Unitree Goes Public, Ushering in an Era of Capital Frenzy for Robots?

06/12 2026

06/12 2026

558

558

After showing off its skills on the Spring Festival Gala stage, Unitree Technology needs more money.

In early June, Unitree Technology smoothly passed its IPO review on the STAR Market. Frankly speaking, this company established less than a decade ago has used quadruped robots to open the door to the global market and humanoid robots to ignite capital enthusiasm.

Unitree Technology sends a clear signal to the outside world: Whether it's upstream suppliers of joint motors and reducers or end-users of terminal products, the business model for robots, especially humanoid robots, is gradually taking shape and entering a stage of scale-up.

In simpler terms, the capital market recognizes the long-term value of this direction, even though embodied intelligence is still in the 0-to-1 stage for C-end scenarios.

From a small team with an initial registered capital of 100,000 yuan to a current valuation of 42 billion yuan, Unitree Technology's growth history resembles a tale of mutual achievement between capital and technology.

Objectively speaking, the embodied intelligence industry may seem glamorous, but behind capital optimism still lies a ruthless survival rule: Without continuous capital infusion, even the most advanced technology can only remain in the laboratory. If players in the field cannot ultimately deliver sales volumes, even the highest valuations will eventually evaporate.

Perhaps Unitree Technology's listing will truly mark the beginning of an era of capital frenzy for the entire robotics industry. This raises another soul-searching question: With hundreds of players in the embodied intelligence industry, if not giants, how should those manufacturers still surviving on meager shipment volumes proceed with their next move?

| Walking on Two Legs: Capital and Technology |

Telling stories, defining products, announcing cool technological patents, gradually moving toward the market, and then ringing the bell on the securities market—this has almost become a common pattern followed by emerging tech companies in recent years.

Even for Unitree Technology, its successful listing, while seemingly a technological victory on the surface, is actually a product of the perfect combination of capital and technology.

We can try to understand a logic: In the money-burning race of embodied intelligence, no single enterprise can achieve the leap from technological breakthrough to mass production solely through its own accumulation. Looking back at history, Unitree is no exception. Every product iteration and market expansion it has undertaken has been driven by capital.

According to publicly available financing data, since its establishment in 2016, Unitree Technology has completed 11 rounds of financing before going public, with the scale of financing growing rapidly. Financing at different stages carries different missions.

The first few rounds of financing occurred during the industry's embryonic exploration stage, with funds mainly used for breakthroughs in core technologies and product refinement. At that time, Unitree was still a small team needing to prove that its technological route was feasible and its products had a market.

In contrast, the background of the last few rounds of financing before the IPO was entirely different. By this point, Unitree had already established itself as a global leader in quadruped robots and was striving for scale in the global market, laying out new tracks in industrial-grade robots, and expanding production capacity. All these required huge amounts of capital support, which the company's own profits could no longer meet.

Corresponding capital not only brought funds to Unitree but also industrial resources and market channels, helping it quickly grow into an industry leader.

Today, the industry landscape has changed. Even more and more automakers are entering the field, making the entire race increasingly intense. Thus, the current fundraising obviously has new purposes. Public information shows that Unitree Technology plans to raise 4.2 billion yuan in this IPO, with projects including intelligent robot model R&D, robot ontology (body) R&D, new intelligent robot product development, and the construction of an intelligent robot manufacturing base.

As a result, Unitree Technology is poised to become the first company listed on the A-share market primarily engaged in humanoid robots.

Comparing horizontally with peers, before Unitree Technology, humanoid robot manufacturers UBTECH and RoboTrek had already gone public in Hong Kong. For the entire industry, Unitree's listing means that capital demands have begun to serve as a crucial turning point for industry development.

Before these companies entered the capital market, financing in the robotics industry mainly concentrated in the early stages, with outsiders placing more emphasis on the tech team, product prototypes, and practical performance on public stages. Later, commercialization and competitiveness became new evaluation factors, which is also why manufacturers need new capital injections to enhance these effects.

It's not hard to judge that more robotics companies will follow Unitree's example in the future, accelerating development through capital operations, and the entire industry will enter an era of capital frenzy.

But then again, "Capital is water, and technology is a boat. Only when the water rises can the boat rise, but water can also capsize it." After Unitree successfully enters the capital market, the rules of the game for the entire embodied intelligence track (track) will also change accordingly.

| Where Does Unitree Spend Its Money? |

"Robots are harder than cars because you can sell a car once you make it, but robots are different—they're probably more complex." This is roughly what He Xiaopeng stated in an interview.

This means that the scale and speed of monetization in the robotics industry are probably far slower than those in the new energy vehicle industry. Digging deeper, why has the robotics industry become one that requires long-term investment?

Humanoid robots are known as the "ultimate form of artificial intelligence." Compared to the Internet, mobile Internet, or even large language models, embodied intelligent robots require greater capital investment, longer technological iteration cycles, more complex hardware supply chains, and higher costs for mass production ramp-up.

So where does the huge amount of money usually go?

First is R&D investment. Embodied intelligent robots are a multidisciplinary field involving mechanical engineering, electrical engineering, computer science, artificial intelligence, materials science, and more.

Second is the hardware supply chain. The core components of robots include motors, reducers, controllers, sensors, cameras, etc. Affected by factors such as the progress of import substitution and technological barriers, overall prices remain high. Taking the main six-axis force sensors as an example, the current price for a single unit is mostly over 20,000 yuan. Assuming a manufacturer ships around 5,000 humanoid robots a year, the cost for this component alone exceeds 100 million yuan (Unitree's net profit last year was 288 million yuan). Meanwhile, the prices for a single 2D/3D camera are approximately 1,000/2,500 yuan, respectively. To reduce costs and improve performance, although Unitree Technology has chosen a full-stack self-research route, its humanoid robot products still start at tens of thousands of yuan, indicating that related costs remain high.

According to Unitree's prospectus, the company's main raw materials include mechanical parts, electronic components, electrical materials, etc. Electronic components cover capacitors, resistors, inductors, PCBs, transistors, crystals, chips, antennas, etc. From January to September 2025, the procurement amount for electronic components was 130 million yuan, accounting for 25.10% of the total raw material procurement; in 2024, it was only 46.2681 million yuan, accounting for 23.89%. This means that expenditure on supply materials has grown rapidly with delivery volumes.

Promotion and sales expenses also consume significant funds. As a new product, robots require educating the market and cultivating user habits. Unitree Technology is moving offline into large retail stores and more direct-sale store (direct-operated stores), which may require more fixed asset cost expenditures. All these activities demand huge expenses.

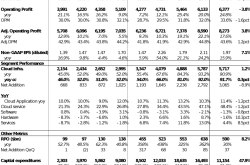

According to the prospectus, from 2023 to 2025, Unitree Technology's total expenses were 93.6733 million yuan, 137 million yuan, and 687 million yuan, respectively, accounting for 58.86%, 34.88%, and 40.41% of revenue in the same periods. Breaking it down specifically, from 2023 to 2025, the company's cumulative expenditures on R&D, sales, and administrative expenses were 265 million yuan, 238 million yuan, and 420 million yuan, respectively.

From the above, we can see where Unitree Technology spends its money. However, as He Xiaopeng mentioned, uncertainties still abound after going public.

In the first quarter of 2026, Unitree Technology achieved revenue of 423 million yuan, with the year-on-year growth rate dropping from 332.64% in the previous year to 68.49%. Net profit attributable to the parent company was approximately 50.01 million yuan, down 47.69% year on year. This indicates that Unitree's profit foundation is still not solid enough and requires sustained high investment to maintain growth.

Currently, the main bottleneck for the entire industry, including Unitree Technology, lies in commercialization. Although Unitree Technology has achieved profitability, the entire industry is still in its early stages.

Most robotics companies are still burning money and have not found a clear path to profitability. Even for Unitree, its revenue mainly comes from the B-end market, while the C-end market has not truly opened up. The price of a household service robot at tens of thousands of yuan is still too high for ordinary consumers to afford. Moreover, the intelligence level of robots is not yet high enough, and the tasks they can perform are relatively limited.

For Unitree Technology, the ability to continuously prove itself and build robust and Consistently leading (continuously leading) market competitiveness in the industry is crucial.

| Industrial Scenarios and the C-End Market Are Key to Commercialization Returns |

Unitree Technology's journey from financing to going public has created a miracle in China's robotics industry. However, as everyone knows, going public is not the finish line but a new starting point. The capital market is never a charity; it only pays for companies that can continuously create value.

All the previous financing and high valuations ultimately need to be redeemed with hard cash brought by sales volumes. For Unitree, achieving a sharp increase in sales volumes is the first hurdle it must overcome after going public.

Since all the previous financing and high valuations ultimately need to be redeemed with hard cash brought by sales volumes, the capital market has given Unitree a valuation of 42 billion yuan based on expectations of future sales growth.

If Unitree cannot achieve the expected sales growth and maintain its leading position, its valuation may face downward pressure. Taking humanoid robots as an example, in 2025, Unitree's shipments of humanoid robots exceeded 5,500 units (not order quantities), already the highest globally, but still far from true mass production.

Public information also shows that from January to September 2025, the company's humanoid robots generated 595 million yuan in revenue, with 73.6% coming from Research and Education (scientific research and education) clients, including universities and research institutions. Revenue from commercial consumption scenarios accounted for 17.39% of humanoid robot revenue. Therefore, among the thousands of humanoid robots sold by Unitree Technology, industry applications such as corporate guided tours, intelligent manufacturing, and intelligent inspections contribute significantly.

In layman's terms, the current humanoid robots sold by Unitree Technology have limited applications as large-scale production tools. Moreover, as more and more companies enter the embodied intelligence race, market competition will become increasingly fierce.

Unitree not only has to face competition from international giants like Boston Dynamics and Tesla but also challenges from domestic peers such as UBTECH, Zhiyuan, and Yunshenchu. According to data compiled by Southern Weekly last year, the industry is highly competitive in terms of order acquisition, which is indeed the current reality that Unitree Technology must confront.

Theoretically, economies of scale are the core competitiveness of the manufacturing industry. Only when sales volumes reach a certain scale can R&D costs, production costs, and sales costs be effectively amortized, thereby improving gross and net profit margins.

Although Unitree Technology is actively exploring new application scenarios, extending from the consumer market to industrial and commercial markets to find new growth points, the C-end market, which remains difficult to penetrate, is indeed a headache for all peers. Tesla faces the same challenge, as its Optimus Gen-3 still needs to complete factory validation.

There are many reasons why the C-end market is difficult to crack: high markups across the supply chain lead to expensive prices, the lack of a general-purpose large model for robots results in insufficient product practicality, and the absence of scale advantages makes it difficult to amortize and offset industrial chain (supply chain) costs, creating a vicious cycle.

Of course, looking back, for other competitors, Unitree's listing is both an opportunity and a challenge. The opportunity lies in the fact that Unitree's success proves the commercial value of the robotics industry, attracting more capital to enter this track (track).

On the challenge side, Unitree has gained more financial support, which will further widen the gap with other companies. It is foreseeable that in the coming years, the embodied intelligence track (track) will undergo a brutal industry shakeout. A group of companies with weak technological capabilities and insufficient financial reserves will fall before the IPO and be eliminated by the market.

Image sourced from the internet. Rights reserved for the original creator.

-

![]()

Apple Shareholders Paid $230 Billion in 'Make-Up Exam Fees' for Apple's AI

-

![]()

Oracle Plummets? The Irreparable Flaws Beyond AI Infrastructure - 'High Interest, High Debt + Stagnant Software'

-

![]()

Oracle Plummets? The Irreparable Damage That AI Infrastructure Can't Fix—'High Interest, High Debt + Failing Software'

-

![]()

The Largest IPO in History Is on the Horizon: Why SpaceX Justifies a $1.75 Trillion Valuation

-

![]()

Cook's Gourd Holds No Magic Cure for Apple's AI Woes

-

![]()

Uber Exhausts Annual AI Budget in Just Four Months: Why Can't Even Uber Sustain AI Token Costs?

-

Unitree Goes Public, Ushering in an Era of Capital Frenzy for Robots?

-

![]()

In-Depth Exploration of the Physical AI Industry Ecosystem