Can Alibaba still leap after Taobao and Tmall's prolonged squat?

11/18 2024

11/18 2024

640

640

Although its share price performance has been lukewarm, it has always been a key focus of the market and a major recommendation for sellers. Alibaba Group recently released its second-quarter report for FY25. How did it perform? Here's Dolphin Investment Research's take:

I. Shareholder Returns Remain Top Tier

According to company disclosures, Alibaba repurchased $4.1 billion worth of shares during the quarter ending in September, reducing its total share capital by 2.1%. Although this is slightly lower than the average of over $5 billion in the first half of the year, considering the share price increase in late September, the slight decline in repurchases is understandable. With stable quarterly repurchases of $4 billion to $5 billion, corresponding to Alibaba's market capitalization of less than $220 billion, the return rate is at least 8%. This does not even consider additional potential dividend returns. Compared to other Chinese companies listed overseas, which have seen a decline in repurchases in the third quarter (partly due to recent significant gains), Alibaba performs exceptionally well in this area.

II. Taobao and Tmall Remain the Family's Biggest 'Burden'

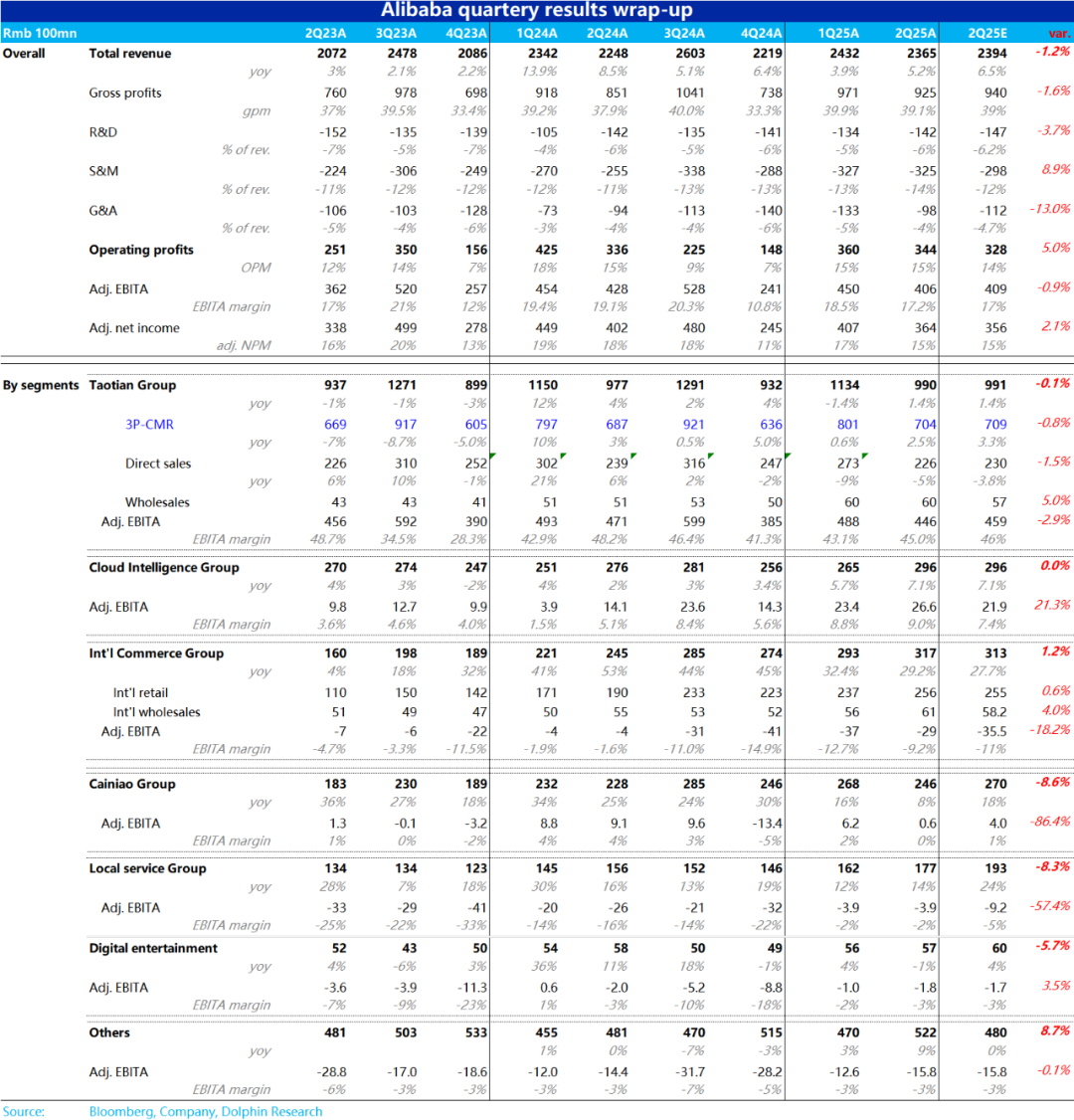

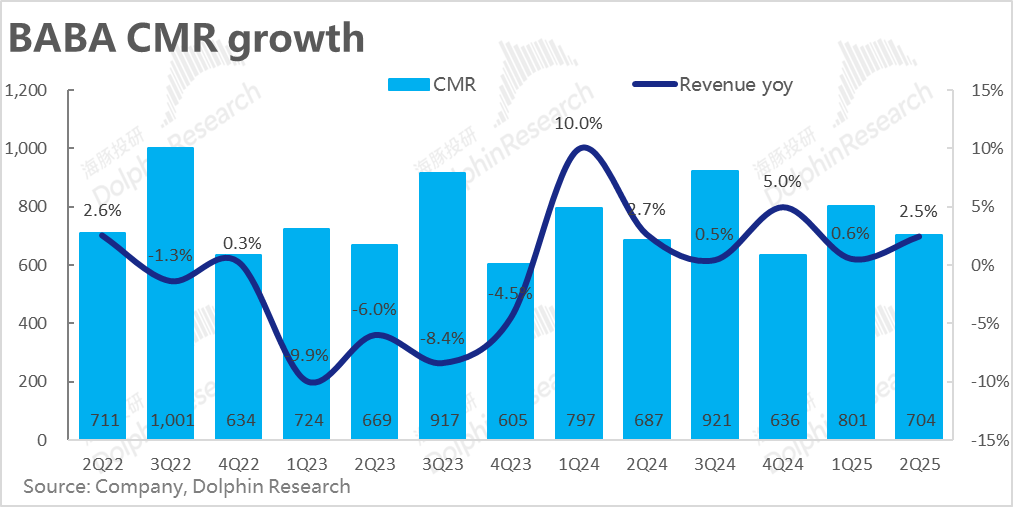

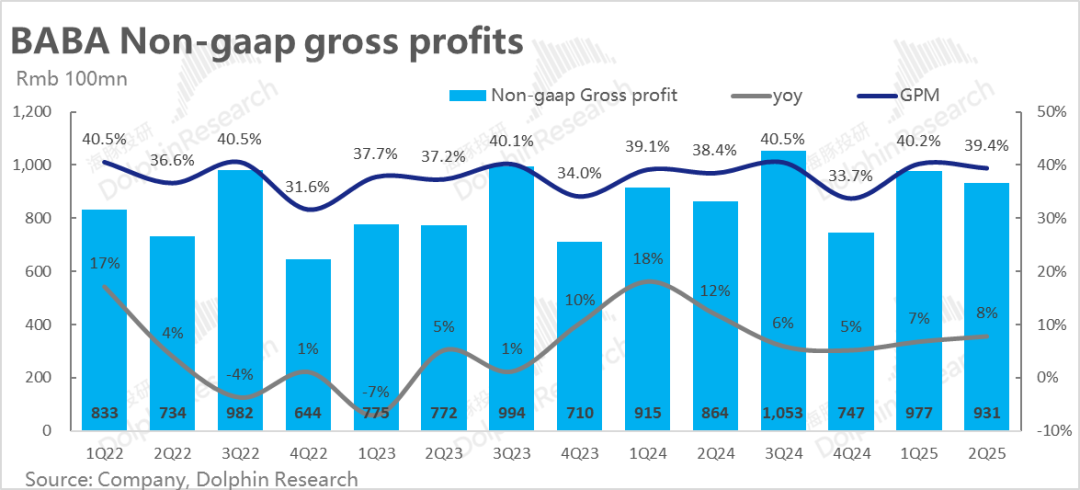

Alibaba's core business, Taobao and Tmall, reported a 2.5% year-on-year increase in domestic retail customer management revenue (CMR) this quarter, an improvement from the previous quarter's 0.6%. However, this still fell short of the consensus average of 3.3%, indicating a subpar performance.

In terms of performance trends, the past few quarters have consistently shown a pattern of order growth rate > GMV growth rate > revenue growth rate > profit growth rate. This quarter, the difference between CMR and GMV growth rates may have nearly disappeared. Although the company did not disclose the GMV growth rate, it did state that the take rate has stabilized year-on-year. Coupled with the implementation of a 0.6% technical service fee and Full site advertising tool ( Full site advertising promotion tool ) in early September, the benefits released in the third quarter of the calendar year were limited. As these two new initiatives gradually take effect, the growth rate difference between CMR and GMV will continue to narrow, and it is likely that CMR growth will eventually surpass GMV growth.

While the improving trend in CMR growth can barely compensate for its weaker-than-expected performance, there is no room for compensation at the profit level. Taobao and Tmall Group's adjusted EBITA declined by about 5.3% year-on-year this quarter, an expansion from the previous quarter's 1% decline and below expectations by about 3%. Combined with other data, the significant increase in marketing expenses is likely the main reason behind the decline in Taobao and Tmall's profits.

III. Alibaba Cloud Increases Revenue and Profit, Steadily Moving Towards Expected Goals

Alibaba Cloud, the group's second most important segment, has struggled with single-digit revenue growth for nearly two fiscal years. However, management announced early this year that cloud business growth would accelerate to double digits in the second half of the year. This quarter, Alibaba Cloud generated revenue of $29.6 billion, up 7.1% year-on-year, an improvement from the previous quarter's 5.7% (but not beating expectations). According to the company, the recovery in growth was mainly driven by double-digit growth in its public cloud business (with contributions from AI), partially offset by the private cloud segment.

From a profit perspective, Alibaba Cloud's adjusted EBITA profit reached $2.66 billion this quarter, exceeding expectations by 21%. The adjusted EBITA margin increased by another 0.2 percentage points quarter-on-quarter, maintaining the trend of profit improvement. Although there is still some distance from double-digit growth, the continued increase in revenue growth and profit margins this quarter will undoubtedly strengthen market confidence in the cloud business's recovery.

IV. International E-commerce 'Mutes Its Success', Prioritizing Loss Reduction

The international e-commerce segment, which has the second-largest revenue volume in the group, continued its trend of more refined operations this quarter. Despite a noticeable increase in the same-period base, revenue growth slowed slightly to 29% year-on-year but was still 1.5 percentage points higher than expected. Specifically, international retail and wholesale businesses grew at 35% and 9.4%, respectively, a slowdown of 3-4 percentage points from the previous quarter but at a similar pace.

Correspondingly, the international segment's losses continued to narrow this quarter. Adjusted EBITA losses narrowed from $3.7 billion in the previous quarter to $2.9 billion, better than expected. The loss rate also narrowed from -12.7% to -9.2%. Amid increasing regulatory risks in cross-border business, a preference for muted success, and local e-commerce players in Southeast Asia choosing to prioritize profits, it is likely that international business will maintain 'high-quality' growth and prioritize loss reduction.

V. Profits Return to Zero, with Cainiao Taking on the Heavy Lifting of Investments

Cainiao, closely tied to the group's overseas business development, saw its year-on-year revenue growth rate decline from 15.7% to 8% this quarter due to the deceleration in international business. However, due to the high capex investments required for cross-border logistics, Cainiao, which was profitable in the previous quarter, saw its adjusted EBITA narrow significantly to only $60 million this quarter, well below expectations. When combining international e-commerce and Cainiao, the combined loss narrowed by only about $200-$300 million quarter-on-quarter, indicating a lackluster performance in loss reduction. It can be said that Cainiao has taken on the heavy lifting of heavy asset investments.

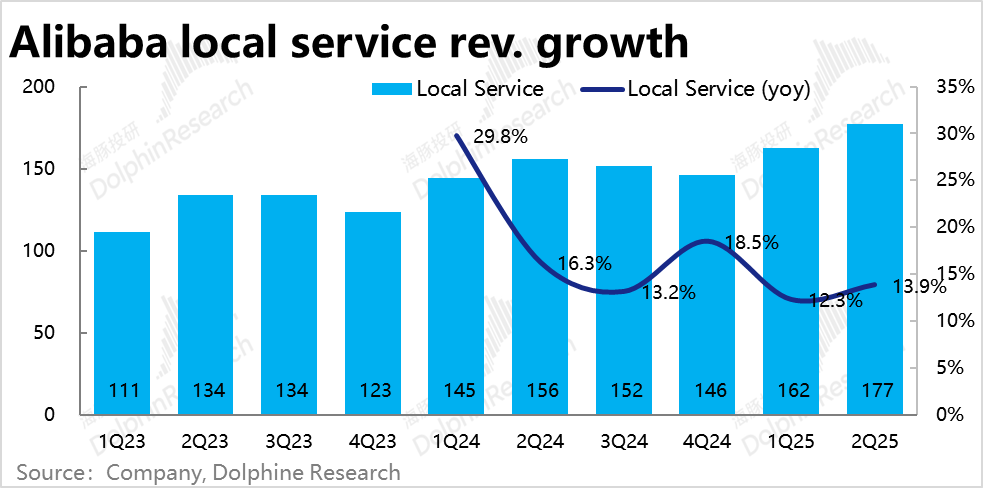

VI. Local Services Also Prioritize Loss Reduction

Alibaba's local services revenue grew by 13.9% this quarter, a slight acceleration but significantly missing the market's expectation of 24% growth. However, the actual loss of $390 million was significantly lower than the market's expectation of a $920 million loss. Unlike the market's expectation of high investment, high growth, and high losses, Alibaba actually adopted a strategy of steady growth and loss reduction, which may be a better choice.

VII. Suspension of Loss Reduction Progress for the Entertainment and 'N' Companies: The entertainment segment reported a loss of $180 million this quarter, higher than the previous quarter's loss of $100 million and market expectations. The 'N' companies collectively reported a loss of $1.58 billion, in line with market expectations but an expansion from the previous quarter's $1.26 billion loss. It seems that investment efforts have increased?

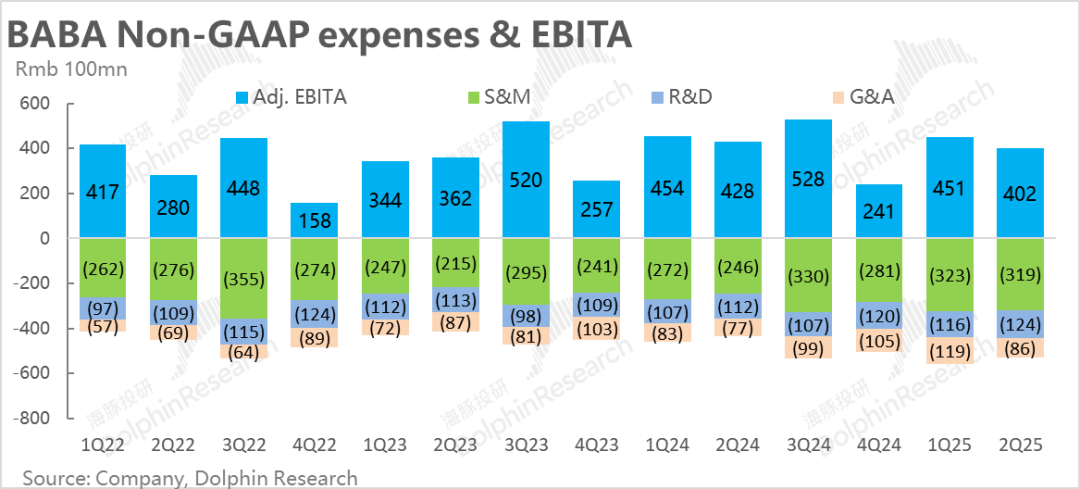

VIII. Aggressive Spending is the Biggest Culprit Behind the Group's Profit Decline

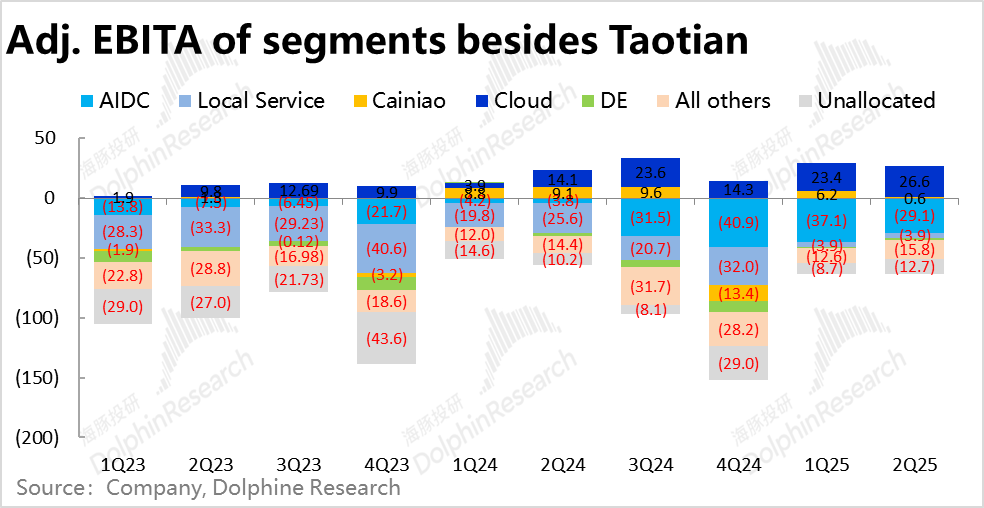

From a profit perspective, Taobao and Tmall Group's lower-than-expected profit (missing by about $1.3 billion) was offset by Alibaba Cloud, which continued to improve its profits, and the local services business, which operated more refinedly and had significantly lower-than-expected losses. Overall, the group's profit indicators were largely in line with expectations. However, the group's adjusted EBITA margin declined from 18.5% in the previous quarter to 17.2% this quarter. The trend of significantly improved group profit margins due to better-than-expected loss reduction/profit increase in all businesses except Taobao and Tmall in the previous quarter did not continue this quarter. The reason is that marketing expenses (excluding SBC) increased by nearly 30% year-on-year (19% in the previous quarter), about 9% more than market expectations. While administrative and R&D expenses increased by 10%-11% year-on-year, although not as drastic as marketing expenses, the expense ratio still expanded compared to the mere 5% increase in revenue. It is evident that the significant increase in expenses was the main cause of the decline in profit margins this quarter.

Dolphin Investment Research Viewpoint:

Overall, Dolphin Investment Research's view on Alibaba's latest performance is somewhat negative. Firstly, regarding Taobao and Tmall's business, although the CMR growth rate has marginally improved, the absolute growth rate remains at a low 2.5%, falling short of expectations and not considered good. More seriously, the profit amount declined year-on-year, and the profit margin also dropped. The market has always been concerned about whether Taobao and Tmall's previous GMV growth recovery was driven by subsidies. The consecutive quarterly year-on-year declines in Taobao and Tmall's profits, with expanding declines, have not improved but worsened these concerns. Therefore, describing Taobao and Tmall's performance as 'weak' would not be an exaggeration.

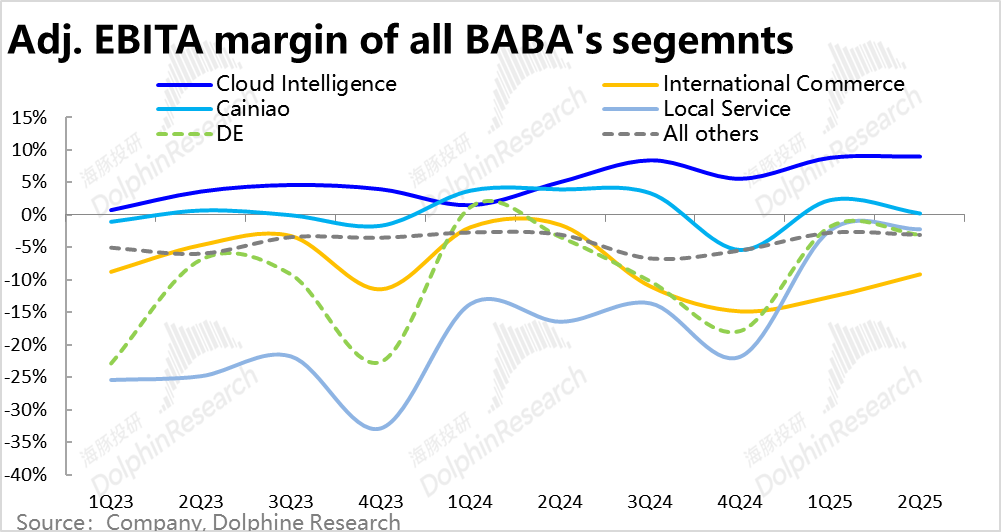

The second and third businesses, Alibaba Cloud and the symbiotic pair of international e-commerce and Cainiao, showed mixed performances. Alibaba Cloud, with accelerating revenue growth and improving profit margins, still has noteworthy performance and a promising future worth market expectations. However, the revenue growth of the international e-commerce and Cainiao duo slowed, and their combined losses did not narrow significantly. While the loss rate of the international e-commerce segment alone declined, this was at the cost of Cainiao bearing the logistics asset investments. Collectively, the performance was not good. As for other less significant businesses, the highlight of the previous quarter was that the loss rates of these 'relatively marginal' businesses narrowed significantly both in terms of expectations gap and quarter-on-quarter trends.

However, this quarter, the loss amount of the local services business remained flat quarter-on-quarter, and the losses of the entertainment and 'N' companies even expanded slightly. Combined with the expense data, it seems that reinvestment may have led to increased losses. The positive effect of rapid loss reduction in 'relatively marginal' businesses has also disappeared (temporarily).

From the perspective of current performance, Alibaba's performance can at best be described as 'weaker than expected.' Currently, Dolphin Investment Research's attitude towards Alibaba's investment value is: relying on high repurchases to support the valuation floor downwards and 'hoping' that Taobao and Tmall can recover slightly following government consumption stimulus and enhanced monetization on Taobao upwards.

Looking downwards, the current return rate of at least 8% brought by repurchases to Alibaba ranks in the top tier among all Chinese assets, providing a very solid bottom support for the company.

In terms of capital or event catalysts, the market has long anticipated Alibaba's dual primary listing in Hong Kong and inclusion in the Stock Connect program, which has now been realized. Although the process of southern-bound funds or passive index funds allocating to Alibaba may not be complete, from an expectation perspective, this positive development is now in the past. The only potential event catalyst left is the rumored re-IPO of Ant Group. Unlike Alibaba's inclusion in the Stock Connect, which was only a matter of time, whether Ant Group will re-IPO remains speculative, and investors should not have excessive expectations.

Fundamentally, after several quarters of adjustment, there are still no signs of a true turning point in Taobao and Tmall's business (e.g., a significant increase in CMR and at least stabilizing profits to catch up with revenue growth). The positive effects of the 0.6% technical service fee and Full site advertising tool ( Full site advertising promotion tool ) implemented by Taobao and Tmall in early September on monetization rates are expected to take at least six months to materialize. Regarding whether Taobao and Tmall's performance will truly improve, Dolphin believes there is potential for improvement, but there is currently insufficient evidence to support a confident optimistic judgment given the current macroeconomic and industry competitive environment. In summary, hold the bottom line first and then 'envision' possible turnaround opportunities.

Below is a detailed analysis of the performance

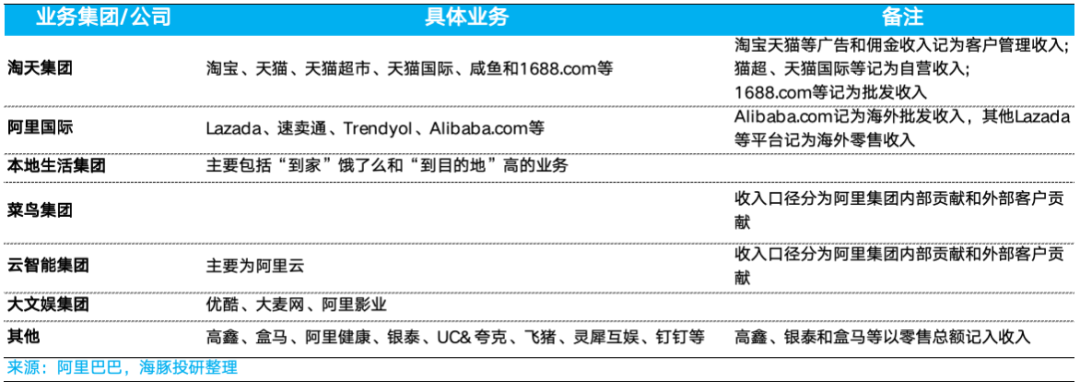

I. Alibaba's New Financial Reporting Framework

Starting in June 2023, Alibaba Group significantly adjusted its financial reporting framework. Here is the latest framework for better understanding subsequent analyses:

1) Taobao and Tmall Group: Taobao, Tmall, Tmall Supermarket + Imported Direct Sales; Domestic Wholesale;

2) International Group: Cross-border Retail (AliExpress), Cross-border Wholesale (International Station), Overseas Local Retail (Lazada, Trendyol, etc.);

3) Local Services: Ele.me and Gaode Maps

4) Cainiao Group: Same as before, but now its revenue calculation includes other Alibaba Group businesses as customers, and the revenue generated by them is included in Cainiao's revenue;

5) Intelligent Cloud Group: Alibaba Cloud; DingTalk was spun off to other business categories in the September quarter of 2023;

6) Entertainment Group: Youku and Alibaba Pictures;

7) All Others: RT-Mart (rumored to be up for sale), Hema, Alibaba Health, Intime (these three belong to self-operated new retail with offline formats, originally under Domestic Commerce); Lingxi Interaction, UC, Quark (formerly part of the Entertainment business), Fliggy (originally part of Local Services), DingTalk (originally part of the Cloud business).

II. Both CMR and Profit Miss Expectations; Taobao and Tmall Remain the Biggest Challenge

After the new management set the top-level strategy for Taobao and Tmall to return to user focus, with measures to Tilt flow rate (tilt traffic) towards small and medium-sized merchants and benefit consumers, the pattern of order growth rate > GMV growth rate > revenue growth rate > profit growth rate has been the norm for Taobao and Tmall Group over the past few quarters.

Due to weak retail sales data this quarter, market expectations for Taobao and Tmall's GMV growth rate were revised downward from high single digits in 1Q25 to low single digits this quarter. However, due to the additional 0.6% service fee and Full site advertising tool ( Full site advertising promotion tool ) implemented in early September, Taobao and Tmall's monetization rate stabilized, narrowing the gap between CMR and GMV growth rates.

In actual performance, domestic retail customer management revenue (CMR) increased by 2.5% year-on-year this quarter, an improvement from the previous quarter's 0.6% but slightly missing the consensus average of 3.3%.

Although Alibaba did not disclose the GMV growth rate or range this time, it only stated that order volume growth remained in double digits. However, the company officially announced that the take rate has stabilized year-on-year. Although this does not necessarily mean that the take rate has completely stabilized or rebounded (i.e., the GMV growth rate is approximately 2% this quarter), it is likely that the growth rate difference between CMR and GMV will continue to narrow in the coming quarters, with CMR growth eventually surpassing GMV growth.

While the improving trend in CMR growth can barely compensate for its weaker-than-expected performance, there is no room for compensation at the profit level. Taobao and Tmall Group's adjusted EBITA was $44.6 billion this quarter, a year-on-year decline of about 5.3%, an expansion from the previous quarter's 1% decline and below expectations of $45.9 billion. According to the company, the decline in profits was mainly due to increased investments to enhance customer experience (such as subsidies).

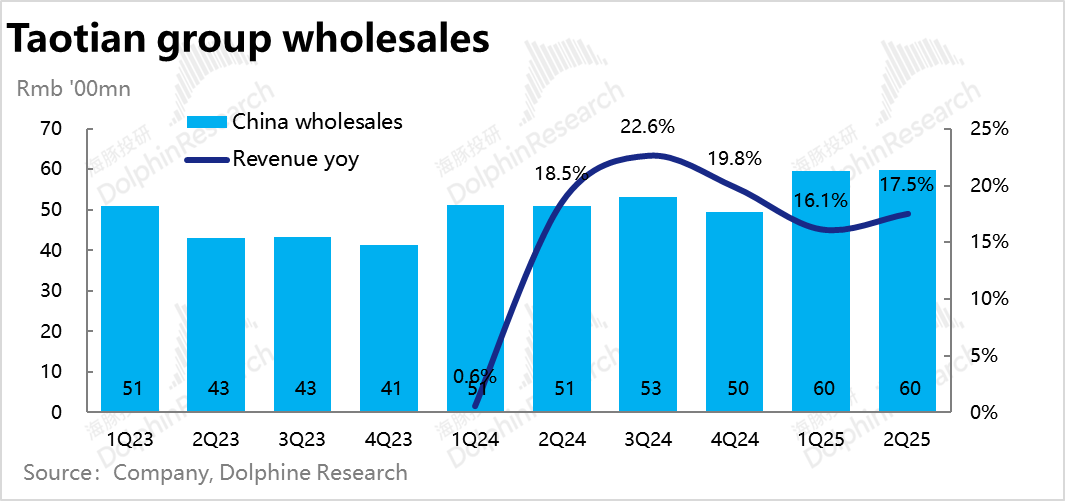

III. Self-operated Retail Continues to Decline, While 'Veteran' Wholesale Thrives

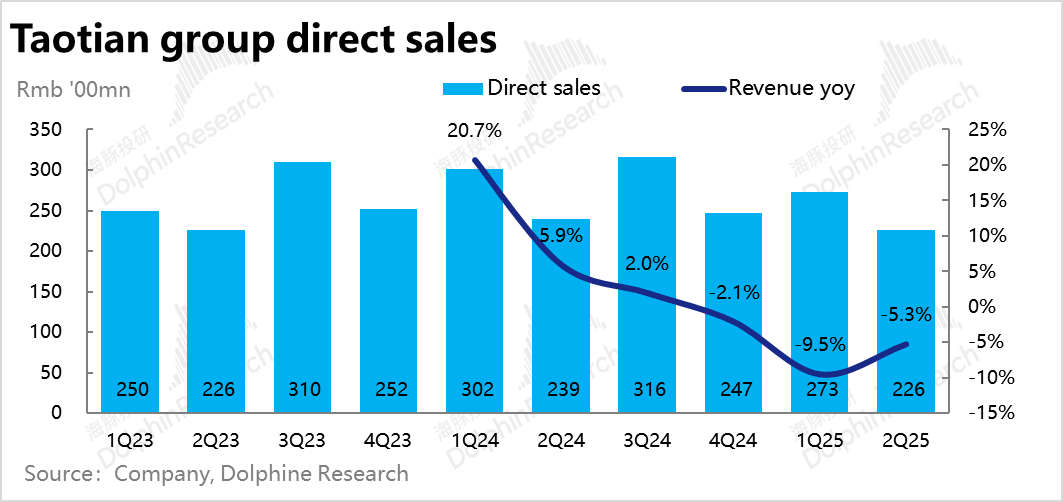

Taobao and Tmall Group's self-operated retail business reported a year-on-year revenue decline of 5.3% this quarter, a narrowing from the previous quarter's -10% and coincidentally in line with JD.com's self-operated retail performance. According to the company, the continued revenue decline was mainly due to a drop in sales of home appliances. We believe that the national subsidies also contributed significantly to the improvement in Taobao and Tmall's self-operated growth rate, but JD.com has a stronger presence in home appliances, so Taobao and Tmall may have benefited relatively less.

The oldest 1688.com wholesale business, as a main focus of Taobao and Tmall's 'cost-effective' strategy, reported a year-on-year revenue increase of 17.5% this quarter, maintaining high growth and slightly accelerating, driven by the transformation to a 2C model and as a supply source for cross-border e-commerce.

Overall, the slightly under-expected CMR was hedged by strong wholesale revenue, and Taobao Tianmao Group's overall revenue for this quarter increased by 1.4% year-on-year, basically meeting market consensus expectations.

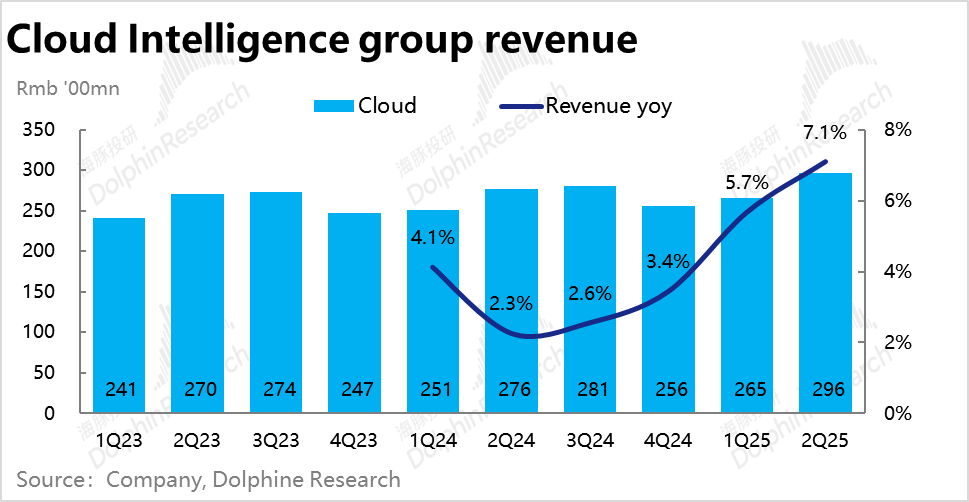

IV. Alibaba Cloud Continues Towards Double-Digit Growth

Alibaba Group's second pillar, Alibaba Cloud, achieved revenue of 29.6 billion this quarter, with a year-on-year growth rate of 7.1%, an improvement from 5.7% in the previous quarter. However, it did not exceed expectations. According to the company's disclosure, the recovery in growth was mainly driven by double-digit growth in public cloud services (also contributed by AI), but was dragged down by the active elimination of some private cloud businesses.

From a profit perspective, Alibaba Cloud's adjusted EBITA profit reached 2.66 billion this quarter, exceeding expectations by 21%. The adjusted EBITA margin increased by another 0.2 percentage points quarter-on-quarter, maintaining the trend of profit improvement.

Although there is still some distance from the management's claim that cloud business growth will return to double digits in the second half of 2024, the continued increase in revenue growth and profit margins will undoubtedly further strengthen market confidence in the continued recovery of the cloud business.

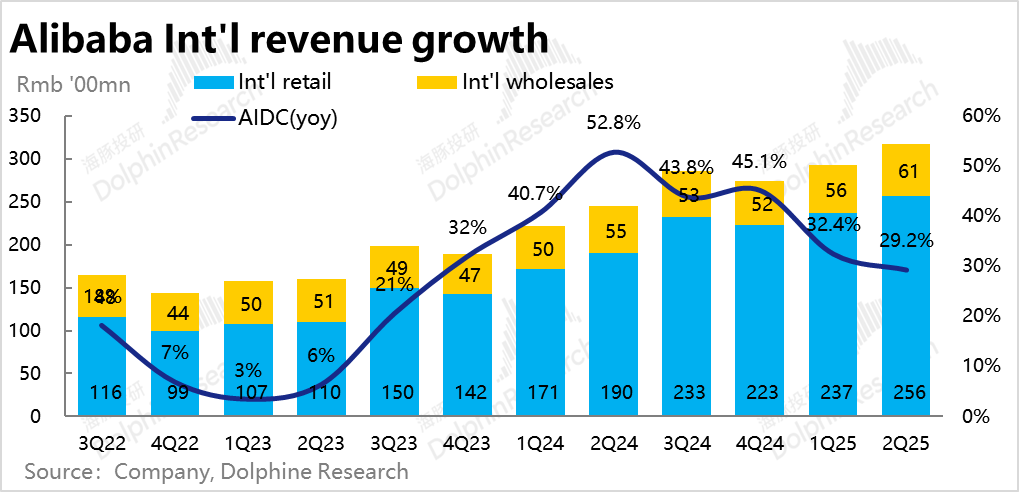

V. International E-commerce Continues Refined Operations, Growth Slows, and Losses Narrow

Compared to the domestic e-commerce industry's internal competition, cross-border expansion for incremental growth has been a consensus among domestic internet companies since 2023. This quarter, due to a shift from an aggressive strategy to more refined operations in international business starting from the previous quarter, and with a significantly higher base in the same period, international e-commerce revenue growth slowed slightly to 29% year-on-year. However, this was 1.5 percentage points higher than market expectations. Among them, international retail and international wholesale businesses grew at 35% and 9.4% respectively, both showing a slowdown of 3-4 percentage points compared to the previous quarter, with similar trends.

Correspondingly to the slowdown in growth, losses in the international segment continued to narrow this quarter. The adjusted EBITA loss, excluding share-based compensation expenses and amortization expenses, narrowed from 3.7 billion in the previous quarter to 2.9 billion, better than expected. The loss rate also narrowed from -12.7% to -9.2%. Amidst increasing regulatory risks for cross-border businesses, where it is more suitable to quietly earn profits, and as international local e-commerce players in Southeast Asia and other regions also continue to pursue profits, the profit margins of international businesses are likely to continue to improve.

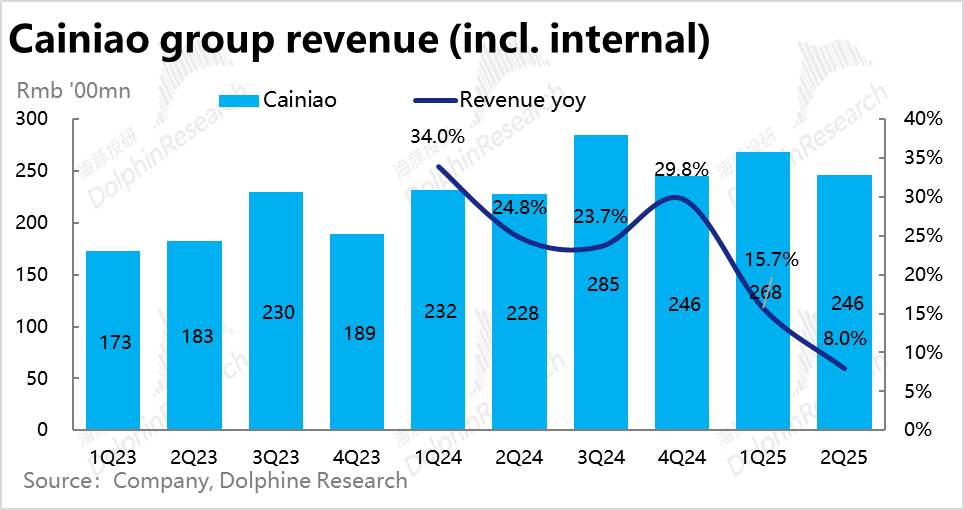

VI. Cainiao, Coexisting with AIDC, Faces a Different Fate

Currently, Cainiao's logic is nearly symbiotic with overseas expansion. Due to the slowdown in the growth of the international e-commerce segment, Cainiao's revenue growth rate also declined from 15.7% to 8% year-on-year this quarter. However, due to the high capex investments required for cross-border logistics, Cainiao, which had been profitable in the previous quarter, saw its adjusted EBITA narrow significantly to only 60 million this quarter, significantly below expectations. If we combine international e-commerce and Cainiao, the total narrowing of losses is only about 200-300 million, which is not considered good. While the asset-light international e-commerce business generates profits, Cainiao bears the heavy asset logistics capex of a difficult business. It can only be said that they share the same origin but have different fates.

VII. Local Services Revenue Misses Big, Loss Reduction Beats Big? Refined Operations Are the Reality

Alibaba's local services revenue grew by 13.9% this quarter, slightly faster, but market expectations were for a growth rate of up to 24%, resulting in a significant miss. However, correspondingly, market expectations for losses were as high as 920 million, while the actual loss was only 390 million.

Therefore, unlike the market's expectations of high investment, high growth, and high losses, Alibaba's local services business actually adopts a strategy of steady growth and loss reduction. Dolphin Research believes that the company's actual strategy is better.

VIII. Cultural and Entertainment and "N" Companies Slow Down Their Turnaround Pace, Investing Again?

Other relatively marginal businesses such as cultural and entertainment and other "N" companies share a common characteristic this quarter: the pace of narrowing losses has slowed down. Cultural and entertainment lost 180 million this quarter, higher than the 100 million loss in the previous quarter and higher than market expectations. Meanwhile, "N" companies as a whole lost 1.58 billion, in line with market expectations but an expansion compared to the previous quarter's loss. It seems that investment efforts have increased again?

IX. Group Profit Margins Decline, No More Surprises of Comprehensive Loss Reduction Across All Businesses in the Previous Quarter

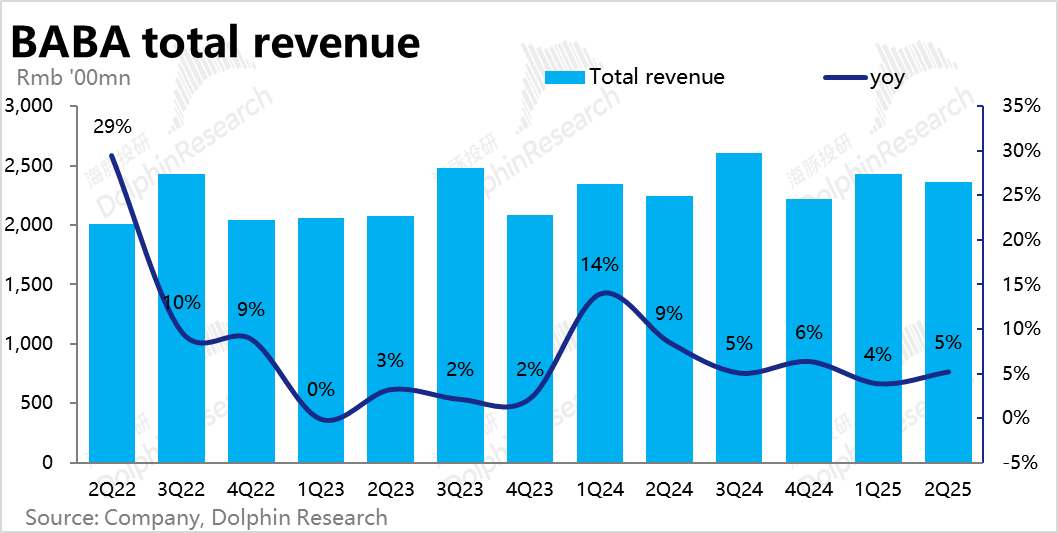

Overall, except for Alibaba Cloud and the international e-commerce segment, which met or slightly exceeded revenue growth expectations, the revenue of other segments missed expectations to varying degrees. Therefore, Alibaba Group's overall revenue growth this quarter was about 5.2%, lower than market expectations of about 6%. The pace of revenue growth did not meet expectations.

In terms of profits, Taobao Tianmao Group's adjusted EBITA profit of 1.3 billion missed expectations, which was offset by Alibaba Cloud's unexpected profit release and the still loss-making local business. The group's overall profit indicators were generally in line with expectations. The group's overall adjusted EBITA margin also declined from 18.5% in the previous quarter to 17.2%. The surprise of significant loss reduction across all businesses except Taobao Tianmao in the previous quarter did not continue this quarter.

X. Expense Investment Efforts Have Indeed Increased Significantly, the "Culprit" of Margin Decline

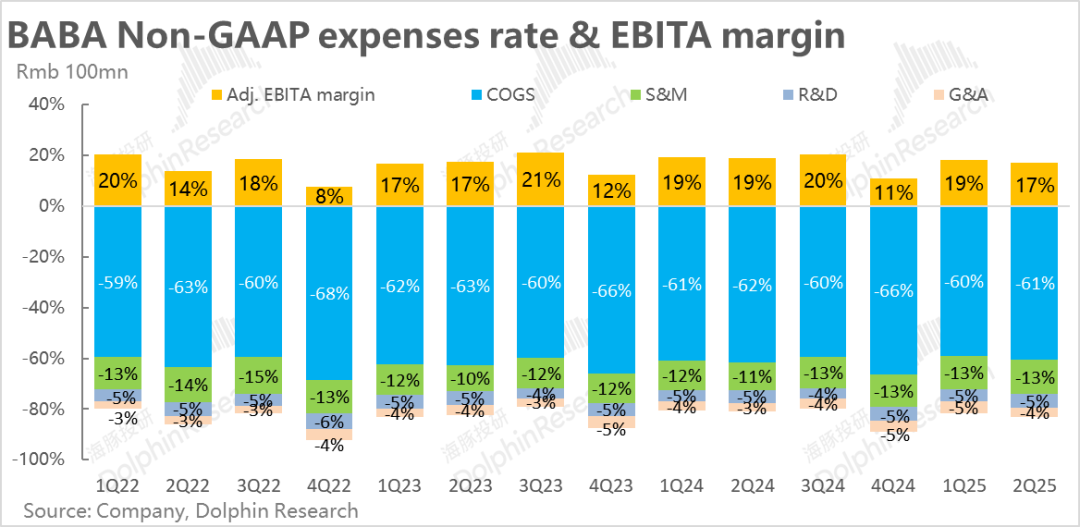

How have costs and expenses changed? First, Alibaba's gross margin after excluding share-based compensation increased by 1 percentage point compared to the same period last year, slightly lower than the 1.1 percentage point increase in the previous quarter. The gross margin continues to improve trendwise, but the magnitude of improvement has indeed narrowed slightly.

In terms of expenses, marketing expenses, excluding share-based compensation, increased by nearly 30% year-on-year, far exceeding the 19% year-on-year growth in the previous quarter. Actual marketing expenditures were also nearly 9% higher than expected. It can be seen that Alibaba's overall expenditure on customer acquisition and subsidies has indeed increased significantly, which is the main driver of the decline in profit margins this quarter.

As for administrative and research and development expenses, they also increased by 10%-11% year-on-year. Although the magnitude is not as exaggerated as marketing expenses, based on the 5% revenue growth this quarter, the administrative and research and development expense ratios are also expanding. It is clear that the "culprit" of the group's profit decline is the increase in expense expenditures.

- END -

// Reprint Authorization

This article is an original article by Dolphin Research. For reprints, please obtain authorization.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!