Will China’s Auto Exports Keep Up Their 'Surging' Momentum in 2026?

03/04 2026

03/04 2026

523

523

Recently, the China Association of Automobile Manufacturers (CAAM) released automotive data for January 2026. Domestic sales stood at 2.346 million units, marking a 3.2% year-on-year decrease. This decline was largely anticipated, given the gradual phase-out of purchase tax incentives, the transitional period before local subsidies took effect, and the fact that many consumers had already made their purchases by the end of the previous year. After all, January typically experiences a lull in sales, making this trend understandable.

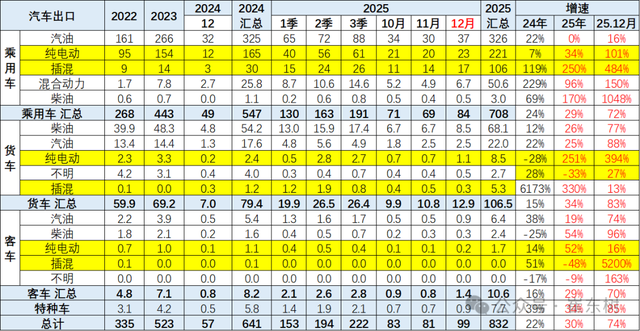

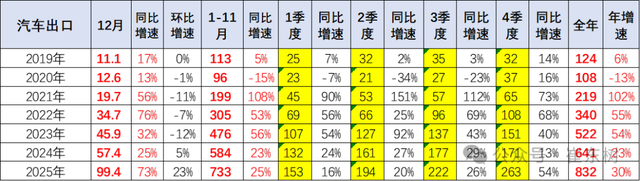

However, the export scene tells a starkly different story: 681,000 units were exported, representing a 44.9% year-on-year increase, with new energy vehicles (NEVs) seeing their numbers double. Frankly, this is a robust start.

As the saying goes, 'If you can't compete at home, go abroad.' This sentiment has been echoed for years, but 2026 seems to be the year it truly materializes. Last year’s impressive full-year exports of 8.32 million units set a high bar, and the growth rate in January-February this year essentially sets the tone for the entire year: In 2026, global expansion will only intensify.

Yet, amid the excitement, key questions linger: Who are the key exporters? Where are they selling? What challenges lie ahead?

The Main Exporters: Likely the Usual Suspects

Let’s begin with who is driving these exports.

An intriguing detail emerges from the January data: NEV exports reached 302,000 units, comprising 202,000 battery electric vehicles (BEVs) and 99,000 plug-in hybrids (PHEVs). While PHEV exports saw a month-on-month dip, they nearly doubled year-on-year. What does this signify? It indicates a shifting product mix for exports—foreign consumers are increasingly embracing PHEVs.

And the companies leading the charge in PHEV exports are, once again, the same few. In 2025, BYD and Chery accounted for over 72% of the export growth, a highly concentrated market share. This trend is expected to become even more pronounced in January of this year.

BYD’s strategy is crystal clear: in-house development of core components (batteries, motors, electronics), rigorous cost control, and models like the Seagull, which are selling well in Southeast Asia and South America. It’s not just about aesthetics; at the same price point, BYD offers a more comprehensive package. Spotting a Seagull on the streets of Bangkok with adults in the backseat and a central control screen for short videos—local consumers have never experienced such features before. That’s competitiveness in action.

Chery, on the other hand, has taken a different route, operating in the Middle East and Latin America for over two decades and establishing genuine distribution channels. Seeing a Chery on the streets of Dubai isn’t due to its affordability but because of its proper 4S stores, readily available spare parts, and reliable after-sales service. This localized operational capability cannot be replicated overnight simply by injecting capital.

But 2026 introduces new variables: joint-venture brands are now eyeing exports. For instance, Volkswagen is exporting the China-made Cupra Tavascan to Europe, FAW-Volkswagen is shipping vehicles produced in Changchun to the Middle East, and Kia is also leveraging China’s manufacturing prowess for export. These cars bear foreign brands but utilize China’s efficient supply chain. Consumers get international brand logos at a lower cost. This 'reverse export' trend is set to grow this year, with joint-venture brands becoming increasingly common on export lists alongside domestic brands.

The Market Has Shifted—Russia Is No Longer the Same

After identifying the key exporters, let’s explore where they’re selling.

The export map in 2025 already displayed clear market differentiations. Russia remained the top market with 555,000 units exported, but that represented a 46% year-on-year decrease. Context is crucial here: Chinese automakers rushed into Russia in 2023 as others withdrew, creating market gaps; in 2024, inventory piled up; by 2025, demand normalized, and exports naturally declined. Companies like Geely, Changan, and Chery, which have established local factories and adapted their products for the Russian market, continue to perform well. Parallel exporters riding the initial wave have mostly been washed out.

The UAE is another major market, with 539,700 units exported in 2025, marking a 74.3% increase and breaking the 100,000-unit mark in December alone. The Middle East is a fascinating market—wealthy consumers, a preference for SUVs, and a decent acceptance of NEVs. Chinese vehicles there aren’t positioned as cheap alternatives but come equipped with smart cockpits, dual screens, and hybrid systems. Local consumers find that Japanese cars at the same price still rely on mechanical gauges, while Chinese cars offer voice-controlled air conditioning—this contrast creates opportunities.

The European market continues to follow a 'premium route,' with Belgium importing 278,000 NEVs in 2025, mainly for re-export. However, terminal markets like the UK, Spain, and Israel all saw growth rates above 40%. UBS predicts that Chinese brands’ market share in Western Europe could rise from 5% to 15% by 2030, assuming price wars don’t escalate and product competitiveness remains strong.

Southeast Asia and Latin America are volume drivers, with Mexico exporting 490,000 units and Brazil 300,000 units, both marking over 30% year-on-year increases. However, the biggest issue in these regions is rapidly changing policies. Mexico is under U.S. scrutiny, and Brazil could impose localization requirements at any time—for example, Brazil recently terminated tariff exemptions for imported Chinese electric vehicle kits, a move driven by automakers like Volkswagen, Stellantis, GM, and Toyota. Both BYD and Great Wall Motors may be affected.

Tariffs, Containment, Localization—The Three Major Challenges Persist

On another note, while export figures look promising, the challenges on the road remain significant.

The most immediate issue is tariffs. The U.S. has just implemented new rules, raising combined tariffs on Chinese battery-grade graphite to over 160%, covering natural graphite, synthetic graphite, and anode materials. This means even if whole vehicles aren’t targeted, battery costs will rise. For automakers using Mexico as a gateway to the North American market, this is an unavoidable blow.

Europe has shifted its tactics—last year, it focused on anti-subsidy investigations; this year, it introduced 'price commitments.' Simply put: 'You’re cheap, right? Fine, we’ll set a minimum price. Below that, no entry.' This protects per-unit profits in the short term but blocks the low-price volume strategy in the long run. To survive in Europe, companies must compete on features, intelligence, and brand recognition—not just price.

Overseas automakers are also wary of China’s surging auto exports. Ford CEO Jim Farley recently expressed anxiety, calling Chinese automakers 'black swans' and even importing a Xiaomi SU7 to the U.S. for personal study. But while they talk tough, their actions are pragmatic—recent reports suggest Ford is in talks with Geely to produce Chinese vehicles at a Spanish factory, while the recently troubled Stellantis directly invested in Leapmotor to bolster its product lineup using their platform. These giants aren’t foolish; if they can’t block you, they’ll partner.

The biggest challenge remains localization. Canada recently signaled interest in establishing Sino-Canadian joint ventures, combining parts suppliers (like Magna and Linamar) with Chinese automakers’ technology to produce electric vehicles in Canada for global markets. If this materializes, it means a shift in export models—no longer 'Made in China, shipped abroad,' but 'Locally made, using local supply chains, serving local and regional markets.'

Canada aims to reduce its reliance on the U.S. market, and China’s technology and production capacity offer ready collaboration options. For Chinese automakers, this is both an opportunity and a test—whether they can meet requirements on labor standards, software security, and local supply chain development will determine the extent of these partnerships.

The Window of Opportunity Remains, but a New Approach Is Needed

Of course, there’s some good news. Germany announced in January that its €3 billion electric vehicle subsidy program is now open to all manufacturers, including Chinese brands. Canada allocated an annual quota of 49,000 units, with a 6.1% most-favored-nation tariff within the quota, temporarily setting aside the previous 100% surtax. The EU’s price commitment scheme, while setting thresholds, at least offers transparent rules, eliminating uncertainty about sudden tariff hikes.

Putting these signals together, the 2026 export market won’t just be about 'volume growth.' Last year’s impressive full-year exports of 8.32 million units and January’s 44.9% surge are noteworthy, but the real focus should be on structural adjustments.

If we only consider sales volumes, the top exporters will likely still be BYD, Chery, SAIC, Geely, and new players like Leapmotor with overseas channel advantages, especially now that Stellantis desperately needs electrification solutions. Leapmotor International, leveraging Stellantis’ overseas networks and factories, can enter European markets faster. This 'technology-for-channels' model carries less risk than going it alone. Expect more such collaborations in 2026—traditional giants need China’s technology and cost solutions, while Chinese automakers need their networks and local expertise. This mutual need will partially offset tariff and containment pressures.

Ultimately, exports hinge on products and users. Behind the numbers are real vehicles on the road, being used and evaluated. While 2026 starts with strong growth, challenges won’t disappear. Trade barriers will evolve, overseas rivals are learning fast, and localization pitfalls remain. But one thing is certain: Chinese automakers have shifted from 'testing the waters' to 'deep cultivation,' from 'selling cars' to 'building ecosystems.' As more Chinese brands establish factories overseas, increase local parts sourcing, and expand maintenance networks to more cities, the 'outsider' feeling will fade. By then, export volumes may just be numbers—what matters more is that Chinese cars become a normal, reliable, and even liked choice in local lives. That recognition is more precious than any growth rate.

The 2026 window remains open, but to thrive, a new approach is needed.

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?

-

![]()

618 Battle Report | China's Online Learning Tablet Market Sees Significant Decline in Volume and Value; Zuoyebang, Xueersi, iFLYTEK, and Xiaoyuan Account for Nearly 90% of Sales

-

![]()

AI Revolutionizes Automotive PR: The Renaissance of In-Depth Graphic Content!

-

![]()

DJI Addresses Pocket 4P 'Sold Out Immediately' Backlash: Scalpers Identified, Production Accelerated

-

![]()

Musk’s Chessboard Moves Again: SpaceX Secures Another Strategic Acquisition!