Stellantis Re-embraces 'Chinese Capabilities,' But the Approach Has Changed

05/22 2026

05/22 2026

504

504

'Partnerships will be embedded in our future strategy.'

This statement by Antonio Filosa, CEO of the transnational giant Stellantis Group (Italy-France-US), was made on May 12 at the Financial Times 'Future of the Car Summit' in the UK. While primarily addressing how this complex company plans to undergo strategic transformation, it can also be seen as an early annotation of changes underway across the entire group.

Three days later, on May 15, Stellantis officially announced the signing of a strategic cooperation agreement with Dongfeng Group. Joint production of Jeep and Peugeot NEV models will commence at the Wuhan plant, with plans to export globally starting in 2027. The total investment exceeds RMB 8 billion, with Stellantis contributing approximately €130 million.

This is a rapidly unfolding story of joint ventures and cooperation, but its narrative scope extends far beyond this single agreement.

Entering May, Stellantis's partnership activities intensified to a dizzying pace: its cooperation with Leapmotor deepened from distribution to joint factory ownership in Europe, with consideration given to transferring ownership of the Madrid plant to the Leapmotor International joint venture. Meanwhile, market reports emerged that FAW Hongqi was exploring entry into the European market via the Zaragoza plant in Spain using Leapmotor's distribution channels.

On another front, rumors surrounding Maserati also garnered attention. Reports indicated that HiMode, JAC Motors, and Maserati had engaged in discussions about NEV model cooperation. Bloomberg, citing Li Ke (Stella Li), Executive Vice President of BYD, stated that BYD was discussing with Stellantis and other European automakers the possibility of taking over idle factories.

When these fragmented pieces of information are viewed collectively, it becomes clear that the changes underway at Stellantis involve far more than simply 'expanding cooperation.' This traditional automotive giant, boasting 14 brands, is attempting to transform its factories, distribution channels, brands, and manufacturing systems into an industrial platform open to external partners.

'Ending' the 'Shadow' of Carlos Tavares

To understand Filosa's current partnership strategy, one must first examine the state of the group left by his predecessor, Carlos Tavares.

At one point, Tavares transformed Stellantis into one of the most profitable automotive groups globally. In 2023, the group reported revenue of €189.5 billion and net profit of €18.6 billion, with profitability surpassed only by Toyota, Volkswagen, and Hyundai. However, his approach was a classic example of 'scaling to reduce costs'—utilizing shared platforms across 14 brands, standardizing parts, and compressing procurement and R&D to secure profits. While this tactic may have been effective during the traditional internal combustion engine vehicle era, cracks rapidly emerged amid the electrification and software-defined vehicle trends.

In the Chinese market, the 'asset-light' model previously pursued by Stellantis nearly ground to a halt. The Jeep brand, once selling over 10,000 units per month, has now virtually disappeared from the Chinese market. GAC Fiat Chrysler's bankruptcy in 2022 marked a symbolic turning point in Stellantis's retreat from China. Meanwhile, brands like Peugeot and Citroën continued to marginalize, while Chinese domestic NEV automakers rapidly advanced in intelligence, electric propulsion, and product definition.

Faced with these changes, Tavares's late-stage response was retrenchment: layoffs, production cuts, and plant closures. This led to increasingly fierce conflicts and tug-of-war with European unions and governments, ultimately culminating in his departure at the end of 2024. Stellantis recorded a net loss of approximately €22.3 billion in 2025, marking the worst performance in group history.

But in a sense, this previous retrenchment precisely laid the groundwork for today's 'openness.'

Substantial idle production capacity has become Filosa's most critical negotiating resource. The Cassino plant in Italy and the Rennes plant in France have both been discussed by European media as potential targets for takeover by partners. The Zaragoza plant in Spain currently produces the Peugeot 208 and Lancia Ypsilon, but rumors of cooperation involving the Leapmotor B10, Opel electric SUVs, and even a European version of the Hongqi model continue to swirl around this production line. The Madrid Villaverde plant has even been rumored to potentially be fully integrated into Leapmotor International's Spanish subsidiary.

These factories, once part of Stellantis's internal brand ecosystem, are now being redefined. This may not represent a fully proactive strategic choice, but in Filosa's hands, the 'passive assets' burdened by excess capacity are being reorganized into industrial infrastructure open to external partners.

How the Open Strategy Evolved from the 'Leapmotor Model'

The best entry point to understand Stellantis's open strategy is Leapmotor.

In 2023, Stellantis acquired approximately 20% of Leapmotor's equity for around €1.5 billion, becoming its largest external shareholder, and established 'Leapmotor International,' a joint venture in which Stellantis holds a 51% stake. This granted Stellantis exclusive sales and manufacturing rights for Leapmotor models outside Greater China. Initially, this resembled a typical channel cooperation. Stellantis hoped to leverage its extensive European sales and service network to rapidly introduce Leapmotor models like the T03 and C10 to overseas markets, while Leapmotor gained access to scarce European resources such as distribution channels, after-sales service, and localization capabilities.

However, the boundaries of cooperation soon expanded. On May 8, 2026, Stellantis announced further deepening of its partnership with Leapmotor: the Leapmotor B10 is scheduled to commence production in CKD (Completely Knocked Down) form at the Zaragoza plant in Spain in the fourth quarter of 2026, while an Opel electric SUV based on Leapmotor's architecture is planned for mass production in 2028.

If the initial Leapmotor cooperation remained at the level of 'selling Chinese cars in Europe,' today, this partnership has begun to penetrate deeply into the manufacturing system, platform architecture, and even the factory assets themselves. Filosa articulated this evolutionary logic bluntly at the conference mentioned earlier, stating that by jointly developing technology improvement, supply chain optimization, and capacity utilization roadmaps with partners, mutual benefits can be achieved. He explicitly viewed the Leapmotor model as a replicable reference, noting, 'There's still much that can be done in this area.'

In a sense, the true significance of the Leapmotor model lies not merely in Stellantis bringing a Chinese NEV automaker onboard but in how it redirected the trajectory of their cooperation. For decades, the logic of cooperation between traditional multinational automakers and Chinese companies largely followed a pattern of 'Europe exporting technology, China providing the market.' However, in the Leapmotor partnership, the direction of technology flow began to reverse. Future Opel electric vehicles will directly adopt Leapmotor's platform and supply chain rather than relying solely on Stellantis's internal systems. This marks the first systematic integration of Chinese NEV technology into Stellantis's core European brand products.

Changes are also occurring at the factory level. The Zaragoza plant in Spain, previously dedicated to producing Stellantis's in-house brand models, is now being redefined as a manufacturing node capable of accommodating multiple partners, brands, and platforms. To some extent, this approaches the logic of an 'OEM platform' in the electronics industry, where the factory itself ceases to be merely a brand appendage and evolves into a callable manufacturing service capability.

The 51%/49% equity arrangement in Leapmotor International further solidifies this binding relationship. Stellantis retains control over manufacturing and distribution, but Leapmotor is deeply integrated into its European expansion chain. This structure preserves traditional automakers' need for systemic control while leaving replicable space for additional partners.

If Leapmotor represents the template, the continuous stream of partnership rumors and new projects over the past two months suggests this template is beginning to radiate outward.

The new cooperation with Dongfeng Motor Group represents the first tangible step. According to officially announced information, Jeep NEV off-road models and Peugeot NEV models are scheduled to begin production in Wuhan in 2027, targeting both Chinese and global markets for export. This indicates that Stellantis is reintegrating Chinese factories into its global manufacturing system rather than merely using them as localized production bases for the Chinese market.

On May 19, Automotive News Europe, citing French media reports, stated that Dongfeng Motor might also produce vehicles at Stellantis's Rennes plant in France. If confirmed, this would mark the first large-scale localized production by a Chinese automaker in France.

Meanwhile, Reuters, citing multiple sources, reported that Hongqi, a brand under China's FAW Group, was engaging with Stellantis through Leapmotor's channels regarding the use of the Zaragoza plant. If realized, this would not only signify Hongqi's first manufacturing base in Western Europe but also demonstrate that Stellantis's European factories are truly opening their manufacturing capabilities to Chinese brands.

Another more closely watched—and uncertain—thread involves Maserati. Market rumors suggest that Huawei's HiMode, JAC Motors, and Maserati are discussing NEV model cooperation: Huawei would provide intelligence and product definition, JAC would handle R&D and manufacturing, and Maserati would contribute design and brand resources. While no official confirmation has been obtained as of now, this rumor remains intriguing. On one hand, Maserati has faced sustained sales pressure in recent years and needs to explore new product and technology pathways. On the other hand, Huawei requires premium brand resources with international recognition to support its next-stage globalization narrative.

Even direct competitors like BYD are being drawn into this ecosystem. Bloomberg, citing Li Ke (Stella Li), reported that BYD was engaging with multiple European automakers, including Stellantis, regarding the takeover of European factories. Although still in early stages, the symbolic significance is clear: Stellantis is gradually transforming from a traditional automaker into an industrial platform capable of opening its factories, distribution channels, and manufacturing systems to external partners.

These ongoing or potentially advancing cooperation formats are being reconnected under Stellantis's perspective into a single logic.

An Inevitable Choice Under Pressure

Stellantis's current open transformation does not represent a proactively designed strategy but rather appears to be a forced search for new survival and transformation pathways amid multiple pressures.

The most immediate pressure stems from Europe's manufacturing system itself. The aggressive expansion under Tavares's tenure left Stellantis with a batch of underutilized European factories. As electrification progresses, demand for traditional internal combustion engine vehicles declines, but the pace of Europe's shift to pure electric vehicles consistently falls short of industry expectations. This has created an awkward situation: existing internal combustion engine production capacity cannot rapidly exit, while new electric vehicle demand remains insufficient to fully utilize factories.

This is not a problem unique to Stellantis. European automakers like Volkswagen and BMW face similar dilemmas, but Stellantis's pressure is more concentrated. According to estimates by firms like AlixPartners, the average capacity utilization rate of European automotive factories has dropped to approximately 55%, with some Stellantis plants performing even worse.

This means fixed costs from factories are continuously eroding profits. For Stellantis, opening up production capacity to external partners has become the most practical option: whether providing manufacturing services to Leapmotor, opening production lines to potential partner brands, or directly incorporating some factory assets into joint ventures, these approaches are far more meaningful than allowing production lines to remain idle long-term.

Another pressure arises from the rapid advancement of China's NEV industrial chain. Over the past few years, Chinese industry players have made significant progress in key areas such as batteries, electric propulsion, intelligent cockpits, and advanced driver-assistance systems (ADAS), establishing clear cost and iteration advantages. For Stellantis, continuing to rely on traditional internal development systems would make its electric vehicle products difficult to compete with Chinese NEV brands in terms of both development cycles and cost structures.

Take Opel's future new electric SUV as an example: by adopting Leapmotor's platform, product definition to mass production is expected to take no more than two years. In contrast, traditional European automakers typically require five to seven years to develop a completely new electric vehicle. This is why Stellantis is increasingly eager to integrate Chinese technology into its European brand lineup.

Meanwhile, the EU's anti-subsidy investigation into Chinese electric vehicles has, to some extent, reinforced this cooperation trend. Although related disputes have gradually shifted toward price commitment negotiations, the process has made more Chinese automakers realize that localized manufacturing is nearly inevitable if they wish to continue expanding in Europe. This complements Stellantis's needs: Chinese automakers require European manufacturing capabilities, while Stellantis needs new orders to fill idle capacity. Hence, bilateral cooperation has rapidly intensified in a short period.

However, historical lessons remain relevant. Before celebrating Filosa's open strategy, it is worth revisiting a chapter of history. The bankruptcy of GAC Fiat Chrysler has already proven that brand licensing and factory cooperation do not automatically guarantee commercial success. Jeep's issues in China were never merely manufacturing system problems but also involved product definition, brand perception, and market timing. If brands fail to reinvent themselves for the new energy era, even a reentry into the market leveraging Dongfeng's technology and production capacity may not truly unlock the situation.

Meanwhile, the 'open industrial system' itself also implies extremely high management complexity. When a single factory needs to simultaneously accommodate multiple partners, multiple brands, and even different technology platforms, production scheduling, quality systems, intellectual property protection, and union coordination will become far more complex than in traditional models. Stellantis is currently advancing multiple cooperation lines simultaneously in Europe and China, with many projects still in the negotiation phase. For Fulosha, the real challenge is no longer just 'securing cooperation' but how to make these collaborations ultimately form an industrial system capable of long-term operation. Therefore, whether a sufficiently clear strategic framework can be provided will be the first critical test of Fulosha's execution capability as viewed by the outside world.

Of course, examining Stellantis's cooperation model within the industry context also highlights its greatest difference from other European automakers. Volkswagen has taken a 'technology procurement' approach by acquiring stakes in XPeng and jointly developing models with SAIC, but its German factories have not yet been opened to Chinese partners. Similarly, Audi's platform development with SAIC is currently limited to the Chinese market.

However, Stellantis's openness exhibits more pronounced bidirectionality. Chinese technology and brands are entering Stellantis's European factories and distribution networks; at the same time, Stellantis's own factories, sales networks, and even partial factory ownership rights have begun to form part of the cooperation negotiations. This transformation is gradually shifting Stellantis from a traditional vehicle manufacturer to a role closer to that of an 'industrial platform operator.' Of course, this openness also reflects Stellantis's relatively urgent financial pressures compared to its competitors. Its willingness to discuss factory ownership transfers inherently means that Stellantis must reevaluate the 'heavy asset-heavy control' logic of the traditional automotive industrial era.

Breaking the 'Platformization' Deadlock for Traditional Giants

In a sense, what the outside world truly focuses on next is not just whether Stellantis can continue to expand its cooperation but whether these collaborations can gradually form a stable, replicable, and long-term operational industrial framework.

On May 21, 2026, Fulosha held an Investor Day event at Stellantis's North American headquarters and unveiled the group's future business plans. However, the market is actually waiting for several more core questions: How will Stellantis define its future role? Is it still a traditional automaker, or is it transforming into an 'industrial platform operator'? What functions will factories in Wuhan, Zaragoza, Madrid, and elsewhere assume within this system in the future?

At the same time, questions such as whether Maserati will further enter the open cooperation framework, whether Leapmotor International will have more independent capitalization possibilities in the future, and whether these collaborations can ultimately improve Stellantis's profitability in the coming years remain unresolved. After all, what the capital market ultimately needs to see is never just 'openness' itself but whether this openness can truly translate into efficiency, sales volume, and profits.

An automotive giant that once prided itself as a 'multi-brand empire' is now opening its factories, brands, and distribution networks to China's new energy vehicle supply chain to improve capacity utilization and accelerate electrification transformation. This transformation itself is the result of a mix of passivity and proactivity.

Without the pressure of idle capacity or the rapid rise of China's new energy vehicle supply chain, such deep openness would not exist today. On the other hand, Fulosha and Stellantis have at least begun attempting to reorganize these issues, originally belonging to crisis management, into a new form of industrial collaboration. Whether this experiment ultimately succeeds may not only relate to Stellantis's own fate but also serve as a microcosm of how the entire European traditional automotive industry seeks a path forward in the new energy era.

Image: Sourced from the Internet

Article: Auto Review

Layout: Auto Review

-

![]()

Token Package Launched: The 'Traffic War' in the AI Era Now Involves Doubao and Peers

-

![]()

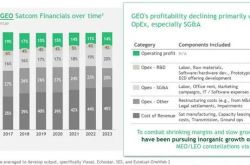

Structural Transformation in Satellite Communications: Growth Driven by Technology, Geopolitics, and Commerce

-

![]()

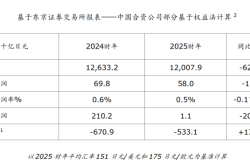

China Telecom’s Monumental 17.4 Billion Yuan ‘Token Factory’ Deal Revealed! A New Stealthy Competition Among Telecom Operators in the AI Era

-

![]()

Nissan Faces 1.2 Trillion Yen Loss Over Two Years, Stakes Its Future on the Chinese Market

-

Token Is Not a Lucrative Business

-

![]()

The Retreat of European and American Brands Accelerates Chinese Automakers' Seizure of the Ultra-Luxury Market

-

![]()

Chip ETF Tumbles! ChinaAMC Rides the Wave of AI Profits

-

![]()

Stellantis Re-embraces 'Chinese Capabilities,' But the Approach Has Changed