Fuel-Powered Vehicles Struggle Amid Price Cuts: A Vicious Cycle

05/29 2026

05/29 2026

353

353

Lead

Introduction

Is the era of transformation for new energy vehicles (NEVs) and fuel-powered vehicles finally upon us?

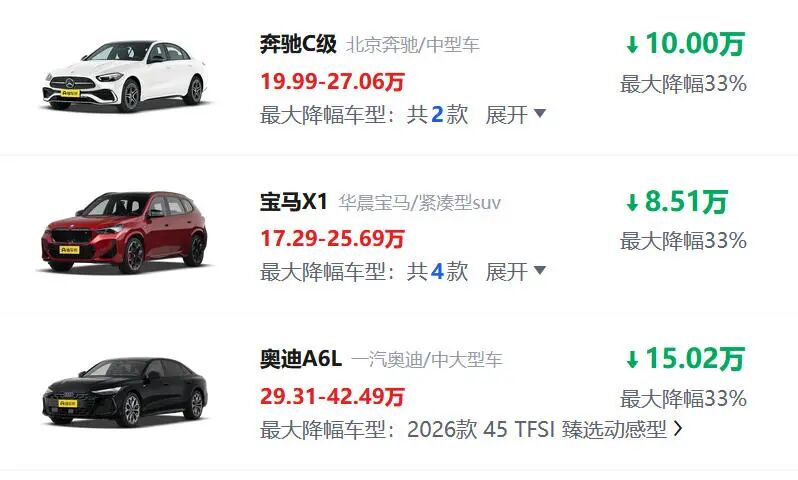

Observers of automotive market trends will have noticed that since May of this year, reports of price reductions on fuel-powered vehicles have surfaced intermittently. The trend has recently intensified, with luxury brands like BMW, Audi, and Mercedes-Benz joining the fray. The base price of a certain C-class executive sedan has plummeted to around RMB 260,000.

Mainstream brands such as Volkswagen, Honda, and Nissan are also offering substantial terminal discounts, often amounting to tens of thousands of yuan. A joint-venture A-class sedan that might have cost RMB 120,000-150,000 to purchase five years ago can now be acquired for just RMB 50,000.

But are these price cuts enticing consumers to buy?

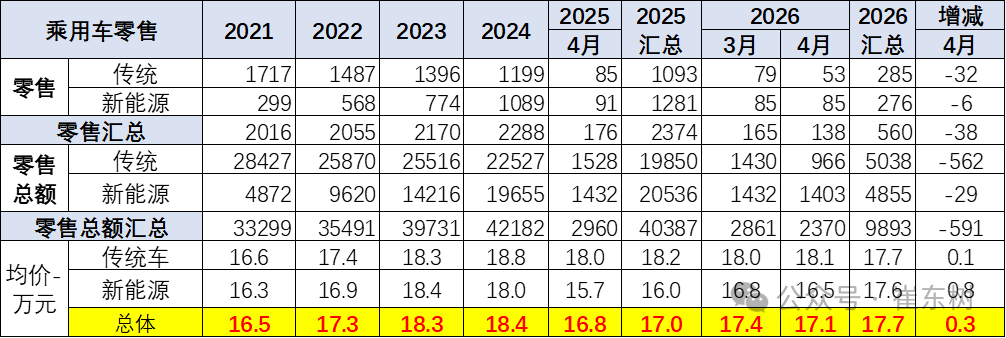

Data from the China Passenger Car Association (CPCA) reveals that in April 2026, domestic narrow passenger car retail sales reached 1.384 million units, marking a 21.5% year-on-year decline. Within this overall downturn, fuel-powered vehicles fared particularly poorly, with retail sales plummeting to 534,000 units—a staggering 37.2% year-on-year decrease and a 32.7% month-on-month drop.

In the same month, the average price of fuel-powered vehicle models that underwent price cuts was RMB 131,000, with an average discount of RMB 23,000 per vehicle, equating to a 17.2% price reduction. In essence, prices were slashed by nearly 20%, yet sales plummeted by nearly 40%. The strategy of trading price cuts for increased volume appears to be faltering.

The current reality is that the more challenging it becomes to sell fuel-powered vehicles, the more prices are slashed; and the more prices are cut, the harder it becomes to sell.

01 The Vicious Cycle of Poor Sales and Price Cuts

The most conspicuous changes are evident in sales figures. In January of this year, seven of the top ten best-selling models were fuel-powered vehicles; by February, this number had dropped to six; in March, it further declined to five; and by April, only one fuel-powered vehicle—the Geely BinYue, ranked eighth—remained in the top ten. Moreover, this eighth-place position is tenuous, with only a few hundred units separating it from the ninth-place Leapmotor A10 and tenth-place BYD Dolphin, making it susceptible to dropping out at any moment.

Even when considering the top twenty models, fuel-powered vehicles occupy only four spots. Once-popular joint-venture models like the Volkswagen Lavida and Toyota RAV4, which used to sell 20,000-30,000 units per month, have now fallen outside the top eighteen. This is not an isolated incident for a single brand or model but a widespread phenomenon affecting the entire fuel-powered vehicle industry.

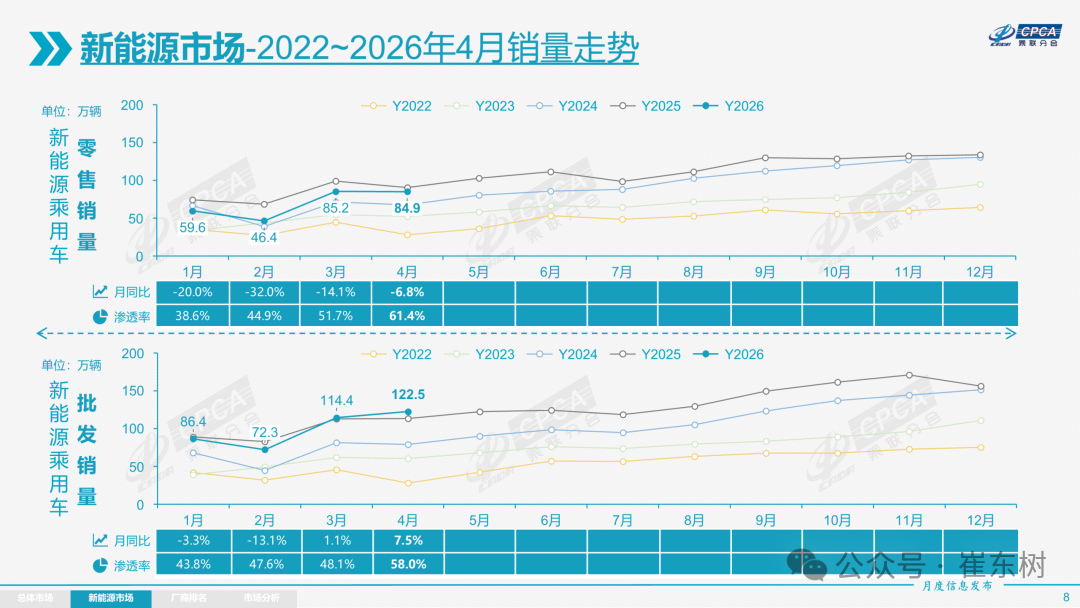

In stark contrast to the declining fuel-powered vehicle market, the new energy market is thriving. In April 2026, the retail penetration rate of new energy passenger vehicles exceeded 60% for the first time, reaching 61.4%. Cui Dongshu, Secretary-General of the CPCA, directly stated a harsh reality: The surge in new energy penetration in April was not primarily due to the exceptional sales of NEVs but because "fuel-powered vehicles declined too rapidly."

Faced with a shrinking market share, fuel-powered vehicle manufacturers have almost exclusively resorted to price cuts. From entry-level compact cars priced at tens of thousands of yuan to luxury vehicles costing hundreds of thousands, the magnitude of price reductions continues to escalate. However, these substantial promotional discounts have not resulted in a sales rebound. More critically, the driving force behind this round of price cuts has shifted.

Last year, dealers predominantly subsidized promotions with their own funds. This year, manufacturers are taking the lead. Relying solely on dealers to offer discounts has proven to have limited effectiveness and sustainability. Manufacturers stepping in personally indicates that the situation is more severe than last year, reaching a point where action is unavoidable. Moreover, the objective of manufacturer-led promotions is clear: to reduce inventory.

Yet, inventory levels have not decreased but have instead continued to accumulate. Data from the China Automobile Dealers Association (CADA) reveals that in April 2026, the comprehensive inventory coefficient of automobile dealers reached 1.89, marking a 7.4% month-on-month increase and a 34% year-on-year surge, far exceeding the safety warning line of 1.5. Behind this soaring inventory pressure lies the fact that sales velocity lags significantly behind manufacturers' push for inventory.

Based on terminal sales that month, dealers held approximately 2.6 million units in inventory. What does 2.6 million units signify? It is equivalent to more than a month's production of fuel-powered vehicles nationwide. These vehicles, languishing in warehouses, incur financial costs daily.

Among all brands, joint-venture brands face the heaviest inventory pressure, with an inventory coefficient of 2.24; luxury and imported brands' inventory coefficient has also risen to 1.99, just one step away from the psychological threshold of 2.0. In other words, a new vehicle needs to sit in a dealer's inventory for nearly two months before being sold.

Some dealers believe that manufacturers' annual sales targets are excessively high, leading not only to increased inventory but also to price inversions, where vehicles are sold at a loss. However, according to media reports, BMW, Mercedes-Benz, and Audi are adjusting dealers' sales targets and wholesale assessment criteria to varying degrees, attempting to alleviate terminal pressure.

02 Consumer Confidence Wavers

The direct boosting effect of price cuts on sales is rapidly diminishing, and there is a deeper underlying reason: consumer attitudes toward car purchases have shifted.

A set of data from McKinsey's "2026 China Automotive Consumer Insights Report" released in May 2026 is noteworthy. Among those who purchased a vehicle in the past year, 22.2% held a negative attitude toward price wars, while 19.2% believed that price wars would delay or suppress their purchasing decisions.

This has led the fuel-powered vehicle market into a vicious cycle: the more frequent the price cuts, the more consumers perceive that waiting will lead to even lower prices, prompting them to hold onto their money and delay purchases. When price cuts transition from a short-term promotional tactic to a normal expectation, their ability to stimulate demand rapidly declines and even begins to erode consumer confidence.

Besides waiting, consumer purchase intentions are also shifting. Rising fuel prices are a significant driving force. Since 2026, international oil prices have surged, with intra-year increases exceeding 50%. The per-liter prices of No. 92 and No. 95 gasoline have risen by approximately RMB 1.7 and RMB 1.8, respectively, compared to the beginning of the year. Filling a regular family car's tank now costs nearly RMB 100 more.

The sustained rise in fuel prices directly amplifies the operating cost advantage of NEVs, accelerating consumer migration. Moreover, this migration is occurring on a significant scale.

Data indicates that currently, as high as 81.2% of fuel-powered vehicle users consider NEVs when replacing their vehicles, while the proportion insisting on continuing to purchase fuel-powered vehicles has shrunk to 13.3%. This means the customer base for fuel-powered vehicles is rapidly and irreversibly dwindling.

Strategic shifts at the manufacturer level are also profoundly influencing consumer attitudes toward fuel-powered vehicles. More and more automakers are redirecting resources away from the fuel-powered vehicle segment toward NEVs. Traditional giants like Volkswagen, Toyota, and Honda, while still selling fuel-powered vehicles, have significantly slowed the pace of new product launches and allocated more R&D resources to electrification platforms and intelligent technologies.

The signal perceived by consumers is that even automakers themselves are moving toward NEVs. How long can the lifecycle of fuel-powered vehicles be?

Today, more and more consumers no longer consider whether to buy German-made or Japanese-crafted vehicles. The core factors driving purchase decisions have shifted to technical dimensions such as safety, intelligence, and electrification.

As the generational gap between fuel-powered vehicles and NEV models widens in areas such as next-generation electronic/electrical architectures, advanced driver-assistance systems, and intelligent cockpits, price competition has become the last and most feeble weapon for fuel-powered vehicle manufacturers.

The China Automobile Dealers Association pointed out in its April analysis that disrupted international oil routes and high oil prices directly reduce the sales scale of the domestic fuel-powered vehicle market. Meanwhile, factors such as weak consumer confidence and cautious household income expectations have compounded, leading to an overall contraction in terminal demand. The CPCA predicts that with oil price fluctuations, the fuel-powered vehicle market will remain weak in 2026.

It can be said that the phenomenon of fuel-powered vehicles "the harder it is to sell, the more prices are cut; the more prices are cut, the harder it is to sell" has become a long-term dilemma. The reasons behind this are neither simply cyclical fluctuations nor a life-and-death price war among automakers but a profound generational shift occurring in the automotive industry at the levels of energy pathways, technological iteration, and consumer perception.

Editor-in-Chief: Yang Jing Editor: He Zengrong

THE END

-

![]()

Embrace Freedom, Live Boldly! Great Wall Motor’s Menglong PLUS Launches in the Greater Bay Area, Unlocking Enhanced Lifestyles with One Vehicle

-

![]()

The Agent hasn't arrived yet, but Ascend has already paved the way from hardware to software.

-

![]()

In 71 years, He sold products to 100 million people

-

![]()

First-hand Practical Test! Opus 4.8 Vs ChatGPT 5.5 Vs Kimi 2.6: Which is the Most Usable?

-

![]()

Fourfold Uncertainty Challenges Facing China's Agent Industry - Interpretation of the 'Report' (Part Six)

-

Crazy Anthropic

-

![]()

CNPC’s Kunlun Model Advances with 152 Implemented Scenarios, Showcasing Proactive AI

-

![]()

Revenue Increases, But Profits Don't: Pinduoduo's Anxiety Amidst Billion-Dollar Brand Building