Three Generations of 'Kings of Online Ride-Hailing': BAIC, Aion, and BYD All Want to Move On | MIRROR Pro

07/08 2026

07/08 2026

546

546

What you can't have is always in turmoil, but once you become the king, you can cut ties without fear. This is the attitude of automakers toward the online ride-hailing market.

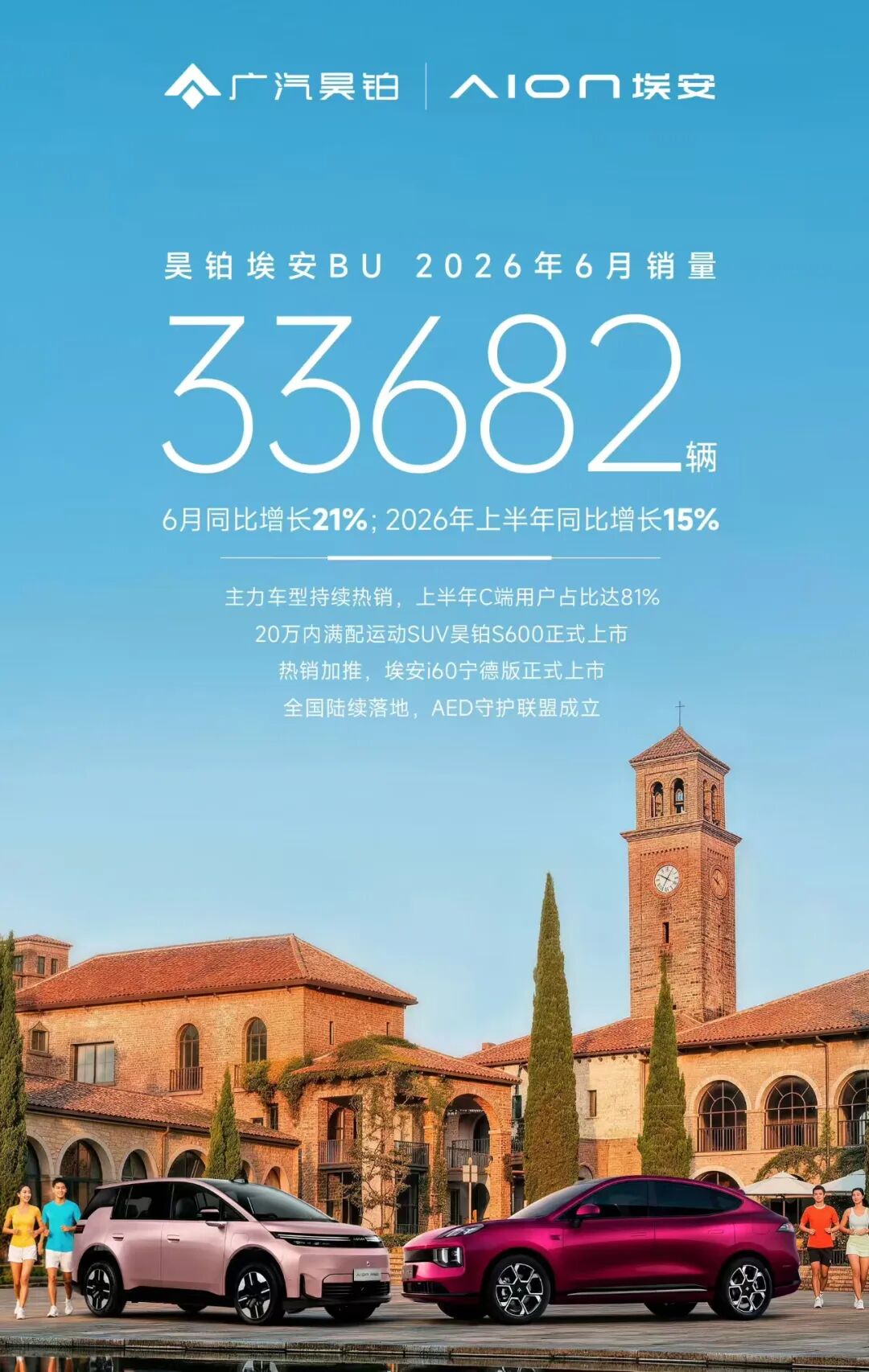

In Aion's sales report in early July this year, the 'King of Online Ride-Hailing,' which emerged even earlier than BYD, specially (deliberately) highlighted in its report card the 'continuous improvement in the proportion of C-end individual retail sales, reaching 81%.' The intention behind this could not be clearer. When individual users make up the vast majority, it means that Aion's transformation, which began in 2022 to reduce its B-end market share and expand its C-end market, has been successful. As a result, the label of 'King of Online Ride-Hailing'—a title that is both loved and hated—will be removed from its brand, and it will truly enter a new stage of development.

Online ride-hailing is an unavoidable topic for new energy vehicle brands targeting the mainstream market in their early development. Over the past decade, three brands have emerged as the kings of China's online ride-hailing market: BAIC New Energy, Aion, and BYD.

Founded in 2009, BAIC New Energy was the first independently operated new energy vehicle company in China. It secured the first 'birth certificate' for new energy vehicles and officially listed on the A-share market in 2018, becoming the 'First Share of New Energy Vehicles in China' (Stock Name: BAIC Blue Valley). In the early stages of electric vehicle development, private consumer acceptance was low, so automakers focused on expanding the B-end market. Against this backdrop, BAIC New Energy quickly gained traction through financial subsidies and B-end business opportunities, such as public transportation orders (e.g., taxis) in Beijing and other cities, as well as orders from sharing platforms.

Beginning in 2012, it became the sales champion in China's pure electric vehicle market, a record that lasted until 2019. At its peak, BAIC New Energy even accounted for 23% of China's new energy vehicle market share. By securing a large number of orders in sectors such as taxis, ride-hailing, time-sharing leasing, driver training vehicles, and police vehicles, its B-end business accounted for over 70% of sales at its peak, making BAIC New Energy the first-generation king of new energy ride-hailing vehicles. At the same time, BAIC New Energy's sales exceeded 100,000 units and quickly climbed to the top of global sales—yes, surpassing Tesla at the time.

Of course, this also laid the groundwork for BAIC New Energy's future challenges. Since the first-generation electric vehicles were primarily based on retrofitting internal combustion engine vehicles and offered a poor user experience, they damaged the brand's reputation in the mobility market. This made it even more difficult for BAIC New Energy to break through in the C-end market. At the same time, its low-price, high-volume product strategy led C-end consumers to stereotype it as a brand exclusively for ride-hailing vehicles—failing to achieve the goal of building a reputation for reliability and durability through the mobility market. Around 2018, BAIC New Energy began a planned transformation, but progress was slow.

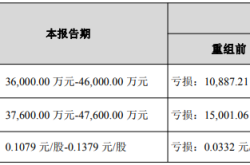

In 2019, as new energy vehicle subsidies declined, BAIC New Energy experienced a rare sales drop. That year, its sales reached 150,600 units, down 4.69% year-on-year. Then, during the three years of the pandemic, its sales plummeted. In 2020, cumulative sales were only 25,900 units, a sharp decline of over 80% compared to 2019. In 2020, BAIC Blue Valley reported a net loss of 6.482 billion yuan, turning from profit to loss. The reasons included: the concentrated launch of first-generation electric vehicles; secondly, after the outbreak of the pandemic, sales of ride-hailing vehicles, taxis, and other B-end businesses nearly ground to a halt.

After BAIC New Energy fell from its throne, GAC Aion took over. Founded later than BAIC New Energy, GAC Aion benefited from being a latecomer. In 2017, GAC Aion was established. That same year, it launched the GEP1.0, a pure electric platform centered around 'batteries,' ensuring that its products were built on a pure electric platform from the start, giving them a significant advantage in user experience. This propelled Aion's rapid growth in the market. From 2019 to 2022, GAC Aion's annual sales were 42,000, 59,500, 120,200, and 271,200 units, respectively. In 2023, GAC Aion's annual sales reached 480,000 units, up 77.02% year-on-year.

Of course, in this process, competition for the mobility market was also essential. From 2018 to 2019, as major automakers launched their own mobility platforms, GAC's OnTime quickly propelled Aion to become a major force in the ride-hailing market. The AION S and AION Y models became new 'favorites' in the ride-hailing market. In 2021, GAC Aion's B-end sales accounted for over 43% of its total. Among them, the AION S and AION Y accounted for 63.01% and 20.33% of B-end sales, respectively. In 2023, data released by the China Passenger Car Association showed that 848,000 new vehicles were sold in China's ride-hailing market, with GAC Aion selling approximately 219,000 units, capturing a 25% market share. BYD sold 191,000 ride-hailing vehicles in 2023, ranking second.

Like BAIC New Energy, Aion also became concerned after ride-hailing vehicles accounted for over 40% of its sales. To reduce its reliance on the ride-hailing market, starting in 2021, Aion took a series of measures to lower its B-end market share and avoid repeating BAIC New Energy's mistakes. For example, it launched the Aion S Plus to replace the original Aion S, which had been labeled as a ride-hailing vehicle, and introduced the Aion Y and Aion V to boost the C-end share of the Aion brand. In September 2022, GAC Aion launched its luxury pure electric brand, Hyper, aiming to make a clean break.

However, Hyper's final sales proved the strategy unsuccessful. On the product side, Aion continued to make adjustments. But as the ride-hailing market gradually became saturated and competition intensified, GAC Aion's sales growth in the B-end market began to falter. This led to a sales decline for Aion in 2024 and 2025. In 2024, GAC Aion launched a new 'AION' letter logo and introduced three global C-end strategic models, boosting the C-end sales share. In 2025, GAC Aion initiated a comprehensive B/C-end brand separation strategy internally, creating exclusive models, channels, and operations for different user groups. According to previous reports, this B-end brand was expected to be launched in June 2025, but it has yet to materialize. The reasons remain unclear.

Judging by its performance in the first half of this year, Aion's sales have rebounded, with C-end sales making up the vast majority, indicating that its transformation is complete.

After Aion, BYD took over as the 'King of Online Ride-Hailing,' even going to greater extremes. Of course, due to BYD's massive overall sales volume, its proportion was not as exaggerated as BAIC New Energy or Aion, but its absolute numbers far exceeded Aion's peak. Moreover, BYD was the earliest company to specifically develop ride-hailing vehicle models. In its product lineup, models primarily used for commercial operations include the e6 (developed specifically for the taxi and ride-hailing market), Qin EV, e3, D1 (a dedicated ride-hailing vehicle developed in collaboration with Didi), e9, Qin PLUS EV, Denza D9 EV, Han EV, and Yuan PLUS.

BYD has generated numerous anecdotes in the ride-hailing market in recent years, truly becoming the 'King of Online Ride-Hailing.' As early as 2023, BYD models accounted for over 40% of newly added ride-hailing vehicles in China, with the Qin PLUS DM-i winning the ride-hailing market sales championship for three consecutive years. Subsequently, BYD's sales continued to soar, and its products were favored by the ride-hailing market due to their low prices. Unlike Aion and BAIC New Energy, although BYD's proportion was smaller, its ride-hailing vehicle inventory and sales were enormous, making it synonymous with 'ride-hailing' in both public opinion and the market.

This 'reputation' clearly became a burden for BYD. In 2025, BYD planned to launch a dedicated ride-hailing brand, 'Linghui,' to completely separate it from the parent brand. This is because, for BYD, which has already achieved annual sales of over 4.5 million units, elevating its brand is the next logical step. Moreover, as the automotive price war comes to a halt, BYD is shifting toward higher quality overall. Unlike BAIC New Energy and Aion, BYD has deeper pockets, allowing it to make a clean break when facing such issues.

Whether it's BAIC New Energy, Aion, or BYD, all three automakers have benefited from the massive demand in the ride-hailing market but quickly cut ties with it, viewing it as a threat. However, in reality, companies like Toyota, Hyundai, Mercedes-Benz, BMW, and Audi all hold significant shares in their home country's taxi markets, and this has not hindered their brand development. For Chinese automakers, there is no shortage of new brands today, but many have very short lifespans. This means that competition among Chinese automakers largely remains focused on configurations and parameters, devolving into price wars.

A quote from William Li, chairman of NIO, earlier this year is worth pondering. Li said that the automotive industry has now moved from point-based competition to systemic competition. Brand, as a crucial part of systemic competition, continues to gain prominence in value. As technologies converge and products become increasingly homogeneous, users may have once chosen based on parameters, but now they are increasingly choosing based on brand.

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry