Why Are Users Dissatisfied with MiniMax's 'Covert Price Hike?'

06/12 2026

06/12 2026

507

507

Author|Amy

Editor|Su Man

Overnight, MiniMax started charging by tokens.

On June 1, alongside the release of its new flagship M3 model, MiniMax quietly shifted its billing model from "per-use" to "per-token consumption."

Image Source: MiniMax Official Website

Without SMS alerts or in-app notifications, many individual developers discovered the rules had completely changed when they logged in as usual. This "act first, explain later" approach sparked widespread controversy on social media and among developers.

For developers who had integrated MiniMax into their daily workflows, the change in billing logic directly impacted their cost structures and tool choices. Some users publicly sought redress on platforms like Heimao Complaints, requesting refunds, while others explicitly stated they would not renew their subscriptions.

The timing of MiniMax's billing model shift was rather delicate. Currently, the entire industry is exploring how to price coding plans without incurring losses. MiniMax took the opportunity of the M3 release to redefine its billing system but faced far greater public backlash than expected.

01 Why Did a Billing Switch Trigger Significant User Dissatisfaction?

MiniMax's paid system for individual developers has undergone two key transformations.

Initially, the product was called the "Coding Plan," a fixed monthly subscription service for programming scenarios using a "per-use deduction" logic. Users had a fixed number of calls within each 5-hour window, after which they could wait for a refresh.

The model's biggest selling point was the absence of weekly limits. Among domestic AI programming service markets, MiniMax was one of the few platforms adopting this design.

At the same time, aggressive pricing was another key reason MiniMax won developer favor.

While many mainstream providers generally set monthly fees between 40 and 50 RMB for programming subscriptions, MiniMax opted for a significantly lower price band: Starter at 29 RMB (9.9 RMB for the first month), Plus at 49 RMB, Max at 199 RMB, and Ultra at 899 RMB.

This "low price for scale" strategy attracted a large number of individual developer users and directly drove rapid revenue growth for the platform. MiniMax noted in its 2025 annual report that token consumption under the Coding Plan had surged, becoming a key driver of open platform revenue growth.

However, MiniMax clearly wanted to further upgrade this model. The turning point came in March 2026, when the "Coding Plan" was upgraded to the "Token Plan." The name change already hinted at MiniMax's intentions.

Notably, this renaming initially did not alter the core billing logic. Users could still subscribe and use the service as before, but the scope expanded from a single programming model to a multimodal unified system encompassing video, images, voice, music, and more. Officially dubbed the "world's first all-modal unified subscription plan," it marked a significant evolution.

However, users didn’t have long to celebrate. Just three months later, on June 1, the "Token Plan" was infused with its "soul"—with the release of the new M3 model, the plan began charging based on token consumption, sparking controversy.

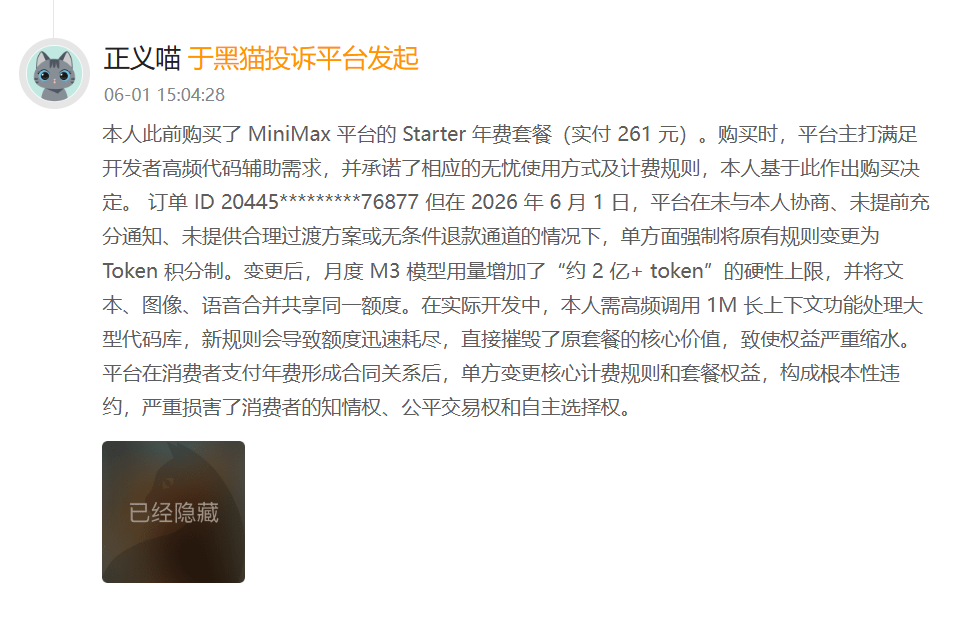

After adopting the new billing method, users quickly encountered a practical issue: under equivalent usage intensity, quota depletion rates far exceeded expectations.

Image Source: Heimao Complaints Platform

A heavy user who publicly sought redress on Heimao Complaints stated that their development work required frequent calls to the 1M long-context feature for handling large codebases. For tasks of similar scale, the quota now depleted at an alarming rate. Another Plus-tier user reported on social media that whereas they could previously make around 1,500 calls within a 5-hour window, the revised plan only supported 300 to 500 calls in practice.

Even more troubling for heavy users was that while the Token Plan retained the 5-hour window, it introduced a weekly quota limit. This meant that quotas previously sufficient for a week could now be exhausted in two to three days, leaving users waiting for quota restoration for the remainder of the week.

This stark disparity drove users to flood official platforms and complaint channels like Heimao, demanding refunds and compensation.

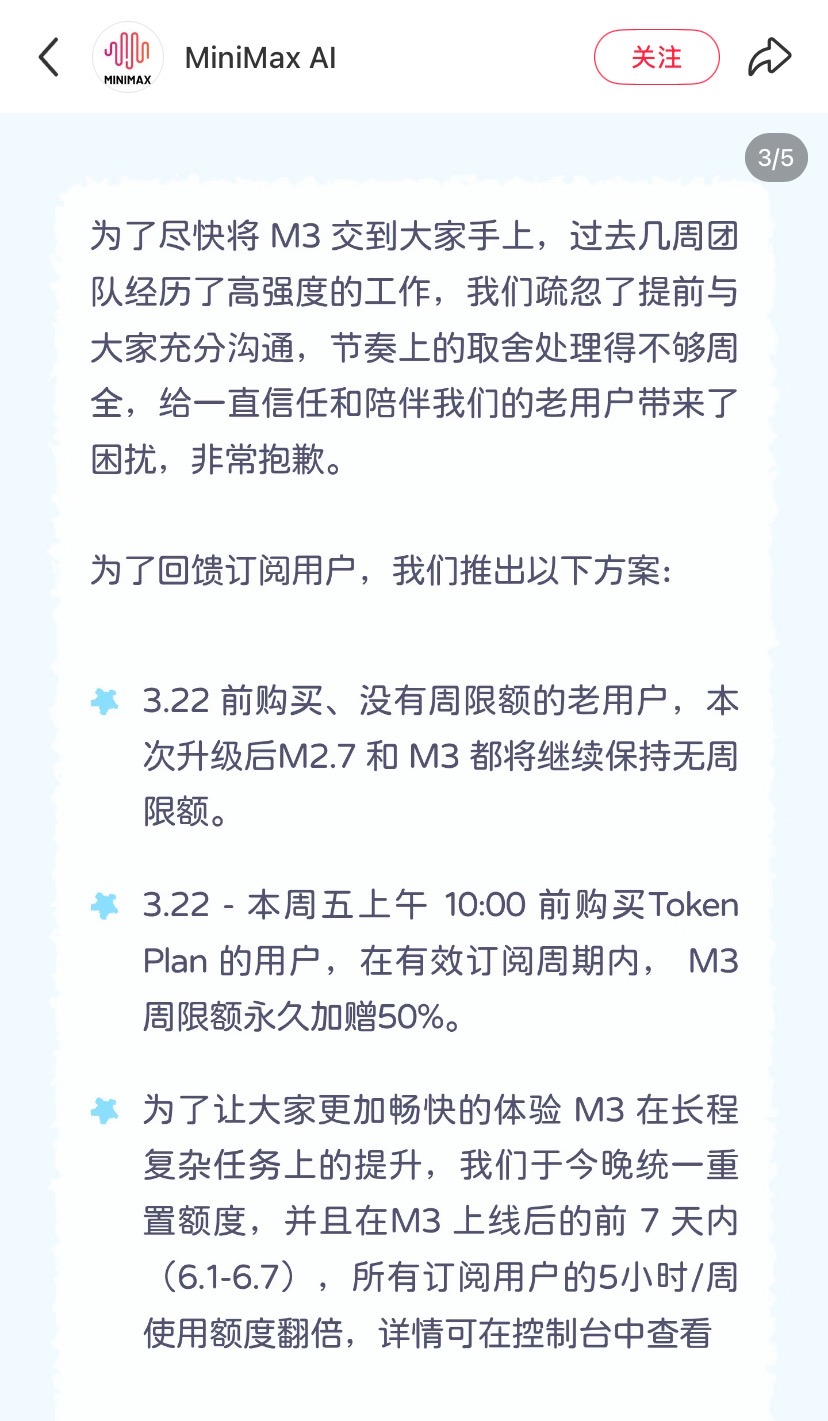

In response to the concentrated user backlash, MiniMax's parent company, Xiyu Technology, issued an apology announcement on the evening of June 1, admitting that "this adjustment failed to adequately communicate with users in advance and did not clearly explain billing and package changes, reflecting shortcomings in the company's approach." It also acknowledged mishandling issues such as weekly limits for existing users.

MiniMax attempted to pacify users with compensation plans, which can be summarized into two categories. The first category targeted existing users: those subscribed before March 22, 2026, could make unlimited calls to M2.7 and M3 models each week after upgrading; users who purchased the Token Plan between March 22 and June 5 (before 10 a.m.) received a permanent 50% increase in their weekly M3 model quota.

Image Source: MiniMax's Xiaohongshu Account

The second category applied to all subscribers: during the first seven days after M3's launch, the usage quota within the 5-hour window was temporarily doubled.

Market reactions to these remedial measures were mixed. Some existing users felt that retaining unlimited weekly calls preserved core benefits that initially attracted them to MiniMax. Combined with newly granted M3 access rights and multimodal quotas, the overall package remained acceptable.

However, dissatisfaction persisted, primarily centered on the rapid token depletion rate of the M3 model. Under the same weekly quota, the actual number of tasks that could be completed decreased significantly.

Negative sentiment was even more widespread among new users. Unable to benefit from "unlimited weekly quotas," they had no choice but to accept the new Token Plan system. Many expressed on social media that they felt "discriminated against" compared to existing users.

User trust may be quietly eroding. In the AI programming service market, MiniMax serves as a "viable alternative" but has not yet established irreplaceability.

JPMorgan recently noted in a report that positive data for M3 has not fully alleviated market concerns about its sustained pricing power. The bank believes the next critical test lies in retention: if OpenRouter maintains strong usage after its 50% discount ends and M3 continues to gain traction in coding tools, MiniMax's premium model strategy will become more convincing, strengthening its narrative around Annual Recurring Revenue (ARR) quality.

Conversely, if token usage declines significantly after discounts end or feedback on coding tools remains mixed, the market may continue to question whether M3's quality advantages justify premium pricing against competitors like DeepSeek.

02 High Costs Put Pressure on MiniMax

Sudden shifts in commercial behavior often trace back to cost structures.

As an AI company centered on consumer-facing products, MiniMax's cost structure during its scaling phase is notably heavy.

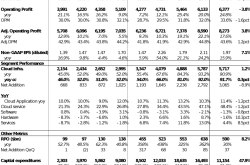

In 2025, R&D expenditures accounted for 319.8% of total revenue. In 2024, this figure reached 619.1%. These costs primarily stem from cloud computing resources consumed during model training.

Beyond R&D computing investments, product iteration, global market expansion, and user growth operations also require sustained capital injections.

An undeniable industry reality is that the stronger an AI model's capabilities, the longer its context window, the more complex its tool-calling chains, and the higher its inference consumption—every user call generates real computing costs.

MiniMax's technical prowess is widely recognized. OpenRouter data shows that in mid-March 2026, MiniMax M2.5's weekly call volume reached 1.75 trillion tokens, ranking first globally for five consecutive weeks; in April's programming scenario rankings, M2.7 topped the list again with 124 billion tokens; after M3's release, daily token consumption quickly surpassed 500 billion.

Image Source: MiniMax Official Website

Throughout 2025, MiniMax achieved total revenue of $79.038 million, up 158.9% year-on-year, with international markets contributing over 70%.

However, rapid revenue growth has not effectively translated into profit improvement. In 2025, MiniMax reported an adjusted net loss of approximately $251 million (around 1.73 billion RMB), roughly flat year-on-year; overall gross margin stood at 25.4%, with B-end business margin around 70% and C-end business margin just 4.7%.

MiniMax remains in the early commercialization stage where "revenue expansion outpaces profit recovery."

As of the end of 2025, MiniMax held $1.05 billion in cash reserves, up 19.3% from the end of 2024—sufficient for now, but management clearly aims to shift focus from subsidy-driven growth to optimizing unit economics.

From an industry perspective, token-based billing has long been standard practice for global AI large models. OpenAI and Anthropic both adopt this model, with domestic players gradually following suit. It ensures that every revenue dollar corresponds to a defined cost, serving as a key to improving unit economics.

Strategically, MiniMax is on the right path. However, its controversy stems from execution pace and timing.

Operationally, MiniMax failed to provide users with sufficient transition buffers. Many users faced the new cost structure entirely unprepared.

Timewise, this adjustment coincided with multiple unfavorable factors: DeepSeek released V4 in late April and announced a permanent 75% price cut; Xiaomi's MiMo-V2.5 also implemented price reductions; while competitors like Zhipu and Kimi loomed large.

Triggering a user trust crisis at this sensitive juncture may actively push undecided users toward competitors.

Currently, the AI industry's competitive logic is shifting: from a growth phase focused on user scale to an operational phase emphasizing commercial sustainability. Price adjustments directly reflect this transition, testing not just pricing power but also user communication and trust maintenance capabilities.

While MiniMax may excel technically, it still has significant lessons to learn on its path to becoming a mature platform company.

03 Rapid A-Share Return Within 5 Months: MiniMax Needs More Capital

On May 29, 2026, MiniMax signed a STAR Market IPO Tutoring Agreement (listing Tutoring Agreement , listing tutoring generally refers to pre-IPO coaching) with CITIC Securities. This occurred just 141 days after its Hong Kong Stock Exchange main board listing—less than five months.

Such "immediate A-share return" speed is rare in Hong Kong stock history. In contrast, its direct competitor Zhipu initiated A-share coaching nine months before its Hong Kong listing.

This timing difference sends a clear signal: post-Hong Kong listing experiences convinced MiniMax management that a single Hong Kong platform may not sufficiently support long-term capital needs.

MiniMax's post-listing stock performance in Hong Kong has been dramatic. After debuting on January 8, 2026, its share price tripled within three months. On March 18, it briefly hit HK$1,330, nearing a HK$390 billion market cap.

However, the stock entered a sustained correction phase after March due to multiple pressures: DeepSeek V4's release raised competitive concerns; Zhipu's market cap surpassed and widened its lead; and market enthusiasm for high-valuation AI stocks cooled.

MiniMax's May 29 STAR Market coaching announcement and June 1 M3 release failed to reverse the trend. By June 10's close, shares traded at HK$451.8, down over 65% from the year's peak, erasing about HK$240 billion in market value.

As Hong Kong valuations undergo "disillusionment" and discounts may deepen, the STAR Market's "hard tech premium" offers more appealing valuation support for MiniMax.

Image Source: MiniMax's Official Weibo Account

Greater pressure comes from July's lock-up expiration window. HSBC Holdings Plc estimates that currently, only about 5% of MiniMax's total share capital is freely tradable, with approximately 65% of total shares entering the market in July.

When lock-up shares flood the market, if liquidity cannot support high valuations and fundamentals are weak, share prices often face sharp corrections. This would harm early investors' interests and weaken the company's future financing capabilities.

Initiating a STAR Market IPO prepares a "backup plan" for the capital chain in advance.

MiniMax has not yet announced specific fundraising amounts for its STAR Market IPO, but Zhipu's plan offers a reference: seeking to raise 15 billion RMB, with 12 billion for an AI general-purpose large model project, 2 billion for a MaaS one-stop service platform, and 1 billion for working capital.

Moreover, a question worth pondering is whether the June 1 Token Plan billing shift also serves as preparation for the STAR Market IPO.

By charging based on actual usage, the Token Plan theoretically aligns each revenue dollar with quantifiable costs, helping improve gross margins. If the STAR Market IPO lands in 2027, MiniMax can then demonstrate sustained profitability improvements to A-share investors.

In the AI industry, where "better models cost more," MiniMax stands at a critical crossroads between "burning cash" and "generating cash."

The STAR Market IPO could buy it more time, but whether time translates into irreplaceable technological barriers and mature commercialization capabilities will determine if it evolves from one of the "Six Little Tigers" into a true platform-level company in the AI era.

-

![]()

Apple Shareholders Paid $230 Billion in 'Make-Up Exam Fees' for Apple's AI

-

![]()

Oracle Plummets? The Irreparable Flaws Beyond AI Infrastructure - 'High Interest, High Debt + Stagnant Software'

-

![]()

Oracle Plummets? The Irreparable Damage That AI Infrastructure Can't Fix—'High Interest, High Debt + Failing Software'

-

![]()

The Largest IPO in History Is on the Horizon: Why SpaceX Justifies a $1.75 Trillion Valuation

-

![]()

Cook's Gourd Holds No Magic Cure for Apple's AI Woes

-

![]()

Uber Exhausts Annual AI Budget in Just Four Months: Why Can't Even Uber Sustain AI Token Costs?

-

Unitree Goes Public, Ushering in an Era of Capital Frenzy for Robots?

-

![]()

In-Depth Exploration of the Physical AI Industry Ecosystem