Global Capital Betting Big on Chinese Robotics

05/12 2026

05/12 2026

476

476

Author: Tang Fei

Editor: Li Xiaotian

In the spring of 2026, China's robotics industry is experiencing an unprecedented wave of capital migration.

Since April alone, nine companies have secured large-scale financing rounds exceeding RMB 1 billion. Among them, TStone Robotics raised over RMB 3 billion in a single round, setting an industry record.

The first quarter was even more frenetic. According to incomplete statistics from IT Juzi, over 200 financing events were disclosed in Q1 2026 (approximately 90 days), with total disclosed funding surpassing RMB 30 billion. On average, more than two robotics-related companies secured financing each day.

The secondary market is also surging. Multiple A-share "robotics concept stocks" have seen significant gains. Among the strongest-performing sectors in Q1, Unitree Robotics concepts rose by 31%, while humanoid robotics concept groups recorded 28%-30% growth.

Analyzing investment trends in this wave reveals that foreign capital is becoming a dominant force in both primary and secondary markets.

From a financing structure perspective, international capital's layout (strategic layout ) in China's robotics industry exhibits a clear "dumbbell" pattern: one end involves participating in early-stage unlisted companies through primary markets to secure key technology tracks in advance; the other end involves heavily investing in listed industry leaders through secondary markets to share in the industry's rapid growth dividends.

Extending the timeline reveals that two years ago, China's robotics financing landscape was dominated by Chinese capital. However, a noticeable shift this year is the rapidly rising visibility of international capital.

In April, Digua Robotics announced the completion of a USD 150 million Series B2 financing round, with foreign investors including Prosperity7 Ventures (Saudi Arabia), LOOK CAPITAL (Singapore), and Vertex Growth (Singapore). Long-time investor Vertex Growth has been involved since Series A, consistently increasing its stake in each subsequent round.

Around the same time, Bain Capital, a U.S. private equity giant, announced a strategic investment in Chinese smart tool and robotics company Powerplus Group. Bain explicitly stated in its official announcement that this investment would support Powerplus's next phase of international growth, product innovation, and expansion into high-growth categories.

Foreign capital presence intensified throughout Q1. Starry Robotics' RMB 1 billion strategic financing round saw participation from three foreign investors: Samsung (South Korea), Woori Capital (South Korea), and Singtel (Singapore). In February, Qianxun Intelligence secured reinvestment from existing shareholder Prosperity7. During LimX Dynamics' Series B round, UAE-based Stone Ventures participated, while Qiongche Intelligence's Series A round saw involvement from Sea Limited (Singaporean tech company) and Prosperity7.

According to CVSource statistics from Touzi Jiachuan, among China's over 200 embodied AI companies, 19 have received investments from overseas institutions (excluding Hong Kong funds). South Korean and Southeast Asian investors and industrial players have all made moves, with Middle Eastern capital placing the largest bets.

For instance, Prosperity7, a diversified venture fund under Saudi Aramco named after Saudi Arabia's first oil-producing well "Prosperity Well," has invested in multiple companies beyond Digua Robotics, Qianxun Intelligence, and Qiongche Intelligence. It is also an investor in Keenon Robotics, Fourier Intelligence, and JAKA Robotics.

Like Prosperity7, Stone Ventures from the Middle East is another significant investor in Chinese robotics.

Headquartered in Dubai, UAE, Stone Ventures focuses on emerging Asian markets, particularly hard technology sectors in China. Its portfolio includes LimX Dynamics and Neolix Robotics, with three consecutive investment rounds in Qixin Robotics.

This capital insight and activity are not confined to unlisted companies; some listed robotics concept stocks have also become key targets for foreign capital.

With all A-share first-quarter reports disclosed, the latest holdings landscape of QFIIs (Qualified Foreign Institutional Investors) has emerged.

For example, Goldman Sachs' top-held stock by market value is chip concept stock OmniVision; Barclays' largest holding is newly added robotics concept stock Huagong Technology, with 2.5563 million shares, ranking 10th among the company's top ten tradable shareholders. UBS is also actively deploying in the AI supply chain, with multiple new market favorites among its top 20 holdings, such as Yuanjie Technology, TFC Communication, and Demingli. Simultaneously, UBS is not only betting on individual stocks but also increasing its stake in Chinese robotics chip leader Rockchip through ETFs, while heavily holding 8.66 million shares of Shiyun Circuit, which supplies high-temperature-resistant PCBs for Tesla robots.

From primary to secondary markets, from startups to industry leaders, international capital is systematically betting big on China's robotics industry. This is no by chance (coincidence) but based on a fundamental assessment: China has established comprehensive advantages in robotics.

Capital's instincts rarely err. When frontline institutions like Samsung, Singtel, Goldman Sachs, and UBS repeatedly bet on the same sector, a shared underlying logic must exist.

Breaking it down, the core drivers of international capital's heavy investment in Chinese robotics stem from the superposition (superposition) of three critical dimensions: technology, application, and capital. These three advantages reinforce and support each other, forming a unique industrial ecosystem barrier for "Chinese robotics."

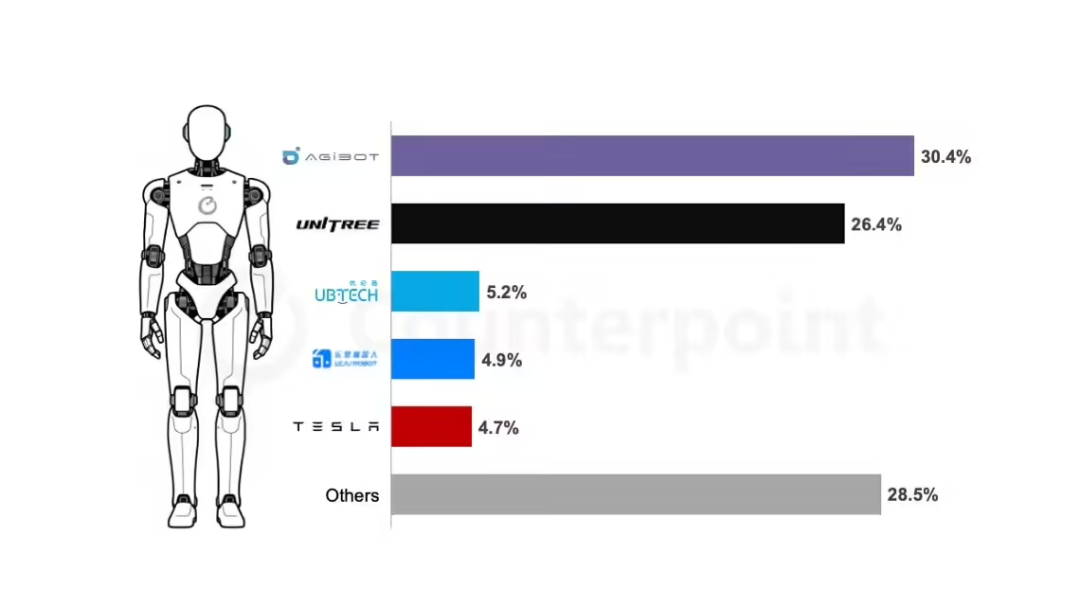

First, in terms of technology, China's robotics industry has evolved from "assembly integration" to "full-stack self-research." Market research firm CounterPoint Research released a report early this year stating that 2025 will see a commercialization boom in the global humanoid robotics industry, with approximately 16,000 units installed annually, of which China will contribute over 80%. Moreover, the head effect (leading firm effect) is pronounced, with Chinese companies occupying the top four spots in the industry CR5.

Source: CounterPoint Research

Notably, in February 2026, China's first "Humanoid Robotics and Embodied AI Standards System (2026 Edition)" was officially released, covering over 200 detailed rules across six major sectors, including foundational commonalities and safety ethics, clearing institutional barriers for corporate collaboration and large-scale production. This dual drive of "technology + standards" is forming a systematic competitiveness for China's robotics industry.

Second, China boasts the world's richest and most diverse robotics application scenarios, with market depth surpassing any single economy.

Data shows that China has been the world's largest industrial robot application market for 12 consecutive years, with market influence continuously rising. According to the National Bureau of Statistics, in 2025, China's industrial robot output reached 773,000 units, up 28.0% year-on-year, while service robot output reached 18.581 million units, up 16.1% year-on-year.

These robots' "working lives" may begin in diverse scenarios such as logistics distribution, smart retail, healthcare, and education. For example, Starry Robotics has partnered with China Post and SF Group to deploy robots in over ten logistics centers, with some centers' embodied AI robots achieving over 85% efficiency compared to human levels. Fourier Intelligence collaborated with Yangzhi Rehabilitation Hospital affiliated with Tongji University to develop the Galileo system, covering simulation scenarios like daily living, occupational labor, driving simulation, mountain climbing, and glass walkway navigation to help patients regain self-care abilities. Galaxy General's "Galaxy Space Capsule" unmanned retail model has been deployed in over 20 Chinese cities.

Goldman Sachs noted in its research that Chinese humanoid robots are shifting from "general concepts" to vertical scenarios leveraging existing capabilities, such as security patrols, public space guidance services, and factory logistics sorting. This pragmatic approach is driving major manufacturers to set 2026-2027 shipment targets at multiple times their 2025 levels.

Simultaneously, 2025 marked the first inclusion of "embodied AI" in the government work report; in 2026, the 15th Five-Year Plan incorporated it into six key future industry layout (strategic layout ), elevating it to a national strategic level. Beijing, Shanghai, Hubei, and other regions have established hundred-billion-yuan industrial funds, forming a policy system with central-local coordination and full-chain promotion.

Finally, China's capital market's inclusiveness toward hard technology provides efficient listing and exit channels for robotics companies. For example, Unitree Technology's IPO application, from initiating IPO counseling in July last year to formal acceptance by the Shanghai Stock Exchange, took only 132 days.

Hong Kong stock investors are also highly optimistic about the robotics industry. In March, Kainergy, specializing in intelligent warehousing and logistics equipment, successfully listed on the Hong Kong Stock Exchange. Its public offering was oversubscribed by 2,153 times, closing at HKD 30.70 on its debut day, up 84.27%, with an intraday peak gain of 109%. That same month, Huayan Robotics listed on the Hong Kong Stock Exchange, with its IPO public offering oversubscribed by 5,059 times, setting an annual record for Hong Kong's new stock oversubscription, with an intraday peak gain of 25.88%.

Industry analysts note that intelligent transformation (intelligent transformation) across industries has become a major trend, with the robotics industry's growth logic remaining solid. In the future, driven by technological innovation, scenario expansion, and import substitution, the industry's high business climate (prosperity) will continue. International capital's judgment to "bet big on China" is thus unsurprising.

Li Mingshun, founder of Shunfu Capital, pointed out that when overseas capital invests in domestic embodied AI companies, they tend to focus on those with relatively mature commercialization and capitalization. "They may not invest in very early-stage companies but rather in mid-to-late-stage ones with greater certainty, capable of exiting through capital markets."

Beyond these reasons, international capital has its own considerations when making investments.

From a policy and strategic perspective, Middle Eastern capital's heavy investment in China's robotics industry is "reserving space" for its own development.

On one hand, amid energy transition, Middle Eastern capital is actively seeking growth engines for the "post-oil era," with AI and robotics seen as new strategic industries. For example, the UAE's "Smart Dubai" plan explicitly aims to increase AI's economic contribution to 14% by 2031, promoting large-scale local deployment of AI robotics solutions. In Saudi Arabia's Neom (New Future City) project vision, this future city will house more robots than humans, with solar panels sufficient to cover China's Great Wall.

On the other hand, Middle Eastern sovereign funds' past investment paths relied too heavily on the U.S., creating significant risks under geopolitical conflicts. Thus, diversification has become the new strategic theme for these funds.

More international capital is motivated by optimism toward China's robotics industry and a desire for long-term growth companionship. For instance, Bain Capital partner Xu Yuyi expressed recognition of Powerplus's global brand strength and innovation capabilities, vowing to support its next-generation technology investments. Vertex Growth's investment in Digua Robotics stems from deep recognition of its "replicable success experiences" and high confidence in its technological barriers and ecosystem potential in the embodied AI infrastructure sector.

Over the past year, Elon Musk has repeatedly emphasized a core judgment at the Davos Forum, Tesla earnings calls, the X platform, and multiple in-depth interviews: "China is not 'rising' but 'restoring' its historically deserved technological and manufacturing status." He straightforward (bluntly stated) that China has formed a "trinity" of systemic advantages in power generation capacity, AI computing power, new energy vehicles, and supply chain resilience.

What truly concerns him, however, is China's globally most complete robotics supply chain system.

In Shenzhen, a startup can go from designing a robotic dexterous hand to receiving samples in just three days; in Europe and the U.S., this cycle may span months. Core components for humanoid robots, such as servo motors, harmonic reducers, and sensors, all have domestic suppliers in China, with localization rates increasing annually.

In the past, Chinese robots primarily played the roles of "manufacturers" and "assemblers" in the global value chain, earning the lowest profits on the "smile curve."

Now, the landscape is undergoing fundamental changes. With technological strength and capital advantages, Chinese companies are beginning to move upstream in the industrial chain and towards the ecological platform layer. The business models of leading companies have also made the leap from 'burning money to show off technical prowess' to 'product revenue streams.'

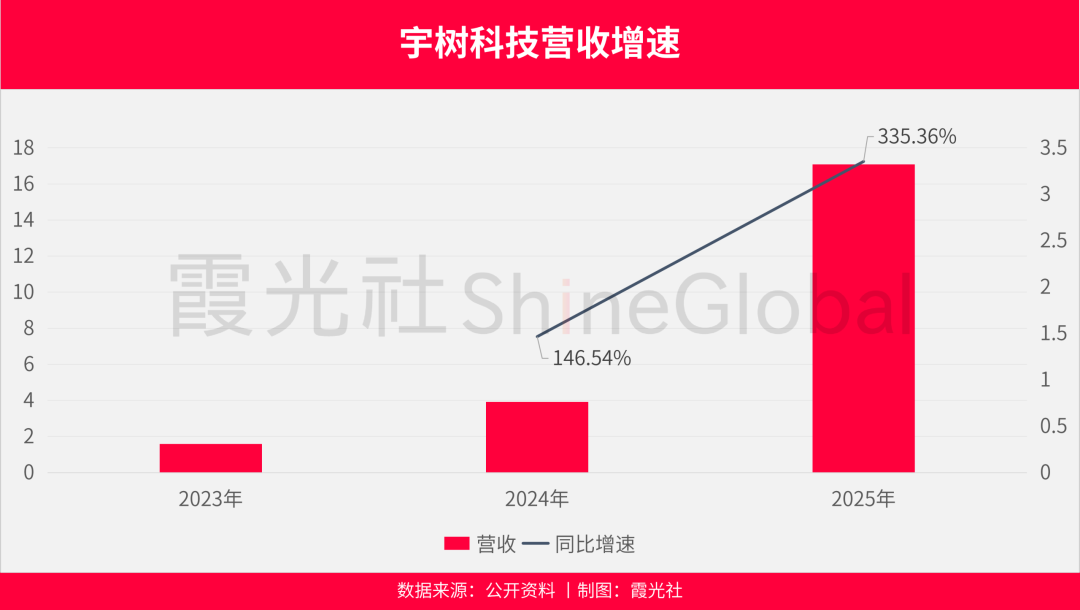

Unitree Technology achieved revenue of RMB 1.708 billion in 2025, a year-on-year increase of 335%, with a gross profit margin as high as 60%, establishing initial 'self-sustaining capabilities.' During the same period, UBTECH's revenue reached RMB 2.001 billion, a year-on-year increase of 53.3%, ranking it first among global humanoid robot companies, with revenue from full-sized humanoid robots surging more than 22-fold in a single category.

However, amid this massive industrial wave, some maintain a cautious attitude. At the end of last year, a relevant official from the Policy Research Office of the National Development and Reform Commission stated at a press conference that 'speed' and 'bubbles' have always been issues that need to be balanced in the development of cutting-edge industries, and the same applies to the humanoid robot industry. While the rapid influx of capital is beneficial for innovation, it is also necessary to guard against risks such as the simultaneous launch of similar products and compressed research and development space.

In March of this year, Zhu Xiaohu, Managing Partner of GSR Ventures, publicly stated that the company is exiting investment projects in the humanoid robot sector in batches. He pointed out that humanoid robot companies generally face two major challenges: first, high technological costs, with single-unit prices often reaching tens of thousands of yuan, far exceeding the willingness to pay in actual scenarios; second, vague application scenarios, with many companies proposing customer needs that 'seem more like imagination than reality.'

Liu Bo, Partner at Crystal Stream Capital, shares a similar view, stating, 'Over the past two years, among the dozens of companies claiming to be in the embodied AI space, most are more about embodiment than intelligence.' This is because most of the hot capital has flowed into the visible and tangible hardware manufacturing sector, while the core factors that determine whether robots can truly 'work'—embodied large models and high-quality physical data—are facing a severe 'data shortage.'

However, on the whole, the strategic direction of China's robotics industry is clear. This all-encompassing ecological advantage is transforming China's role in the global robotics industry—no longer just the 'largest market' and 'main factory,' but increasingly becoming the 'core hub' and 'standard setter.' The next three to five years will be a critical window for reshaping the global robotics landscape, and China is standing at the forefront of this wave.

References:

[1] '2026 Humanoid Robot Industry Report,' McKinsey & Company

[2] '2026 In-Depth Analysis Report on the Intelligent Robot Industry,' China Investment Consulting

[3] 'In-Depth Analysis Report on Robot Development in China and the United States,' China Science & Technology Venture Capital Research Institute

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!

-

![]()

AI Agent Smartphones: The Next Competitive Edge Transcends Large Models

-

![]()

Over 880 Million Yuan Worth of Orders Unveiled, Bidding Launched for Shenzhen Eastern Public Transport

-

![]()

Tesla's Robotaxi Hits the Road: A Monumental Gamble with an Uncertain Future