Annual Earnings of 2.4 Billion and Leading in Market Share: Why is Desay SV Still Pursuing Capital Raising in Hong Kong?

04/15 2026

04/15 2026

475

475

Source: Zhiche Technology

On April 12, Desay SV formally submitted its listing application to the Hong Kong Stock Exchange, with Morgan Stanley and Huatai International as joint sponsors, thereby initiating the dual-listing process on both 'A' and 'H' shares.

This automotive electronics giant, with a market capitalization of approximately 63 billion yuan on the A-share market, currently holds the top market share in China. According to its 2025 annual report, the company achieved full-year revenue of 32.557 billion yuan, marking a 17.88% year-on-year increase; net profit attributable to shareholders reached 2.454 billion yuan, up 22.38% year-on-year, both setting new records.

However, beneath these impressive figures, two signals warrant closer attention. Firstly, the gross margin declined from 20.0% to 19.1%, with 92.6% of revenue still derived from the Chinese market. Secondly, from January 30 to April 2, 2026, Desay Group, the largest shareholder, reduced its stake and cashed out approximately 700 million yuan.

On one hand, the company reported its best-ever financial performance; on the other, a major shareholder cashed out. While it maintains the top domestic market share, its gross margins remain under pressure. What is Desay SV's strategy behind this Hong Kong listing?

Intelligent Driving Grows Rapidly, But Profits Face Challenges

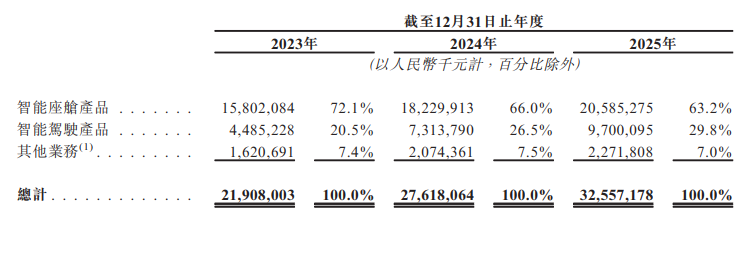

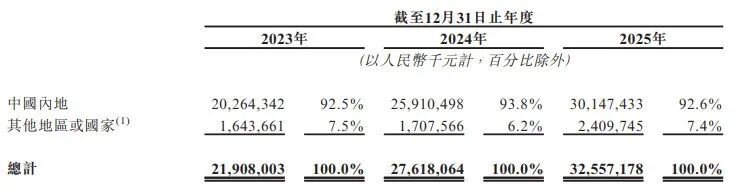

The prospectus reveals that from 2023 to 2025, Desay SV's revenue surged from 21.908 billion yuan to 32.557 billion yuan, representing a cumulative increase of 48.6% over three years, with a compound annual growth rate of 21.9%. Net profit during the same period rose from 1.542 billion yuan to 2.473 billion yuan, totaling 6.033 billion yuan in net earnings over three years. The net profit margin increased slightly from 7.0% to 7.6%, indicating limited improvement in profitability.

However, the growth trajectory is slowing: revenue growth was 26.1% in 2024 but dropped to 17.9% in 2025; net profit growth also declined from 30.9% to 22.6%.

More notably, there has been a significant shift in the business structure. The intelligent cockpit business remains the primary revenue contributor, accounting for 20.585 billion yuan in 2025, or 63.2% of total revenue. However, this share has steadily declined from 72.1% in 2023.

While the cockpit business remains the absolute mainstay, the contribution from intelligent driving is accelerating. Revenue from this segment surged from 4.485 billion yuan in 2023 to 9.7 billion yuan in 2025, representing a roughly 116.3% increase over three years, with its revenue share rising from 20.5% to 29.8%. Desay SV disclosed in the prospectus that annualized sales from new intelligent driving project orders have exceeded 13 billion yuan, while new intelligent cockpit project orders have surpassed 20 billion yuan in annualized sales.

With orders secured, growth is expected. Whether profits can keep pace remains uncertain.

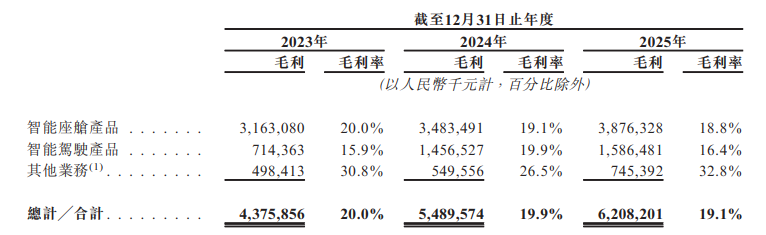

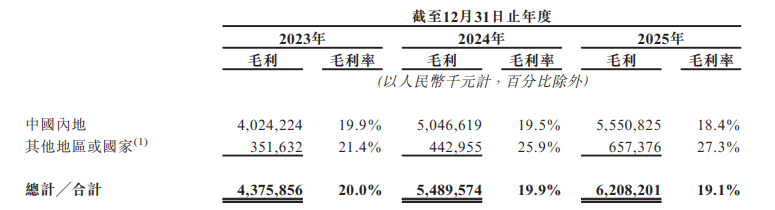

From 2023 to 2025, Desay SV's overall gross margins were 20.0%, 19.9%, and 19.1%, respectively, declining by a cumulative 0.9 percentage points over three years. The gross margin for intelligent driving products fluctuated significantly—peaking at 19.9% in 2024 before falling to 16.4% in 2025.

The reasons for margin pressure are clear: downstream, automakers' annual price reduction pressures on suppliers have increased yearly; upstream, rapid iteration in intelligent driving technology has kept R&D investment high. In 2025, Desay SV's R&D expenditure reached 2.642 billion yuan, up 17.1% year-on-year, accounting for 8.1% of revenue. The domain controller market is transitioning from a blue ocean to a red ocean, and as L2+ functions become standard rather than optional, price pressures are an inevitable consequence.

A deeper issue lies in the business model. Research by Soochow Securities points out that the foundry model with some new energy vehicle clients 'suppresses gross margins.' This suggests that during its rapid expansion, Desay SV's intelligent driving business remains more 'project-driven' than 'software product-driven,' potentially sacrificing profit margins for order scale.

Cockpit Leads, Driving Catches Up

Desay SV has delivered strong results in its core businesses.

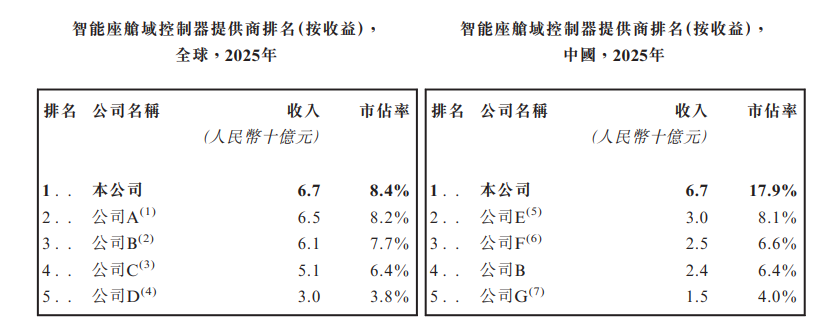

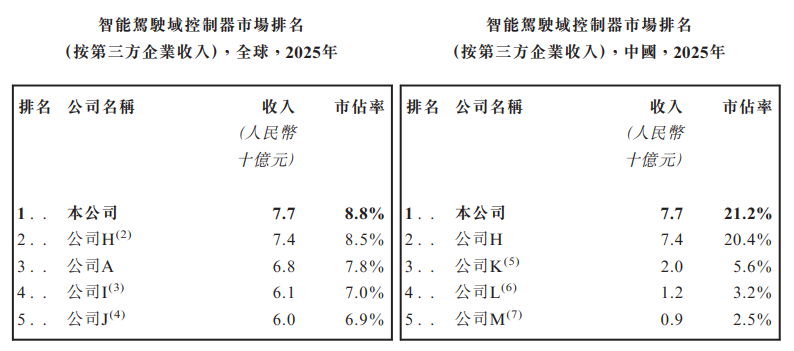

According to Frost & Sullivan data, in 2025, Desay SV ranked first in China's intelligent cockpit domain controller market with a 17.9% share by revenue and also topped the global market with an 8.4% share. For intelligent driving domain controllers among third-party suppliers, Desay SV held a 21.2% share in China and an 8.8% share globally, both ranking first. In the first half of 2025, its global market share for high-computing-power domain controller products was approximately 26.1%.

Its client roster is equally impressive. The prospectus shows that Desay SV has established business relationships with nine of the world's top ten automakers (by global sales in 2025) and all of China's top 15 automakers (by Chinese sales), with products and services covering over 80 automakers worldwide. Its client list includes domestic mainstream brands like Chery, Geely, Li Auto, Great Wall, Xiaomi, and Xpeng, as well as international automakers such as Volkswagen, Toyota, Mercedes-Benz, and Skoda.

In product iteration, Desay SV has launched multiple generations of intelligent cockpit and intelligent driving domain controllers and released integrated cockpit-driving solutions—the 'One-Chip' and 'One-Box' schemes—attempting to consolidate cockpit and driving functions within a unified architecture, aligning with the industry trend toward centralized computing platforms.

In terms of R&D, Desay SV has established research centers in China, Singapore, Japan, and Germany, forming a research network covering major markets in Asia and Europe. By the end of 2025, the company held 1,433 registered patents and 234 software copyrights in China.

Highly Dependent on Domestic Market, New Businesses Yet to Deliver

If Desay SV has a 'fatal flaw,' it is its excessive reliance on the Chinese market.

Prospectus data shows that in 2025, 92.6% of Desay SV's revenue came from mainland China. Although the company has established overseas branches in 16 countries and regions, including Germany, France, Spain, Japan, and Singapore, and its factories in Indonesia and Mexico began production in 2025, with its Spanish factory expected to start mass production in 2026, the 'going global' results have yet to be reflected in financial statements.

Customer concentration is also a concern. In 2025, the top five clients accounted for 55.5% of Desay SV's sales, with the largest client contributing 14.5%. In 2024, this ratio was even higher—the top five clients once accounted for 59.3% of sales.

The flip side of concentrated orders is fragile risk resistance. Any fluctuation or supplier switch by major clients would directly and severely impact revenue. For a Tier 1 aiming for global reach, reducing reliance on a single market and single clients may be more urgent than securing the next large order. Moreover, the relatively low penetration of intelligent technologies in overseas markets represents significant growth potential.

The dual 'A+H' listing is a crucial step for Desay SV to break out of this stalemate. The H-share listing will provide new financing channels to support overseas capacity building, R&D investment, and potential strategic acquisitions. The company disclosed that the proceeds will be used for sustained R&D in intelligent driving, intelligent cockpits, and integrated cockpit-driving solutions, as well as capacity expansion.

In the intelligent driving domain controller market, Desay SV faces no shortage of competitors.

Globally, traditional Tier 1 giants like Bosch, Continental, and Aptiv continue to strengthen their efforts; in China, automakers like Huawei and BYD are also ramping up in-house R&D. Notably, Desay SV's market share statistics for intelligent driving are limited to 'third-party suppliers'—meaning in-house developments by automakers are not counted. If more automakers choose vertical integration in the future, the potential market space for third-party suppliers could shrink.

Another concern is that new businesses are unlikely to contribute meaningful revenue in the short term.

In 2025, Desay SV launched 'Chuanxing Zhiyuan,' an autonomous delivery vehicle brand for urban logistics, and the AI Cube, an intelligent robot base, attempting to extend its automotive technology capabilities to robotics. However, the prospectus admits that as of the end of 2025, these two businesses had yet to generate substantial revenue. The company expects them to gradually enter mass production in 2026.

Technologically, transferring automotive-grade perception, computing, and control capabilities to robotics is feasible, but commercialization will take time to validate. Market interest in Desay SV's robotics business is high; at recent earnings briefings, investors frequently asked about progress in robotics and head automaker design wins for intelligent driving domain controllers, indicating market expectations for this growth space but also meaning the company must deliver tangible results in 2026.

Meanwhile, competition in China's cockpit domain controller market is intensifying. Data from Gasgoo Automotive Research shows that in 2025, Desay SV led the market with a 16.1% installation share, followed by Bosch at 8.4%, but domestic chipmakers like Huawei, Semidrive, and Chipway Technologies are rising rapidly. The latest data for January-February 2026 shows Desay SV installed 214,209 cockpit domain controllers, a 15.5% market share—still first but with a narrowing lead over the second-place competitor.

Desay SV's Hong Kong listing comes at a critical window for Chinese auto parts companies accelerating their global expansion. The A-share market has already valued it at 63 billion yuan; the H-share valuation will depend more on two variables: whether overseas operations can deliver growth expectations and whether new businesses can truly open a second growth curve.

In summary: the cockpit business is stable, intelligent driving is accelerating, globalization is still underway, and new businesses are yet to deliver.

For a company aiming to transform from a 'Chinese champion' into a 'global player,' the Hong Kong listing is not the finish line but the start of a more complex challenge.

- End -

Disclaimer:

Any works marked 'Source: XXX (non-Zhiche Technology)' in this public account are reprinted from other media, intended to disseminate and share more information, and do not represent this platform's views or endorsement of their authenticity. Copyright belongs to the original authors; please contact us for removal if there is any infringement.

-

![]()

Embrace Freedom, Live Boldly! Great Wall Motor’s Menglong PLUS Launches in the Greater Bay Area, Unlocking Enhanced Lifestyles with One Vehicle

-

![]()

The Agent hasn't arrived yet, but Ascend has already paved the way from hardware to software.

-

![]()

In 71 years, He sold products to 100 million people

-

![]()

First-hand Practical Test! Opus 4.8 Vs ChatGPT 5.5 Vs Kimi 2.6: Which is the Most Usable?

-

![]()

Fourfold Uncertainty Challenges Facing China's Agent Industry - Interpretation of the 'Report' (Part Six)

-

Crazy Anthropic

-

![]()

CNPC’s Kunlun Model Advances with 152 Implemented Scenarios, Showcasing Proactive AI

-

![]()

Revenue Increases, But Profits Don't: Pinduoduo's Anxiety Amidst Billion-Dollar Brand Building