Top 10 Automakers Dominate 80% of Market, Leaving Smaller Players to Fight for Survival

04/01 2025

04/01 2025

587

587

Introduction

The automotive landscape is dominated by the top 10 automakers, leaving smaller players struggling to survive amidst the shadows of their success.

A decade ago, as the industry's growth slowed, the Matthew Effect began to manifest. In that year, domestic auto sales totaled 28.028 million vehicles, with the top ten enterprises (groups) accounting for 88.34% of the market.

Since then, the phenomenon of winners rising and losers falling has been pronounced. While some automakers have achieved brand breakthroughs through premium offerings or specialized products, others have lost their way, facing greater challenges.

Today, as the industry rapidly shifts towards electrification and intelligence, this "strong get stronger" effect has become uncontrollable, reshaping the entire landscape.

Amidst this unprecedented structural transformation in the Chinese auto market, leading automakers are locked in fierce competition, while smaller players find themselves on the brink of survival.

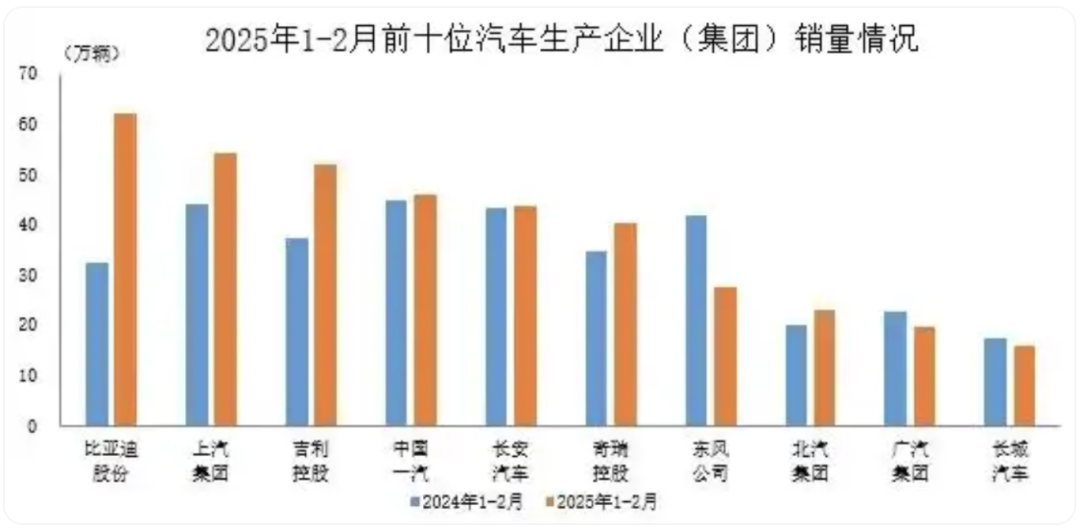

Sales data for the first two months of this year reveals that the top ten automakers (groups) sold a total of 3.856 million vehicles, accounting for 84.7% of total auto sales. This concentration of over 80% has remained largely unchanged over the past decade. For instance, in 2024, the top ten enterprises accounted for 84.9% of total sales; in 2023, it was 85.4%...

Market disputes are intensifying, with the scent of competition permeating the sales tables.

Leading automakers are forging unbreakable competitive barriers through their comprehensive advantages in technology, capital, and the industrial chain. In stark contrast, most smaller enterprises are incurring losses, overwhelmed by numerous development challenges. In this game of industry reshuffling, they face the grim reality of either restructuring or disappearing.

01 "Snowball" Growth

In 2024, BYD sold 4.27 million vehicles globally, a year-on-year increase of 41.26%. This achievement cemented BYD's leading position in the global new energy vehicle market, ranking first in China and among the top five globally.

Changan Auto also sold 2.683 million vehicles in 2024, achieving positive year-on-year sales growth for five consecutive years, setting a new high in the past seven years. Of these, Changan's independent brand sold 2.23 million vehicles, and new energy sales reached 734,000, a year-on-year increase of 52.8%. Geely Group sold 2.177 million vehicles, surpassing the annual sales target of 2 million set at the beginning of the year and achieving significant growth in the new energy field with 494,000 Yinhe series vehicles sold, a year-on-year increase of 80%.

Whether it's BYD topping domestic sales or the continuous achievements of Changan and Geely, they all demonstrate their dominance in the new energy race. These leading enterprises have thrived in the long-term competitive auto market through a closed loop from technology research and development to large-scale production, cost dilution, and market expansion.

In this battle for market share, the competition for core technology positions is crucial.

Technologies such as BYD's Blade Battery, Geely's Leichun Hybrid, and Tesla's FSD autonomous driving have created distinct competitive advantages.

Take the Blade Battery as an example. Since its inception, BYD's Blade Battery has stirred up excitement in the power battery field with its high safety, high strength, and long endurance. This technological revolution not only improved battery performance but also allowed BYD to stand out in the new energy vehicle market.

Today, all BYD models are equipped with Blade Batteries, freeing them from external battery supply dependence and providing significant cost advantages.

With technological advantages boosting sales and profits, leading players have more funds to invest in research and development, creating a virtuous cycle where R&D outputs fuel further technological advancements.

In 2024, the average R&D investment ratio of leading independent automakers was 4.76%, far exceeding the industry average of 3.15%. Among them, Geely Automobile's R&D investment ratio was 4.24%, Great Wall Motors was 6.97%, Chery Automobile was 5.13%, and BYD's R&D investment even reached 14.8%. These data highlight the commitment of leading automakers to enhancing their competitiveness through increased R&D investment.

While technology and R&D create competitive advantages, supply chain discourse power further exacerbates differentiation.

"Without a sales volume of millions, you can't even find a seat at the supply chain negotiating table."

A previous statement by a leading automaker underscores the lack of discourse power for smaller enterprises in supply procurement. Especially during black swan events, leading suppliers like CATL and Bosch prioritize ensuring the capacity of major customers, leaving smaller customers to pick up the scraps, putting them in a very passive position.

In summary, leading automakers are forming unbreakable competitive barriers through their comprehensive advantages in technology, capital, and the industrial chain. This creates a "suffocating" environment for the development of smaller enterprises.

02 "Suffocating" Survival

Public data shows that in 2024, the total revenue of the domestic auto industry was 10.647 trillion yuan, a year-on-year increase of 4%. Despite this revenue growth, costs also increased by 5%, reaching 9.3301 trillion yuan. However, profits fell by 8% year-on-year to only 462.3 billion yuan, with an auto industry profit rate of only 4.3%, far below the average level of 6% for downstream industrial enterprises.

Clearly, amidst fierce competition, the auto industry is deeply entrenched in a "price war," eroding overall industry profits. The game is often dominated by the industry's largest profit earners, forcing many automakers to choose between prioritizing sales or profits, ultimately leading to a "bleeding" business model.

For automakers with options, the choice between sales and profits may not be the cruelest. At least, they can choose one. For those with neither, every vehicle sold may be their last.

On February 18, Lifan Technology officially changed its name to Qianli Technology, bidding farewell to the "Lifan" era for the once "first private automaker stock."

This once leading private automaker was the largest exporter of Chinese auto brands and once ranked among the top domestic brands, launching several best-selling models. However, with the overall downturn in the auto market and its own deep-seated issues, Lifan's situation worsened, continuously losing the confidence of investors and consumers. In 2022 alone, it incurred a loss of 4.68 billion yuan, a year-on-year decrease of 1950.83%. Behind this huge loss are numerous operational and managerial challenges.

Lifan's exit serves as a warning for other domestic automakers. In this rapidly changing market, technological innovation is the core driving force for enterprise development. Only by continuously investing in research and development and mastering core technologies can one gain a competitive edge. Brand building is also crucial, as a clear and unique brand image can foster a sense of identity and loyalty among consumers. Market insight is indispensable, as enterprises need to constantly monitor market dynamics, adjust strategies timely, and seize development opportunities.

Besides the fading glory of brands like Zotye and Lifan, new forces such as WM Motor, AITO, HiPhi, and Jiyue have also fallen one after another. Data shows that for every 1 percentage point increase in industry concentration (CR10), 3-5 marginal enterprises face elimination, and smaller automakers are at risk at every step in the future.

Behind this phenomenon lie not only market changes and pressure from leading players but also the "mountainous" development issues of smaller automakers themselves.

First, costs are out of control, with rising raw material prices increasing the cost of single vehicles. However, smaller automakers lacking premium pricing power dare not easily raise prices. Second, channels are shrinking, with dealers accelerating their concentration towards leading brands, and the withdrawal rate of dealers for automakers below the waistline is extremely high. Third, the financing winter is harsh, with capital markets becoming increasingly stringent towards smaller automakers, and industry financing continuously flowing to leading enterprises.

03 Drivers of Industry Reshuffling

The primary challenge for smaller automakers is the "life-and-death race" of the new energy transition.

In 2024, the penetration rate of new energy vehicles successfully broke through the 50% threshold, up from 32.8%. Against this backdrop, the industry rules have completely changed. The market share of traditional fuel vehicles is shrinking monthly, and automakers that fail to complete the electric transition are accelerating their exit. Many executives have emphasized that "electrification is not a choice but an elimination race."

On the path to electrification, intelligence follows closely.

The "arms race" among automakers regarding intelligence is intensifying, with the computing power of automotive chips doubling every year. L2+ assisted driving has become standard, and L3 is on the horizon. Xpeng Motors invests 3.5 billion yuan annually in NGP research and development. In contrast, the smart cockpit research and development budgets of smaller automakers are paltry, and the OEM model leads to severe product homogenization.

Moreover, global competition poses a multidimensional threat to smaller automakers.

Tesla's Shanghai factory continues to break production capacity records, and leading independent brands are accelerating their overseas expansion. Leveraging their domestic scale advantages, leading enterprises crush regional brands. Based on this, the market share of Chinese brands in the Southeast Asian market has soared from 14.7% in 2020. In this global competition, the paths available to smaller enterprises are becoming fewer and narrower.

For smaller automakers, amidst the industry reshuffling, there is no choice but to break through. Either restructure or disappear.

On the path of exploring survival strategies for smaller automakers, vertical integration is crucial.

"We want to be the Uniqlo of the new energy sector!" said Zhu Jiangming, the founder of Leap Motor. Under his strategy, Leap Motor does not compete on configuration and marketing but focuses on "cost control."

By adhering to full-domain independent research and development, from the three-electric system to the smart cockpit and even chip algorithms, Leap Motor has achieved significant cost savings. Relevant documents mention that Leap Motor's independent research and development costs account for 60% of the entire vehicle, a significant reduction compared to outsourcing. For example, the LEAP 3.0 architecture highly integrates the battery, electric drive, and intelligent driving system, eliminating redundant parts, reducing costs, and maintaining performance.

It was this strategy of vertical integration that allowed Leap Motor to achieve quarterly profitability for the first time in the fourth quarter of 2024, one year ahead of schedule. Simultaneously, it positioned Leap Motor in the final circle of the new energy race on its ninth anniversary.

In addition, niche focusing is also a viable development option for smaller automakers. For instance, NIO Auto has deeply cultivated the market below 100,000 yuan, creating niche advantages through extreme cost-effectiveness. Leap Motor, mentioned earlier, has also carved its niche by focusing on large space and cost-effectiveness. Of course, the simplest path is to emulate Thalys and partner with industry giants like Huawei.

Leveraging Huawei's Smart Selection mode, Thalys and JAC are empowered, employing ICT technology to address manufacturing deficiencies. In this collaborative framework, Huawei and its partners harness their respective strengths, complementing each other to establish a comprehensive vehicle value chain. Huawei boasts robust capabilities in product definition, research and development, distribution channels, and marketing, offering technical support to small and medium-sized automakers, thereby enabling them to compete favorably in terms of technology and branding.

Last year, the automotive market confronted a significant challenge: a surge in automaker bankruptcies loomed on the horizon. Among the newcomers to the industry, with precedents set by companies like HiPhi, WM Motor, and Jiyue, many brands appeared to be teetering on the brink of survival.

Concurrently, several automaker founders, including He Xiaopeng, Li Bin, and Lei Jun, anticipated that the future automotive market would not support more than seven, or even five, brands. Amidst this fierce competition, the success stories of leading automakers conceal the numerous struggles of smaller players. As the Matthew Effect intensifies, survival hinges on becoming an integral part of the industry giants.

Editor-in-Chief: Du Yuxin

Editor: Chen Xinnan

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving