Chinese Automakers Pursue Independent R&D and Domestic Substitution as Qualcomm and NVIDIA Spark Price War in Automotive Chip Market

04/03 2025

04/03 2025

578

578

Currently, China stands as the world's largest producer, seller, and exporter of new energy vehicles, commanding over 70% of the global market.

What does this imply? It signifies that China now dominates the global new energy vehicle market, shaping many of its demands.

In contrast to traditional fuel vehicles, the demand for automotive chips in new energy vehicles has soared, particularly for smart cockpit and autonomous driving chips, which are rarely required in fuel vehicles.

Previously, NVIDIA was the go-to for most autonomous driving chips, while Qualcomm dominated the smart cockpit chip market.

NVIDIA's Orin chip once held a commanding 70% share of the domestic market, while Qualcomm's Snapdragon cockpit chip peaked at over 80% market share.

However, in recent years, Chinese automakers have embarked on a journey of domestic substitution, either through independent R&D or adopting domestic third-party chips.

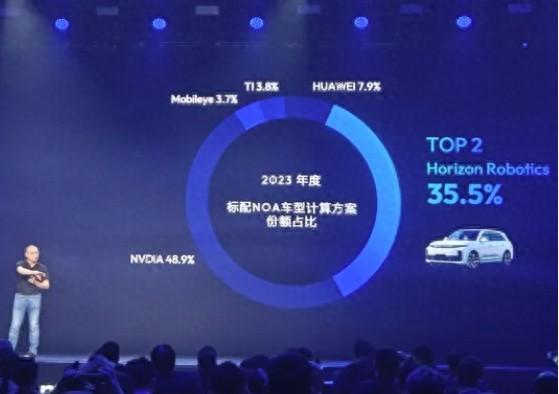

For instance, in the autonomous driving sector, by 2023, Chinese manufacturers already accounted for over 43% of the market share. While NVIDIA remained at the top, Horizon Robotics and Huawei followed closely in second and third place, respectively.

By 2024, the share of Chinese manufacturers further increased to over 50%, while NVIDIA's share continued to decline, and the shares of Mobileye and Texas Instruments became insignificant.

Moreover, chips independently developed by NIO and XPeng are poised to be integrated into vehicles, replacing previously used NVIDIA chips.

A similar trend is evident in the smart cockpit market. Qualcomm once held sway, but now numerous domestic manufacturers have emerged, introducing a series of smart cockpit chips. Some automakers have also undertaken independent R&D for domestic substitution.

Consequently, Qualcomm and NVIDIA find themselves under significant pressure. China, being the largest market with the greatest demand, presents a crucial challenge. If purchases decline in the Chinese market, who will they turn to for sales?

Recently, media reports have indicated that Qualcomm, a leading chip manufacturer, has reduced prices for the Chinese electric vehicle market, specifically targeting top-tier automakers and competing fiercely on price.

NVIDIA has similarly followed suit, reassessing and adjusting its market strategy accordingly, poised to engage in a price war.

It remains to be seen how Chinese automakers will navigate this situation. Will they revert to using Qualcomm and NVIDIA chips due to the price reduction, or will they remain committed to domestic substitution regardless of the cost advantage of foreign chips?

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving