Xiaomi’s Financial Report: Automotive Arm Stabilizes While AI Bets on Future Growth

03/30 2026

03/30 2026

657

657

By Liang Tian

Source / Node AI

On March 19th, Xiaomi’s new SU7 sedan officially launched, securing 15,000 orders in just 35 minutes—a remarkable achievement. However, within a week, Xiaomi’s market value dropped by HKD 100 billion.

This mixed reception highlights the story beneath the surface: the financial report.

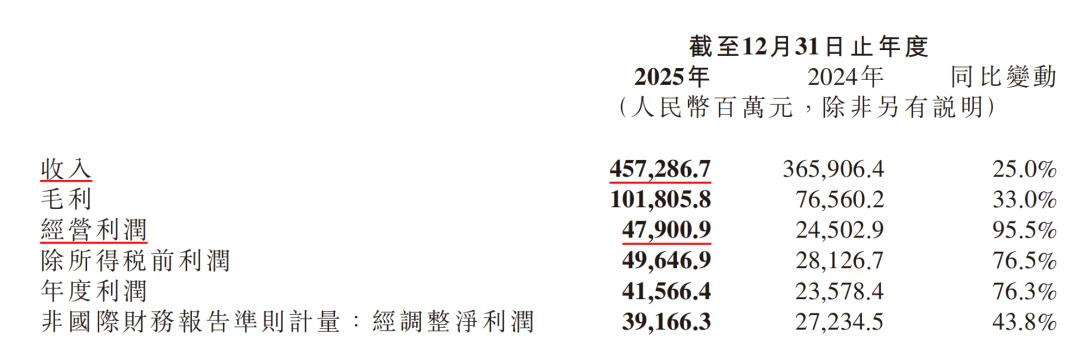

For the full year of 2025, Xiaomi reported total revenue of RMB 457.3 billion, up 25% year-on-year, with adjusted net profit reaching RMB 39.2 billion, a 43.8% increase. The automotive business achieved a major milestone, surpassing RMB 100 billion in annual revenue for the first time and delivering RMB 900 million in full-year operating profit.

Yet, the fourth quarter signaled a shift.

Quarterly revenue reached RMB 116.9 billion, growing just 7.3% year-on-year—a marked slowdown compared to the first three quarters. Adjusted net profit fell by approximately 24% year-on-year to RMB 6.3 billion.

From a capital market perspective, Xiaomi’s financial report may seem underwhelming—the reason behind the HKD 100 billion drop. The automotive business has just reached profitability but still requires heavy investment. The legacy mobile business faces pressure from the phase-out of national subsidies and rising storage costs. Xiaomi is now outlining a growth narrative for the future—during an earnings call, the company announced plans to invest RMB 60 billion in AI over the next three years.

From Node Finance’s perspective, Xiaomi stands at a critical juncture of multi-line parallel development amid a technological revolution. Established tech giants are all investing heavily in AI, and Xiaomi is no exception. The scale of this endeavor’s potential is already visible in the financial report.

410,000 Vehicles Sold in a Year, Earning RMB 6,100 per Unit

In 2025, Xiaomi delivered 410,000 vehicles, far exceeding its initial target of 300,000 units.

This pace is remarkable in today’s automotive industry.

In contrast to the adjusted net loss of RMB 6.2 billion in 2024, Xiaomi’s smart electric vehicle and AI innovation businesses (hereinafter referred to as "automotive and innovation businesses") generated RMB 106.1 billion in revenue in 2025, achieving positive full-year operating income for the first time at RMB 900 million. Q4 alone saw RMB 37.2 billion in revenue and RMB 1.1 billion in operating income, marking two consecutive quarters of profitability. After deducting RMB 1.6 billion in equity incentives, actual operating profit stood at approximately RMB 2.5 billion—indicating stronger real profitability than reported.

A rough calculation shows that the automotive and innovation businesses had a cost ratio of about 77.7%. With cumulative sales of 411,000 units, gross profit per vehicle was approximately RMB 63,000, but operating profit per vehicle was only about RMB 6,081. The difference was absorbed by R&D, sales, and administrative expenses. Operating expenditures for this segment reached RMB 24.9 billion in 2025, up 87.7% year-on-year.

These are necessary costs during the expansion phase and essential for building long-term competitive barriers.

The ASP (average selling price) of smart electric vehicles also rose, increasing from approximately RMB 234,000 in Q4 2024 to about RMB 250,000 in Q4 2025—a 6.6% increase primarily driven by deliveries of the higher-priced YU7 series.

Of course, challenges remain.

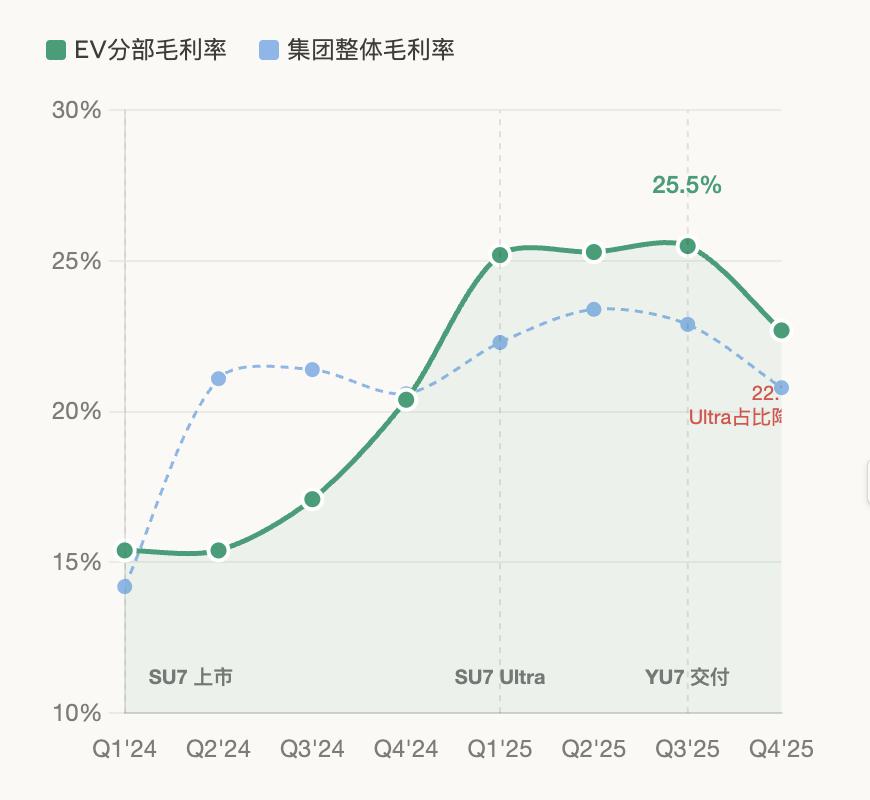

Xiaomi’s automotive gross margin was unstable, with Q4 at only 22.7%, down from Q1 (23.2%), Q2 (26.4%), and Q3 (25.5%). The decline was due to factors such as sales of existing and display vehicles.

With a gross profit of RMB 63,000 per vehicle but only RMB 6,081 in operating profit, most of the difference was consumed by R&D, sales, and administration. Naturally, these figures are difficult to optimize in the short term—Xiaomi’s operating expenditures reached RMB 24.9 billion in 2025, up 87.7% year-on-year.

Pressure also lies ahead. Xiaomi aims to deliver 550,000 vehicles in 2026, a 34% increase from 2025, meaning continued investment in production lines, stores, and after-sales networks. Sales and marketing expenses have already risen from RMB 25.4 billion in 2024 to RMB 33.2 billion in 2025 and are expected to climb further. By year-end, Xiaomi had 477 automotive sales stores. Management also reaffirmed its commitment to long-term investment in core technologies like chips, with over RMB 50 billion earmarked over ten years, and is currently developing automotive chips.

In the short term, expense ratios are unlikely to decline, making it difficult for the automotive business to immediately contribute substantial net profit. However, considering how quickly it turned profitable within two years, Xiaomi’s execution in the automotive sector has exceeded most expectations. The key now is whether economies of scale can outpace expense growth.

Storage Chip Prices Surge Sevenfold, Xiaomi Phones Raise Prices by USD 70

While the automotive business delivered surprises, the once-"pillar" mobile business faced pressure.

Full-year smartphone revenue reached RMB 186.4 billion, down 2.8% year-on-year. The fourth quarter was more pronounced, with revenue dropping 13.6% to RMB 44.3 billion from RMB 51.3 billion in Q4 2024.

Of course, this isn’t due to Xiaomi’s phones underperforming but rather a challenging macro environment.

Lu Weibing, Xiaomi Group Partner and President, admitted during the earnings call that the cycle and magnitude of memory price increases far exceeded Xiaomi’s forecasts.

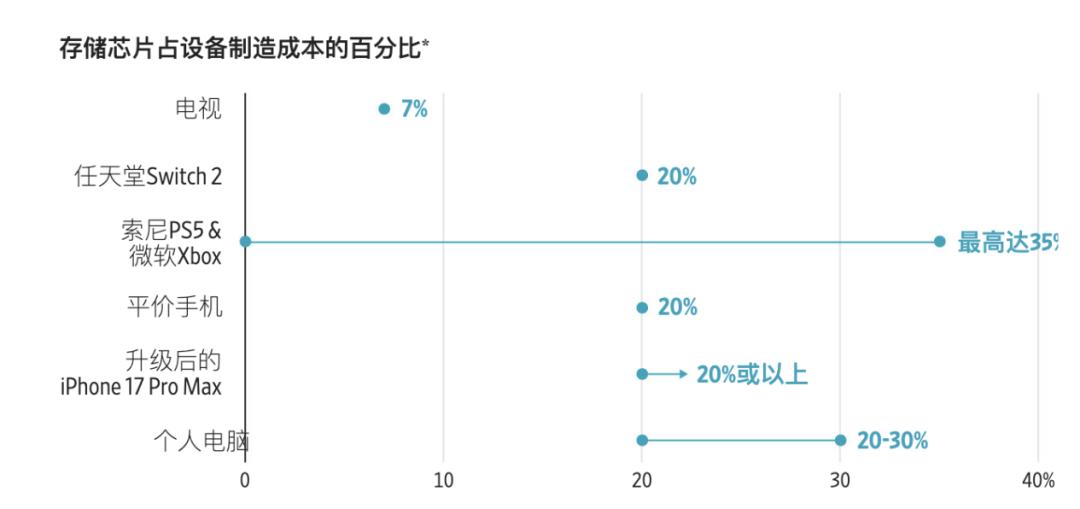

Storage chips are among the most ubiquitous and critical components in technology, primarily divided into DRAM and NAND flash memory. DRAM handles short-term, immediate tasks like running applications, while NAND flash memory is used for long-term storage of photos, videos, and other data, typically accounting for about 20% of a device’s total cost.

According to TrendForce’s tracking data, contract prices for DRAM and NAND flash memory have surged approximately sevenfold over the past 12 months, impacting

Recently, manufacturers like OPPO and vivo officially announced price hikes for their phones. In response, Lu Weibing stated that he fully understands this approach, as no phone maker would willingly raise prices unless absolutely necessary. "If we can’t hold out, Xiaomi will also raise prices. We hope consumers will understand when that happens—the trend of price increases is ultimately inevitable."

Xiaomi is already responding with product strategy adjustments. According to public information, the new Xiaomi flagship phone, the 17 Ultra, no longer offers a 256 GB version, instead providing only a version with double the storage space at a price about USD 70 higher than the previous model.

IDC indicates that storage supply challenges will persist throughout 2026 and may continue into 2027. Global smartphone shipments are expected to decline by 12.9% in 2026, with revenue dropping by 0.5%. Growth is anticipated to resume at 1.9% in 2027 and rebound to 5.2% in 2028.

This means Xiaomi faces significant challenges this year.

A 1 Billion-Device Ecosystem: Xiaomi Aims for Premiumization

Beyond mobile phones and automobiles, IoT and consumer products represent Xiaomi’s most underrated business segment.

Full-year revenue reached RMB 123.2 billion, up 18.3% year-on-year, setting new historical highs both domestically and internationally. Gross margin stood at 23.1%, a 2.8% year-on-year improvement, far surpassing the mobile business’s 10.8%, with full-year gross profit reaching approximately RMB 28.5 billion—a key profit driver.

In terms of scale, by the end of 2025, Xiaomi’s AIoT platform connected over 1 billion devices, making it the world’s largest consumer IoT platform and the infrastructure for Xiaomi’s "human-vehicle-home" ecosystem.

Xiaomi is also actively expanding into new product categories.

In June 2025, it launched AI glasses, selling nearly 50,000 units in the first three days. Overall, Xiaomi’s AI glasses ranked third globally in shipments and first in mainland China for 2025.

However, Q4 data revealed concerns.

IoT revenue for the quarter was only RMB 24.6 billion, down about 20% year-on-year—the lowest among all four quarters of the year. This was primarily due to a sharp decline in smart large appliance sales following the phase-out of national subsidies. This suggests that much of the high growth in large appliances during the first half of the year was driven by policy incentives rather than pure organic demand.

A deeper challenge lies in premiumization.

Xiaomi IoT’s core strengths are affordability and ecological synergy, using the Mi Home app to connect phones, air conditioners, refrigerators, and robot vacuums into a closed loop.

However, in the large appliance sector, Xiaomi still lags significantly behind Midea, Haier, and Gree in core technologies, offline installation services, and premium brand perception.

Currently ranked fourth in air conditioners, Xiaomi sits behind Gree, Midea, and Haier—each with decades of channel accumulation and manufacturing experience.

Fortunately, management has clear goals. Lu Weibing aims to make Xiaomi the top two air conditioner brand in China by 2030—an aggressive target but one that shows management understands the gaps and where to focus efforts.

Of course, the value of the IoT business cannot be measured solely by profit, nor can it be simply compared to established home appliance players—it provides Xiaomi’s AI with the richest hardware scenarios and user touchpoints. When AI truly penetrates endpoints, these 1 billion devices will represent Xiaomi’s greatest first-mover advantage.

AI Isn’t in a Rush to Monetize: Human-Vehicle-Home as Key Infrastructure

After all this, we can finally discuss AI. Xiaomi is a latecomer to AI, but considering the short time frame, its achievements are commendable—and the company places great importance on AI, as evidenced by the nearly half-page coverage of AI-related topics in its financial report.

Xiaomi is a true doer—after recruiting Luo Fuli, the "genius girl" from DeepSeek in 2025, the company made frequent moves that year:

In December 2025, Xiaomi released and open-sourced MiMo-V2-Flash;

In March 2026, facing the Agent era, Xiaomi unveiled MiMo-V2-Pro, boasting over one trillion total parameters, a hybrid attention architecture, and support for one million-token context lengths. An interesting side note: before its official release, Xiaomi first launched the model on the Open Router large model arena under the alias Hunter/Healing Alpha, sparking speculation that it was DeepSeek V4.

On the Artificial Analysis large model intelligence index, MiMo-V2-Pro ranked eighth globally by model and fifth by brand. On the PinchBench agent evaluation leaderboard, it achieved the third-highest average task completion rate globally. On the OpenRouter platform, MiMo-V2-Pro ranked first in model call volume.

Xiaomi also released the full-modality foundation model MiMo-V2-Omni, which integrates text, vision, and voice capabilities, natively supporting multimodal perception, tool invocation, function execution, and GUI operation. On the PinchBench leaderboard, MiMo-V2-Omni ranked second globally in average task completion rate.

Amid the craze for lobster-themed models among major companies, in March 2026, Xiaomi launched a small-scale closed beta for Xiaomi Miclaw, a mobile Agent built on the MiMo large model.

Xiaomi claims Miclaw aims to transform phones into AI tools, understanding user intent and, with authorization, invoking apps and ecological capabilities. It can autonomously select system-level tools to complete user commands, continuously adjust behavior, expand capabilities, and accumulate experience through a memory system.

From the financial report, AI and other innovation businesses have not yet generated substantial direct revenue for Xiaomi, but investment is accelerating. Based on the earnings call, Xiaomi itself is not overly concerned with immediate monetization.

Lu Weibing revealed that Xiaomi will invest RMB 16 billion in AI, embodied intelligence, and other fields in 2026, with total investment exceeding RMB 60 billion over the next three years. This may pose certain challenges to future profits.

However, we must look beyond immediate gains. Amid a global tech industry burning money on AI, Xiaomi at least possesses something most AI companies lack: a real-world application ecosystem spanning phones, homes, automobiles, and wearables. If AI capabilities truly mature, Xiaomi may be the fastest to deliver them to users.

Xiaomi’s current situation shares similarities with Tencent and Alibaba—all are investing current profits into future growth. The difference is that Tencent and Alibaba’s core businesses remain highly profitable cash cows, while Xiaomi’s mobile business is under pressure, its automotive business has just crossed the break-even point, and its AI business is still in the pure investment phase. However, from another perspective, Xiaomi may be one of the few Chinese tech companies today that simultaneously holds "hardware scale, ecological connectivity, and AI capabilities"—three critical assets. There are challenges, but also opportunities. It’s difficult to declare a clear winner amid this emerging tech wave, and that’s the challenge every company faces.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?