Structural Transformation in Satellite Communications: Growth Driven by Technology, Geopolitics, and Commerce

05/22 2026

05/22 2026

519

519

Recently, renowned consulting firm Boston Consulting Group (BCG) released its report titled

What are the notable characteristics of satellite communications today?

BCG's report analyzes the drivers of change, future growth paths, and competitive landscape in satellite communications connectivity, revealing the most prominent trends in the global satellite communications sector.

First, examining the underlying drivers of satellite communications, BCG identifies three key forces driving structural change:

1. Technological advancements. Continuous progress in reusable rockets, mass satellite production capabilities, and inter-satellite links has significantly reduced the costs and communication latency of Low Earth Orbit (LEO) satellites. This has expanded the application scenarios for LEO constellations, enabling them to dominate and compete with terrestrial communications to a certain extent.

2. Geopolitical influences. The Russia-Ukraine conflict has accelerated the militarization of commercial space services, making them a critical component of modern hybrid warfare. In response, Europe launched the €11 billion IRIS² program, Canada supports the Lightspeed project, and Germany advances Satcom BW Stage 4, elevating sovereign communications capabilities to a national strategic necessity.

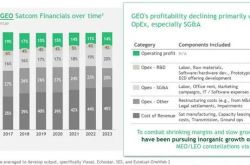

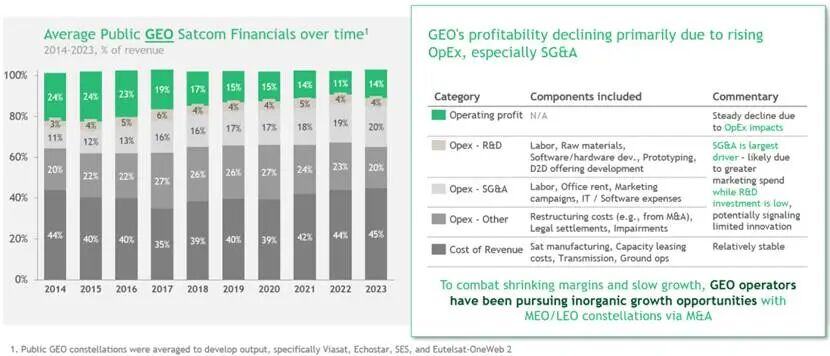

3. Increased competition. Vertically integrated LEO operators have reshaped cost structures, leading to declining profit margins for traditional Geostationary Orbit (GEO) operators, who now face stagnant revenue growth and consolidation risks. For example, SpaceX, through vertical integration, covers the entire satellite value chain—from development and launch to terminals and services—achieving costs and efficiency levels that far surpass traditional GEO operators. Between 2019 and 2024, total shareholder returns for GEO operators declined by approximately 20%, with most operating margins falling below 20%, marking an era of survival of the fittest in the industry. The chart below illustrates the sustained decline in GEO operating profits over the past few years.

Second, future incremental value in satellite communications will primarily come from three areas:

1. In-flight connectivity in the aviation industry. Global air passenger volumes have recovered and surpassed pre-pandemic levels, with annual growth exceeding 4%. Passenger demand for internet access, streaming, and video conferencing has risen, shifting in-flight connectivity needs from basic communication to streaming and business applications. In 2014, only 10% of aircraft worldwide were equipped with connectivity systems; this figure rose to about one-third by 2024 and is expected to exceed 50% within a decade, covering over 900 airlines.

2. Direct-to-Device (D2D) satellite services. This is currently a key focus area within the satellite internet sector. Only one-third of the global landmass has cellular network coverage, leaving approximately 2.7 billion people without mobile network access, driving demand for Non-Terrestrial Networks (NTN). Currently, D2D primarily serves emergency communications but will evolve toward broadband applications, allowing operators to cover remote areas at lower costs compared to traditional base stations and fiber optic infrastructure. However, the D2D business model is still in its early stages, with spectrum allocation and regulatory challenges remaining.

3. Sovereign constellations and partnerships. Defense and security needs are prompting governments to reduce reliance on foreign commercial assets, accelerating the development of autonomous and controllable communication networks, with governments becoming stable customers. Sovereign projects generally adopt dual-use (civil-military) designs, meeting both defense security needs and commercial revenue goals to alleviate financial burdens.

Third, the satellite communications sector will see a "one superpower, multiple strong players" competitive landscape.

SpaceX's Starlink, through full vertical integration, dominates global satellite communications capacity, achieving rapid user growth and revenue expansion while establishing sustainable barriers in consumer broadband and standardized in-flight connectivity. However, the satellite internet sector is still in its early stages, and a winner-takes-all market has yet to emerge.

Globally, Amazon's LEO satellite project (Amazon Leo) leverages AWS cloud and logistics ecosystems to focus on integrated "cloud + satellite" services. Blue Origin's Terawave initiative plans to build a constellation of over 5,000 satellites targeting enterprises, data centers, and government agencies. Canada's Telesat Lightspeed project, government-backed, focuses on secure private networks for government and enterprise users. Europe's Eutelsat-OneWeb emphasizes multi-orbit integration (GEO + LEO services), targeting the European market and maritime and aviation sectors. The European sovereign constellation program IRIS² will create a secure multi-orbit network for government, defense, and commercial users. These new entrants are competing differentially by addressing Starlink's weaknesses, such as sovereign concerns and enterprise demand for secondary options.

Domestic Satellite Communications Development Amid Global Opportunities

China's commercial space sector has evolved over the past decade and is now entering a critical phase of large-scale development. Satellite constellation plans, such as China Starnet's "GW" and GX Innovations' "Qianfan," aim to launch over 20,000 satellites to provide broadband services, accelerating the growth of satellite communications. Meanwhile, China has established a comprehensive industrial ecosystem covering rocket development, satellite manufacturing, launch services, ground equipment, and application services, with over 600 related enterprises.

However, constrained by multiple factors, the domestic satellite communications market remains in its early stages, with limited user scale and a need to accelerate LEO satellite network deployment. In the future, as the commercial space industrial chain matures and 3GPP NTN standards become the industry norm, the domestic satellite communications market potential will begin to unlock.

Currently, satellite IoT stands out as a relatively mature and initially scaling segment within satellite communications. Market research firm IDC projects the satellite IoT market to reach $3.219 billion by 2030, growing at a CAGR of 21.4%. As the world's largest IoT market, China boasts a rich IoT industrial ecosystem. Against the backdrop of policy incentives and rising market demand, satellite IoT is poised for rapid large-scale development.

Policy incentives continue to unfold. In 2025, the Ministry of Industry and Information Technology (MIIT) issued policies for commercial satellite IoT trials. Recently, MIIT approved State Grid Hi-Tech to conduct commercial satellite IoT trials, making it the first licensed private enterprise. Market-driven explorations have also yielded initial results. State Grid Hi-Tech will leverage its self-built and operated "Tianqi Constellation" to provide wide-coverage, low-power, and high-reliability IoT connectivity services for industry users, enabling all-weather, intelligent data collection and remote control in key sectors such as marine fisheries, energy and water conservation, and transportation logistics. Besides State Grid Hi-Tech, several other companies have deep experience in satellite IoT, with some achieving large-scale commercialization. For example, Geespace has completed a 64-satellite constellation, processing approximately 340 million daily communication requests and serving 20 million users globally across intelligent connected vehicles, marine fisheries, and construction machinery.

The 15th Five-Year Plan proposes the proactive construction of new infrastructure, including accelerating LEO satellite internet network deployment. Over the past few years, satellite communications have proven to be a commercially viable direction within the commercial space sector. Given China's vast territory, extensive ground communication coverage gaps exist in remote mountainous areas, offshore waters, and polar research regions. Simultaneously, emerging scenarios such as connected vehicles, in-flight communications, low-altitude economy, and emergency rescue present strong demand, providing rich opportunities for satellite communications development.

-

![]()

Token Package Launched: The 'Traffic War' in the AI Era Now Involves Doubao and Peers

-

![]()

Structural Transformation in Satellite Communications: Growth Driven by Technology, Geopolitics, and Commerce

-

![]()

China Telecom’s Monumental 17.4 Billion Yuan ‘Token Factory’ Deal Revealed! A New Stealthy Competition Among Telecom Operators in the AI Era

-

![]()

Nissan Faces 1.2 Trillion Yen Loss Over Two Years, Stakes Its Future on the Chinese Market

-

Token Is Not a Lucrative Business

-

![]()

The Retreat of European and American Brands Accelerates Chinese Automakers' Seizure of the Ultra-Luxury Market

-

![]()

Chip ETF Tumbles! ChinaAMC Rides the Wave of AI Profits

-

![]()

Stellantis Re-embraces 'Chinese Capabilities,' But the Approach Has Changed