Seres, Once a Profit Leader, Shifts from Gains to Losses in H1: It’s Not Entirely Huawei’s Fault | MIRROR Pro

07/14 2026

07/14 2026

527

527

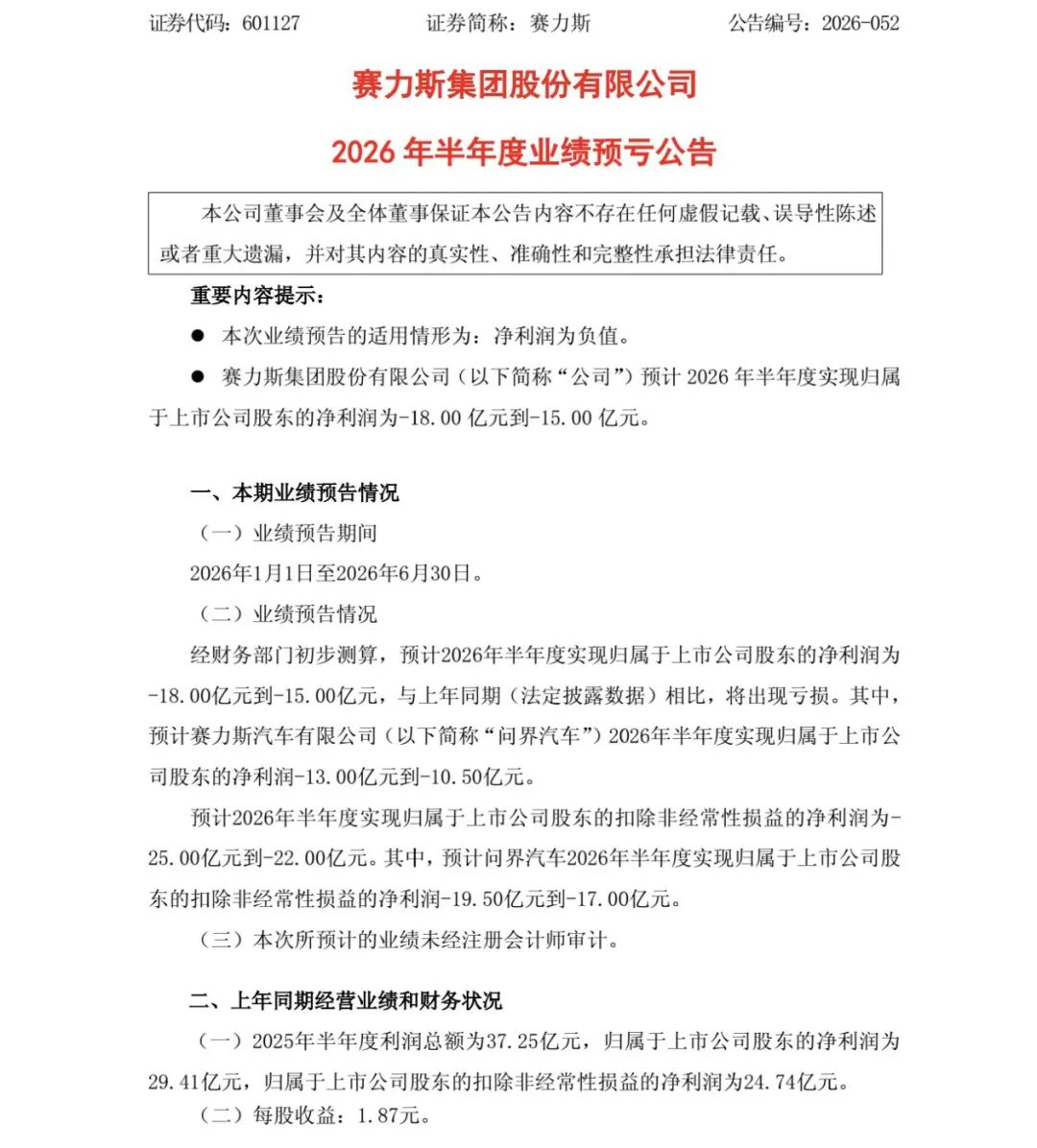

Seres, which reported profits in Q1, unexpectedly announced a loss in Q2. On the evening of July 12, Seres Group Co., Ltd. revealed it expected a net loss attributable to shareholders of listed companies ranging from RMB 1.5 billion to RMB 1.8 billion for the first half of 2026, a stark contrast to the RMB 2.941 billion net profit recorded in the same period the previous year. The non-GAAP net loss attributable to shareholders is projected to be between RMB 2.2 billion and RMB 2.5 billion. Notably, AITO, its flagship asset, also reported a rare loss. According to the announcement, Seres anticipates Seres Automotive Co., Ltd. ("AITO Automotive") to report a net loss attributable to shareholders of listed companies ranging from RMB 1.05 billion to RMB 1.3 billion for the first half of 2026, with a non-GAAP net loss estimated between RMB 1.7 billion and RMB 1.95 billion.

This news swiftly stirred up a commotion. It marks the first quarterly loss for Seres since it turned profitable in Q1 2024 following its partnership with Huawei. On July 13, Seres' A-shares opened at the daily limit down, while its Hong Kong-listed shares plummeted by 13.72%, both marking their largest declines in the past year. Clearly, the capital market was caught off guard by Seres' losses. The "surprise" from the outside world is understandable:

Firstly, AITO currently boasts the highest gross profit margin in China's automotive industry and stands as the most profitable automaker. Data indicates that Seres' gross profit margin surged to 26.21% in 2024. In 2025, it peaked at 29.1%, and in Q1 2026, it stood at 26.2%, second only to Ferrari and Aston Martin among major global automakers and significantly surpassing the industry average of around 15%. During the same period, BYD's gross profit margin was 20.49%, XPeng's was 12.8%, Li Auto's was 17.9%, and NIO's was 14.6%. A high gross profit margin typically signals strong pricing power, underscoring AITO's premium market position.

After divesting loss-making businesses like Landian, Seres' listed assets are predominantly AITO, streamlining its asset portfolio.

Secondly, Seres' performance in Q2 was not lackluster, with sales on the rise. Data shows that AITO's sales increased sequentially in H1 2026. In Q1, Seres' core AITO brand delivered 70,200 units, while in Q2, it delivered 90,600 units. From an operational standpoint, its net profit was RMB 754 million in Q1 but is expected to range from a loss of RMB 1.8 billion to RMB 1.5 billion in Q2 2026. This marks the first quarterly loss since Seres became profitable in Q1 2024 following its collaboration with Huawei. Despite an overall sales increase, operations shifted from profitability to a loss, which was unexpected.

Seres' official explanation cites two primary reasons: Firstly, escalating costs. In its announcement, Seres attributed the losses to increased production costs stemming from rising prices of key raw materials such as memory chips, industrial metals, and lithium carbonate. In June of this year, Zhang Xinghai, Chairman of Seres Group, stated at the 2026 China Automotive Chongqing Forum that automakers face numerous challenges, with the most significant being the fivefold increase in memory chip prices. Meanwhile, lithium carbonate prices rose from RMB 80,000 per ton last year to RMB 180,000 per ton this year. He added that as a result, the average manufacturing cost per AITO vehicle increased by RMB 15,000 to RMB 20,000.

Of course, if we calculate based on the maximum cost increase of RMB 20,000 per vehicle, costs rose by up to RMB 1.8 billion in Q2 this year.

Another factor contributing to the Q2 loss is that Seres recognized some "additional costs" early on. In its performance forecast, Seres stated that, based on prudence and considering the expected future returns of assets, it adjusted the book value of certain existing assets with limited adaptability due to technological iterations and model replacements. This refers to asset impairments for outdated models, essentially recognizing them all at once. Seres has not yet disclosed the specific amount of these asset impairments, which is expected to be revealed in its H1 financial report in August. However, this indicates that Seres' overall performance would have been significantly better without this move.

Seres' share price has been under pressure this year, with its Hong Kong-listed shares falling 60.9% and its A-shares dropping 54.99% year-to-date. For Seres, its current market value has reverted to 2024 levels. In this low-expectation and overall declining capital market environment, Seres opted to concentrate the release of its "bad performance news." This strategy can hedge against future performance expectations and pave the way for a rebound in the second half of the year.

On the other hand, the current decline in Seres' performance is often attributed by many to the "Huawei tax": On one hand, they believe Huawei is extracting too much from Seres, leading to its performance decline; on the other hand, they argue that the proliferation of Huawei-branded products has eroded AITO's pricing power.

According to previous disclosures, since partnering with Huawei to build cars in 2021, Seres has paid Huawei over RMB 75 billion in procurement fees in just three and a half years, with RMB 20 billion in H1 2025 alone. Some analysts point out that Huawei charges AITO models a total fee of about 10%, including 8% for marketing and distribution and 2% for technology licensing. This means that for an AITO model with an average price of RMB 400,000, RMB 40,000 is paid just for these two items.

However, it cannot be overlooked that Seres' successful transformation and the success of the AITO brand are both attributed to Huawei's support.

Public information reveals that Seres' collaboration with Huawei commenced in 2019. The two sides launched their first model, the Huawei Smart Selection SF5, in April 2021, which also became the first model to enter Huawei's sales network. Financial reports show that from 2019 to 2022, Seres' net profit attributable to shareholders were RMB 66.7215 million, -RMB 1.729 billion, -RMB 1.824 billion, and -RMB 3.832 billion, respectively. Including 2023, its net losses over four years reached RMB 9.4 billion to RMB 10 billion. However, Seres became profitable starting in 2024.

It is easy for outsiders to attribute Seres' losses to its collaboration with Huawei, but in reality, without Huawei, Seres' path to the premium market would have been exceedingly challenging. At least, before partnering with Huawei, Sokon had already tried for three years.

In 2016, Sokon Holdings established an R&D center in Silicon Valley, USA. In 2017, it acquired a factory from AM General in the USA and founded SF MOTORS. Later, Jinkang New Energy launched the JinKang brand in China. In 2019, Jinkang New Energy rebranded to Seres, with its first model retaining the name SF5 from SF MOTORS. Data shows that from 2017 to 2019 alone, Sokon Holdings invested over RMB 6 billion in equity investments related to new energy vehicles, with more than two-thirds directly invested in Jinkang New Energy.

After partnering with Huawei, Seres found a clear direction despite its high expenditures. In 2022, although Sokon Holdings was still incurring losses, Zhang Xinghai, Founder and Chairman of Sokon Holdings, stated, "Even if BMW approached me now to discuss a joint venture for car manufacturing, I wouldn't do it. I would unwaveringly pursue cross-border cooperation with Huawei." At that time, there were still two years to go before the first profitability following the collaboration with Huawei. This underscores the transformation and confidence that the collaboration with Huawei has brought to Seres. Even from a business performance perspective, Seres has earned over RMB 12 billion in profits in two years, essentially recovering its cumulative losses from the previous years within that period.

Therefore, attacking Huawei at this juncture is futile and serves to sow discord between Seres and Huawei. If Seres were to leave Huawei now, its development would only become more arduous. Of course, relying solely on Huawei is also not viable. For any company, establishing diversified profit channels is crucial to hedge against risks. Hence, after divesting Landian, Seres also chose to collaborate with ByteDance to create Saido Technology, attempting to replicate a new AITO.

-

![]()

HK$340 Billion Wiped Out in 4 Months, Founder Takes 'No Salary' Pledge: What’s Ailing MiniMax?

-

It's Time to Tally the ROI for Tokens

-

![]()

WPS, with 678 Million Users, Seeks Equilibrium Between Revenue Growth and User Experience

-

![]()

Seres, Once a Profit Leader, Shifts from Gains to Losses in H1: It’s Not Entirely Huawei’s Fault | MIRROR Pro

-

![]()

Why Google Remains 'Others' After 16 Years in the Smartphone Business

-

![]()

The Theory of Distillation Threat

-

![]()

Iterative Communication in Automotive Electronics: ADI's Innovative AB, GMSL, and EB Solutions

-

![]()

Despite AITO’s Explosive Sales, Why is Seres Still Struggling Financially?