The Boom of Short Drama Going Global: In the 3.6 Billion Market, Only a Few Are Truly Making Money

05/19 2026

05/19 2026

573

573

By Hengxin

Source: Bowang Finance

A few years ago, ReelShort, a Chinese short drama app, quietly surged to the top of the U.S. App Store’s entertainment chart.

Its screen looped with 60–90-second vertical dramas like “I’m Pregnant with the 50-Year-Old CEO’s Child” and “The Surrogate Bride Awakens for Revenge,” captivating North American homemakers and Latin American youth alike, who eagerly paid to unlock episodes.

This scene ignited capital markets’ imagination of “micro-short dramas going global.” After all, the last industry to make foreigners pay for Chinese internet content was online literature and mobile games.

In 2025, the story took a new turn: AIGC began permeating the entire micro-short drama supply chain—script-assisted generation, multilingual AI dubbing, AI-animated adaptations, virtual digital actor performances, and AI-generated ad materials—slashing localization and production costs for individual dramas while exponentially boosting content supply efficiency. The industry slogan evolved from “dubbed exports” to “AI-driven full-chain globalization.”

Yet beneath the glitz, data revealed a different picture: Leading platform ReelShort swung from profit to loss in 2025; DramaBox’s parent, Dianzhong Tech, admitted its short drama business net margin fell below 1%.

This raises the core question of this article: Is AI-powered short drama exports the next billion-dollar growth market for content globalization, or just another round of cash-burning games reliant on financing and user acquisition spending?

01

Explosive Overseas Growth, But Profitability Remains Highly Concentrated

The global micro-short drama export market has validated real demand and exponential growth through data.

According to the *2025 Overseas Short Drama Industry Report* released at the 13th China Internet Audio-Visual Conference, overseas short drama apps saw 1.199 billion downloads in 2025, up 268% year-on-year, with total revenue reaching $2.329 billion, a 133% increase. Active markets expanded from 37 to 46.

The *AI-Driven Global Micro-Short Drama Innovation Report* further showed that by 2025, the international market (excluding China) hit $3.6 billion, with Chinese firms contributing ~90%. The top 10 overseas short drama platforms by in-app purchase revenue all had Chinese backgrounds, accounting for $1.65 billion (~45.83% of the market).

By revenue, North America, Europe, and Japan/Korea were the top three markets for Chinese micro-short dramas. North America alone contributed 45% of overseas in-app purchase revenue, with U.S. users paying $8.27 per download.

By downloads, Southeast Asia, South Asia, and South America led, each capturing ~20% of the market. Southeast Asia topped with 403 million downloads (22% of the total), followed by South Asia (367 million, 20%) and South America (357 million, 19%).

The business model typically mixed monetization: 3–5 free episodes upfront, followed by pay-per-episode unlocks or incentive ad viewing (IAA) for access. By 2025, IAA short drama apps surged from 4.7% to 24.7% of downloads, tapping price-sensitive markets like Southeast Asia.

However, stark regional payment disparities and a winner-takes-all landscape left most mid-tier players unable to share in growth, creating a typical “prosperous market, scarce profits” dynamic.

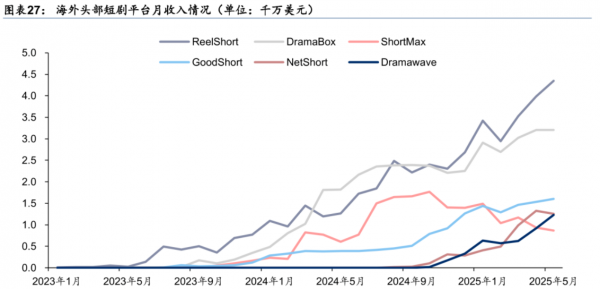

In 2025, 74 new short drama apps launched while 19 smaller ones exited, mostly low-cost dubbed drama platforms targeting Southeast Asia. DramaBox and ReelShort, both Chinese, dominated the top tier for two years, but among the 2025 mid-tier apps in the top 10, five saw declines in both downloads and revenue—all developed by Chinese teams.

This suggests the market is validated, but “inclusive gold rushes” do not exist.

02

AI Cuts Costs but Isn’t a Profit Panacea

AI is substantially reducing costs and boosting efficiency across key micro-short drama supply chain nodes, particularly multilingual AI dubbing, which slashed traditional localization costs by an order of magnitude, and AI-animated adaptations, which lowered content creation barriers.

However, it also accelerated content homogenization, leaving the “hit-driven power law” intact. AI merely increased trial frequency and ad targeting precision without eliminating the industry’s high failure rate in “spray-and-pray” hit strategies.

AIGC’s penetration in short drama exports manifests in five areas:

1. **Script-assisted generation**: LLMs rapidly produce multiple script outlines, episode summaries, and dialogues, ideal for batch-adapting online literature IPs.

2. **Multilingual AI dubbing**: Neural TTS delivers near-human emotional delivery in English, Spanish, Portuguese, and Indonesian, slashing translation costs and timelines.

3. **AI-animated/static comic adaptations**: Tools like Midjourney and ComfyUI generate coherent storyboards or convert live-action drama keyframes into anime style, paired with lip-sync tech for “AI-animated dramas.”

4. **Virtual digital actor performances**: Some platforms experiment with full-CGI “simulated human dramas,” offering long-term potential to bypass actor schedules and fees.

5. **AI-generated ad materials**: Automatic highlight clipping, multi-size vertical preview generation, and A/B testing drive high ROI for overseas ad campaigns.

This tech shift has three structural impacts:

1. **Barriers drop, supply explodes**: “Fast-in, fast-out” content floods the market.

2. **Local production costs pressure AI adoption**: Dubbing + AI dubbing became the primary cost-control method for smaller players, while top platforms trialed high-budget local productions to build content moats.

3. **New formats divert user time**: TikTok now hosts dozens of AI short drama accounts, with single-drama views topping 600 million. By Q1 2026, AI short drama revenue exceeded $2 million, signaling social media platforms could bypass standalone apps via “content + algorithmic distribution,” creating new cross-border competition.

Yet clarity is needed: AI cannot erase the “hit-driven power law”—a few top dramas generate most revenue, while most lose money.

AI reduces production/localization marginal costs, accelerates material iteration, and improves ad efficiency, lowering trial costs per unit. However, it does not fundamentally alter business logic and may worsen click dispersion due to oversupply.

Thus, AI is a critical efficiency lever and differentiation tool but not a profit guarantee. It lets top players build content libraries at lower costs (boosting LTV) while accelerating the demise of followers lacking content judgment who rely solely on buying users.

03

Chinese Platforms Lead in a “Triple Giant” Race, But Face Bleeding Growth and Second-Tier Predators

China’s micro-short drama exports now feature ReelShort (Crazy Maple Studio), DramaBox (Dianzhong Tech), and ShortMax (Jiuzhou Culture) as the top tier, forming a “duopoly + challenger” pattern (pattern). However, leading players generally face “revenue growth without profit” expansion phases.

ReelShort pioneered the overseas paid short drama model, backed by Crazy Maple Studio’s team experienced in Chinese online literature exports. Financially, it generated RMB 5.721 billion ($850 million) in 2025 revenue (+97% YoY) but swung to an RMB 85+ million loss, epitomizing “bleeding growth.”

Sensor Tower and Huatai Securities data show ReelShort earned $43.48 million in May 2025 with 11.48 million downloads. Monthly active users (MAUs) reached 25.57 million, ranking third.

Strategically, ReelShort was first to build a local U.S. production team for original English dramas, combining heavy ad spending with data-driven content selection, leveraging COL’s online literature IP library for scripts. Its risk lies in soaring Meta/Google ad costs in North America.

Dianzhong Tech, a domestic genuine (licensed) online literature and short drama operator, launched DramaBox globally in 2023. By 2024, revenue exceeded RMB 2 billion ($300 million) with 100+ million downloads across 200+ countries.

Content-wise, DramaBox still relies heavily on dubbed dramas, adapting proven domestic hits with AI-generated English/Spanish/Portuguese dubbing. According to *36Kr Outbound*, Dianzhong disclosed an overall ~10% gross margin, with short dramas contributing <1% net margin—highlighting profit erosion from high ad spending.

Jiuzhou Culture, an early private player in Chinese micro-short drama production, owns hits like *The Peerless*. Its ShortMax platform captured ~7.1% market share in January–May 2025, ranking fourth, and briefly topped the U.S. iOS Entertainment Free chart with ~5.5 million DAUs at peak.

ShortMax emphasizes “online literature IP exports + localized adaptations,” launching comic IP adaptations in Japan and Spanish-language local productions in Latin America. It seeks a middle ground between ReelShort’s high-cost originals and DramaBox’s mass dubbing, leveraging upstream production capabilities to support its global platform.

Meanwhile, Kunlun Wanwei’s DramaWave, COL’s FlareFlow/Sereal+, Zhangyue’s iDrama, and ByteDance’s Melolo are carving out niches with distinct strategies.

Undoubtedly, China’s short drama exports now feature a top tier of ReelShort and DramaBox duopoly with ShortMax in pursuit, plus second-tier layout (deployments) by Kunlun, COL, and ByteDance. The industry has entered a “capital-intensive + content-driven” deep water zone.

Leading players currently trade profits for scale, betting on localized hit libraries and LTV growth to cross the breakeven point—a severe test of investor patience and financial strength.

Conclusion

Labeling AI short drama exports as merely “the next online literature export” or “another bike-sharing cash burn” is overly simplistic.

For investors tracking this space, focus on: quarterly shifts in top platforms’ IAA revenue mix and customer acquisition cost inflection points; whether ROI for North American/European original hits turns positive; quantifiable AIGC-driven cost reductions in dubbing and animated adaptations; and user dilution effects on standalone apps from TikTok’s native short dramas.

Short-term valuations are prone to hype-driven volatility. True safety margins come from “who first achieves a sustainable unit economic model without continuous funding.”

Micro-short drama exports won’t be a trap—they represent the fastest-growing pillar of China’s “new three” cultural exports (online literature, gaming, short dramas). However, for individual companies, until they achieve positive unit economics, most players are merely fuel for this billion-dollar celebration.

-

![]()

Why Did Tesla’s Profits Drop and Cash Flow Go Negative?

-

![]()

AI Titans Are All in the Red: Time for Intelligent Driving Car Buyers to Reassess?

-

![]()

In the Next Decade of Joint Ventures, Honda Should Move Away from 'Stubbornness'

-

![]()

Operating Profit Plummets by 57%! What Caused Tesla’s Profitability to Decline in Q2?

-

![]()

Starting at 12,999 Yuan! Samsung’s Pioneering Wide Foldable Phone Unveiled: Sleek, Lightweight, and Ushering in a New Era for Android Foldables

-

![]()

Seven Bankruptcies Fail to Topple It! Aston Martin Raises £550 Million to Keep Afloat

-

![]()

Weichai's 'Triple Leap': From Diesel Engine Manufacturer to a 400 Billion Yuan Powerhouse

-

![]()

Tesla’s Financial Acumen Outshines Even Huawei’s