Despite AITO’s Explosive Sales, Why is Seres Still Struggling Financially?

07/14 2026

07/14 2026

556

556

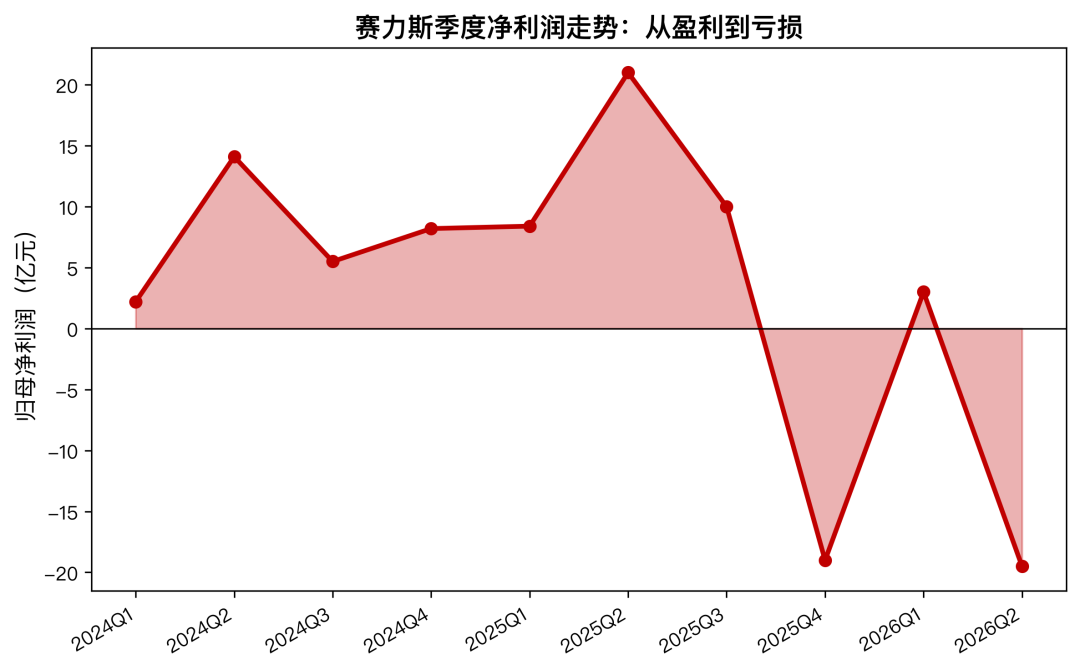

On July 12, 2026, Seres released a performance forecast that sent shockwaves through the market.

The net profit attributable to shareholders for the first half of the year is projected to incur losses ranging from 1.5 billion to 1.8 billion yuan, with net losses from non-recurring profit and loss items estimated between 2.2 billion and 2.5 billion yuan.

Just a year prior, in the first half of 2025, the company had reported a net profit of 2.941 billion yuan, with non-recurring profit and loss contributing a net profit of 2.474 billion yuan.

In a mere 12 months, the company's financial situation deteriorated from profitability to significant losses, with a staggering gap of nearly 5 billion yuan.

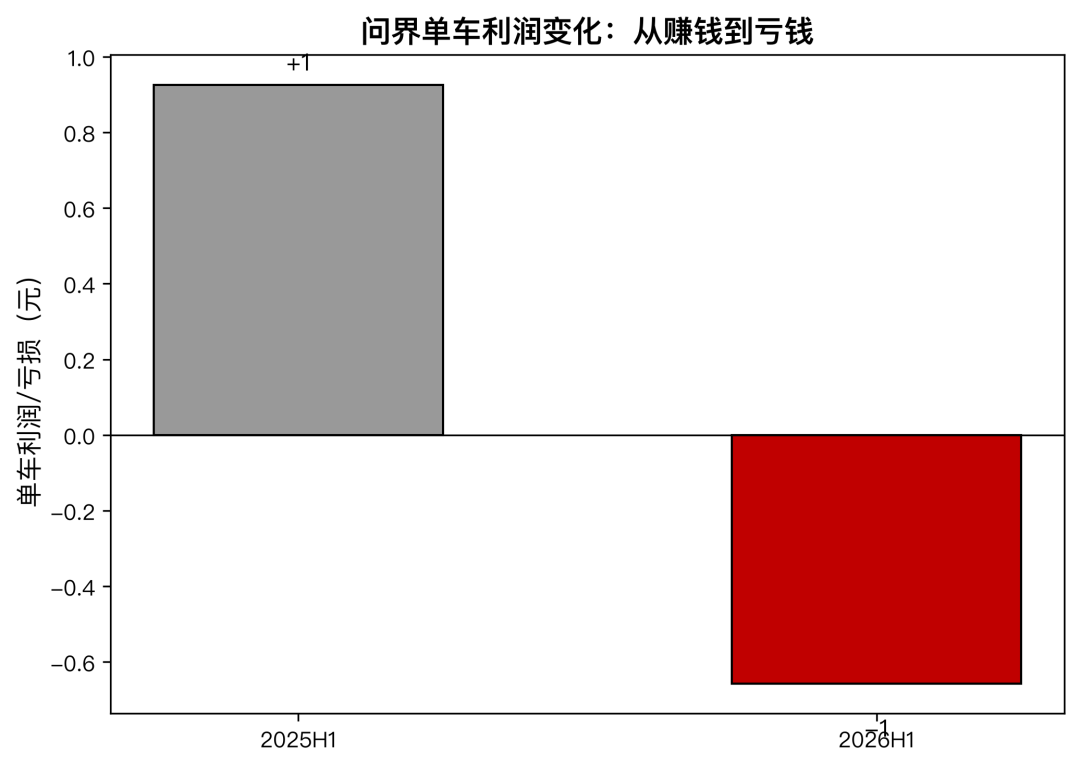

The performance of its core subsidiary, AITO, is even more striking.

The announcement revealed that AITO incurred losses between 1.05 billion and 1.3 billion yuan in the first half of the year, with second-quarter losses alone ranging from 1.9 billion to 2.15 billion yuan. Essentially, any meager profits earned in the first quarter were completely wiped out by the second quarter.

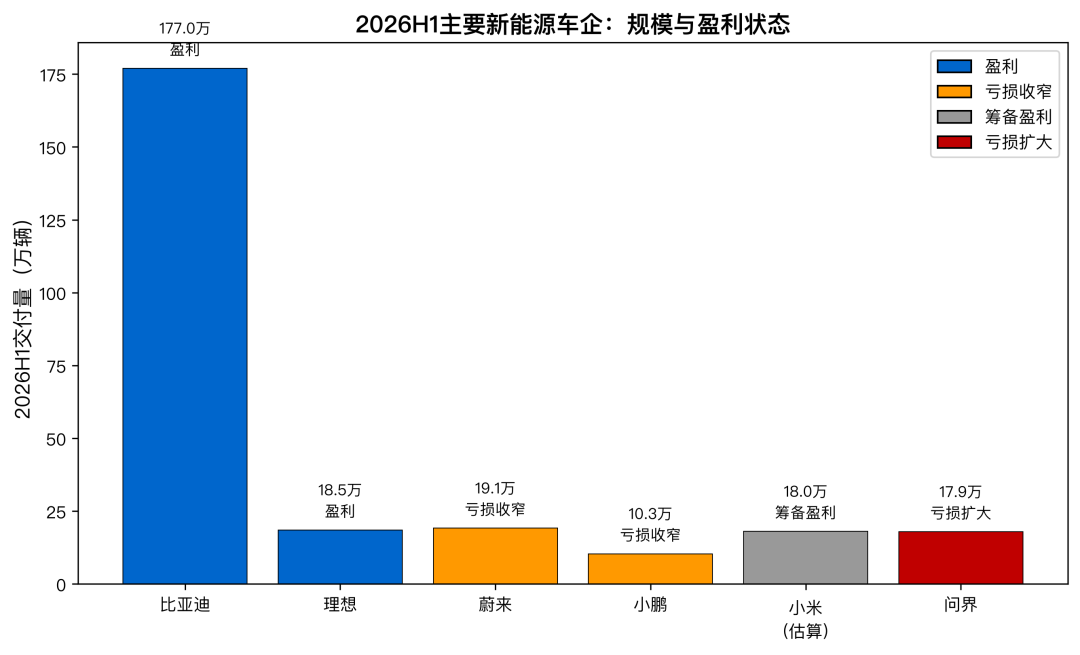

The paradox here is that sales have not plummeted. From January to June 2026, Seres' sales of new energy vehicles reached 178,800 units, with AITO deliveries increasing by 10.2% year-on-year. The new M9 model received over 42,000 firm orders within a month of its launch, while the M6 surpassed 30,000 deliveries in just 54 days. By any standard for new energy vehicle (NEV) startups, these sales figures are impressive.

Sales are on the rise, yet profits are in the red. This underlying dynamic warrants closer examination.

1. Financial Indicators Suggested Losses Were Imminent

Seres attributes its losses primarily to two factors: escalating raw material costs and asset impairments.

At the raw material level, memory chips, industrial metals, and lithium carbonate experienced widespread price hikes in the first half of the year.

Lithium carbonate prices rebounded from approximately 70,000 yuan per ton at the end of 2025 to over 100,000 yuan, while memory chip prices surged due to increased demand from the AI sector. Industrial metals like copper and aluminum remained at elevated levels, all contributing to higher vehicle manufacturing costs.

Regarding asset impairments, Seres adjusted the book value of certain existing assets that had limited adaptability due to "technological iteration and model upgrades."

In simpler terms, certain molds, production lines, and component inventories for older M5 and M7 models required impairment charges due to the launch of new models or upgrades to intelligent driving systems.

While both factors are valid explanations on their own, their combined impact reveals deeper structural issues.

Rising raw material costs are a challenge faced by the entire industry. In the first half of 2026, companies like BYD, Li Auto, Xiaomi, and XPeng all expanded production and encountered similar upstream cost pressures.

Yet, the outcomes varied significantly: Li Auto has been profitable since 2024 and earns money on every vehicle sold; BYD continues to scale its profits through vertical integration; NIO, while still incurring losses, has narrowed its deficit; Xiaomi Auto, the fastest-growing player, has a clear path to profitability. Only Seres saw its net profit turn negative despite experiencing sales growth.

This suggests that rising raw material costs were not the primary culprit but rather the final straw that broke the profit camel's back.

The real issue lies in Seres' weak resilience to cost fluctuations.

2. AITO's Dilemma: Growth Without Profitability

The phenomenon of sales growth coupled with profit decline—known as "growth without profitability"—is not uncommon in traditional manufacturing. It occurs when companies slash prices, offer promotions, and ramp up R&D to capture market share while being unable to pass on upstream cost increases, resulting in selling more vehicles but losing more money in the process.

AITO's situation, however, is more nuanced.

On one hand, it leverages Huawei's intelligent driving systems and brand endorsement to establish strong product competitiveness in the 250,000–500,000 yuan price range. On the other hand, Huawei's empowerment comes at a significant cost.

Huawei's chips, sensors, and software licenses are technologically sophisticated but expensive. AITO's core selling point is its "Huawei content," which inherently implies a high-cost structure.

As industry price wars intensify, with competitors like Li Auto, Xiaomi, and BYD cutting prices, AITO faces a dilemma: if it follows suit and lowers prices, its gross margins will shrink; if it maintains prices, sales may decline.

The first-half 2026 financials reflect the consequences of the latter strategy. By maintaining prices, AITO preserved its sales growth, but with no room to compress costs further, profits were devoured.

Digging deeper, AITO's product iteration speed is accelerating. The M5, M7, M8, and M9 form a dense product matrix, with ADS upgrading from 3.0 to 4.0. While rapid iteration helps sustain product freshness, it also accelerates the depreciation of molds and components for older models, exposing Seres' inexperience in asset management and capacity planning.

AITO has brand recognition and cutting-edge technology but has yet to translate its scale advantages into cost advantages.

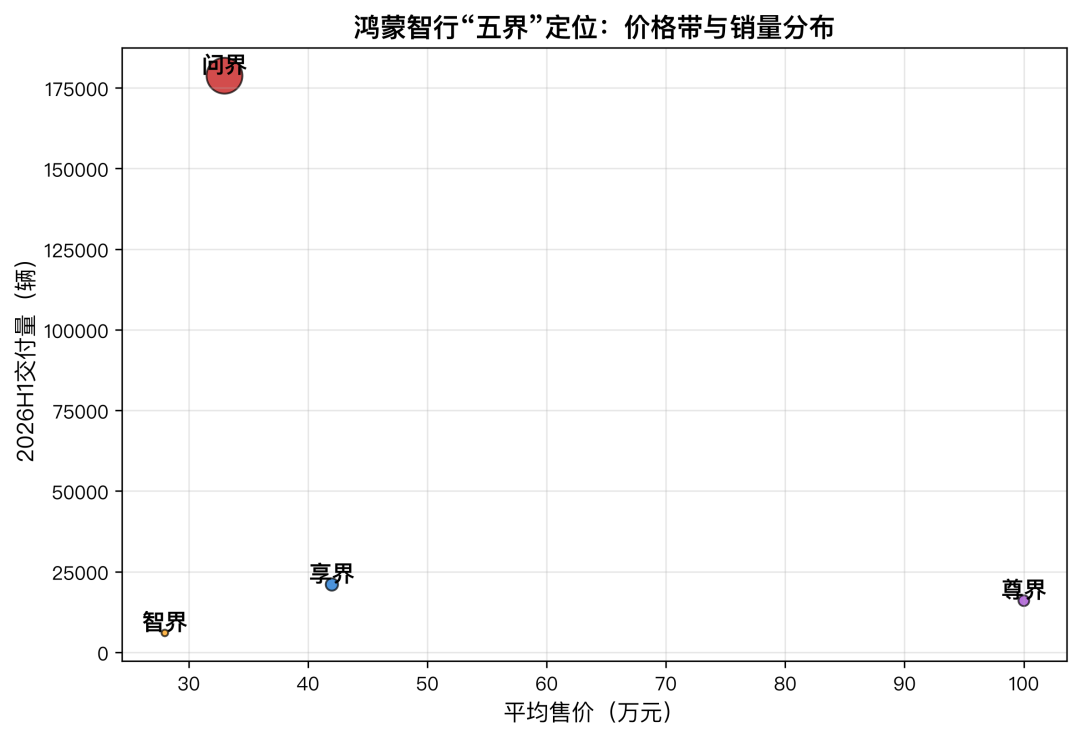

3. Huawei's "Five Brands" Strategy Dilutes AITO's Scarcity Premium

Seres is not Huawei's only automotive partner. Harmony Intelligent Mobility now includes five brands: AITO, Luxeed, Enjoy Auto, ZEEKR, and Shangjie. Their first-half performances varied sharply.

Enjoy Auto stood out as a success story. Beiqi Enjoy Auto delivered 21,000 units in the first half, up 119.58% year-on-year, claiming the crown for NEV sedan sales in the 300,000+ yuan price range for eight consecutive months. The extended-range version's market share rose, as did the penetration of ADS high-end intelligent driving variants. Enjoy Auto's success proves that Huawei's empowerment model can replicate beyond Seres.

Luxeed, a collaboration between Chery and Huawei, serves as a cautionary tale. Its March retail volume was just over 2,300 units, lagging far behind AITO and Enjoy Auto. Luxeed S7 faced delivery hurdles at launch, and subsequent models like R7 failed to gain traction. This shows that Huawei's empowerment is not a panacea; automakers' execution matters equally.

ZEEKR is making slow progress in the ultra-premium market. ZEEKR S800 delivered 16,000 units in 10 months. While acceptable for million-yuan luxury vehicles, the market size is limited.

More notable are rumors of a "Sixth Brand." Chang'an Avatr, GAC Group, Dongfeng, and FAW Hongqi are rumored to join Harmony Intelligent Mobility.

If true, Huawei's technical, channel, and marketing resources will be further diluted, diminishing AITO's former status as Huawei's "favorite son."

"For Seres, Enjoy Auto's success is a double-edged sword. It validates Huawei's model but diminishes AITO's scarcity premium.

As more 'Jie' brands emerge, consumers may ask: If they all use Huawei tech, why buy AITO?"

4. Triple Siege from Li Auto, Xiaomi, and BYD

AITO's pressure comes not just from within Harmony Intelligent Mobility but also from external competitors.

Li Auto is a direct rival in the same segment. Both target extended-range, family-oriented, mid-to-large SUVs. In June 2026, Li Auto delivered 30,900 units, with cumulative deliveries surpassing 1.73 million. Having turned profitable in 2024, Li Auto has greater pricing flexibility and R&D capacity, with steady iterations of the L8 and L6 maintaining product rhythm.

Xiaomi Auto represents an ecological dimensional strike. It delivered over 410,000 units in 2025 and targets 550,000 in 2026. The Xiaomi SU7, YU7, and upcoming extended-range SUVs directly compete in the 200,000–350,000 yuan market. Lei Jun's popularity and Xiaomi's IoT ecosystem provide natural traffic entry points. AITO's core selling point is the "Huawei ecosystem," but Xiaomi is capturing users with a similar logic at lower prices.

BYD exerts scale-based pressure. It sold over 1.77 million passenger vehicles in the first half, dominating the 100,000–300,000 yuan price range. Fangchengbao, Tengshi, and Yangwang cover off-road, premium, and ultra-luxury segments, respectively. While Yangwang's sales are modest, it directly targets AITO M9's high-end positioning.

NIO and XPeng cannot be ignored. NIO's three brands delivered 191,000 units in the first half, up 67.4%, with over 3,300 battery swap stations. XPeng delivered 103,000 units in Q2, leading in intelligent driving and Robotaxi deployment.

In this fiercely competitive landscape, AITO's 10.2% sales growth reflects its product strength. However, this growth comes at the expense of profits, while many rivals are already reaping scale-based rewards.

-END-

Disclaimer: This article is based on the public company attributes of listed companies and a core analysis of information disclosed by them in accordance with legal obligations (including but not limited to interim announcements, periodic reports, and official interaction platforms). Shiyu Xingkong strives for fairness in content and viewpoints but does not guarantee accuracy, completeness, or timeliness. The information or opinions expressed herein do not constitute investment advice, and Shiyu Xingkong assumes no responsibility for any actions taken based on this article. Copyright Notice: This article is original content by Shiyu Xingkong and may not be reproduced without authorization.

-

It's Time to Tally the ROI for Tokens

-

![]()

WPS, with 678 Million Users, Seeks Equilibrium Between Revenue Growth and User Experience

-

![]()

Seres, Once a Profit Leader, Shifts from Gains to Losses in H1: It’s Not Entirely Huawei’s Fault | MIRROR Pro

-

![]()

Why Google Remains 'Others' After 16 Years in the Smartphone Business

-

![]()

The Theory of Distillation Threat

-

![]()

Iterative Communication in Automotive Electronics: ADI's Innovative AB, GMSL, and EB Solutions

-

![]()

Despite AITO’s Explosive Sales, Why is Seres Still Struggling Financially?

-

![]()

For Seres, Losses Aren't the Toughest Challenge