Kuaishou’s AI Video Division Kling Targets $20 Billion Valuation Amid Key Founder’s Move to Alibaba

05/18 2026

05/18 2026

600

600

By Guo Chuyu

Edited by Hou Yu

In May, an announcement sent ripples through Beijing’s tech sector.

Kuaishou revealed it is considering a spin-off and independent financing plan for its AI video large model business, Kling, with market speculation suggesting a valuation as high as $20 billion (around RMB 136 billion).

This figure nears two-thirds of Kuaishou’s current market capitalization. Yet financial data shows Kling contributed just RMB 1.04 billion in revenue to the group in 2025, less than 1% of total revenue, and remains in a phase requiring substantial ongoing computational investment.

Meanwhile, one name keeps resurfacing in industry discussions: Zhang Di, former Kuaishou Vice President of Technology and a core founder of the Kling project, who departed last year.

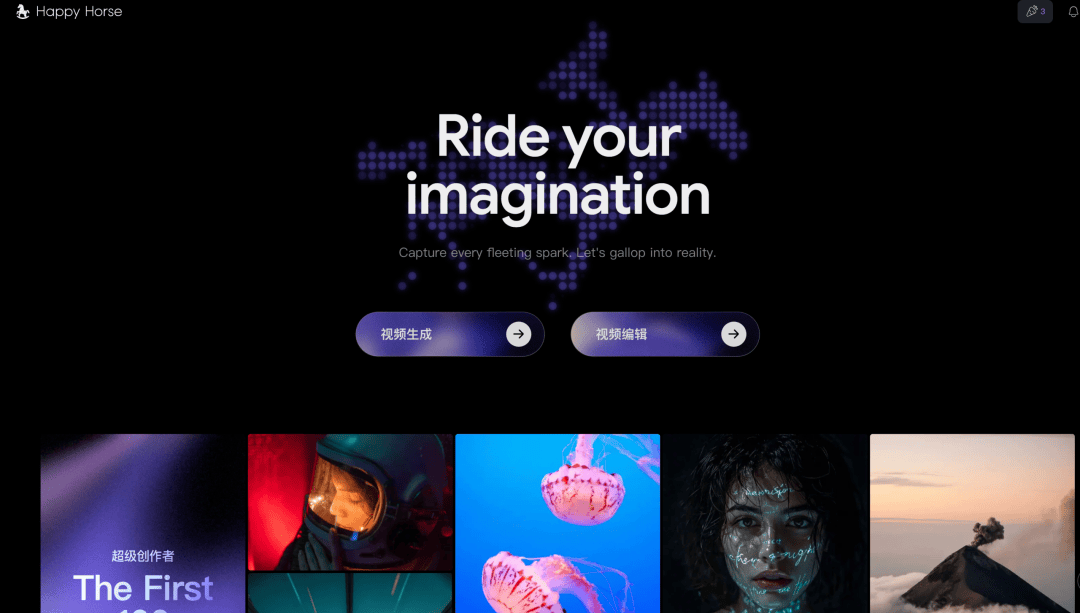

He now heads the Future Life Lab at Alibaba’s Taobao & Tmall Group. His team recently launched the AI video generation model “Happy Horse,” which has demonstrated competitive performance against Kling in multiple evaluations.

Ironically, as the business Zhang Di helped build approaches a $20 billion valuation milestone, he has joined a rival camp.

This scenario vividly reflects the current realities of AI industry competition and technical talent mobility.

Valuation Logic: Proven Business Model and Global Competitiveness

Kling’s high valuation is grounded in solid commercialization progress.

Since its launch in June 2024, it became the world’s first photorealistic video generation model available to the public, introducing membership fees just 48 days later.

In the computationally intensive and costly field of AI video generation, Kling’s strategy of prioritizing consumer (C)-end deployment is clear: rapidly complete market validation and secure stable paying users.

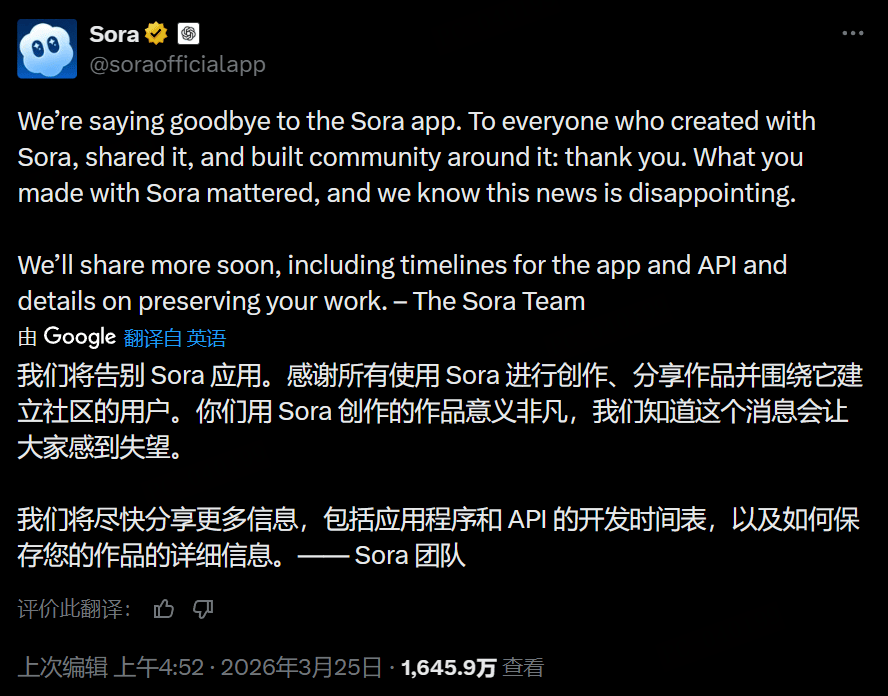

In contrast, many competitors persist with free models, ultimately trapped in cost dilemmas. OpenAI’s Sora, which shut down in March 2026, exemplifies this: its daily operational costs reached $15 million, while total consumer-side revenue accumulated to just approximately $1.4 million, creating a severe cost-revenue imbalance.

Kling has taken a different path—beyond C-end subscriptions, its business-to-business (B)-end operations are equally robust. By the end of 2025, Kling provided API services to over 30,000 enterprise clients and developers globally, covering 149 countries and regions. Prominent clients include Xiaomi, Baidu, BlueFocus, global creative platform Freepik, and AI model platform FAL.

BlueFocus CEO Pan Fei revealed that the company uses Kling AI to create 20,000-30,000 high-quality cinematic-grade videos monthly. Freepik’s CEO stated that among the 10+ video generation large models integrated, users choose Kling-generated videos more than all other models combined.

Kling’s most notable achievement lies in its successful globalization. In Q1 2026, approximately 70% of its $75 million revenue came from overseas markets like North America. SensorTower data shows Kling ranked first in art and design app downloads in over 40 countries and regions, topping graphic design app charts in South Korea, Turkey, Singapore, and even reaching No.1 in iPhone graphic and design app revenue in South Korea and Russia. Sora’s exit created space for Kling to meet overseas market demand.

A clear business model has driven sustained growth. Kling’s annual recurring revenue (ARR) surged from $100 million to $500 million in 13 months—an unprecedented commercialization speed in AI video generation. Meanwhile, Kling stands at the forefront of AI-driven content industry transformation: in micro-drama production, AI reduces costs to below one-third of traditional levels and shortens cycles by over 60%.

Spin-Off Funding: A Strategic Necessity

However, Kling’s rapid development contrasts with mounting pressures on Kuaishou Group. The computational demands of video generation large models are extremely costly. Kuaishou plans to invest RMB 26 billion in capital expenditures in 2026, while its 2025 adjusted net profit is projected at RMB 20.6 billion.

This means supporting Kling’s growth will directly erode the group’s overall profitability. Institutions like Citigroup, HSBC, and Huatai Securities have downgraded Kuaishou’s 2026 profit forecasts due to concerns over short-term profit impact from heavy AI investments.

A more fundamental challenge lies in Kuaishou’s core business. Financials show the platform’s 2025 average daily active users reached 410 million, growing just 2.76%. E-commerce growth slowed from 78% in 2021 to 15% in 2025, while Douyin’s e-commerce maintained nearly 30% growth. Notably, Kuaishou stopped disclosing GMV data separately in 2025, interpreted by markets as the end of its e-commerce hypergrowth era.

Against this backdrop, spinning off Kling became Kuaishou’s proactive strategic choice.

Retained within the group, Kling would remain an ancillary to online marketing services, with its massive computational costs burdening the parent company’s stagnant core business. Independent financing would allow Kling to leverage external capital to expand computational reserves and accelerate technological iteration, unshackled from group resource constraints.

A spin-off means removing hundreds of billions in annual computational investments from the group’s profit statements, shifting risks to capital markets. The true test lies in whether Kling can build independent self-sustaining capabilities and maintain leadership amid intensifying competition without Kuaishou’s full protection.

Competitive Siege and Loss of Key Figures

Kling’s independent path faces obstacles. By 2026, competition in AI video generation had turned fierce. In February, ByteDance released Seedance 2.0, praised by Game Science founder Feng Ji as “the strongest video generation model on Earth.”

In early April, Alibaba’s anonymous model HappyHorse-1.0 outperformed Kling 3.0 on third-party benchmarks—a model led by former Kuaishou Vice President Zhang Di.

Zhang Di’s background is highly representative. With bachelor’s and master’s degrees in computer science from Shanghai Jiao Tong University, he joined Alibaba in 2010 and served as engineering architecture lead for Alimama’s big data and machine learning. In 2020, he followed his mentor, former Alibaba P10 executive Gai Kun, to Kuaishou. By early 2023, he took full charge of large model and multimedia technology teams, becoming key to Kuaishou’s AI strategy. From 2024, he led Kling AI’s technical development from infrastructure to implementation.

According to people close to the team and public reports, Zhang Di was evaluated internally as a low-key, pragmatic, and efficient technical expert. His management style was highly results-oriented, focusing on problem-solving. During Kling’s early stages, facing industry shock from Sora’s release, he decisively chose a rapid reuse-plus-self-research optimization path at a critical February 2024 technical review, pushing the team to abandon hesitation and fully commit—a decision 1-2 months ahead of peers, securing Kling’s early-mover advantage.

A former colleague described Zhang Di as a leader who understood technology, could make decisions, and avoided bureaucracy—technical issues could be resolved directly with him without cumbersome processes.

Yet this technical leader, seen internally as a pragmatic builder capable of solving thorny problems, suddenly resigned in August 2025. After a brief transition, he joined Bilibili in September, then returned to Alibaba in November to lead Taobao & Tmall Group’s Future Life Lab.

Zhang Di’s departure was not isolated at Kuaishou—in December 2025, Vice President Zhou Guorui, in charge of foundational large models and recommendation systems, also left. Since Cheng Yixiao became chairman in 2023, over ten vice presidents have departed Kuaishou, significantly impacting its AI talent reserves.

Ironically, Kuaishou is known in the industry for strict talent retention and confidentiality measures. The company’s detailed Kuaishou Employee Information Security Guidelines rigorously regulate access, storage, and transmission of confidential information. According to insiders, core technical personnel face particularly tight controls—HR staff often accompany employees on business trips to prevent accidental leaks. Yet even under such stringent protections, key figures like Zhang Di chose to leave.

Talent outflow has directly impacted Kling. Zhang Di took not just his technical skills but deep understanding of Kling’s technical roadmap, computational scheduling, and product iteration rhythm. This directly helped competitors shorten technical replication time—just five months passed between Zhang Di joining Alibaba and HappyHorse-1.0’s release.

Why Can’t They Retain Talent? Organizational Inertia vs. Talent Demands

Zhang Di’s exit raises an industry-wide question: Why can’t tech giants retain core figures who built their benchmark innovative businesses?

An industry insider familiar with internet sector rules points to the crux: Companies offer top salaries to attract elite talent but constrain them with assembly-line hierarchical frameworks. The money is sufficient, but not the creative independence and decision-making authority needed.

This is not unique to Kuaishou. In March 2026, Alibaba also faced mass exits of core AI talent, including Qwen technical lead Lin Junyang, followed by several team leaders.

The root cause lies in the fundamental conflict between management logic and technical philosophy. Alibaba planned to modularize the Qwen team into pre-training and post-training units, pursuing standardized processes and strong production-research collaboration. However, Lin insisted that pre-training, post-training, and infrastructure must advance as an integrated system—two incompatible approaches leading to parting ways.

Even with industry-leading HR systems, Alibaba failed to retain top AI talent. This exposes a common dilemma: No management system, however rigorous, can reconcile the inherent conflicts between technical ideals and commercial rules, or individual creativity and organizational control.

The HR Business Partner (HRBP) system was designed to address such conflicts. Its intent was to align human resources with business frontlines, understand technical teams’ unique needs, and customize recruitment, incentives, and organizational structures—acting as translators between business and management, and architects of talent growth.

But reality has diverged. According to Kuaishou insiders, many HRBPs, while embedded in businesses, struggle to grasp AI research’s uncertainty and creativity. Their focus leans toward process compliance, team structure, and cost control, neglecting to identify and protect uniquely talented technologists.

This bias is pronounced at Kuaishou. Employees privately label some HRBPs as “process supervisors”: well-versed in rules, wielding approval power in hiring, promotions, and salary adjustments—often vetoing or delaying decisions—yet indifferent to frontline technical challenges and talent development needs.

Some insiders report that when issues arise, certain HRBPs prioritize identifying procedural flaws and assigning blame over collaborative problem-solving, stifling innovation. On workplace communities, Kuaishou employees complain that some HRBPs, detached from business realities, mechanically follow processes and prioritize risk avoidance over supporting innovation.

HRBPs, meant to provide support, have instead become control nodes requiring extra effort from technical teams, increasing innovation friction. While salaries and ranks can be standardized, this cannot constrain top talent’s aversion to inefficiency or their commitment to technical ideals. When management systems suppress creativity and exclude mavericks, departure becomes the loudest silent protest.

From Kuaishou losing Zhang Di to Alibaba releasing AI core talent, the essence is the same industry dilemma: Creative talent seeks freedom for technical breakthroughs, while large platforms pursue certainty in business operations—fundamentally incompatible logics making divergence inevitable.

The AI industry relies heavily on top talent, whose demands transcend salary and rank. They need autonomy, stable resource allocation, and an error-tolerant, innovative environment. When rigid organizational inertia and management models persistently misalign with top talent’s core needs, outflow becomes the norm.

Editor’s Postscript: The $20 Billion Valuation and Unanswered Questions

Kling’s $20 billion spin-off valuation reflects capital markets’ endorsement of its business model, global capabilities, and growth potential. Zhang Di’s departure and career shift reflect new norms in AI talent mobility.

These parallel events reveal two dimensions of current AI industry competition: Commercial success requires product, market, and capital synergy; sustained technical competitiveness depends on organizations’ ability to systematically attract and retain those defining the future.

The former can be achieved through capital operations, while the latter demands deeper organizational cultural, management, and incentive reforms.

Kling’s independent chapter begins—not just a single business’s fate, but an industry-wide quest for new balance among technology, capital, talent, and organization. As AI technology rapidly evolves, constructing systems that inspire innovation while achieving commercial success will remain a long-term challenge for all participants.

The spin-off of Kling marks a capital blitz won by Kuaishou. However, Zhang Di’s departure signals the beginning of a more protracted and fundamental talent war.

The former serves as a litmus test for technological prowess and financial acumen, whereas the latter puts organizational sagacity to the test. As the incremental dividends from China's internet sector reach their zenith, the internal competition to attract creators will become even more cutthroat than the external battle to acquire users. The story of Keling is on the brink of standing independently, yet the question of how Chinese tech companies can harmoniously coexist with top talent remains largely unanswered.

Perhaps, the linchpin to triumph in the upcoming clash will no longer hinge on a technical parameter showdown, but on which company can first crack the code of creator retention. Otherwise, today's $20 billion valuation extravaganza may merely serve as a down payment for an even more catastrophic talent exodus down the road.

-

![]()

Ford and Geely Forge New Joint Venture in Spain, Sidestepping Changan and JMC

-

![]()

199 RMB! Godox's First Camera Review: Subpar Photography, Transparent Viewfinder Frame is the Highlight

-

![]()

AI Smartphones: A Modern-Day 'Emperor's New Clothes'?

-

![]()

Yonyou Network: A Company Selling 'Transformation' but Struggling in Its Own Transition

-

![]()

Focus | CCCC’s Takeover of Greentown Comes to Fruition: Why Did the 11-Year ‘Control Without Authority’ Era End?

-

![]()

Final Verdict: The 2026 China Auto Forum Shines with Unique Characteristics at a Pivotal Moment

-

![]()

Tencent Maintains Matrix Approach, Alibaba Merges Entry Points: Tech Titans Initiate AI Agent Consolidation

-

![]()

Geely Secures Portion of Ford’s Spanish Production Capacity