Who Will Dominate the Global Stage for Chinese Automakers in 2026?

07/08 2026

07/08 2026

386

386

For the first time, Japanese automakers are experiencing genuine apprehension in the face of global competition.

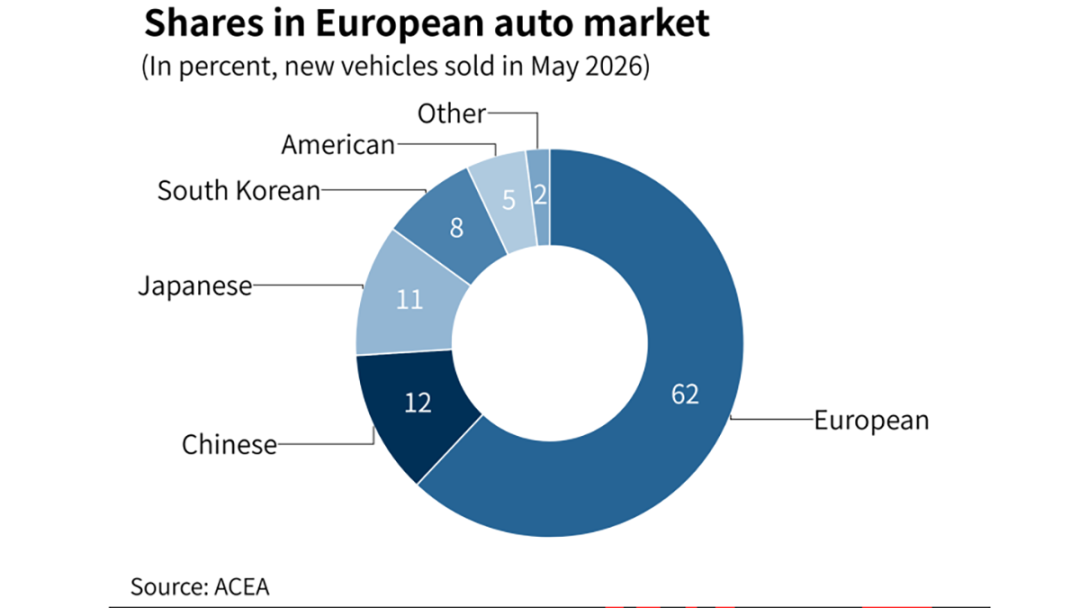

As the first half of 2026 draws to a close, with more statistical reports emerging, Chinese automakers have set a series of new benchmarks. Data from the ACEA (European Automobile Manufacturers Association) in May revealed that in 31 major European countries, five Chinese automakers—BYD, SAIC, Geely, Chery, and Leapmotor—collectively sold 138,400 new vehicles, marking a year-on-year increase of 65%. This figure surpassed the combined sales of six Japanese automakers by over 5%. Toyota, Nissan, Suzuki, Mazda, Honda, and Mitsubishi sold a total of 130,400 vehicles, experiencing a year-on-year decline of 3%.

According to another metric, in the narrowly defined EU-27 market, the year-on-year increase in new car registrations for the five major Chinese automakers in May exceeded 60%. By various measures, Chinese automakers have, for the first time in history, outperformed their Japanese counterparts.

Undoubtedly, the significance of this data transcends mere numbers; it represents a head-to-head contest in the world's third-largest automotive market.

Three Tiers: Who Wields the New Global Influence?

It's not just about collective achievements; individual automakers are also pushing their boundaries.

Chery Automobile: Overseas sales constitute over 70% of the group's total sales, with four consecutive months of breaking China's monthly automobile export records. Monthly exports have also exceeded 190,000 vehicles for the first time.

BYD Auto: Monthly overseas sales of passenger vehicles and pickups reached 174,900 units, setting a new internal record and closely trailing Chery.

Geely Auto: Monthly overseas sales surpassed 100,000 units for the first time, reaching 102,900 units in June. Its growth rate is astonishing, with overseas new energy vehicle sales reaching 277,200 units in the first half of 2026, a year-on-year increase of 585%.

Changan Automobile: The proportion of overseas sales is steadily rising. In June, for instance, total sales were 201,900 units, with overseas sales accounting for 91,000 units, nearly half of the total.

Great Wall Motors: The proportion of overseas sales has also begun to approach 50%, with overseas sales of 291,400 units in the first half of the year, accounting for nearly 50% of total sales of 583,800 units.

SAIC Motor: It has also set new sales records in Europe, with the MG brand retaining its title as China's best-selling brand in Europe for the 11th consecutive year.

In addition to traditional automakers, new energy vehicle startups are also witnessing rapid growth.

Leapmotor: Overseas sales in the first half of the year approached 100,000 units, surpassing its total sales for 2025 and overtaking XPENG to become the leader in overseas sales among new energy vehicle startups.

XPENG: Monthly overseas sales continue to climb, with overseas deliveries exceeding 8,000 units in June. Its sales target for 2026 is set at 90,000 to 100,000 units.

From a numerical standpoint, Chinese automakers in overseas markets can currently be categorized into three tiers:

The first tier is led by Chery, with overseas sales of 943,800 units, marking the first time in Chinese automotive history that half-year exports exceeded 900,000 units. BYD ranks second with nearly 790,000 units in overseas sales for the first half of the year, and SAIC Motor ranks third with over 730,000 units.

The scale difference between the second and first tiers is approximately 50%. Geely Auto sold over 470,000 units in the first half of 2026, with notably rapid growth, potentially exerting pressure on SAIC Motor's annual sales. Changan Automobile's half-year overseas sales were 402,000 units, while Great Wall Motors' were 291,000 units.

The third tier comprises Leapmotor and XPENG. Leapmotor plans to expand its dealer network to 500 locations in 2026, while XPENG has already expanded its overseas sales and service network to 380 stores across 60 countries and regions. Both are expected to swiftly narrow the gap with the second tier.

From a model perspective, Chery's current export sales are dominated by fuel-powered SUVs, primarily the Tiggo 7 and Tiggo 8. BYD's top export models in the first half of the year were the Yuan PLUS and the BYD Dolphin.

Geely's top export models are the Galaxy Starship 7 and the Geely EX2 (known as the Xingyuan in China). Changan Automobile's sales are led by the fuel-powered CS55PLUS and CS75PLUS, as well as the growing popularity of the Deepal S05 in Southeast Asia's new energy sector. Great Wall Motors' main models are the Haval H6 and Great Wall Cannon. Leapmotor's current best-seller is the Leapmotor T03, while XPENG's is the XPENG G6.

Considering regional and national dimensions, competition is less intense than in the Chinese domestic market, with generally lower friction, meaning that market focuses are temporarily less overlapping. Chery dominates the Middle East, Great Wall Motors leads in Eastern Europe, BYD currently holds sway in the Brazilian market, and MG is the sales champion in Europe. However, with BYD's Hungarian factory expected to commence operations in the fourth quarter, the sales crown in 2027 may change hands.

Although MG is a British brand with strong consumer recognition, BYD's expansion is remarkably swift, with an expected doubling of sales points in Europe by the end of 2026 compared to the end of 2025, reaching around 2,000 locations.

Additionally, Chery Automobile is actively adjusting its strategic deployment, having already surpassed the Middle East market in Europe in the first half of 2026.

In summary, Chery, Great Wall Motors, and Changan Automobile hold sway in fuel-powered vehicles in different markets, while BYD, Geely, and MG dominate the pure electric and plug-in hybrid segments across various regional niche markets.

More Than Just Numbers or Prestige

The surge in overseas markets is a necessary phase for Chinese automakers. Early European, American, Japanese, and Korean automakers all underwent similar processes. This is because all emerging markets transition from incremental to stock markets, and automakers need to expand externally for sustained development. This principle applies not only to manufacturing but also to the internet or AI industries.

Of course, the current influence only reflects present performance and does not necessarily indicate trends for 2027 and beyond.

Therefore, to deeply assess the overseas potential of Chinese automakers, the focus should be on factories (or overseas production capacity) and sales and service networks.

Chery Automobile has 10 KD assembly factories overseas, with over 1,500 dealers and nearly 3,000 dealer outlets. Additionally, it is set to take over Nissan's former factory in Sunderland, England, with production expected to start as early as April 2027.

BYD Auto had planned up to 13 overseas factories, with current operations in Thailand, Brazil, and Uzbekistan. By the end of 2026, it is expected to have over 2,500 dealer outlets. Regarding its second European factory, it is currently in the final stages of site selection and decision-making, with company executives expressing a personal preference for acquiring existing idle factories in Europe.

SAIC Motor currently has four major manufacturing bases overseas (in Thailand, Indonesia, India, etc.) and plans to have its first European manufacturing factory operational by the end of 2028, with over 3,000 dealer outlets.

Geely Auto has 20 overseas factories globally, with over 1,100 overseas sales and service outlets.

Changan Automobile has established nine major overseas factories, with plans for 20 overseas factories and a global dealer network exceeding 14,000 outlets.

Great Wall Motors has 16 factories overseas and over 1,500 overseas sales channels.

Leapmotor currently has its international factory in Poland in operation and is expanding strategic cooperation in Europe in 2026, seeking to take over dual factories in Spain. It has approximately 950 overseas sales and service outlets, with 85% located in Europe.

XPENG manufactures through Magna in Austria and has 380 overseas stores.

In conclusion, in terms of planning, Changan Automobile has the largest scale. In terms of efficiency, BYD, Chery, and SAIC Motor are currently the best. In terms of potential, Geely Auto and Leapmotor are the most promising.

All of the above is not just about who captures their territory first but also a visible export of China's competitiveness in three electric areas and intelligence following the competition in the Chinese market. Moreover, these efforts will further return to and benefit the domestic market.

The explicit advantage is that, after experiencing more complex road conditions and usage scenarios, the maturity of the product is expected to upgrade very rapidly in the facelift. For instance, the usage environment in the Southeast Asian market is characterized by high temperatures and humidity, while in the UK market, it is cold and damp. In the Brazilian market, road conditions are often poor and damp, whereas in Eastern Europe, the environment is cold with relatively poor road conditions.

In fact, since the first large-scale expansion overseas, there has been significant feedback regarding product stability. For example, Great Wall Motors currently enjoys a strong reputation for quality, giving Wei Jianjun the confidence to proclaim 'peace of mind' at product launches.

Of course, in addition to this, there is still room for upgrades in areas such as the three electric systems (battery, motor, and electronic control) and AI. In terms of the three electric systems, for example, charging facilities are not well-established in many regions of Italy. Regarding intelligence, it will have to wait for the gradual release of data and regulations, at which point domestic systems will have the opportunity for further upgrades.

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry