B-End Acceleration and Soaring Gross Margins: MiniMax Reaches a New Inflection Point

03/04 2026

03/04 2026

531

531

By Wang Huiying

Edited by Ziye

The year 2025 marks a watershed moment for China's AI large model industry.

This year, capital has shifted from chasing parameter competitions to questioning closed-loop business models, while users have moved from trial-based experiences to practical considerations. Doubts about the extent of the bubble in the large model industry continue to loom over players like a sword of Damocles.

As the noise fades, the industry has come to realize: The ultimate goal of AI is not technical papers but sustainable business growth.

Against this backdrop, the first annual report from large model company MiniMax after its listing is destined to be more than just its own scorecard—it serves as a snapshot of the entire sector's trajectory.

According to MiniMax founder Yan Junjie, as of February 2026, the company's ARR (Annual Recurring Revenue) has exceeded $150 million.

Throughout the year, this large model company, which broke through with its C-end application Talkie, did not follow a script of sustained high revenue growth. Instead, it opened up new market expectations through revenue structure optimization and full-modal models.

What truly warrants repeated market reflection is Yan Junjie's vision for MiniMax's future.

MiniMax aims to become a platform company in the AI era and is confident of winning key AI battles... This large model company is attempting to forge its own path as a platform company amid a sector dominated by giants.

1. Quarterly Weakness, Structural Optimization: MiniMax Seeks Resilience

On March 2, MiniMax, less than two months after its listing, released its first full-year performance report.

In 2025, the company achieved total revenue of $79.038 million, up 158.9% year-on-year, surpassing analysts' average expectation of $71.4 million. International revenue accounted for 73%, with business covering over 200 countries and regions and a cumulative user base of 236 million.

Breaking it down, revenue from AI-native products, represented by Talkie, reached $53.075 million, up 143.4% year-on-year, accounting for 67.2% of total revenue and remaining the foundation.

From the user side, MiniMax's C-end foundation has become substantial. In the first three quarters of 2025, AI-native products had 1.7716 million paying users, with average spending per paying user rising from $6 in 2023 to $15.

Supporting this revenue are MiniMax's dual layout (strategic layout ) of emotional companionship and productivity tools, including Talkie, which focuses on emotional companionship and user interaction with virtual characters, and Hailuo AI, which focuses on video generation.

Source: Hailuo AI official website

The larger increment (growth) came from enterprise revenue. In 2025, revenue from open platforms and enterprise services reached $25.963 million, surging 197.8% year-on-year, significantly leading the pack. The number of paying clients exceeded 214,000, becoming the second growth engine.

In February this year, new registrations on open platform products for enterprise clients and individual developers reached more than four times the level in December 2025.

At the profit level, despite sustained high investment in the large model industry in 2025, MiniMax's loss persisted, with an adjusted net loss of $251 million, up 2.7% from $244 million the previous year.

The most eye-catching aspect of this report was the leap in gross margin. In 2025, MiniMax's gross margin reached $20.079 million, up 437.2% year-on-year. The report explicitly attributed this to improved model and system efficiency and optimized infrastructure allocation.

In the AI large model field, high R&D costs have long been a daunting challenge, but MiniMax has demonstrated commendable R&D efficiency.

In 2025, its R&D expenditure was $250 million, up 33.8% year-on-year, but R&D efficiency improved significantly. The proportion of R&D expenditure to total revenue fell from 619% in 2024 to 320% in 2025.

Numerous financial indicators are sending positive signals, with MiniMax transitioning from high investment to healthy operations and achieving scale effects.

Admittedly, when we focus on the fourth quarter, MiniMax's revenue growth slowed markedly. Based on published revenue for the first three quarters, MiniMax generated approximately $26 million in revenue in Q4, up 131% year-on-year. While higher than market expectations, this was a significant slowdown from the 175% growth in the first nine months.

The reason, when combined with the 2025 annual report and prospectus, is that MiniMax's C-end revenue in Q4 slightly exceeded $15 million, up 82% year-on-year—nearly halved from the nearly 150% growth in the previous three months.

However, this single-quarter slowdown did not affect institutional ratings of MiniMax, with UBS setting a target price of HK$1,000 and Morgan Stanley giving a target price of HK$930.

The logic is that this single-quarter deceleration was essentially a manifestation of revenue structure optimization.

In Q4, revenue from open platforms and other enterprise services reached $11 million, up 278% year-on-year, accelerating further from the 160% growth in the first three quarters.

Previously, the market's biggest question (doubt) about MiniMax centered on its "over-reliance on C-end and weak B-end" structure, fearing the company's excessive dependence on a single hit product and insufficient risk resistance. Now, the 2025 financial data directly addresses this question (doubt).

The past model of relying on C-end hits like Talkie and Hailuo AI for growth is shifting toward a dual-engine structure of steady C-end operations and rapid B-end expansion. This transition involves short-term growth fluctuations but reduces reliance on a single product and enhances business resilience in the long run.

This is not passive compromise but active choice. The shift from single-hit-driven to dual-wheel-driven growth marks a symbolic transition for large model companies toward maturity. MiniMax's resilient financial report proves that its commercialization is evolving from product luck to systemic capability.

2. Technological Upgrades and Cost Reductions: MiniMax Accelerates Commercialization

MiniMax's performance is not just a two-year commercialization summary but also an important observational sample of the global generative AI industry's shift from conceptual hype to value realization.

In the second half of 2025, China's large model industry quietly completed a shift in competition focus, with many leading players moving from large parameter counts to efficient inference and from model capability benchmarking to commercial scenario implementation.

Industry consensus has gradually clarified: The next competition point lies not in who can build the smartest model but in who can make smart models cheap, user-friendly, and scalable enough.

Amid this collective pivot, MiniMax completed a critical leap from technological catch-up to commercial validation.

"We iterated the M2 series from the first generation to the third generation in just 108 days," Yan Junjie said at the earnings call.

In Q4 2025, MiniMax launched three models: M2, M2.1, and M2-her. In just 108 days, it completed continuous upgrades from M2 to M2.5, significantly outpacing overseas giants like Anthropic, OpenAI, and Google.

M2, emphasizing foundational text and dialogue capabilities, became the first Chinese model to exceed 50 billion daily token consumption on OpenRouter while topping HuggingFace's global weekly hot list. M2-her focused on long-form dialogue and emotional interaction, leading globally in 100-round dialogue performance.

More prominent was M2.5, which became the culmination of MiniMax's technological capabilities.

Source: MiniMax official website

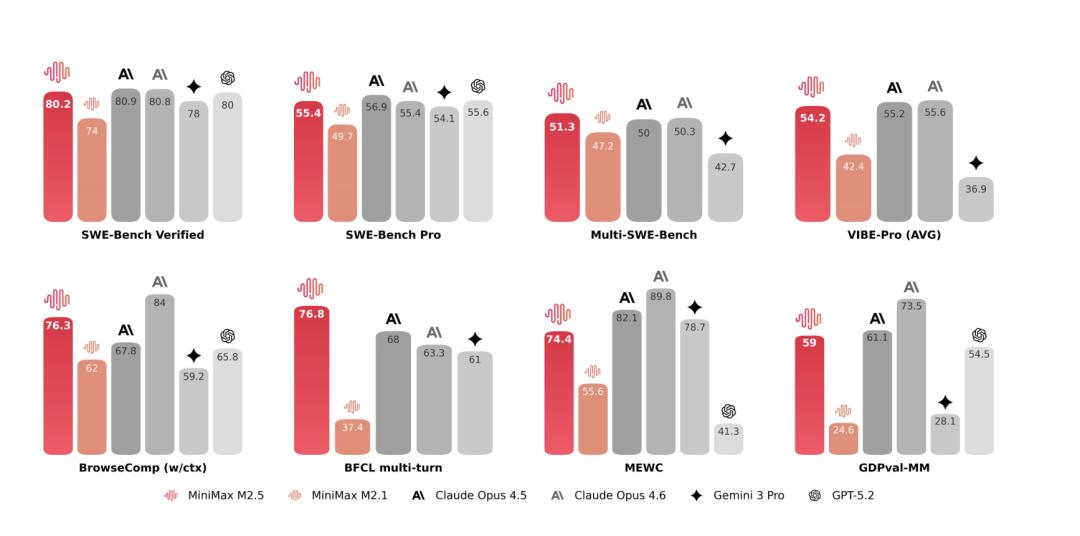

In the core programming test SWE-Bench Verified, M2.5 scored 80.2%, setting an industry record. It also ranked first in multilingual tasks (Multi-SWE-Bench) and reached industry-leading levels in search and tool invocation benchmarks like BrowseComp and Wide Search.

More critically, efficiency improved. In SWE-Bench Verified, M2.5 completed tasks 37% faster than its predecessor M2.1.

In specific application scenarios, M2.5 can proactively dissect architecture and plan workflows before coding, approximating real architect thinking. It can independently handle full-cycle development from requirement analysis and system design to code implementation and defect repair, transforming from a simple code completion tool into a deployable software development assistant.

In office scenarios, M2.5 comprehensively optimized high-level tasks like Word, PPT, and Excel financial modeling, improving tool invocation and search capabilities by 20% and completing complex agent tasks with fewer rounds and higher accuracy, clearing ability barriers for enterprise-level implementation.

But what truly gives M2.5 commercial competitiveness is its extreme cost advantage.

At 100 tokens per second, M2.5 costs just $1 for an hour of continuous work; at 50 tokens per second, it costs only $0.3. By output price, this is just 1/10 to 1/20 of overseas models like Claude Opus, Gemini 3 Pro, and GPT-5.

This means $10,000 can keep four agents working nonstop for a year. When compute costs are no longer a constraint, enterprise clients' attitudes have shifted from "piloting AI" to "actively embracing AI." This explains MiniMax's rapid B-end business growth over the past year.

The explosive growth in invocation volume is the most intuitive (direct) evidence of developers voting with tokens. The average daily token consumption of M2 series text models in February 2026 grew more than sixfold from December 2025, with programming scenarios seeing over 10x token consumption growth.

MiniMax is converting technological iteration and reduced inference costs into tangible commercialization results. Technological breakthroughs bring cost advantages, which drive commercialization volume, especially B-end growth, which in turn feeds technological iteration—MiniMax's commercialization flywheel is spinning faster.

3. Multimodal Breakthrough: MiniMax Aims to Be "AI Era Infrastructure"

With commercialization progress, another question arises: How high a ceiling can model invocation fees support?

In the fiercely competitive large model sector, this ceiling seems not very high. More importantly, if MiniMax remains just an API provider, it may ultimately get dragged into a price war with giants.

To sustain capital market appeal and run longer in this marathon, MiniMax needs a higher-dimensional strategy. At the earnings call, Yan Junjie offered his answer: The company's next-stage strategy is to evolve from a large model company into a platform company for the AI era.

A platform company in the AI era is not like a Traffic platform (traffic platform) in the internet era but an enterprise capable of defining intelligence boundaries while delivering industry dividends at the product and commercial levels.

Yan Junjie believes the value of an AI-era platform company can be roughly estimated as "intelligence density multiplied by token throughput."

Intelligence density addresses "what can be done," while token throughput addresses "how large a scale can be served." In other words, using more models to serve more clients and populations unlocks greater value.

With OpenAI, Google, and other giants also striving to become AI platform companies, how can MiniMax, just a few months after listing, forge its own path?

Supporting this strategy is MiniMax's continuous accumulation of full-modal capabilities. Unlike most AI large model companies that start with language models before adding voice and vision, MiniMax decided from the outset to develop multimodal models and was among China's first teams to launch MoE models.

Based on its multimodal approach, MiniMax has persistently pursued parallel R&D in language, video, voice, and music modalities. During this earnings call, Yan Junjie reiterated the rationale for choosing multimodality, arguing that fusing multiple modalities is a fundamental prerequisite for continuously improve ( continuously improve : continuous improvement) in intelligence.

By the end of 2025, video models like Hailuo 2.3 had generated over 600 million videos. Additionally, the Fast model reduced batch operation costs by 50%. The voice model Speech 2.6 generated over 200 million hours of speech, supporting 40+ languages, while the music model Music2.5 supported long-form content generation with complex emotions and diverse singing styles...

According to MiniMax, the upcoming MiniMax-M3 and Haigou 3 series models in the first half of this year will represent the latest achievements in multimodal fusion.

In product positioning, MiniMax has also made sober strategic choices to differentiate itself through breakthrough (breakthrough).

MiniMax explicitly chooses not to build a general-purpose personal assistant like Doubao or ChatGPT Mobile but to focus on high-value productivity scenarios, including programming, office work, and interactive entertainment.

Yan Junjie stated that the company does not pursue all-around leadership in every dimension but focuses on building model capabilities with unique advantages. The differentiated performance of series models like M2, Hailuo 2, and Speech2 is a product of this mindset.

This is undoubtedly a wise choice. During the resource-constrained startup phase, focusing on areas that generate unique value and building differentiated competitiveness helps MiniMax bypass giant competition and gain a foothold while making its platform positioning more focused and clear.

Notably, to advance toward a platform company, MiniMax has used itself as a testing ground for AI-native organizational transformation.

By the end of 2025, MiniMax's internal Agent "interns" had supported nearly 90% of employees across scenarios like programming development, data analysis, and HR recruitment.

This "self-use before external sale" path positions the company not just as a model supplier but potentially as an infrastructure provider for enterprise-level AI productivity platforms. If this model succeeds, MiniMax will achieve a strategic leap from "large model developer" to "platform company."

Of course, challenges remain. High R&D investment will continue to suppress profit performance, while global compute cost fluctuations and international competition pressures cannot be ignored. The evolving competitive landscape introduces another layer of uncertainty. For now, MiniMax's profitability timeline remains unclear, and long-term capital consumption pressures are significant.

From a long-term perspective, the AI race has entered its second half, and MiniMax is standing at a critical tipping point. To transition from a large model company to a platform-based company, more real-world foundations are needed for support. Only by balancing the speed of technological iteration with commercialization efficiency can a crucial step forward be taken.

As Yan Junjie said: 'In the AI era, what ultimately determines the outcome is not simply burning money and resources, but the speed of progress in intelligent capabilities, which enables the generation of larger-scale commercial revenue and market size. And speed comes from R&D efficiency.'

The performance in 2025 will be a validation of capabilities, while the execution in 2026 will determine whether MiniMax can truly complete this strategic upgrade.

(The header image of this article is sourced from the official website of MiniMax.)

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once