Hundreds of Brands Struggle to Hit 10,000 Monthly Sales: Despite a Surge in Orders, Maintaining 10,000 Monthly Sales Remains Tough | MINGJINGpro

05/19 2026

05/19 2026

350

350

Automakers have been on a roll lately, launching a dazzling array of new models. According to data from the China Passenger Car Association (CPCA), a total of 55 new or refreshed models hit the market from January to April this year, with 35 of them debuting in April alone. The entire industry seems to be riding the wave of a "product explosion," as if simply churning out more cars and hosting more launch events would be enough to secure a foothold in the fiercely competitive market.

However, the reality is far less rosy. Many new models quickly fade into obscurity, with only a handful achieving stable monthly sales exceeding 10,000 units. In April, domestic passenger vehicle retail sales reached 1.384 million units, marking a year-on-year decline of 21.5%. Out of the 666 models available for sale that month, only 29 managed to surpass the 10,000-unit monthly sales mark, accounting for a mere 4.35%. These top performers collectively sold 426,000 units, capturing over 30% of the total market share.

Among the models that consistently exceed 10,000 monthly sales, the disparity is striking. Only the Geely Xingyuan consistently surpasses 30,000 units. The Xiaomi SU7, Tesla Model Y, and Li Auto L6 fall within the 20,000-30,000 unit range, while the remaining 25 models cluster between 10,000-20,000 units. Notably, four of these 25 models "barely" exceed 10,000 units (less than 10,500 units), making them vulnerable to slipping below the threshold with even slight market fluctuations or the introduction of a competitive new model. Truly blockbuster models are limited to just a handful at the top.

From a powertrain perspective, new energy vehicles (NEVs) have established an undeniable dominance. Among the 29 models exceeding 10,000 units, 13 are pure electric, and 8 are pure electric + plug-in hybrid/extended-range, totaling 21 NEVs. In contrast, only 8 are fuel-powered vehicles. Among the top 10 selling models, only the Geely BinYue, a fuel-powered vehicle, holds its ground, with the remaining nine spots occupied by NEVs. The remaining 7 fuel-powered vehicles all rank at the lower end of the 10,000+ sales list. The message is clear: NEVs are rapidly expanding their market share, while the space for fuel-powered vehicles is continuously shrinking.

The price range of these 29 top-selling models is highly concentrated around the RMB 100,000 mark. As many as 18 models have starting prices below RMB 100,000, with 9 of them dipping into the sub-RMB 70,000 range. The common thread among these models is extreme cost-effectiveness—meeting core consumer demands within limited budgets. The Geely Xingyuan, for instance, offers a 410-kilometer range at a price of just over RMB 60,000. Meanwhile, the Leapmotor A10, which surpassed 10,000 units in sales just two months after its launch, brings advanced intelligent driving with lidar to the RMB 80,000 price point.

Among the models with full-series prices exceeding RMB 200,000 that achieve monthly sales exceeding 10,000 units, there are only four: the Xiaomi SU7, Tesla Model Y, Li Auto L6, and NIO ES8. The first three each exceed 20,000 units in monthly sales. At this price point, consumers shift their focus from mere cost-effectiveness to brand strength, product quality, and differentiated experiences. The NIO ES8, as the only model with a starting price exceeding RMB 400,000, speaks volumes about its value proposition.

It's worth noting that BYD holds a dominant position in the mainstream market but has yet to establish a truly stable blockbuster in the high-end segment. The Denza D9 has lost its top spot in the MPV market, and subsequent models like the N9 and N8L, while initially seeing strong sales, quickly experienced declines. The robust Fangchengbao only saw rapid growth after launching lower-priced models like the Tai 3 and Tai 7. In the high-end market, BYD seems to always fall just short.

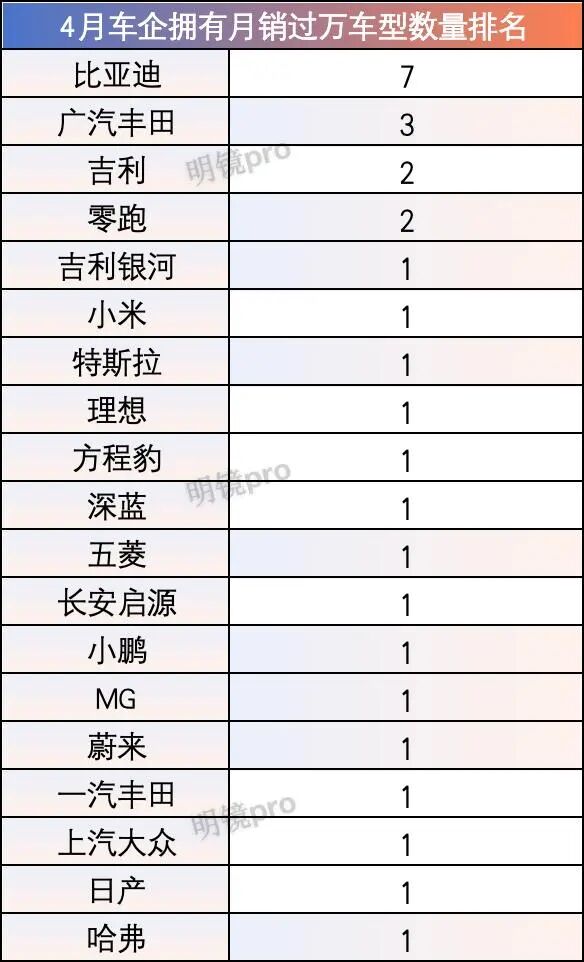

From a brand distribution perspective, the 29 models exceeding 10,000 units in sales belong to 19 brands, with independent brands securing 23 spots and joint-venture brands only 5. Data shows that there are currently over 120 brands in the domestic market, meaning at least a hundred brands lack any model achieving monthly sales exceeding 10,000 units. Among the top performers, BYD alone occupies 7 spots, and if Fangchengbao's models are included, the entire BYD Group accounts for 8 spots, fully demonstrating its scale advantage. The Geely Group has three models exceeding 10,000 units: the fuel-powered BinYue and Boyue L from the China Star series, along with the Geely Xingyuan. Changan has two models exceeding 10,000 units: the Qiyuan Q05 and Shenlan S05, while Great Wall Motors has only the Haval Big Dog.

Among the new forces, Leapmotor is the only brand with two models exceeding 10,000 units in sales: the A10 and C10. Xiaomi, Li Auto, XPENG, and NIO each have one model. Xiaomi currently has only two models, with the other, the YU7, selling nearly 10,000 units (9,876) last month, indicating that both models have the potential to achieve monthly sales exceeding 10,000 units—a feat accomplished by few brands.

The Li Auto L6 has maintained monthly sales exceeding 20,000 units eight months after its launch, breaking the industry curse of "strong initial sales followed by decline" and becoming Li Auto's new sales leader. However, other models in the Li Auto L series have experienced varying degrees of decline, with the flagship L7's sales dropping to less than 10,000 units in April, at just 5,560 units. XPENG, after launching nine models over the past few years, has only managed to produce one model, the MONA M03, that consistently exceeds 10,000 units in sales, with the rest seeing relatively flat sales after their initial launch boosts.

Among joint-venture brands, GAC Toyota has three models exceeding 10,000 units in sales: the Camry and Frontlander, both fuel-powered, and the bZ3X, a pure electric model. The bZ3X is also the only electric model from a joint-venture brand among the 29 models achieving monthly sales exceeding 10,000 units, marking Toyota's success in stabilizing its fuel-powered vehicle base while having an electric model support sales. Additionally, FAW Toyota has only the RAV4 Hongyi exceeding 10,000 units in sales, SAIC Volkswagen has only the Lavida, and Dongfeng Nissan has only the Sylphy.

Except for the aforementioned 19 brands, no other brand had a single model achieving monthly sales exceeding 10,000 units in April. Let's briefly examine a few brands with high market heat: AITO had none of its five models exceed 10,000 units in April, with its two sales leaders, the M7 and M8, selling 8,670 and 6,889 units, respectively. The Zeekr 9X and Aion i60 briefly surpassed 10,000 units in March but fell back to just over 9,000 units in April, with other models from these two brands selling below 5,000 units monthly. Lynk & Co, with 11 models available for sale, had a single-model peak sales of just 3,324 units in April, while the Lynk & Co 900, launched last year, saw its monthly sales drop below 5,000 units after six months of strong sales, further declining to just over 1,000 units last month.

Additionally, new energy brands from traditional automakers, such as ARCFOX, VOYAH, Avatr, and IM Motors, currently have overall sales just barely exceeding 10,000 units, and these figures are unstable, let alone establishing a single model with stable monthly sales exceeding 10,000 units.

Chery, following the strategy of "having more children to fight better," operates six brands—Chery, Jetour, Exeed, iCAR, Luxeed, and QQ—with approximately 40 models available for sale. However, none of its models achieved monthly sales exceeding 10,000 units in April. The closest was the QQ 3EV, with 8,493 units sold. Despite lacking a model exceeding 10,000 units in sales, Chery's multi-model strategy covers a broad market, enabling the Chery Group to rank among the top in overall sales in April, surpassing Geely and Changan, and second only to FAW Group and BYD.

Furthermore, traditional luxury brands like Mercedes-Benz, BMW, and Audi, as well as mainstream joint-venture brands like FAW-Volkswagen, GAC Honda, and Dongfeng Honda, similarly lacked any model achieving monthly sales exceeding 10,000 units in April. Of course, this analysis is based solely on April's single-month data, and sales performance for some models may fluctuate due to factors such as initial production ramp-up after launch, concentrated order releases, or being in the final stages of product replacement.

In summary, creating a model that achieves monthly sales exceeding 10,000 units is no small feat, and sustaining stable monthly sales above that threshold is even more challenging. As market competition intensifies, automakers like Geely, Dongfeng, and Changan have already begun consolidating brands and resources. The era of indiscriminate market expansion is over; the focus now should be on concentrating all resources to create truly competitive, continuously iterative, and product cycle-transcending best-selling blockbuster models, establishing a solid user reputation and brand moat.

-

![]()

JD AI’s New Frontier: Shifting from Hardware Sales to Dominating the Next-Gen Gateway Market

-

AI Becomes Baidu's Primary Growth Engine, Changing the Revaluation Logic for Chinese Internet Stocks

-

Why Have Valuations of China’s Leading AI Model Firms Suddenly Topped $10 Billion?

-

![]()

When Sports Marketing Steps into the 'Cultural Resonance' Era, What Impact Does Vatti’s Partnership with the Spanish National Team Have on the Kitchen Appliance Industry?

-

![]()

Is Kling Losing Its Affection for Its 'Parent Company' Kuaishou?

-

![]()

Should Extra-Large New Energy Vehicles Go on a 'Diet'? A Proposal for a Special Consumption Tax

-

![]()

Outpacing JD.com, Tmall Youpin Ramps Up Offline Mega-Store Expansion This Year

-

![]()

Hundreds of Brands Struggle to Hit 10,000 Monthly Sales: Despite a Surge in Orders, Maintaining 10,000 Monthly Sales Remains Tough | MINGJINGpro