“Three-Way Showdown” in Unmanned Delivery: Giants, Pioneers, and Newcomers—Who Will Reign Supreme?

10/13 2025

10/13 2025

767

767

By: Tan Qing Shuo AI

Amid the swift evolution of intelligent driving and Robotaxi services, it comes as a surprise that unmanned delivery vehicles are on the verge of becoming the inaugural large-scale commercialized and profitable sector within L4 autonomous driving and embodied AI.

Just days prior to National Day, Neolix, a company specializing in unmanned delivery, officially unveiled its 10,000th vehicle.

Furthermore, another frontrunner in the unmanned delivery realm, 9D Robotics, declared earlier this year its ambition to achieve a cumulative production and delivery of 10,000 unmanned delivery vehicles within the same year.

The milestone of 10,000 units is widely acknowledged as a pivotal moment for scalability, marking a significant achievement for the industry.

Against this backdrop, in the previous month alone, two publicly listed companies—Desay SV and Minieye—introduced new products, officially stepping into the unmanned delivery vehicle market.

Reports also suggest that several firms, including Momenta, are gearing up to enter the industry and secure a slice of the market.

In this context, the industry has entered a phase of fierce competition and rapid growth.

Multi-Party Game: Strengths and Weaknesses of Enterprises Across Different Tiers

Currently, the industry is primarily dominated by three tiers of companies:

Big Players—Cainiao, JD.com, Meituan: Among them, JD.com and Meituan view unmanned delivery as an “internal utility,” prioritizing self-sufficiency before considering external supply. In contrast, Cainiao adopted a market-oriented approach from the outset.

2. Pioneering Duo—Neolix and 9D Robotics: Leveraging their early-mover advantage, they have secured mainstream orders and operational scenarios, becoming the current “delivery volume leaders.”

3. Capital Newcomers—Desay SV (Chuanxing Zhiyuan) and Minieye (Xiaozhu Unmanned Vehicles): Both are publicly listed companies viewing unmanned delivery vehicles as a new growth avenue. With vehicle-level supply chains and autonomous driving technology, they aim to disrupt the market using “capital + technology.”

It is evident that the unmanned delivery industry is currently witnessing a “clash of titans.” Who will ultimately prevail?

Let’s first examine the big players. Unlike startups that rapidly pursue large-scale expansion, they prioritize stability.

For instance, Li Qiang, CTO of Cainiao, recently stated, “We are not concerned about keeping pace with scalability.”

For a company like Cainiao, reputation matters more than speed.

With robust ecological resources—such as Cainiao’s backing by Alibaba—they have no shortage of orders, technological accumulation, or funding.

Their solid foundation allows them to maintain a competitive edge by focusing on product quality, service excellence, and cost reduction.

More importantly, big players like Cainiao possess a trust-based competitive advantage.

Unmanned vehicles are not a one-time hardware sale but a long-term commitment: purchasing the vehicle is just the beginning. Subsequent services like autonomous driving subscriptions, system upgrades, sensor calibration, and cloud-based scheduling and maintenance all rely on the service provider. Essentially, every kilometer of operation depends on the provider’s “lifelong support.”

Much like how new energy vehicle owners fear the scenario where their car remains functional, but the manufacturer or after-sales service disappears, big-name service providers offer strong trust backing, providing customers with greater peace of mind.

Leveraging this unique advantage, Cainiao remains unfazed by Neolix’s aggressive expansion.

In fact, rushing into large-scale deployment before the technology is truly mature could harm user experience and even pose risks to urban operations.

Moreover, brands like Cainiao are constantly under public scrutiny. Any negative publicity could affect the entire ecosystem behind them, which is why they adopt a more cautious approach to promoting unmanned delivery vehicles.

However, for startups like Neolix and 9D Robotics, caution is not an option.

On one hand, they need revenue to sustain operations; on the other hand, they must demonstrate the viability of their business model to investors.

According to the Tianyancha APP, since the beginning of the year, Neolix and 9D Robotics have secured continuous funding. Neolix has raised over RMB 1 billion, while 9D Robotics has obtained nearly USD 300 million.

As industry pioneers, they are bold and aggressive, requiring greater scalability and more orders to prove themselves.

Today, they have established a full-chain operation encompassing “supply chain–operations–data.” For example, Neolix has integrated its hardware into the last-mile delivery networks of companies like SF Express, building trust with governments and logistics enterprises across more than 200 cities over 2–3 years. Their fleet of 10,000 L4 autonomous vehicles has accumulated tens of millions of kilometers, creating a data feedback loop that forms a short-term, unreplicable scenario-based moat.

At the same time, they hold more road rights and offer advanced pricing and services.

For the current unmanned delivery vehicle industry, road rights determine market entry, while pricing and services define growth potential.

Without road rights, vehicles cannot operate legally.

As of now, Neolix has obtained public road rights in over 280 cities across China.

By April this year, 9D Robotics had achieved normalized operations in more than 200 cities across 29 provinces, municipalities, and autonomous regions.

In terms of pricing and services, both companies have adopted a “close-quarters combat” approach to stay competitive.

For instance, 9D Robotics’ E6 model has reduced the base price of a single vehicle to below RMB 20,000 while offering flexible FSD subscriptions. Additionally, over the past two years, 9D Robotics has established a service network requiring a presence in every location where its vehicles operate, ensuring clients receive responses within one minute at any time.

Neolix is no less competitive, focusing on financial cost reduction. After offering a limited-time “RMB 888 down payment” promotion in June, it upgraded its offer in September—its main models now come with “zero down payment, zero interest, and 48-month financing,” along with lifetime free FSD.

Their relentless competition in pricing and services is intensifying industry rivalry while enhancing their own competitiveness.

However, despite their leading position, frontrunners often encounter industry ceilings first.

Further large-scale expansion remains hindered.

Last month, Yu Enyuan expressed concerns about Neolix’s development, citing public acceptance and safety as key issues.

Residents need time to accept the sudden appearance of various unmanned vehicles in cities. Additionally, safety is a non-negotiable red line for unmanned vehicles, with news of accidents already emerging in different regions.

These issues currently hang over the industry like a Sword of Damocles, preventing rapid short-term expansion.

However, because the industry is still in its early stages and faces scalability constraints, latecomers have opportunities to catch up.

For Desay SV and Minieye, they possess differentiated strengths.

Desay SV focuses on “automotive-grade reliability + low cost.” With four decades of experience in the automotive industry, it has mastered large-scale production and supply chain integration, positioning itself as a “muscle memory” expert. It was the first to propose building “automotive-grade” unmanned vehicles, emphasizing reliability.

Minieye emphasizes “leading autonomous driving technology + rapid scenario adaptation.” Specializing in autonomous driving technology, it has deep expertise in perception algorithms and decision-making systems, enabling it to quickly transfer advanced passenger vehicle technologies to unmanned delivery scenarios.

Moreover, Minieye has ambitious goals, aiming to deliver 10,000 units by 2026, directly challenging Neolix and 9D Robotics.

However, as previously mentioned, established players have already secured advantages in market trust and road rights, making it difficult for latecomers to overtake them quickly.

Take market trust and collaboration barriers, for example. Early players have solidified client relationships through long-term deliveries: Neolix is now SF Express’s largest unmanned vehicle supplier, while 9D Robotics has signed multi-year framework agreements with leading enterprises like China Post.

Those familiar with B2B operations understand that such partnerships demand extremely high stability and reliability. Once established, they become difficult to replace.

For Desay SV and Minieye to break in, they must demonstrate significantly superior product reliability, cost-effectiveness, and scenario adaptability to trigger client reevaluation.

Even then, the validation process for logistics giants typically takes two to three years, involving rebuilding scheduling systems, updating high-definition maps, and overhauling operation and maintenance frameworks—all requiring substantial investment and time.

The timeline for rebuilding trust and ecosystems means market expansion for new entrants will be more challenging than in the early stages.

More New Players Enter, Industry Enters Phase of Refinement

Beyond Desay SV and Minieye, the sector still harbors disruptive X-factors.

Momenta dominates the algorithm space with a 60.1% market share in NOA; Huawei’s influence is undeniable, disrupting the new energy vehicle and unmanned mining truck sectors;

BYD excels at cost reduction, holding core capabilities in battery and vehicle manufacturing. Combined with its experience as a Tier 0 supplier for Nuro’s L4 unmanned delivery vehicles, its potential entry could directly squeeze existing players’ survival space.

However, the presence of uncertainties and continuous new entrants has amplified the “catfish effect,” forcing the industry onto a fast track of “quality and efficiency improvements.”

First, competitive pressure compels companies to accelerate technological iteration and refine product services. Second, potential crossovers by giants like Huawei and BYD could unify fragmented technical filing and safety regulatory standards across regions, reducing institutional costs for cross-regional operations.

Competition propels the industry forward, shifting focus from product-centric approaches to holistic service excellence and from regional standard fragmentation to eventual unification.

As the industry achieves scalable profitability, more companies will enter, leading to multifaceted competition beyond just pricing.

This signifies the arrival of scalable development, demanding a transition from rapid expansion to refinement.

From a developmental perspective, the industry is indeed deepening its evolution.

1. Product diversification: Specialized models like cold chain versions and compartmentalized cabinet vehicles are emerging for different scenarios.

Take Neolix as an example: its unmanned vehicles have iterated into three major products—X3, X6, and X12—covering the full range from three-wheelers to vans and light trucks. These multi-purpose vehicles cater to diverse logistics needs, including e-commerce express, fresh food cold chains, supermarket fast-moving consumer goods, and wholesale markets, serving a broader array of scenarios.

Yu Enyuan previously stated that while Neolix’s revenue from the express delivery industry will continue to grow rapidly next year, sales in non-express sectors like urban distribution and instant logistics may account for nearly half.

This indicates that scenario-based services for unmanned delivery will further deepen compared to the past.

2. Operation and maintenance management is upgrading from “single-vehicle intelligence” to “group collaboration,” requiring greater refinement.

Large-scale commercialization of unmanned delivery vehicles is now feasible. Leading companies like Neolix and 9D Robotics already manage real-time scheduling for fleets numbering in the thousands. Platform algorithms must perform millisecond-level path recalculations, dynamic order allocations, and empty-run suppression, with system complexity scaling exponentially with size.

This places new demands on operation and maintenance management. Behind every so-called unmanned vehicle lies human intervention—a remote control center at the backend and an offline rescue network at the frontend. If a vehicle encounters issues, safety officers must take over remotely, or engineers must repair it on-site.

In other words, the future will no longer be solely about pricing but also about operation and maintenance services.

To succeed in this business, operation and maintenance personnel must understand driving, technology, and customer needs, requiring companies to build versatile “three-dimensional” operation and maintenance teams with more refined talent requirements.

3. Ecosystem collaboration is strengthening. Unmanned delivery will integrate deeply with automatic sorting, unmanned stations, and other logistics links, potentially forming end-to-end “warehouse-transportation-station” unmanned solutions.

Take Cainiao Smart Logistics Holdings Limited as an example: its “AI + logistics” system targets complex county-level road networks and high co-delivery demands. By launching an “automated sorting + unmanned vehicle direct delivery” model at county-level co-delivery centers, it streamlines sorting, trunk transportation, and last-mile delivery in one go, improving rural express sorting and delivery efficiency while significantly reducing operational costs.

Currently, unmanned delivery operates as an isolated transportation node, but in the future, it will embed into broader logistics and urban operating systems.

These trends indicate that the unmanned delivery industry is gradually entering a mature phase.

However, while the future looks promising, the industry still faces stark realities.

Technological challenges continue to loom large, including the absence of essential infrastructure for traffic light information interoperability and dedicated lanes for autonomous vehicles. This lack of infrastructure compels unmanned vehicles to function in isolation. Furthermore, the complexity of dense urban traffic and the rapidly evolving nature of road conditions necessitate more advanced computational capabilities and sophisticated algorithms for real-time perception and decision-making, pointing to the need for further enhancements to current technological frameworks...

Only by systematically tackling these "hard truths" can the unmanned delivery sector achieve maturity and unlock its full market potential.

Scalability represents merely the starting point for the unmanned delivery industry. As Neolix CEO Yu Enyuan has articulated, the delivery of 10,000 units signifies a fresh industry benchmark. Looking ahead, unmanned vehicles are poised to become integral elements of the global logistics infrastructure, akin to express cabinets and freight stations, fundamentally reshaping the interconnections among people, goods, and locations.

-

![]()

Personnel Shuffle: Independent Director Mi Xuming Steps Down from OFILM

-

![]()

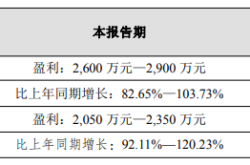

Net Profit Anticipated to Skyrocket by 103%: What Gives This Optical Company a Competitive Edge?

-

In Just One Year, China Unveils Unicorns Valued at 10 Trillion Yuan!

-

![]()

6 Park Companies Shine at WAIC: How Hong Kong Science Park Bridges AI from Research to Industry

-

![]()

Wang Wenjing’s Third Act: Can Yonyou Reinvent Itself in the AI Era?

-

![]()

Performance Coupe Entry Threshold Reduced to 170,000 Yuan: Assessing the 2027 Exeed ES's Prospects

-

![]()

Battery "Crisis" for 4 Million New Energy Commercial Vehicles

-

【Focus】Fluorinated Photosensitive Polyimide (FPSPI): A High-End Subdivision of PSPI with Great Potential in High-Tech Industries