Is NVIDIA Slowing Down as Q2 Guidance Cuts Growth Rate in Half?

05/22 2026

05/22 2026

502

502

Editor | Zhang Lianyi

A 'money-printing machine' generating $80 billion per quarter suddenly slashed its growth rate from 20% to 11%—has NVIDIA's era of hypergrowth ended?

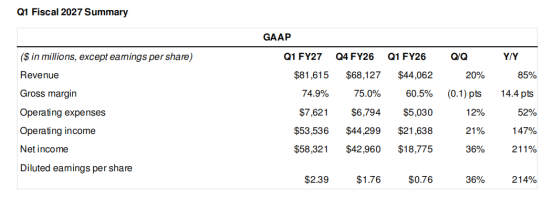

On May 21, NVIDIA delivered another stellar earnings report: Q1 FY2027 revenue hit $81.6 billion, surging 85% YoY and 20% QoQ; net profit reached $58.321 billion, up 211% YoY. The data center segment contributed $75.246 billion (92% of total), with gross margin stable at 74.9% and free cash flow hitting a record $49 billion. NVIDIA also announced a dividend hike from 1 cent to 25 cents per share quarterly and an $80 billion share buyback acceleration.

But this impressive report hid a critical contradiction: While demand remains parabolic, growth signals deceleration for the first time. NVIDIA's Q2 revenue guidance of $91 billion implies sequential growth crashing from 20% to ~11%—nearly halved. Is this a warning of peak AI computing demand or a necessary adjustment during NVIDIA's acceleration phase?

After earnings, NVIDIA shares initially plunged over 3% in after-hours trading before paring losses.

01 The 'Bright and Dark Lines' in Data: High Revenue Growth vs. Halved Sequential Growth

NVIDIA's Q1 core metrics met nearly all optimistic expectations.

First, total revenue reached $81.615 billion, up 85% YoY and 20% QoQ, marking 14 consecutive quarters of sequential growth.

Data center revenue hit $75.246 billion, up 92% YoY and 21% QoQ, accounting for 92% of total. The Blackwell architecture and GB300NVL72 became dominant, with hundreds of thousands deployed—the fastest ramp in history.

Second, NVIDIA maintained a 74.9% gross margin at scale, demonstrating pricing power and cost control.

Additionally, NVIDIA returned ~$20 billion to shareholders in a single quarter: $80 billion in new share buyback authorization and a dividend hike from $0.01 to $0.25 per share, signaling strong cash flow confidence.

More optimistically, computing rental prices continue to rise, especially for legacy models: H100 leasing prices surged 20% YoY, A100 cloud pricing jumped nearly 15%, and older cards remain profitable beyond depreciation, directly refuting 'overcapacity' and 'AI bubble' claims. Meanwhile, networking revenue (InfiniBand/SpectrumX) nearly tripled YoY, becoming the second growth engine outside data centers.

Beneath these bright numbers, the market's most sensitive signal emerged.

NVIDIA's Q2 FY2027 guidance: $91 billion revenue (±2%), with sequential growth slowing to 11% and gross margin holding around 75%.

1. Q2 total revenue sequential growth drops from 20% to 11%—nearly halved.

2. Hyperscale cloud revenue grows just 12% QoQ, significantly lower than ACIE's (AI Cloud/Industrial/Enterprise) 31%, indicating slowing purchases by top cloud providers.

3. Gross margin peaks at 75%, with limited upside, narrowing profit flexibility.

NVIDIA explicitly excludes China data center revenue, even as U.S. approved limited H200 exports—neither current nor projected revenues include this.

This marks NVIDIA's first clear growth deceleration after nearly doubling annually for two years. For a $1 trillion company valued on 'persistent acceleration,' 'growth continues but at a slower pace' is enough to trigger valuation re-rating. Post-earnings share volatility reflects market voting on whether the 'high-speed phase' has ended.

Undeniably, deceleration is inevitable after massive scale. The question isn't whether it will slow, but whether markets will accept 'slowing from now on.'

02 Hand-to-Hand: NVIDIA's 'Supplier Financing' Closed Loop

To understand the past two years' explosive growth, we must follow NVIDIA's money.

Ahead of earnings, NVIDIA filed its 13F holdings as of March 31, showing public holdings swelled to $18.3 billion, highly concentrated in 5 companies: Intel (51.6%), CoreWeave (20%), Coherent, Synopsys, and Nokia.

Compared to Q3 2025's 13F, NVIDIA's investment portfolio surged from $3.8 billion to $18.4 billion in Q1 2026, marking a sharp increase in external investments.

In Q3 2025, NVIDIA invested in small AI computing, autonomous driving, and biotech firms. By Q1 2026, it shifted to chip giants, semiconductor tools, communications, and laser/photonics leaders, notably doubling down on CoreWeave (AI computing cloud). From chip design to manufacturing to connectivity to computing output, NVIDIA holds a stake at every AI supply chain junction.

More notably, this supports a sophisticated 'hand-to-hand' closed loop.

Specifically, by investing $5 billion for a 4% stake in Intel, NVIDIA secures both financial returns and supply chain safety—Intel is the only U.S. foundry for advanced nodes.

After heavily investing in CoreWeave, NVIDIA became its shareholder (11% stake) and signed a $6.3 billion backstop agreement—if CoreWeave can't lease its computing power, NVIDIA buys it back. This makes NVIDIA a shareholder, customer, and final buyer.

Binding model companies like OpenAI—NVIDIA signed a $100 billion deal with OpenAI, stipulating the funds must deploy 100,000 H100 GPUs.

Jensen Huang bluntly stated: 'There are several top model companies. We invest in all. Whoever wins, they use our GPUs.'

This strategy is essentially supplier financing: NVIDIA uses its cash to 'accelerate' downstream demand, then recoups it through card sales. In a single quarter, NVIDIA deployed $18.6 billion externally (exceeding all of 2025), earning nearly $9 billion in paper profits from equity appreciation in a year.

03 Concerns: Will Slowing Growth Trigger a 'Cycle Break'?

This closed loop acts as an accelerator in good times but could amplify risks during deceleration.

Supporters argue it's a virtuous cycle: NVIDIA funds industry growth, enabling clients to buy more cards, which generates more cash for NVIDIA to reinvest. Rising rental prices, profitable legacy cards, and tripled networking revenue reflect genuine external demand, not artificial bubbles.

However, skeptics raise two sharp questions:

1. How much of the demand is 'self-supported'? The $6.3 billion backstop with CoreWeave inadvertently reveals that a truly supply-constrained market wouldn't need supplier buybacks. More such agreements suggest demand requires external support.

In September 2025, NVIDIA signed a $6.3 billion deal with CoreWeave.

2. Is the profit structure deteriorating? As investment gains ballooned from $1 billion to nearly $9 billion annually, NVIDIA is transforming from a chip company into an investment firm reliant on portfolio growth. If markets correct, these 'paper profits' could vanish rapidly.

History offers caution: During the dot-com bubble over 20 years ago, telecom equipment giants used 'supplier financing' to inflate results. When the bubble burst, they couldn't recover loaned funds and drowned themselves.

Returning to the opening question: Is Q2's sequential growth halving a temporary adjustment or the start of a sustained slowdown?

-END-

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle