Trillion-Dollar Valuation Makes History! OpenAI Files for IPO in Stealth Mode

06/12 2026

06/12 2026

541

541

The curtain has been lifted on a trillion-dollar IPO spectacle.

On June 8 (local time), OpenAI confirmed on its official website that it had covertly submitted a draft S-1 registration statement to the U.S. Securities and Exchange Commission, officially initiating the IPO process.

In its statement, the parent company of ChatGPT made an intriguing remark: 'We recently submitted an S-1 filing confidentially.'

'We anticipate that this filing may eventually become public, so we've decided to share the news now.' Essentially, since the news was bound to surface, they chose to announce it proactively.

Altman's strategy was astute. Rather than waiting for the media to break the news prematurely and then responding reactively, he used the statement to take control of the narrative.

However, OpenAI also tempered market expectations: No specific timetable for the listing has been set, and as a private company, it may find it more convenient to handle certain matters. Going public 'may still take some time.'

This carefully worded statement leaves OpenAI with flexibility while keeping the market guessing. Will the listing occur in the second half of this year? Or will it be delayed until 2027? The timing now seems likely to hinge on the listing progress of competitors like SpaceX and Anthropic—no company wants to miss out on the initial wave of capital.

This AI giant, with annualized revenue exceeding $20 billion, has finally taken a concrete step toward the public market.

How does OpenAI generate revenue?

Let's first clarify the company's business model. While many associate OpenAI with ChatGPT, its revenue streams are more diverse than commonly perceived.

Currently, its business is divided into three main segments:

The first is ChatGPT subscriptions, which operate on a monthly fee basis. Users who upgrade gain access to additional features and higher usage quotas—a classic SaaS (Software as a Service) model.

The second is API calls. Enterprises and developers utilize OpenAI's models to build their own products, with fees based on usage volume. Altman recently revealed that the API business alone generated over $1 billion in new annual recurring revenue in the past month.

The third is enterprise services, where large companies pay substantial fees for compliance, security, and customized solutions. In January 2026, OpenAI officially began testing ads in the free version of ChatGPT, marking a significant shift in its commercialization strategy. From now on, it will rely on a mix of subscriptions, APIs, advertising, and enterprise services.

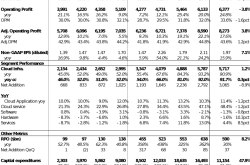

The underlying business logic is straightforward: More users translate to greater computational demand, which strains cash flow. From 2023 to 2025, OpenAI's computational power grew 9.5-fold, while revenue increased tenfold. Computational power is OpenAI's lifeblood—the more it has, the faster it can innovate.

OpenAI's valuation trajectory exemplifies exponential growth. From 2018 to 2020, its valuation hovered around $130 million, a relatively insignificant figure.

The real surge came after ChatGPT's debut. In early 2023, its valuation stood at $29 billion during fundraising, rising to the $27–29 billion range by April 2023. By 2024, valuations continued to climb, and after securing approximately $40 billion in financing in 2025, its valuation surged past $150 billion, joining the 'hundred-billion club.'

In late March 2026, OpenAI announced the completion of $122 billion in financing, locking in a post-money valuation of $852 billion—the largest private funding round in business history.

Data source: Public queries, compiled by Investment Bank Junior Sister

Post-IPO valuation could approach $1 trillion.

A comparison of the three funding rounds tells the story. The $40 billion round in 2025 was once considered historic, only to be surpassed by the $112 billion round in 2026. The final $122 billion round was nearly triple the 2025 figure.

In just six years, its valuation soared from $130 million to $852 billion—a more than 6,500-fold increase.

Most notably, this $122 billion round was led by Amazon, NVIDIA, and SoftBank, which collectively committed $110 billion.

Amazon alone pledged $50 billion, with $15 billion arriving immediately and the remaining $35 billion contingent on OpenAI completing its IPO or achieving Artificial General Intelligence (AGI).

The financial realities behind the glamour

Behind the impressive numbers lie stark financial challenges.

By the end of 2025, OpenAI's annualized revenue approached $20 billion. According to internal documents obtained by The Wall Street Journal, the company projected a net loss of about $9 billion for 2025.

What does that mean? For every $1 earned, it spent approximately $1.69. Analysts at Deutsche Bank put it bluntly: 'No startup in history has operated with losses of this scale. We are in entirely uncharted territory.'

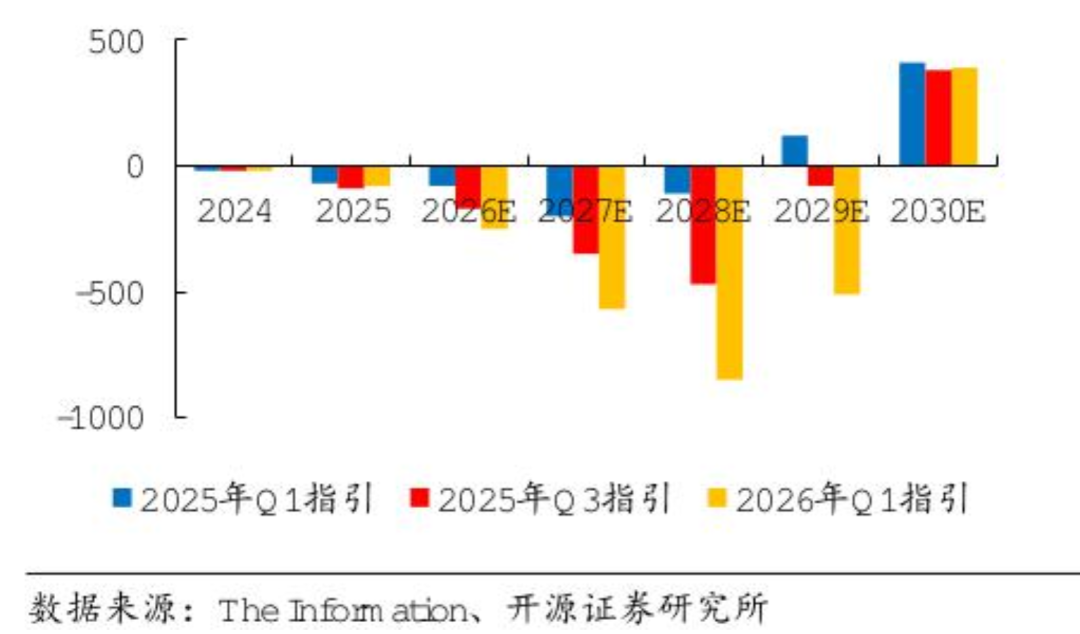

The situation remained dire in 2026, with full-year losses expected to hover around $14 billion. More alarmingly, this cash burn is projected to continue until at least 2029, with cumulative losses potentially reaching $115 billion. Profitability is now expected to be delayed until the 2030s.

The reason for the cash burn is straightforward. Training and running large models is exorbitantly expensive. ChatGPT has over 900 million weekly active users, but only about 50 million are paying customers—a conversion rate below 5%. For every 20 free users served, 19 consume computational resources without paying.

Even more sobering, Altman himself admitted that the $200-per-month Pro plan still operates at a loss. Higher charges lead to heavier usage; heavier usage drives up costs.

Domestic securities firms predict OpenAI's cash flow break-even point could be pushed to 2030: (Unit: $100 million)

A crowded competitive landscape

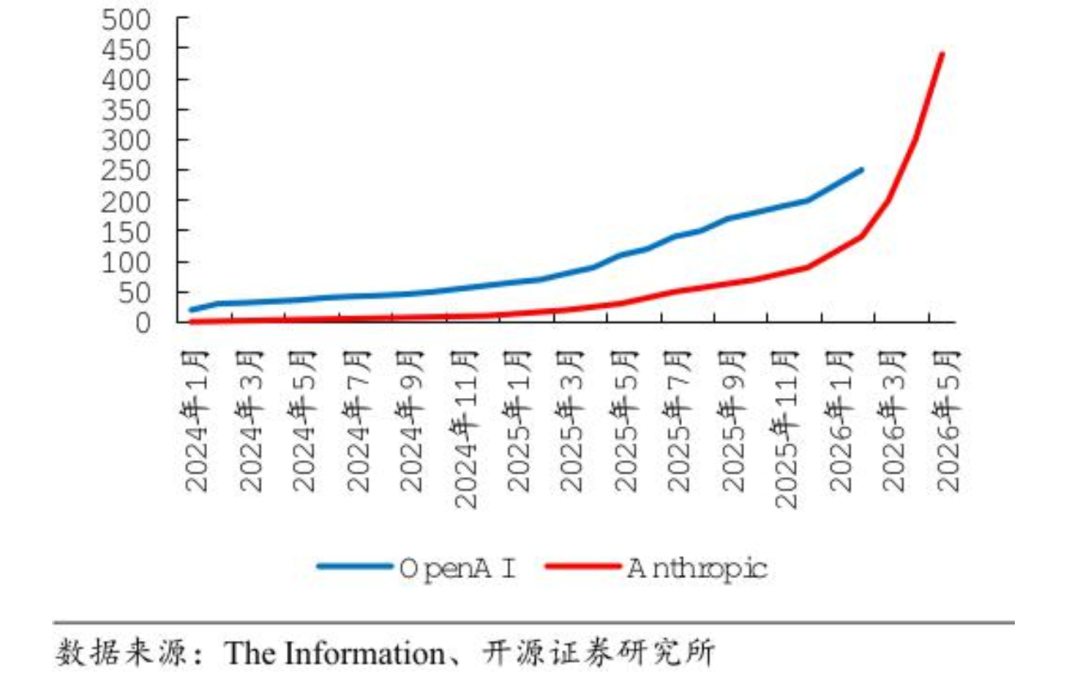

To make matters worse, OpenAI isn't operating in a vacuum. In the same week it submitted its IPO application, rival Anthropic surpassed OpenAI with a $965 billion valuation, becoming the world's highest-valued AI company.

Notably, Anthropic's Annual Recurring Revenue (ARR) growth rate significantly outpaces OpenAI's.

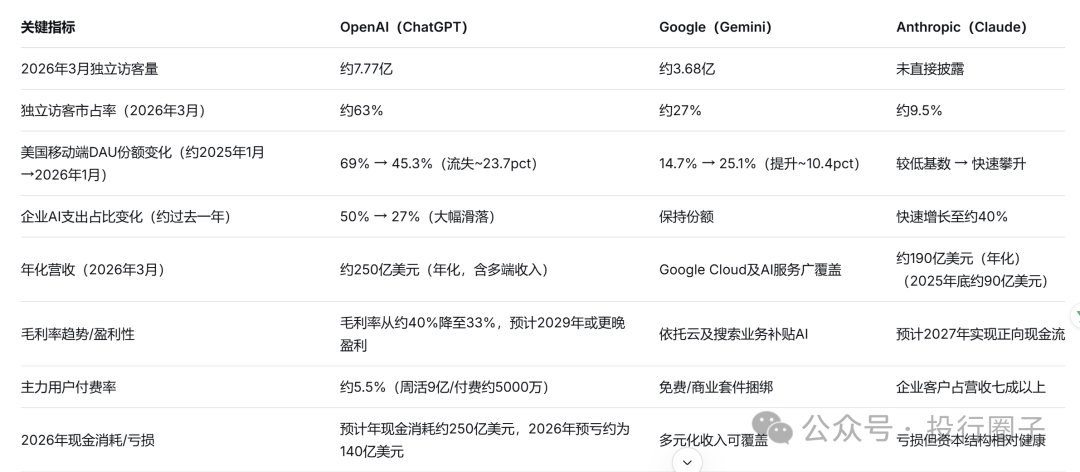

A comparison of core data from both companies reveals the gap:

(Data sources: DoNews, The Wall Street Journal, Counterpoint, Semi Analysis)

In reality, the two companies use different methods for revenue accounting. Anthropic employs gross revenue reporting, counting all sales through cloud partners as revenue. OpenAI uses net revenue reporting, only counting its share of income. Even after adjusting for this, Anthropic's enterprise monetization remains stronger.

At the product level, Anthropic's Claude Code has become a game-changer in enterprise programming. Stripe deployed Claude Code to 1,370 engineers, completing a cross-language code migration in four days that would have taken 10 people weeks to finish.

Data source: Public queries, compiled by Investment Bank Junior Sister

What pressures OpenAI even more is Anthropic's projection to achieve profitability for the first time in Q2 2026, with planned operating profit reaching $559 million. Meanwhile, OpenAI's adjusted operating margin for the same period was -122%—losing $1.22 for every $1 earned.

The market's valuation of these two companies speaks volumes.

Behind the trillion-dollar IPO race, the waters run deep

OpenAI's IPO warrants careful scrutiny for several reasons.

First, it's not going public because it's short on cash. OpenAI just secured $122 billion and isn't hurting for money in the short term. Why rush to list?

The logic is simple: Public equity is the cheapest financing channel available, especially while interest rates remain high. With AI stocks soaring in the U.S., investors are lining up to invest. Missing this window could mean losing momentum if the market cools in a few years.

JPMorgan Chase CEO Jamie Dimon recently issued a warning, noting that the current market euphoria reminds him of 1972, 1986, 2000, and 2007—years that coincided with two major bear markets, the dot-com bubble, and the global financial crisis.

Bridgewater Associates' Ray Dalio also believes U.S. stocks are approaching levels seen before the 1929 Great Depression. Whether their judgments are exaggerated remains to be seen, but at least one thing is clear: Markets feel 'good' precisely when they're most dangerous.

Second, OpenAI's 'platformization' is accelerating. The company's true ambition isn't to be a tool provider but to collect 'rent' in the AI era.

Earlier this year, CFO Friar proposed an intriguing idea: If clients use OpenAI's technology to develop drugs, OpenAI wants a share of the sales revenue.

This isn't selling tools—it's investing in clients' value chains. From subscription fees to API charges to outcome-based royalties, OpenAI is transforming from a 'shovel seller' to a 'gold mine stakeholder.' The trillion-dollar valuation investors are buying isn't for $20-per-month memberships but for access to AI infrastructure.

Third, how will OpenAI's unique governance structure fare post-IPO? Altman doesn't directly hold any equity in OpenAI—a rarity among tech founders. The company employs a 'foundation + for-profit entity' dual structure, where the nonprofit arm owns about 26% of the for-profit entity and retains control.

This means investors will have limited say after buying in, and the safety committee can even block the release of high-risk models. Whether this structure will face valuation discounts in the public market is a question the IPO must answer.

A Bet by the Money-Burning Machine

The listing of OpenAI appears to be a capital feast, but at its core, it is a bet on the future.

It bets that AI will become the core driving force of the next economic cycle, just like the internet. It bets that model capabilities will continue to improve, reasoning costs will keep declining, and the user base will keep expanding, ultimately achieving a self-sustaining platform cycle.

Does this logic hold water? Judging from the data of the past three years, the simultaneous growth of computing power and revenue does seem to validate this positive cycle. However, any large-scale infrastructure investment comes with a long payback period. OpenAI's financial data has already made everything clear: in the short term, it remains a money-burning machine.

The warning from JPMorgan Chase's CEO may be worth keeping in mind as a reference point for every investor. But to be fair, every technological revolution is accompanied by bubbles, and only after these bubbles burst do truly fortified companies emerge.

For ordinary readers and investors, it might be

-

![]()

Apple Shareholders Paid $230 Billion in 'Make-Up Exam Fees' for Apple's AI

-

![]()

Oracle Plummets? The Irreparable Flaws Beyond AI Infrastructure - 'High Interest, High Debt + Stagnant Software'

-

![]()

Oracle Plummets? The Irreparable Damage That AI Infrastructure Can't Fix—'High Interest, High Debt + Failing Software'

-

![]()

The Largest IPO in History Is on the Horizon: Why SpaceX Justifies a $1.75 Trillion Valuation

-

![]()

Cook's Gourd Holds No Magic Cure for Apple's AI Woes

-

![]()

Uber Exhausts Annual AI Budget in Just Four Months: Why Can't Even Uber Sustain AI Token Costs?

-

Unitree Goes Public, Ushering in an Era of Capital Frenzy for Robots?

-

![]()

In-Depth Exploration of the Physical AI Industry Ecosystem