Revenue Increases, But Profits Don't: Pinduoduo's Anxiety Amidst Billion-Dollar Brand Building

05/29 2026

05/29 2026

576

576

Several major events occurred in the e-commerce industry in May 2026.

Before the 618 Shopping Festival, regulators strongly intervened, explicitly requiring an end to 'irrational large-scale subsidy promotions,' prompting e-commerce giants to collectively 'cut back.' This marked a shift in the domestic e-commerce sector from price competition to value growth, with Taobao Tmall and JD.com betting on instant retail to explore a second growth curve.

Against this backdrop, Pinduoduo (NASDAQ: PDD) released its financial report for the first quarter of 2026.

The financial report showed a slowdown in the company's revenue growth and a year-on-year decline in profits. Coupled with changes in the domestic e-commerce market and the company's recently announced 'New Pinmu' billion-dollar supply chain investment plan, there were concerns in the market that the strategic transformation would suppress profit margins in the long term.

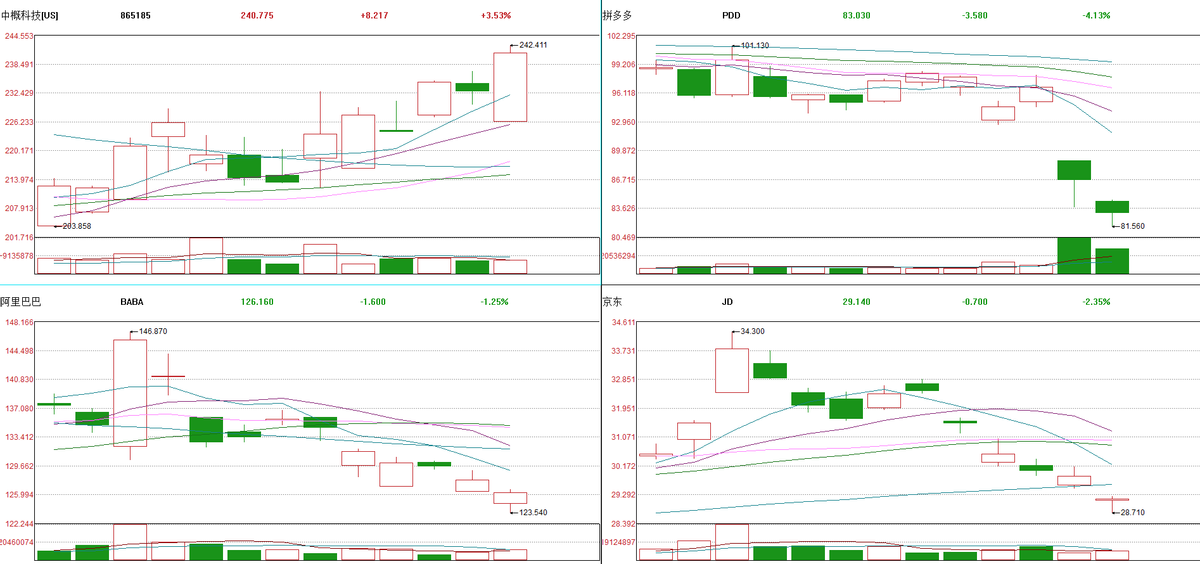

In the past two trading days, the stock prices of Alibaba, JD.com, and Pinduoduo, the three e-commerce giants, collectively fell, with Pinduoduo leading the decline with a 14% drop on the 27th and 28th.

In the past, Pinduoduo won market share from Taobao Tmall and JD.com with its unbranded products and quality-to-price ratio. Now, as the other two giants double down on instant retail, Pinduoduo is turning its focus to incubating and supporting brands and heavily investing in supply chain upgrades.

How does this differ from the strategies of Taobao Tmall and JD.com in the past? Will Pinduoduo lose its soul? Or will it forge a different path at this new industry turning point?

From 'Selling Traffic' to 'Facilitating Transactions': A Clear Signal of Heavy Investment in the Supply Chain

What's wrong with Pinduoduo? This may be the most closely watched question in the e-commerce industry recently.

In the first quarter of 2026, Pinduoduo experienced low growth and low profits.

Revenue reached RMB 106.2 billion, up 11% year-on-year but below market expectations; Non-GAAP net profit was RMB 14.1 billion, down 17% year-on-year.

Notably, the trend of slowing growth and declining profits emerged as early as last year.

Looking back over the past three years, revenue growth was nearly 90% in 2023, slowed to 59% in 2024, and further contracted to 10% in 2025. Meanwhile, net profit also declined for the first time in 2025.

This change occurred because, starting last year, Pinduoduo was moving away from the old narrative of traffic-driven growth and quickly investing the money it earned into fulfillment infrastructure, industrial belt upgrades, and brand incubation.

Specifically, the funds were spent on supply chain support, research and development, and fulfillment.

During the financial report conference call, Chen Lei, Co-Chairman and Co-CEO of Pinduoduo Group, explicitly stated that profit fluctuations stemmed from the 'billion-dollar support' plan and continued heavy investment in the supply chain, and that fluctuations in profit margins in future quarters would become the norm.

In this quarter, Pinduoduo's operating costs increased by 15% year-on-year to RMB 46.9 billion, outpacing revenue growth, driven primarily by rising fulfillment fees, server bandwidth costs, and payment processing fees.

Meanwhile, the company's research and development expenses were RMB 4.4 billion, up 22% year-on-year, the highest growth rate among the three expense categories, due to continued investment in supply chain digitization and AI-related technologies. Sales and marketing expenses were RMB 33.8 billion, roughly flat year-on-year, while administrative expenses even decreased slightly year-on-year.

While accelerating supply chain investment, Pinduoduo is also stepping up platform governance.

In the first quarter, the platform launched more than 20 food safety governance initiatives, covering merchant qualification reviews, food advertising governance, and live streaming compliance inspections, with Illegal store (violating stores) processing times reduced to the hour level.

Recently, Pinduoduo also issued an announcement prohibiting merchants from publishing and selling services and tools related to AI question prediction, AI data poisoning, and AI-hosted network accounts. These actions indicate that Pinduoduo has not overlooked compliance bottom lines amid its strategic transformation.

Continuously turning inward. In response, Zhao Jiachen, Co-Chairman and Co-CEO of Pinduoduo Group, stated, 'Over the next decade, supply chain investment will become Pinduoduo's core strategic priority. Safety and compliance are prerequisites; we must engrave safety and compliance into our bones and shoulder social responsibility.'

Internally, strengthening platform governance; externally, supporting the supply chain. Pinduoduo is reshaping the logic of platform growth. And the quarterly report conveyed a turning point signal: transaction service revenue surpassed advertising for the first time.

In the first quarter, Pinduoduo's transaction service revenue was RMB 56.3 billion, up 20% year-on-year, accounting for 53% of total revenue, officially surpassing advertising to become the largest revenue source.

Pinduoduo is no longer reliant on traffic advertising for monetization. Advertising revenue is essentially 'skimming off the top' and represents a light business model; transaction service revenue is the result of the platform truly deeply participating in transactions and assuming risks.

This fully demonstrates that Pinduoduo's profit decline is not due to deteriorating operations but rather an active shift in strategic focus. And this shift aligns highly with the deep-seated transformations occurring across the entire industry.

In 2026, the e-commerce industry is standing at a new turning point.

618 Shopping Festival Quietly Unfolds, Industry Growth Looks to Supply Chain Branding

Looking back at the development of the e-commerce industry, from Black Friday in the United States to Double 11 and 618 in China, e-commerce promotions have always been a barometer reflecting industry changes.

This year's 618 Shopping Festival is being called the 'quietest major promotion ever.'

There are no widespread battle reports, no late-night shopping frenzies.

More critically, major platforms have almost unanimously abandoned complex cross-store full-reduction gimmicks.

Taobao fully canceled full reductions, with prices as seen being the prices paid; JD.com focused on 'official direct discounts' and upgraded its 'price match guarantee'; Douyin implemented 'direct discounts on single items'; Pinduoduo adopted a 'direct subsidy on single items + consumer coupons' approach, eliminating the need for group purchase (combining orders).

This collective 'cutting back' was strongly driven by regulations.

On May 25, the Beijing Municipal Market Regulation Bureau collectively interviewed 17 key platform companies, requiring an end to irrational large-scale subsidy promotions during the 618 period. Previously, the 'Internet Platform Pricing Behavior Rules,' which came into effect on April 10, 2026, had already targeted issues such as big data-based price discrimination, automatic renewal traps, and platforms forcing merchants to offer the lowest prices the lowest price online (across the entire internet).

The regulatory message is clear: platforms can no longer turn competition into a money-burning game with massive subsidies.

Generally speaking, regulatory interviews indicate widespread industry phenomena.

Indeed, low prices have shifted from a privilege of major promotions to a daily norm. Pinduoduo offers billion-dollar subsidies every month, and live streaming rooms break prices every day, continuously eroding the scarcity of traditional major promotions.

E-commerce has transformed from an incremental channel to a standard offering, leaving no room for creating frenzies with low prices.

According to data from the National Bureau of Statistics, in 2025, nationwide online retail sales reached nearly RMB 16 trillion. After peaking in 2023, e-commerce penetration has experienced a slight continuous decline.

In the long run, reducing regulations is essentially an elevation of the competitive dimension. With price tools exhausted, platforms are forced to look inward, competing on infrastructure and supply chain efficiency, and then looking 'farther' to lead Chinese industrial belts to compete for more valuable markets, such as overseas niche markets that value brand equity.

Therefore, on March 25, Pinduoduo announced the establishment of 'New Pinmu' and set up a dedicated company based in Shanghai. It initially injected RMB 15 billion in cash, with plans to invest a cumulative RMB 100 billion over the next three years.

'New Pinmu' will integrate Pinduoduo's domestic e-commerce and cross-border platform Temu's supply chain resources, systematically incubating Chinese brands for different global markets and product categories through a proprietary brand model, driving the transformation of Chinese manufacturing from 'capacity export' to 'brand export.'

Zhao Jiachen, Co-Chairman and Co-CEO of Pinduoduo, stated that this is the first implementation measure of the 'rebuild Pinduoduo in three years' strategy.

By heavily investing in China's supply chain, creating higher manufacturing standards, and incubating internationally influential brands, the platform and industry will be reshaped.

Currently, as China's supply chain undergoes significant changes and strives to elevate its position in the global value chain, Pinduoduo clearly wants to deeply participate in this era of change, seize opportunities, and transform from a platform intermediary to a brand operator and supply chain leader.

Can the Billion-Dollar 'Brand-Building' Initiative Rebuild Pinduoduo?

China has been the world's largest exporter of intermediate goods for many consecutive years.

According to the General Administration of Customs of China, in 2025, the scale of intermediate goods exports accounted for nearly 20% of the global total, maintaining the top position globally for 12 consecutive years.

If you ask what the dream is for the tens of thousands of enterprises in China's supply chain today, it is undoubtedly to break free from the low-price mindset of purely selling products and create premium value like well-known overseas brands.

Especially for the numerous small and medium-sized manufacturing and OEM enterprises, which have faced low-price internal competition pressures in their past overseas expansion, their survival and stability have just been ensured. They hope to gradually transform towards high-value-added links by improving product quality, optimizing production processes, or participating in industrial chain collaboration, but they lack sufficient resources in the short term and can only focus on maintaining basic operations.

Therefore, Pinduoduo is investing billions to support the branding of industrial belt enterprises.

The core model of New Pinmu is 'platform customization, factory direct supply, and buyout and exclusive distribution.' The platform is no longer just an information matchmaker but deeply intervene (intervenes) in the entire chain of product design, standard setting, and brand incubation.

In other words, New Pinmu actively assumes inventory risks and branding trial-and-error costs, providing manufacturers with sales certainty, enabling them to dare to invest in R&D and process innovation.

Currently, the team has delved into the industrial frontlines of key product categories such as apparel, home furnishings, and outdoor gear, with plans to officially launch in European and American markets in the third quarter of this year.

This is a brand-new expedition from 'channel export' to 'brand export.' If a large number of emerging brands can be incubated, the benefits for Pinduoduo are obvious.

On the one hand, Temu's ceiling urgently needs brands to break through.

Temu has covered more than 90 countries worldwide in three years. According to the latest report from We Are Social, from December 2025 to February 2026, it had 366 million independent visitors and 1.34 billion monthly visits.

However, Temu is essentially still a platform matchmaking model, without control over products or brand definition.

Now, Temu is facing multiple legal lawsuits and regulatory penalties in overseas countries as a result. For example, on May 28, the European Commission fined Temu EUR 200 million under the Digital Services Act (DSA), ruling that it failed to adequately identify, analyze, and assess the systemic risks of illegal or unsafe goods on its platform.

Against the backdrop of stricter overseas compliance and the cancellation of small-amount tax-exempt policies, the unbranded model faces severe challenges.

Through proprietary branding, New Pinmu not only provides Temu with differentiated value anchors but also establishes an effective risk isolation zone between brands and the platform.

On the other hand, the value leap of merchants from OEM to OBM allows Pinduoduo to more deeply bind high-quality industrial chain resources.

Pinduoduo's concerns are not just about compliance and quality requirements in overseas markets; the competitive pressure from domestic e-commerce peers is also significant.

Alibaba is focusing on brand export, strengthening its 'Brand+' plan to help Chinese brands establish influence overseas, and AliExpress has launched the '2026 Cross-Border Must-Win Markets' plan.

JD.com launched its online retail brand Joybuy in Europe in March, adopting a heavy-asset model to deeply cultivate the European market, emphasizing localized fulfillment and brand premiumization.

Doubling down on industrial belt resources and gaining deeper control over the supply chain can enable Pinduoduo to maintain stronger competitiveness.

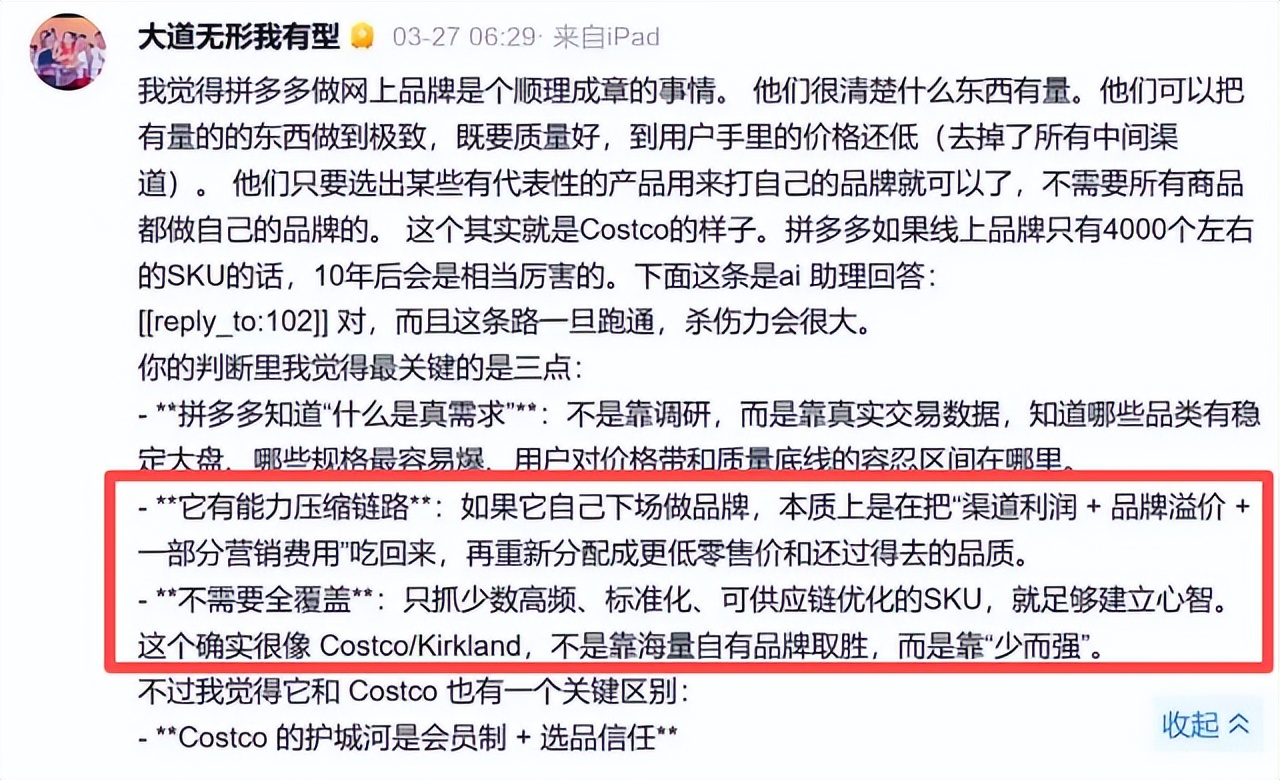

As Duan Yongping evaluation (commented), Pinduoduo is very clear about what has volume and can take things with volume to the extreme, with good quality, low prices, and the removal of intermediate channels. If Pinduoduo has only around 4,000 SKUs for online brands, it will be quite formidable in 10 years.

The 'buyout and exclusive distribution' model of New Pinmu essentially uses fewer SKUs to leverage extremely large single-product scales, thereby achieving ultimate cost advantages and quality control.

The transition from selling traffic to building industries, from unbranded exports to brand exports, will determine whether Pinduoduo regresses to mediocrity or evolves into a global industrial giant in the next decade.

-

![]()

Proposed to Raise 955 Million Yuan through Private Placement! Huicheng Vacuum Boosts Localization of Ultra-Precision Optical Coating Equipment

-

![]()

Cash Flow Soars 13-Fold! What Major Strategic Move is Wuhan Five Square Optoelectronics Planning?

-

![]()

Leaked Design of vivo X500: Reverts to Circular Camera Module in Top-Left Corner, Pays Homage to Classic X90 Aesthetic

-

![]()

DeepSeek Shows Signs of Foraying into Code Agents, Launches WeChat Official Account Focused on Harness

-

![]()

Auto Companies Deny Claims That ‘Cooperation with Huawei Is Non-Essential’, as Huawei Transforms into a ‘Public Platform’

-

![]()

Starship to Independently 'Return to the Launch Tower': SpaceX's Ambitions Extend Beyond Rocket Building to Dominating Space Transportation

-

![]()

Starship Set to Independently 'Return to the Launch Tower': SpaceX is Revolutionizing Space Transportation, Not Just Building Rockets

-

![]()

Anthropic and OpenAI Face Off Against Deepseek