

The answer to this question lies in the previous questions.

In the early stages of technology, value distribution may favor the technology providers (autonomous driving companies). However, as technologies become standardized and demand becomes concentrated, platform providers gain more advantage.

In the era of full AV adoption, there will be multiple autonomous driving providers, and users will still need a unified entry point to hail rides (across cities and operators). Even if AV providers build their own apps, Uber can still leverage its massive platform network effect to divert traffic through partnerships.

Due to the significant decrease in ride costs, the size of the ride-hailing market will explode. Even if AV providers' own apps divert some traffic and Uber's commission rate decreases slightly with the increase in total bookings, Uber can still continue to grow in this extremely large market.

In fact, Uber is not sitting idle in this wave. Uber has launched "Uber Autonomous Solutions," aimed at providing fleet management, data collection, vehicle financing, insurance, and other services to AV partners. This expands its B2B business while increasing the cost for AV providers to leave the platform. Additionally, revenue sources such as food delivery, advertising, and freight transportation buffer some of the risks.

Question 5: How will Uber's ride-hailing revenue and cost structure change after the full adoption of autonomous driving?

The main impacts of autonomous driving adoption on the revenue structure:

Uber's revenue will heavily rely on commissions from AV providers and the services it offers to them.

The high utilization rate of AVs will increase revenue per vehicle.

While commission rates may decline, the reduction in ride costs will drive explosive market growth, thereby boosting revenue.

Key impacts on costs:

Structural reduction in insurance costs: Under the traditional model, commercial insurance for human drivers is one of Uber's heaviest costs. Since autonomous vehicles will ultimately outperform human drivers in terms of safety, their insurance costs will be lower.

Shift from driver payouts to physical infrastructure spending: Uber will no longer pay service fees and subsidies to human drivers. However, this will lead to high maintenance costs. Uber may need to invest heavily in acquiring and building vehicle parking facilities and providing infrastructure services such as charging, maintenance, and cleaning for its autonomous fleet.

VI. Conclusion - We are optimistic about Uber's market performance

By connecting all the information and inferences above, we are optimistic about Uber's market performance.

Uber is a platform company, not a software company. Its platform network effects create a strong moat. Member loyalty is high, and cross-platform spending capacity is strong. Once the advertising business valve (valve) is opened, it will boost profits.

In the future wave of autonomous driving, multiple AV providers will compete. Leveraging its platform network effects, Uber will serve as the entry point for demand, creating value for AV providers by improving vehicle utilization while enjoying the benefits of explosive growth in the convenient travel market.

-

Standing at a Distance, Behind Xiaomi's Phone Slowdown and Layoffs", "Xiaomi Phone, Declining Sales, Offline Stores, Product Strategy, Comprehensive Ecosystem of People, Vehicles, and Homes", "Accordi

-

![]()

Phoenix Optics Forecasts a Nearly 70% Drop in First-Half Net Profit, Yet Optical Business Profit Shows Growth!

-

![]()

A Staggering 50.16% Reduction in Losses Projected! COST's Interim Report Signals a Pivotal Moment

-

![]()

Nearly 19% of National Total! Guangdong Boasts 164 Registered Large Models as New AI Personification Regulations Take Effect

-

![]()

BYD’s Baosha, Sought After by Australians, Makes a Triumphant Return to China

-

【Focus】Analysis of Downstream Demand Sectors and Key Enterprise Development for Acrylic OCA Optical Adhesives in China by 2026

-

![]()

Big News! OpenAI Poaches Apple's Hardware Team

-

Hot Topic | DeepSeek and Zhipu Cross into Chipmaking, Domestic AI Firms Vie for Computing Autonomy