Is Kling AI the 'Solution' for Tencent's 'Ailing Venture'?

05/15 2026

05/15 2026

619

619

Editor: Liu Zhicheng

Reviewer: Xu Xu

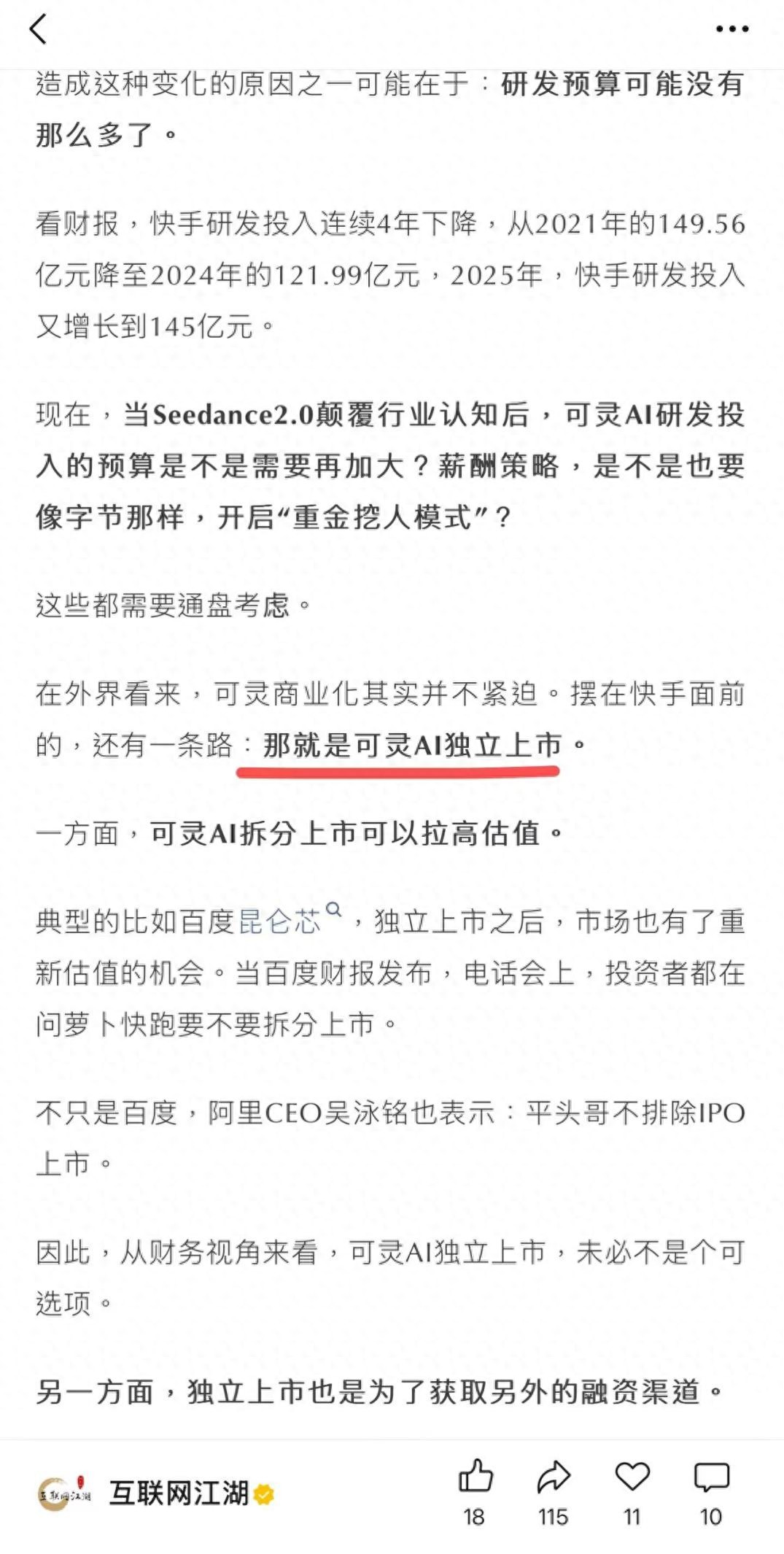

Recently, there has been widespread news about the impending spin-off of Kling.

However, this development comes as no surprise to us.

As early as two months ago, in our analysis article on Kuaishou titled 'Kuaishou Witnesses Revenue and Profit Surge: Will Kling AI Be the Next Big Thing?', we forecasted that spinning off Kling independently would serve as a significant strategic move for Kuaishou.

The only unexpected aspect was the swiftness with which this strategic move was executed.

Yet, upon closer inspection, it becomes comprehensible.

From the end of last year to the present, ByteDance's Seedance 2.0 has reshaped the industry landscape, followed by Alibaba's launch of Happy Horse. With these industry behemoths taking the lead, Kling AI suddenly appeared less groundbreaking.

Thus, Kuaishou could not afford to delay any further. Kling needed to realize its potential ahead of schedule to mitigate prolonged uncertainties.

But then, what implications does this spin-off hold for Kling, Kuaishou, and the rumored investors, such as Tencent?

The Pros and Cons of Kling's Spin-off

From a proactive standpoint, spinning off Kuaishou's Kling offers several advantages.

For instance, post-spin-off, Kling can independently secure funding and attract more external capital.

As reported by media outlets like Lan Jing News and 21st Century Business Herald, market rumors suggest that 'Kling plans to raise $2 billion in this funding round and is in discussions with investors such as Tencent.'

Moreover, Kling can break free from the value logic system of its parent company, Kuaishou, fully unlock its valuation potential, and, akin to DeepSeek and ByteDance's Seed team, utilize stock options to retain and attract top AI talent.

The most direct evidence is Goldman Sachs' earlier estimate this year, which valued Kling, as implied by Kuaishou's stock price, at only around $5 billion. However, the current rumored target valuation for Kling stands at $20 billion...

Furthermore, for the parent company Kuaishou, an independent Kling could enhance profit margins. After all, despite Kling's robust revenue growth, its investments are substantial, and profitability remains a distant goal.

Kuaishou's CFO, Jin Bing, noted during the Q1 2026 earnings call that the group's overall Capex (capital expenditure) is expected to reach approximately 26 billion yuan in 2026.

The additional 11 billion yuan investment compared to 2025 will primarily support Kling's large model and other foundational large models' computing power.

In contrast, Kuaishou's net profit attributable to shareholders for the entire year of 2025 was only 18.62 billion yuan...

Given this scenario, it seems Kling should have been spun off much earlier. But why did Kuaishou wait until now, and so abruptly?

This leads us to the other side of the story: the spin-off of Kling may also reflect Kuaishou's necessity.

More bluntly, Kuaishou may now feel a heightened sense of urgency in the video generation sector.

It's worth noting that last September, the leading players in the video generation sector were primarily Kling, AISHI Technology, and MiniMax.

This year, ByteDance's Seedance 2.0 and Alibaba's Happy Horse have emerged as the new frontrunners.

During this period, Kunlun Wanwei's Tiangong AI large model, SkyReels V4, also topped the global Artificial Analysis ranking list for Chinese text-to-video generation.

Additionally, SenseTime took a unique approach by launching SEKO 2.0, the industry's first intelligent agent for integrated creation and multi-episode generation. This has not only attracted hundreds of thousands of creators but also made the concept of a 'one-person production team' a reality.

So, will there be a second or third Happy Horse in the future video generation sector? It's hard to predict.

But what is certain is that in such a fiercely competitive environment, where companies of all sizes are constantly surpassing each other, Kling's technological lead cannot be stabilized, and corresponding market uncertainties will continue to rise, naturally suppressing its overall valuation premium space.

After all, Kling's current valuation is primarily based on Annualized Recurring Revenue (ARR). For example, based on its January performance this year, Kling's full-year ARR could surpass $300 million.

However, in the actual market, after Happy Horse's official launch at the end of April, if the product performs well and is competitively priced, Kling's API calls and user subscription fees will inevitably be impacted. Whether it can still achieve $300 million in revenue remains uncertain.

Of course, even so, after Sora's shutdown, many believe that technological capability may not be the true competitive edge; a closed commercial ecosystem is.

But a closer look reveals that Sora's downfall was not primarily due to a lack of supporting commercial ecosystems but rather 'issues' with its technological direction and being surpassed in product performance.

If Kling's starting point is to 'enable everyone to create the movies in their minds,' focusing on creativity and scenarios, then what Sora did in the past was akin to a costly and difficult-to-use camera. The videos it generated had a cinematic quality but were not cost-effective, and their motion logic was relatively weak, making it challenging to achieve large-scale adoption in areas like web series, advertising, and e-commerce.

Another piece of evidence is that, according to previous disclosures, about 70% of Kling AI's current revenue comes from overseas user subscriptions and API services. What direct relationship does this have with Kuaishou's domestic commercial ecosystem advantages?

Moreover, even if Kuaishou's Kling has the advantage of embedding advertising, e-commerce, and short-video scenarios, ByteDance and Tencent (Weixin Channels) also possess even stronger and more potential ecosystems.

Therefore, Kling still does not possess unique scarcity, and this scarcity may further decline over time.

Perhaps for this reason, Kuaishou's Kling now needs to strive to realize its value ahead of time.

However, whether proactive or passive, the spin-off of Kling is a significant strategic move at present. So, rather than focusing on 'why,' it is more worthwhile to pay attention to 'what will happen next.'

There are several possibilities: The first scenario is a win-win situation post-spin-off.

Just as PayPal's independence led to a nearly 10-fold increase in its value within five years, driving eBay's stock price up as well.

But this requires the subsidiary to have a true technological edge and sustained revenue growth.

Currently, Kling faces a situation where it has an edge, but it's not profound enough. Compared to Happy Horse and Seedance 2.0, it does not have a decisive advantage.

Whether it can maintain sustained revenue growth and even convert it into profits remains uncertain.

The second possibility is a lose-lose situation, where the parent company becomes hollowed out, and the subsidiary lacks self-sufficiency.

A typical example is Zeekr in the automotive industry. After Zeekr's independence, its valuation was halved, and it was privatized and delisted after 19 months.

Similarly, after the spin-off, Kling and Kuaishou will have lower tolerance for errors.

The AI market expects growth and profitability from Kling, while Kuaishou's core business needs to find new growth opportunities...

So, if both parties underperform after the spin-off, even if Kling successfully goes public in the future, privatization is not out of the question.

In that case, the biggest gain from Kuaishou's spin-off of Kling might be in financing and obtaining capital gains.

The third scenario is that Kuaishou's core business growth gradually weakens, while Kling's AI business thrives.

This tests the growth potential of Kuaishou's core business.

However, from the current perspective, after Kling's spin-off and even a successful future IPO, Kuaishou may primarily gain financial benefits and cost improvements. The overall strategic synergies with its short-video, e-commerce, and other businesses do not seem significant.

This is quite different from the logic behind Baidu's spin-off of Kunlunxin and Alibaba's spin-off of T-Head.

Chips represent entirely incremental business and a proven market direction. At the same time, for companies like Alibaba, which are fully committed to an AI strategy, chips can also achieve highly synergistic growth.

But Kling is different. It has growth potential but also too much uncertainty.

Moreover, in the past, Kling was supported by Kuaishou's short-video ecosystem, but the spin-off means independent operations. When the relationship between computing power sharing and data interchange between the two changes, will it affect their respective competitiveness?

This is worth continuously tracking and observing.

Will Tencent and Others Jump on Board with Kling's 'Spin-off'?

According to articles from media outlets like Lan Jing News and 21st Century Business Herald, Kling's current target valuation is $20 billion, with plans to raise $2 billion in funding. It is currently in talks with potential investors such as Tencent.

Correspondingly, data from Tianyancha APP shows that as of the end of 2025, Kling's actual revenue was close to $150 million. By the end of April this year, its ARR had further surged to $500 million.

A valuation of $20 billion, based on 2025 actual revenue, implies a PS (Price-to-Sales) ratio of approximately 133x.

Based on an annualized revenue of $500 million, the PS ratio is approximately 40x.

This performance is not the most exaggerated among AI companies but is certainly not cheap.

Especially in the current market environment, even a financially strong company like Tencent may not be easily swayed.

Why do we say that?

1. What is Tencent's motivation for investing in Kling now? Or what kind of investment is this?

The most likely answer is that it is a strategic investment in the short term and a financial investment in the long term.

The former is easy to understand. Tencent's move may be similar to its early investments in JD.com, Pinduoduo, and Bilibili, primarily aimed at securing a position in the AI industry ecosystem, closing loops for its own business, and buying insurance for the group's AI strategy.

This also aligns with Ma Huateng's recent statement regarding whether Tencent's AI is lagging: 'A year ago, we thought we had boarded the ship, but later we found that the ship was leaking. Now we feel like we've stepped on board but can't sit comfortably yet. We still hope the ship can speed up.'

But the problem is, in the long run, Tencent has its own Weixin Channels ecosystem and long-video platform, a massive Weixin user base, and continuously strengthening AI capabilities. If Alibaba can create a stunning Happy Horse in a short time, why wouldn't Tencent make a similar move?

Even if Tencent doesn't want to build its own video model, the business demands of Weixin Channels and Tencent Video may not allow it to stay out.

After all, a video generation model is an AI lead that can connect and empower user flows. Essentially, its disruptive logic for long and short-video platforms is the same as that of self-driving technology for the mobility industry. Didi, Cao Cao Mobility, and others will inevitably pursue self-driving technology, and Weixin Channels is unlikely to accept handing over its critical lifeline to a third party...

Therefore, we boldly predict that Tencent's ecosystem will eventually have its own video model, and Kling is not the only solution.

For this reason, Kling AI is an investable opportunity now, but if its valuation premium is too high, things may become uncertain.

2. The long-term uncertainty of Kling's future, as mentioned earlier.

This actually corresponds to the risk-return ratio of Kling's long-term financial investment value.

Kling's revenue appears to be growing rapidly, but its investment costs are also high, and the competitive risks are significant. Kuaishou's Capex investment surging to approximately 26 billion yuan in 2026 is the most direct evidence.

So, to some extent, Kling is not an extremely high-quality investment target and does not align well with the pursuit of certainty in financial investments.

3. The rapid iteration of AI versions means that what is valuable is not the project itself but the people—the core team.

For example, Zhang Di, Kling's former technical lead, left in August 2025, briefly joined Bilibili, and then joined Alibaba in November.

Two months later, without Zhang Di, Kling was surpassed by Seedance 2.0.

Four months later, Zhang Di's first product at Alibaba, HappyHorse 1.0, returned to the top of the leaderboard.

This contrast illustrates one thing: AI investment is not just about investing in technology or products but also in talent and organizational teams.

So, after losing core talent, is Kling still worth investing in at a high premium? This is also a question worth considering.

Of course, it cannot be denied that many market rumors have yet to be further verified, so how will the story unfold?

We need to let the situation develop further.

But what is certain is that for Kuaishou's Kling, an independent spin-off may not be the most ideal path, but it is the most pragmatic one.

Whether in terms of capital reserves or valuation space, it can achieve a strategic leap forward.

Since Kuaishou has taken the first step, we might as well give it some more time and see if Kling can become a name thoroughly remembered in the AI era.

Finally, we wish Kuaishou and Kling all the best—may they find their own certain path in an uncertain future.

Disclaimer: The content of this article is derived from legally disclosed corporate information and publicly accessible data, and it presents the author's personal viewpoints. Nevertheless, the author makes no assurances regarding the comprehensiveness or up-to-dateness of such information. Moreover, the stock market is fraught with risks, so it's prudent to exercise caution when participating. This article is not intended as investment guidance; investors should independently evaluate and make investment decisions after thorough deliberation.

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!

-

![]()

AI Agent Smartphones: The Next Competitive Edge Transcends Large Models

-

![]()

Over 880 Million Yuan Worth of Orders Unveiled, Bidding Launched for Shenzhen Eastern Public Transport

-

![]()

Tesla's Robotaxi Hits the Road: A Monumental Gamble with an Uncertain Future