Chinese Cars Popularize Plug-in Hybrids in the European Market

02/26 2026

02/26 2026

604

604

Lead

Introduction

The former student has finally taught the teacher a lesson.

Decades ago, when German automakers helped China establish the foundation of its contemporary automotive industry and market through joint ventures, neither side could have anticipated that today, the former student would finally teach the teacher a lesson.

In the last week of February, German Chancellor Merz's private jet landed in Beijing. Accompanying him were the CEOs of Volkswagen, BMW, and Mercedes-Benz—three automotive giants—along with around 30 top German business leaders. This was his first visit to China since taking office as Chancellor, with a delegation that included nearly all the elite of German industry.

Two sets of data are at least partially related to Merz's objectives.

One set, released by the German Economic Institute, shows that Germany's automotive exports to China fell below €14 billion in 2025, halving from nearly €30 billion three years earlier.

The other set, from Dataforce, reveals that Chinese auto brands' sales in Europe surged by 80% year-on-year in January, capturing a 7.4% market share—nearly double that of a year ago. Meanwhile, the plug-in hybrid segment, long neglected by European automakers, is being dominated by Chinese brands led by BYD. This has also propelled BYD past MG to become Germany's best-selling Chinese auto brand.

Once dismissed overseas as a transitional and marginalized technology, plug-in hybrids have now become a technological trend exported by Chinese automakers.

Merz hopes to reshape the Sino-German automotive industry landscape, but China's automotive sector should transcend the gains and losses of a single market and delve deeper into the underlying rules and logic of the industry.

01 Shift in Fortunes: Sino-German Automotive Trade Reversal

The decline in Germany's automotive exports to China is not a short-term fluctuation. From a peak in 2022 to a halving by 2025, this trend has persisted for three years. According to the German Economic Institute, Germany's automotive and parts exports fell below €14 billion last year, compared to nearly €30 billion three years ago.

As Germany's most important overseas market, China's demand structure is changing. On one hand, Chinese domestic brands are rapidly improving their product competitiveness in the new energy sector, directly squeezing the market share of German automakers.

On the other hand, Chinese consumers' preference for automotive intelligence is challenging German automakers' product definitions. Tong Oufu, CEO of Mercedes-Benz China, admitted this month: "Every sector faces price wars and new entrants, with dramatic market structure changes."

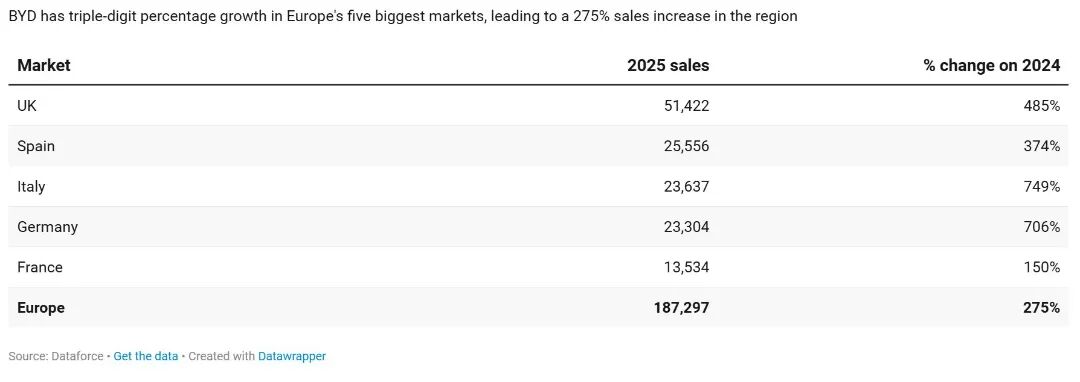

Meanwhile, Chinese brands are gaining ground in Europe. In January, amid a 3.6% decline in the overall European market, Chinese brands' sales surged by 80% to 70,465 units, with their market share rising from 4.0% a year ago to 7.4%.

SAIC's MG remained in first place with 18,537 units sold, but a 3.8% decline significantly narrowed its lead. Sales of the MG ZS compact SUV plummeted by 20%, directly impacting overall performance.

BYD sold 17,630 units in January, up 173% year-on-year, and surpassed MG in Germany with 2,069 registrations—a 1,000% increase.

Lars Bialkowski, BYD's Germany region head, stated the goal is to make Germany a benchmark market for BYD in Europe.

Chery was the fastest-growing Chinese brand, with 17,106 units sold in January, up 354% year-on-year. Through sub-brands like Jaecoo and Omoda, it is attempting to cover more market segments.

Chinese brands have formed a relatively concentrated competitive landscape in Europe. Geely Group ranked fourth with 5,079 units sold, while Leapmotor placed fifth with 4,249 units—its 409% growth rate also noteworthy.

This dynamic shift forms a crucial backdrop for Merz's visit. Before departure, he stated that fair and transparent trade is a prerequisite for successful Sino-German relations and that discussions are needed on how to address the impact of "systemic overcapacity, export restrictions, and market access barriers" on competition. These remarks were directed at both China and the German automotive industry.

02 Plug-in Hybrid Breakthrough: Precision in Technological Approach

Plug-in hybrids have played a pivotal role in this growth. In January, plug-in hybrid models accounted for 29% of Chinese brands' sales in Europe, up from 11% a year earlier. Meanwhile, plug-in hybrid sales across Europe rose 32% year-on-year in January, outpacing the 14% growth in battery electric vehicles (BEVs).

BYD exemplifies this trend. Last year, the Seal U (the domestic counterpart of the Song Plus) became Europe's best-selling plug-in hybrid with 79,518 units sold, up nearly 600% year-on-year.

In January, Seal U sales surged another 178% to 7,390 units, ranking among the top in the mid-size SUV segment, just behind the Skoda Kodiaq. This success proves that European consumers do want plug-in hybrids—they just want ones that work well.

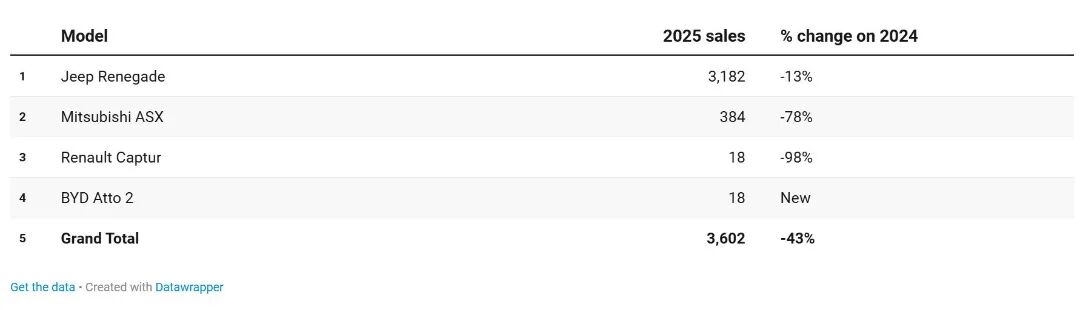

Even more strategically significant is the compact SUV market. Dataforce shows that while total compact SUV sales exceeded 2.24 million units last year, plug-in hybrids accounted for just 3,602 units—a mere 0.16% share. After the discontinuation of the Jeep Renegade PHEV and Renault Captur PHEV, this segment has become virtually vacant.

BYD plans to fill this gap with the Atto 2 PHEV (the domestic counterpart of the Yuan UP). Equipped with an 18 kWh battery, it offers around 90 km of pure electric range under WLTP conditions and over 1,000 km of combined range.

In Germany, the Atto 2 Boost version starts at €38,990. After BYD's €11,500 manufacturer subsidy and Germany's €4,500 electric vehicle subsidy, the actual price drops to €22,990. In contrast, hybrid models like the Toyota Yaris Cross and Volkswagen T-Roc in the same class start above €35,000.

However, the Atto 2's price of around RMB 186,000 is still more than double its domestic starting price of over RMB 70,000.

Florian Ulbricht, BYD's Germany product head, cited a key statistic: Only 2% of Germans drive over 100 km daily. This means the 90 km of pure electric range can meet most people's daily commuting needs. "For most Germans, 90 km of range allows them to drive in pure electric mode most of the time," he said.

This user-scenario-based product definition reflects one aspect of Chinese automakers' rising competitiveness. Another strong performer is the Seagull (known as the Dolphin Surf in Europe), which contributed 3,007 units to the micro-electric vehicle segment in January, ranking third behind the Renault R5 E-Tech and Citroën eC3. From the Seagull to the Yuan UP and Song Plus, BYD's lineup now covers about 90% of Europe's market segments.

The plug-in hybrid strategy also considers tariff factors. Currently, the EU imposes a 27% tariff on Chinese BEVs but only a 10% tariff on plug-in hybrids. Until full production capacity is reached at BYD's Hungary factory (where the Seagull and Atto 2 BEV versions will soon be produced), plug-in hybrids help mitigate the impact of trade barriers.

03 Cycle Dilemma: German Automakers' Pursuit and Challenges

German companies are not without countermeasures against Chinese brands' competition.

In localized R&D, Volkswagen, BMW, and Mercedes-Benz all have mature R&D centers in China, transitioning from "adapting for the Chinese market" to "participating in global R&D." Volkswagen's technical cooperation with XPeng and its joint venture with Horizon Robotics exemplify this trend. In 2023, Volkswagen invested around $700 million in XPeng, with plans to jointly develop two Volkswagen-branded electric models. BMW's joint venture with Thundersoft is also strengthening its localized R&D capabilities in intelligent cockpits.

In terms of technological routes, German automakers are also adjusting. Mercedes-Benz has announced increased investment in hybrid models, while BMW continues to optimize its plug-in hybrids alongside its BEV strategy. These adjustments indicate that German companies are reassessing technological trends in the Chinese market and trying to keep pace.

At the supply chain level, CATL and Eve Energy have established factories in Germany to supply batteries for European automakers, while Huawei's intelligent driving solutions are in talks with some European brands. Such technology procurement and cooperation can help European automakers shorten their catch-up period in electrification.

However, German automakers face relatively long decision-making cycles. Launching a new model typically takes 3-5 years from conception to mass production, while Chinese automakers have compressed their iteration cycles to around 18 months. This rhythm disparity means German companies will struggle to match Chinese brands' pace in the short term. Even with technology procurement and collaborative R&D to address shortcomings, organizational restructuring and mindset shifts will take time.

One of Merz's core objectives during this visit is to secure adjustment time for the German automotive industry. The German Association of the Automotive Industry had previously called on the Chancellor to discuss related issues.

From a practical standpoint, Germany has limited room to maneuver. China's new energy vehicle supply chain advantages are already entrenched and will not change due to external pressure in the short term. A more realistic path is to stabilize expectations through dialogue, ensuring German companies can still grow in the Chinese market while using localized R&D and technology procurement to address shortcomings.

During his trip, Merz will visit Mercedes-Benz's electric vehicle factory and Siemens Energy facilities—both sites sending a signal that German companies continue to invest heavily in China, and the bilateral Interest Link (interest ties) remain intact.

From a longer-term perspective, Sino-European automotive industry interactions are shifting from one-way technology transfers to two-way technological flows. German companies absorb China's intelligence experience through localized R&D, while Chinese companies validate their product definition capabilities in the European market. This interaction drives technological progress, but as cycles shift, the adjustment in offensive and defensive postures has only just begun.

Editor-in-Charge: Shi Jie Editor: He Zengrong

THE END

-

![]()

Depreciation Rate on Par with Mobile Phones: Just 40% Value Retention After Three Years—Why Do Battery Electric Vehicles Lose Their Worth?

-

![]()

Clearing Bugatti Stock Worth 7 Billion: Why is Porsche 'Cutting Ties'?

-

![]()

Don’t Dismiss Huawei’s Potential in Sedans Just Because the Shangjie Hasn’t Hit It Big Yet

-

![]()

Unsold Cars in China Find Success Overseas

-

![]()

Ghosn: Only I Can Save Nissan, Shareholders Beg Me to Return

-

![]()

Expanding Automobile Consumption: It's Time to Address the High Cost of Electric Vehicle Repairs

-

![]()

Luna Ultra Entangled in 'National Subsidy Fraud' Controversy, Insta360 Pushed to the Brink by DJI

-

![]()

People have long suffered from splash ads. Will the 'temporarily disappeared' traffic behemoth make a comeback?