Li Xiang's 'Golden Moment' Has Faded: The Strategic Quagmire Behind a 3 Billion Yuan Loss

06/17 2026

06/17 2026

326

326

In the first quarter of 2026, Li Auto unveiled a financial report that sent shockwaves through the market: revenue of 23 billion yuan, a staggering net loss of 2.3 billion yuan, and a gross profit margin slashed in half.

The once-celebrated "pacesetter among new automotive forces" now appears to be confronting its most formidable challenge since inception.

Yet, the financial figures merely scratch the surface. The crux of the matter lies deeper: with the i6 as its sole standout model, the L series hitting a growth plateau, the aftermath of the pure electric MEGA recall lingering, and Li Xiang's ambitious "embodied intelligence" AI narrative yet to bear fruit—has Li Auto's strategic bedrock truly been compromised?

01 Q1 Financial Report: Unveiling the Three Truths Behind the 2.3 Billion Yuan Loss

Numbers alone are not daunting; it's the underlying trends that warrant attention.

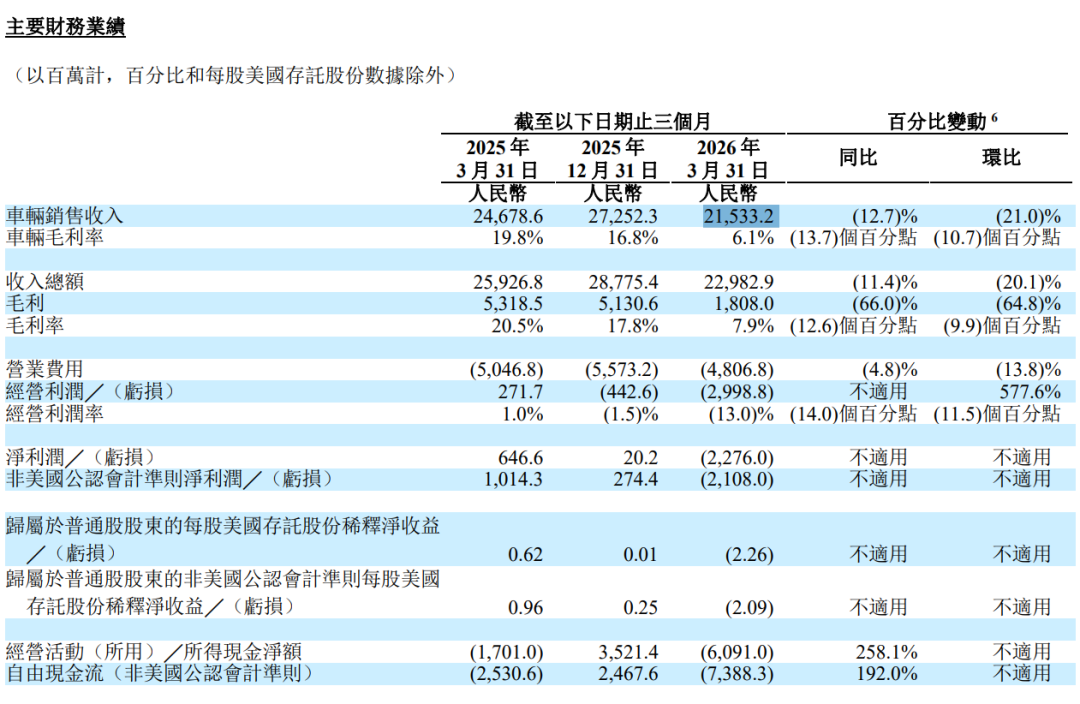

Li Auto's Q1 core metrics: revenue of 23 billion yuan, a net loss of 2.3 billion yuan (a stark contrast to the net profit of 650 million yuan in the same period in 2025 and 8 billion yuan in 2024), a halved gross profit margin, sales of 95,142 units (+2.5% YoY), and a significant decline in operating cash flow.

Source: Li Auto's Q1 2026 financial report

Three fundamental truths must be acknowledged:

Truth 1: The root cause of the loss is "pricing too low."

Li Auto's Q1 vehicle sales revenue stood at 21.5 billion yuan, a year-over-year decline primarily attributable to a lower average selling price due to a shift in product mix—the i6's blockbuster sales dragged down the average, while increased promotions for the L series further depressed the "average selling price." When a premium automaker resorts to trading price for volume, its brand moat is already crumbling.

Truth 2: Leapmotor is encroaching on the extended-range market.

In Q1 2026, Leapmotor surged to the top of the new force sales chart with 110,200 units, while Li Auto trailed with 95,142 units. Leapmotor, essentially a "budget-friendly iteration of Li Auto's model," shares a focus on extended-range technology and targets family users but at a price point 30,000–50,000 yuan lower. By bringing the threshold for extended-range SUVs down to the 150,000 yuan range, Li Auto's L series, priced between 200,000–300,000 yuan, faces pressure from both ends.

Leapmotor C16. Source: Internet

While many deride the "fridge, sofa, big TV" features, the reality is that these elements drove differentiation across the new energy vehicle market. Numerous automakers followed Li Auto's lead and achieved success, Leapmotor among them. Now that these features have become commonplace, it underscores their initial strategic significance.

Truth 3: The i6 is the "lone warrior."

Li Auto's Q1 2026 sales heavily leaned on the i6 model. The L series (once the sales mainstay) hit a growth bottleneck, while pure electric MEGA sales remained sluggish due to the recall incident. Relying on a single model for a quarter's sales is a perilous signal—it implies that other models are either uncompetitive or in a product transition phase.

Li Auto i6. Source: Internet

02 Li Xiang's Strategic Gambit: All-In on AI—Visionary Move or Strategic Blunder?

Faced with mounting sales pressure, Li Xiang opted to "redefine Li Auto through an AI narrative."

On February 5, Li Xiang announced that the new Li L9 would be a "trailblazer in embodied intelligent robots." On May 15, the Li L9 Livis was launched at 509,800 yuan, repositioned from a "premium SUV" to an "embodied intelligent robot." On June 15, Li Auto hosted "Livis Day," a software and AI event outlining standards for "qualified embodied intelligence."

Source: Internet

Is this strategic pivot justified?

The rationale is sound: Vehicles are natural platforms for "embodied intelligence"—LiDAR, cameras, chips, and wire-controlled chassis are core robot components. Competition has shifted from "electrification" to "intelligence," and homogeneous batteries, motors, and range are no longer sufficient. AI also serves as a "premium shield"—the 509,800 yuan Livis needs "AI premium" to compete with the 498,000 yuan NIO ES9 and Seres M9, as configuration and size alone are insufficient.

However, the misalignment is evident: The AI narrative is premature, and the market is not yet convinced—consumers paying 500,000 yuan seek "today's luxury," not "tomorrow's robot." AI features currently lack a "generational edge"—Li Auto's intelligent driving gap with XPeng, Huawei, and NIO is narrowing, not widening, and the perception of being "industry-leading" has not been established. There is no clear consensus on how much consumers are willing to pay for intelligent driving—the L7 at 300,000 yuan and the L9 Livis at 500,000 yuan may differ by only 50,000–100,000 yuan in intelligent driving, yet the Livis costs over 200,000 yuan more.

Source: Internet

Thus, Li Auto's "all-in on AI" feels more like a "necessary gamble"—when traditional hardware differentiation has plateaued, AI is the only avenue left to craft a new narrative. Yet, the chasm between "telling the story" and "buying into it" remains vast.

03 The L Series' SKU Quagmire: 4 Models, 10+ Configurations, 260,000 Yuan Price Band

This is the most underestimated "internal time bomb" for the Li L series.

Current Li L series SKUs (by model × configuration):

Total: ~11 main SKUs (L6: 2 + L7: 2 + L8: 3 + L9 old: 3 + L9 Livis: 1), spanning 249,800–509,800 yuan—a nearly 260,000 yuan range, effectively two distinct price bands.

Problem 1: Severe price overlap between adjacent models.

The L6 Max (279,800 yuan) vs. L7 Pro (301,800 yuan) differs by only 22,000 yuan; the L7 Max (359,800 yuan) vs. L8 Pro (321,800 yuan) sees the L7 Max priced 38,000 yuan higher; the L8 Ultra (379,800 yuan) vs. L9 Pro (409,800 yuan) differs by 30,000 yuan. At dealerships, customers grapple with tough questions: "What's the difference between the L6 Max and L7 Pro for 22,000 yuan? Why is the L7 Max 38,000 yuan more than the L8 Pro? Should I choose the L8 Ultra or L9 Pro for just 30,000 yuan more?"

Source: Li Auto official website

The answer: Aside from size and seating (L7: 5 seats, L8: 6 seats, L9: full-size), core configurations are nearly identical—same extended-range system, same intelligent driving hardware, same interior style. The result is Li Auto effectively trains customers to "choose by seating," but the actual experience difference is far smaller than the price gap—leaving all non-L9 SKUs in a state of "cost-effectiveness self-doubt."

Problem 2: Severe dilution of brand perception.

When a brand sells four models covering a 260,000 yuan range, its "user persona" becomes ambiguous: L6 buyers view it as "just a commuter tool," L7 buyers seek "space," L8 buyers require "6 seats for three generations," and L9 buyers crave "premium." These groups contribute vastly different "mental tags" to the brand. When you spot a Li Auto on the street, you can't discern if it's a 300,000 yuan or 500,000 yuan model—this "price ambiguity" automatically erodes the brand's premium appeal.

Problem 3: Severe internal cannibalization.

The four L series models cannibalize each other's sales, with L7 and L8 suffering the most: The L6 lures entry-level L7 buyers ("Why buy the L7 when the L6 Max is just 279,800 yuan?"), while the L9 Pro entices L8 Ultra buyers ("The L9 Pro is only 409,800 yuan, 30,000 yuan more than the L8 Ultra but with a 5m+ length, 6 seats, and higher specs."). L7 and L8 are trapped in the "middle layer"—pressed by the L9 above and the L6 below, making them increasingly marginalized. Only the L6 (low price) and L9 (flagship) sell well, while L7 and L8 fade into obscurity.

Problem 4: The L9 Livis pushes "refresh" difficulty to the limit.

The May 15-launched L9 Livis (509,800 yuan) is Li Auto's "AI strategic flagship"—but also the toughest L series refresh. The price gap is wider: the old L9 ranged from 409,800–439,800 yuan, while the Livis jumps to 509,800 yuan, widening the price band by 70,000–100,000 yuan for the same model name. AI features aren't fully realized: The Livis is positioned as a "pioneer in embodied intelligent robots," but its AI narrative was only half-told at the June 15 "Livis Day" event. Competitors are closing in: The 509,800 yuan Livis faces direct competition from the 498,000 yuan NIO ES9 and Seres M9, a intensity far beyond the 250,000 yuan segment where the L6 competes.

Source: Li Auto official website

Root cause: Li Auto's product strategy essentially uses "SKU quantity to compensate for product strength."

The "too many SKUs" issue stems from homogenized product strength—the L6/L7/L8/L9 differ little in core powertrains, intelligent driving, or interiors, forcing "formal differences" through size, seating, and configurations. Pricing is passive: Each new model's pricing must avoid "owner protests" and "cannibalizing siblings," leading to ever-finer price segmentation. There's no real technological edge: The i6's pure electric architecture hasn't "spilled over" to the L series, leaving it to rely on "old platform + reskinning."

This means Li Auto's problem isn't "too many SKUs" but "product strength can't support SKU differentiation."

04 Late-Stage Trends in the New Energy Vehicle Market: Saturation, Differentiation, Globalization

Trend 1: The market is saturated; the "growth narrative" is over.

By 2025, new energy passenger vehicle penetration exceeded 50%, and 2026 entered a "zero-sum game"—every automaker's growth comes at the expense of others, not market expansion. This explains why Leapmotor and Li Auto are "cannibalizing" each other—the pie isn't growing, so whoever takes a bigger slice wins.

Source: Internet

Trend 2: Premiumization is the only path, but the bar has risen to "AI-level."

The 100,000–200,000 yuan segment is divided among Leapmotor, BYD, and Geely Galaxy, while the 300,000+ yuan market is reshuffling. To stabilize in the 300,000+ yuan segment, automakers must offer "visible, tangible, and show-off-worthy" differentiation—AI intelligent driving is the easiest story to tell but also the easiest to catch up to.

Trend 3: Global expansion is China's new energy "second curve."

<The first-quarter loss of 2.3 billion RMB is a result of the interplay among product cycle dynamics, promotional strategies, and strategic investments in AI, rather than an indication of the collapse of the company's core operations. However, this loss does reveal a more profound challenge: Li Auto is shifting from a "high-growth phase" to a "strategic adjustment phase." The days when Li Auto could rely solely on the L9 model to dominate the market are gone. Future competition will pivot on multiple models, maintaining generational leads in intelligent driving technology, expanding overseas, and bolstering strategic depth. Li Auto is placing its bets on AI to redefine the automotive landscape. Similarly, Leapmotor is betting that cost efficiency can redefine pricing strategies, and BYD is wagering that overseas expansion can redefine market dynamics. The company that successfully navigates these challenges will shape the industry's future by 2027.

- END -

-

Trillion-Dollar Commercial Space Industry: Profits Start Not with Rockets

-

![]()

Baidu Netdisk Encounters a 'Significant' Challenger: Tencent Netdisk Makes Its Debut

-

![]()

Tencent Cloud Drive: A Rising Contender to Baidu Cloud

-

![]()

AR Optical Leader Quietly Achieves 1 Million Units in Mass Production!

-

![]()

Raising 289 Million for Optical R&D! Olight Technology Prepares for GEM IPO

-

![]()

【OFweek Weike Cup】Cybernetics Officially Nominated for the 2026 Outstanding Contribution Award for Optical Industry Application Solutions

-

![]()

Precocious Ideals, Rebuilding A New Ideal

-

![]()

DeepSeek Finally Accepts 50 Billion Yuan in Funding