Is There Really No Profit to Be Made in Car Manufacturing?

04/16 2026

04/16 2026

443

443

Author | Zhen Yao

Editor | Li Guozheng

Produced by | Bangning Studio (gbngzs)

"Currently, automakers can no longer achieve profitability by relying solely on products—that is, just selling cars."

At the High-Level Forum on Intelligent Electric Vehicle Development (2026) held on April 11, Zhao Fei, General Manager of China Changan Automobile, made this sharp and poignant remark, which encapsulates the harsh realities of the automotive industry.

Several automaker executives who attended the forum also hit the nail on the head regarding industry profitability pain points in their speeches.

"Are we destined to forever engage in domestic fight fiercely [internal competition], losing 20,000 to 30,000 yuan per vehicle sold?" asked Zhou Shiying, Deputy General Manager of China FAW Group's Strategy and Cooperation Department and Director of the Intelligent Industry Development Office.

She noted that many excellent parts companies are struggling to operate, as are Vehicle companies [OEMs]. What everyone sees is superficial prosperity, but who is actually profiting? The flow of money is uncertain.

William Li, Chairman of NIO, directly pointed out the core pain points: First, the entire industry is trapped in a cycle of increasing production without increasing revenue and sales without increasing profits; second, battery and chip costs account for over 50% of total vehicle costs, which are excessively high.

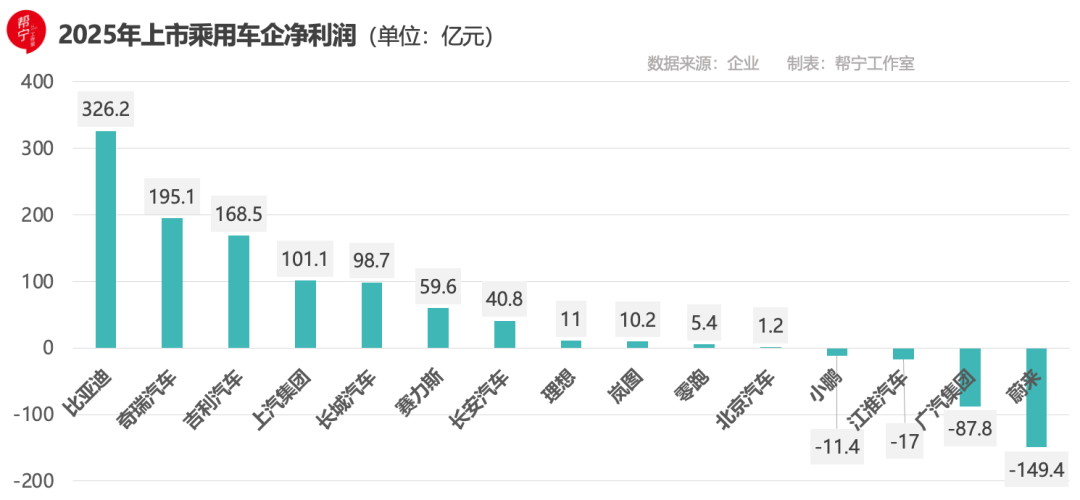

These complaints are not unfounded, as financial report data best illustrates the issue. According to Bangning Studio's statistics on the 2025 financial reports of some listed passenger vehicle manufacturers, only 11 automakers were profitable, including BYD, SAIC Motor, Geely Automobile, Chery Automobile, Great Wall Motor, Seres, Leapmotor, and VOYAH. At least four incurred losses: GAC Group, NIO, XPeng, and JAC Motors.

Even among the profitable automakers, five experienced a decline in net profit, including BYD, Great Wall Motor, BAIC Motor, Changan Automobile, and Li Auto.

The cumulative net profit of the 15 automakers in the table was 75.22 billion yuan. Meanwhile, CATL's net profit alone approached this figure, falling short by just 3.02 billion yuan.

Is there really no profit to be made in car manufacturing?

▍01 Where Did the Money Go?

Where did automakers' money go? Where did the profits go? The answer is straightforward: It was all devoured by three major issues.

First, internal competition and price wars have eroded profits.

Data from Chebaihui shows that there are currently over 30 mainstream passenger vehicle groups, more than 80 automakers, and over 230 factories in China, leading to severe overcapacity. By the end of 2025, 223 companies and 693 models of new energy vehicles were public notice [registered], but capacity utilization continued to decline—in 2024, the automotive manufacturing industry's capacity utilization rate was only 72.2%, with state-owned enterprises and new energy startups at even lower rates of 64% and 66%, respectively, leaving significant idle capacity.

"The direct consequence of overcapacity is the normalization of price wars, leaving little room for profit margins," said Zhang Yongwei, Chairman of Chebaihui.

The latest report by Cui Dongshu, Secretary-General of the China Passenger Car Association, shows that price wars are still spreading: From January to March 2026, the average price of new energy vehicle models that reduced prices was 275,000 yuan, with an average price reduction of 38,000 yuan, a 13.7% decrease; conventional fuel vehicle models that reduced prices had an average price of 258,000 yuan, with an average reduction of 37,000 yuan, a 14.3% decrease.

Some cross-industry examples intuitively illustrate the destructive power of such internal competition.

After JD.com's entry into the food delivery market in February 2025, a year-long money-burning war ensued, with JD.com, Meituan, and Alibaba (Ele.me/Taobao Flash Sale) collectively burning 170-173 billion yuan throughout the year, dubbed "the most expensive marketing war in Internet history."

As a result, Meituan's performance turned from profit to loss in 2025, with a net loss of 23.4 billion yuan and an operating loss of 17 billion yuan, including a 6.9 billion yuan operating loss in its core local commerce segment.

The logic in the automotive market is similar. Under wave after wave of price cuts, the industry's overall profit margin remains below the historical average. "Selling cars is unprofitable, and in some cases, selling one car means losing money on it" has shifted from an isolated phenomenon to a daily reality for many automakers.

Second, high supply chain costs have swallowed up profits, with money going to upstream suppliers.

"What hurts the industry most now is the rapid iteration of intelligent electric vehicles. Every time a chip is upgraded, the entire vehicle must follow suit; every time battery technology advances, the model must be updated. Supply and demand can never balance, and the 'new car effect' disappears quickly," complained Li, highlighting the industry's pain.

Worse still, batteries and chips, the two core components, account for over 50% of total vehicle costs, directly devouring most profits.

NIO is a prime example. For years, NIO relied on NVIDIA chips, with procurement costs reaching $300 million (approximately 2.053 billion yuan) annually at its peak.

Third, heavy R&D investments have not yet translated into profits.

"Automakers are investing heavily, but most of it is going into computing power, data, and model training and inference," said Zhou, noting that nearly every automaker has invested significant financial and human resources to build teams for cockpit and intelligent driving systems. While there have been sporadic achievements, core issues remain unresolved.

For many automakers, intelligent driving and cockpit systems are still fragmented—systems and data can only interact through signals and information, unable to think logically like a human brain, let alone solve "brain-cerebellum" coordination issues. The essence of automotive intelligence comprises five levels, and only by mastering these can a vehicle truly be considered intelligent.

Data underscores the scale of R&D investments. In 2025, BYD's R&D spending reached 63.4 billion yuan, up 17% year-on-year; Geely Automobile's R&D expenses were 17.6 billion yuan, up 28.75%; Seres' R&D investment was 12.51 billion yuan, a staggering 77.4% increase; Li Auto's R&D spending was 11.3 billion yuan, with half going into AI, chips, intelligent driving, and computing power.

The problem is that despite these investments, profit returns have been slow, exacerbating financial pressure on automakers.

Price war internal competition, high upstream costs, and difficulty in monetizing R&D investments—these three issues intertwine to form a logic behind disappearing automaker profits.

▍02 The Path Forward Lies in Scarce Technologies

So, how can automakers achieve profitability?

Zhou proposed that the key to breaking out lies in standardization and specialized division of labor.

She believes the industry should establish unified standardized interfaces around the integration of AI and automobiles, clarifying roles: computing power companies and OS software firms should focus on supplying technological content, while automakers should concentrate on brand building, safety, and integrating powertrains, chassis, and intelligence. "Let specialized companies do what they do best to improve overall industry efficiency."

Li offered a more specific cost-reduction path—standardizing battery cell specifications and unifying chip categories to achieve cost reduction and efficiency gains across the entire supply chain, thereby solving profitability challenges.

He estimated that promoting battery standardization and chip unification could unlock over 100 billion yuan in cost-saving potential for the entire industry.

Zhao added that from an industry trend perspective, the automotive industry is accelerating its shift from a "large industry with a small ecosystem" to a "large industry with a large ecosystem," making cross-domain, cross-entity ecological collaboration inevitable. "Future competition in the automotive industry will essentially be competition among ecosystems."

While collaborative cost reduction can alleviate short-term pressures, the true determinant of long-term automaker profitability lies not in division of labor and standardization but in the scarcity of core technologies.

Future profitability for automakers will not come from car manufacturing itself or the vehicle sales process but from scarce core technologies such as chips, autonomous driving, and power batteries, especially in the era of intelligent vehicles.

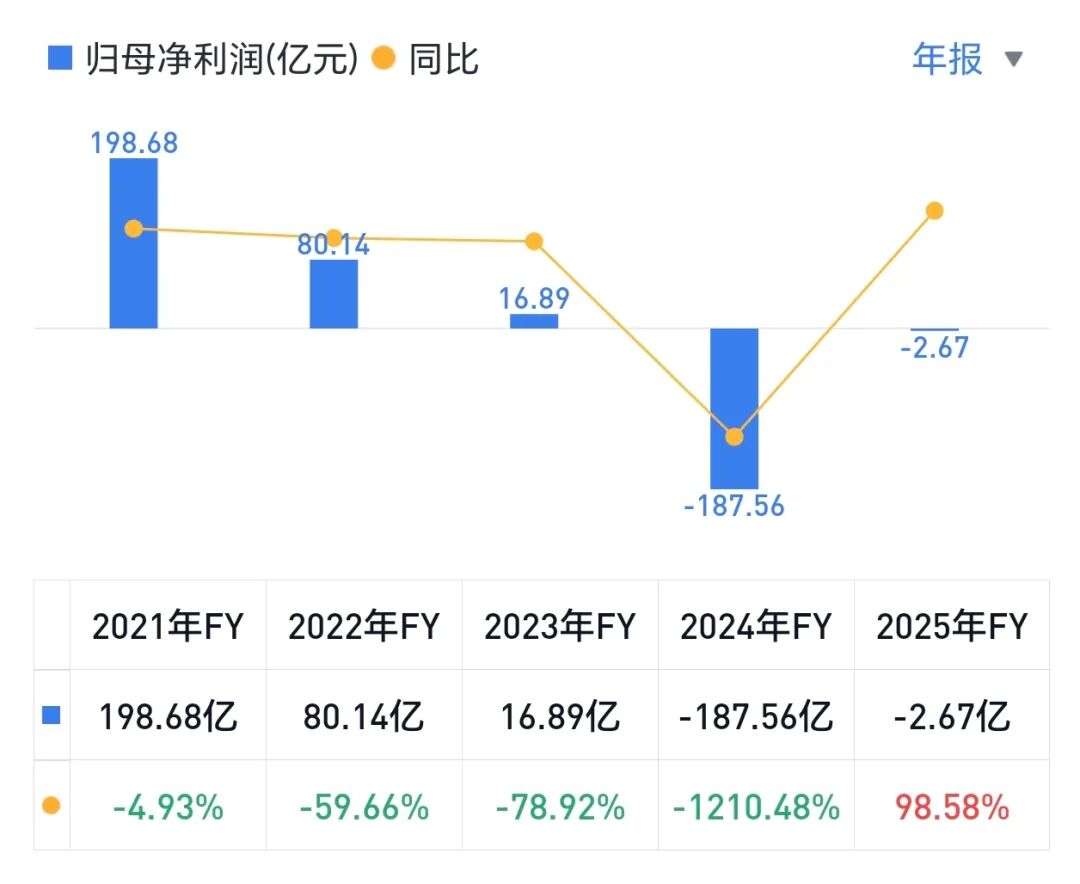

Intel's rise and fall serves as a stark warning.

Early on, Intel's technological monopoly could have kept it ahead, but instead, it chose to coast, delaying technological updates. As a result, it missed the smartphone chip boom, with Samsung and others seizing the market.

● Intel's net profit trend over the past five years / Image source: Xueqiu

● Intel's net profit trend over the past five years / Image source: Xueqiu

2017 marked a turning point for the chip industry. In Q2 of that year, Samsung surpassed Intel, ending its 24-year reign as the chip industry leader. In the GPU sector, Intel also struggled—in Q3 2017, NVIDIA's GPU sales grew 29.53% quarter-on-quarter, far exceeding AMD's 7.63% and Intel's 5.01%, propelling NVIDIA onto a rapid growth trajectory.

By June 2024, NVIDIA's market capitalization exceeded $3 trillion, surpassing Apple to become the second-highest in the U.S. stock market.

Intel's lesson is simple: Without technological innovation, the market will abandon you.

Huawei, Momenta, and CATL have long recognized this. For example, while Huawei publicly advocates "helping automakers build better cars," its core focus, from a technological standpoint, has always been on Qiankun Intelligent Driving and HarmonyOS Cockpit—key to creating technological scarcity.

With the improve [improvement] and relaxation of policies and regulations on autonomous driving, Huawei could earn more from selling autonomous driving systems and services alone than companies that merely manufacture cars. Its exploration of various models and cooperation modes aims to expand market share.

By 2025, China's motor vehicle ownership reached 469 million, including 366 million cars, with 525 million licensed drivers. The core value of this vast market lies in autonomous driving technology.

In the power battery industry, CATL's net profit has grown rapidly for five consecutive years, rising from 15.9 billion yuan in 2021 to 72.2 billion yuan in 2025, with a compound annual growth rate of 66.9%.

Huawei's performance is also noteworthy. On March 31 this year, Huawei released its 2025 annual report, showing global sales revenue of 880.9 billion yuan, up 2.2% year-on-year, and net profit of 68 billion yuan, up 8.7%.

The standout was the explosive growth of its intelligent automotive solution business. The report showed that revenue from this segment climbed rapidly to 45.018 billion yuan in just three years, up 72.1% year-on-year. This growth rate far exceeded Huawei's other core businesses, such as its ICT infrastructure business (up 2.6%), consumer business (up 1.6%), and digital energy business (up 12.7%).

Historically, computer manufacturers have never earned as much as Microsoft, which sells operating systems. Similarly, in the future, car manufacturers will not earn as much as those who control autonomous driving technologies.

Automakers without technologies will be confined to low-end market internal competition, earning meager profits and eventually being eliminated.

-

![]()

Embrace Freedom, Live Boldly! Great Wall Motor’s Menglong PLUS Launches in the Greater Bay Area, Unlocking Enhanced Lifestyles with One Vehicle

-

![]()

The Agent hasn't arrived yet, but Ascend has already paved the way from hardware to software.

-

![]()

In 71 years, He sold products to 100 million people

-

![]()

First-hand Practical Test! Opus 4.8 Vs ChatGPT 5.5 Vs Kimi 2.6: Which is the Most Usable?

-

![]()

Fourfold Uncertainty Challenges Facing China's Agent Industry - Interpretation of the 'Report' (Part Six)

-

Crazy Anthropic

-

![]()

CNPC’s Kunlun Model Advances with 152 Implemented Scenarios, Showcasing Proactive AI

-

![]()

Revenue Increases, But Profits Don't: Pinduoduo's Anxiety Amidst Billion-Dollar Brand Building