Challenges in Claim Settlements and Soaring Premiums: A Ping An Good Car Owner's Tale of Woe

05/12 2026

05/12 2026

463

463

Should owners of gasoline-powered vehicles be held responsible for the high maintenance costs associated with new energy vehicles (NEVs)?

What should a vehicle owner do in the event of a traffic accident? For most, the immediate response would be to file an insurance claim.

However, some vehicle owners who have purchased auto insurance from Ping An find themselves entangled in a web of buck-passing during the claim settlement process. Agents become unresponsive, claim payments are delayed, and owners face instances of underpricing or even outright denial of claims, leading to significant distress.

On the flip side, when renewing their Ping An auto insurance policies, owners may encounter unfulfilled verbal promises, a perplexing pricing system, and unexplained premium hikes.

Why are auto insurance premiums on the rise, despite a year free of accidents and unchanged coverage? This trend appears to be linked to the growing popularity of NEVs, which has driven up vehicle maintenance costs and exerted pressure on insurance companies' performance.

Beyond Ping An, insurance giants like China Life, PICC, and China Pacific Insurance have also witnessed a general uptick in auto insurance premiums for the same reason.

It seems that the difficulties in claim settlement with Ping An auto insurance, compounded by issues with some agents, may also stem from the company's performance pressures. Striking a balance between performance and service remains a long-standing challenge for Ping An Property & Casualty Insurance.

How arduous is the process of getting an auto insurance claim settled?

Recently, Ping An released its financial report for the first quarter of 2026, revealing an operating profit of 40.78 billion yuan, marking a 7.6% year-on-year increase.

Within these figures, property insurance premiums reached 90.951 billion yuan, up 6.8% year-on-year, while insurance service income stood at 84.334 billion yuan, a 3.9% increase from the previous year.

Ping An's performance growth is noteworthy, but some vehicle owners who have purchased auto insurance from the company are growing uneasy after seeing these results.

This is because, when involved in a traffic accident and in need of insurance compensation, they may encounter hurdles in the claim settlement process for various reasons, which manifest in three primary ways:

Firstly, there's the issue of unresponsive agents.

While reversing in Guizhou, Xiao Wang accidentally damaged a tail light. After reporting the incident to Ping An auto insurance, the agent requested photos. However, after sending the photos, the agent ceased all communication, failing to respond to messages or answer calls.

In desperation, Xiao Wang sought assistance from Ping An auto insurance's concierge service, who advised him to visit a 4S shop directly for damage assessment and leave the claims adjuster's contact information with the shop.

After a frustrating ordeal without a response, Xiao Wang eventually managed to get his claim settled and his vehicle repaired, but the unresponsive attitude of the Ping An agent left him feeling disheartened.

Secondly, there's the issue of delayed claim payments.

The lack of responsiveness from insurance agents leaves accident victims in a state of limbo; when claim payments are delayed, owners endure the agony of waiting.

Xiao Mei, a Wuling Bingguo owner in Guangxi, recently collided with an unlicensed electric tricycle at the entrance of her residential area. The traffic police determined that the accident was 70% the other party's fault and 30% hers.

However, despite the tricycle owner having already paid compensation, Ping An auto insurance's claim process was tardy, causing Xiao Mei increasing anxiety.

She shared with Pang Ge: 'The damage assessment took a week, preparing the materials took another week, and processing the claim took yet another week. Now, more than half a month has passed, and the claim still hasn't been settled.'

Finally, there's the possibility of underpricing or even denial of claims.

Aqiang, a Geely Yuanjing owner in Dalian, was involved in a serious accident not long ago. After negotiating with Ping An Property & Casualty Insurance, the damage assessment amount was set at 42,000 yuan.

However, during subsequent processing, Ping An engaged an assessment company to request a modification of the agreed-upon 42,000 yuan compensation in the one-time damage assessment agreement to 26,500 yuan.

On the other hand, netizen Doudou also shared her experience: 'I bought a car last October and hit a railing after the Chinese New Year this year. Since I was in a different location and didn't report the accident on-site, the Ping An auto insurance agent later suspected that my vehicle was for commercial use because it had traveled 24,000 kilometers. They asked me to provide various pieces of evidence and then kept passing the buck, never settling the claim.'

Why are premiums increasing?

After a traffic accident, Ping An auto insurance agents often adopt a passive stance; however, before premium payment, their proactive approach starkly contrasts with their current behavior.

Simultaneously, during the process of paying auto insurance premiums, owners may also be caught off guard by agents' tactics and face hidden charges.

The first issue is unfulfilled verbal promises.

Aduo, a vehicle owner in Shenyang, recounted to Pang Ge: 'Before my car insurance expired at the end of last year, I received a call from a stranger claiming to be a Ping An auto insurance agent, who accurately provided my license plate number, chassis number, and previous insurance coverage. He said he was trying to meet his year-end performance targets and offered a substantial rebate. After purchasing the insurance as instructed, the promised rebate never materialized. When I contacted the agent, they initially delayed and then ceased all communication.'

The second issue is a confusing pricing system.

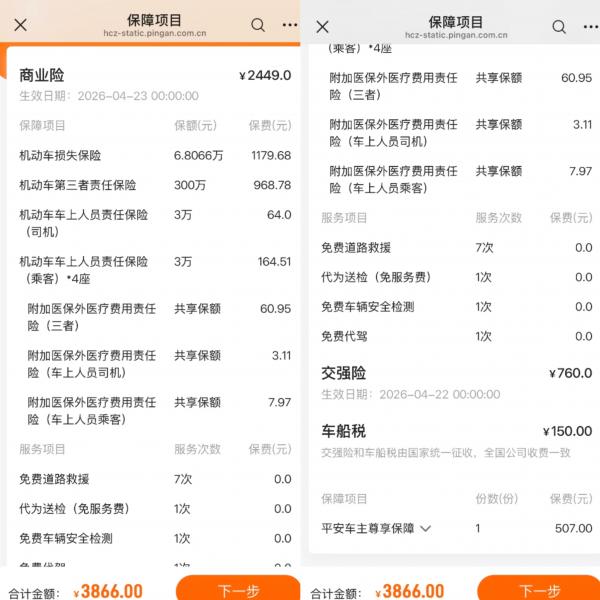

Vehicle owner Xiaojing remarked: 'When I inquired about renewing my Ping An auto insurance, the quote was 5,700 yuan a month ago, but a month later, it had surged to 7,700 yuan. The problem is that I didn't have any accidents last year, so why the sudden price hike?'

On the other hand, another netizen discovered that they had always purchased auto insurance from Ping An and agreed to the bundled 'Ping An Vehicle Owner Exclusive Protection' package. However, upon renewal, they found that the price of this package, which was 556 yuan last year, had doubled to 1,016 yuan this year.

The double blow before premium payment may catch many vehicle owners off guard. When they see the final amount on their policy, they may also discover that their auto insurance costs have increased despite having no accidents last year.

Xiao Zhang, a XPeng G3 owner, shared with Pang Ge: 'This is my fourth year of insurance, and Ping An quoted me over 4,100 yuan, but last year it was only over 3,400 yuan.'

Levin owner Bubu also mentioned: 'For the second year of renewing my Ping An auto insurance, the quoted price after discounts is 3,236 yuan. However, despite having no accidents throughout the year and the coverage remaining the same, my insurance cost last year was 3,070 yuan, which was 166 yuan cheaper than this year.'

The increasing premiums for Ping An auto insurance seem to defy industry norms; however, other auto insurance companies such as China Life, PICC, and China Pacific Insurance may also experience premium increases despite no accidents.

Are gasoline vehicle owners bearing the brunt for electric vehicles?

The aforementioned premium increases for many vehicle owners when purchasing auto insurance may be linked to their vehicle model.

Xiaodan, a Ping An auto insurance agent, explained to Pang Ge: 'The premium coefficient for auto insurance is influenced by overall market conditions, the owner's age, traffic violations, vehicle model, etc. Certain models have a higher accident rate, resulting in higher claim costs for the company, and thus a higher premium coefficient for those models.'

At the same time, she also mentioned: 'Some new energy vehicle brands have fewer 4S shops and expensive spare parts, leading to higher maintenance costs and, consequently, higher insurance premiums. This is all based on big data analysis, and of course, it varies by region.'

After consulting with multiple auto insurance professionals, Pang Ge learned that gasoline vehicles from Japanese brands like Toyota, Honda, and Nissan generally have lower premium coefficients. In the NEV sector, models from Avita and Tesla have relatively cheaper premiums.

It's evident that the calculation of auto insurance premium increases or decreases not only considers the owner's individual circumstances but also the overall performance of the vehicle model. Some NEV owners with higher accident rates and maintenance costs may be pleasantly surprised when purchasing their vehicles but face distress when purchasing auto insurance.

However, why do some vehicle owners who drive gasoline vehicles, which have lower maintenance costs than NEVs, also face premium increases?

This may be because the increasing popularity of NEVs has led to higher overall costs for auto insurance companies, forcing them to pass on some of these costs to gasoline vehicle owners. Those who choose gasoline vehicles become passive scapegoats for electric vehicles.

It's clear that while NEVs are experiencing sales growth, their high maintenance costs and repair difficulties are not only troubling many vehicle owners but also exerting pressure on auto insurance companies.

Against this backdrop, the reasons for the three types of buck-passing employed by auto insurance companies like Ping An during claim settlement, often leading to a convoluted process, seem to be emerging.

However, these increasingly stringent claim settlement rules will not only degrade the owner's experience and tarnish the company's reputation but may also lead to more miscarriages of justice, causing Ping An good vehicle owners to become modern-day victims of injustice.

After all, for insurance companies like Ping An, balancing profit and user service remains an issue that cannot be overlooked.

-

![]()

Liang Wenfeng: Marching to His Own Beat

-

![]()

Trillion-Yuan Intelligent Computing Market Surge: Key Trends in the Computing Power Industry

-

![]()

Global Capital Betting Big on Chinese Robotics

-

Summary of the Online Voice Recorder Market in Q1 2026: A Touchstone for AI Integration into Hardware, with Initial Signs of Ecosystem-Based Competition Emerging

-

Summary of the Online Drone Market in Q1 2026: Ecological Breakthrough and High-Quality Development of the Low-Altitude Economy Entering a New Phase

-

![]()

Challenges in Claim Settlements and Soaring Premiums: A Ping An Good Car Owner's Tale of Woe

-

![]()

AI Glasses Achieve Breakthrough with Lightweight Design: Materials and Balance Emerge as Key Competitive Factors

-

![]()

Volvo Needs Geely, But Not Too Much Like Geely