Lenovo: Best Financial Results Amidst Transformation Dilemmas

06/15 2026

06/15 2026

498

498

Summary: On May 22, 2026, Lenovo Group delivered its best-ever fiscal year performance. For the 2025/26 fiscal year, the company's annual revenue grew by 20.3% year-on-year to RMB 589.9 billion, surpassing the RMB 500 billion mark for the first time. Adjusted net profit surged by 42.1% year-on-year to RMB 14.5 billion, doubling the revenue growth rate. Notably, revenue in the fourth fiscal quarter soared by 27.1% year-on-year to RMB 149.5 billion, marking the fastest quarterly growth in nearly 20 quarters (five years).

The AI business is becoming Lenovo's core growth engine. In the fourth fiscal quarter, revenue from AI-related businesses surged by 84% year-on-year, with its share of total revenue jumping to 38%. Annual AI revenue soared by 105% year-on-year. Specifically, AI-related revenue in Lenovo's China region skyrocketed by over 140% year-on-year, accounting for 32% of the region's total revenue.

Under the new target of "achieving $100 billion in revenue in two years," the question arises: Is this impressive performance a natural outcome of Lenovo's long-term technological accumulation, or merely a stroke of luck for a hardware giant riding the AI boom and storage super cycle?

Below is the main text:

As a core player in the AI sector and one of the few tech companies with significant operations in both China and the U.S., Lenovo was the world's largest PC vendor in Q2 2025, with a global market share expanding to 24.8%, according to IDC. Operating in over 180 countries and regions with more than 80,000 employees and over 30 production bases, Lenovo delivered its best-ever fiscal year performance with exceed expectations (better-than-expected) growth over the past year.

For the 2025/26 fiscal year, Lenovo Group's annual revenue reached RMB 589.9 billion, up 20.3% year-on-year, nearing RMB 600 billion. Adjusted net profit hit RMB 14.5 billion, up 42.1% year-on-year, doubling the revenue growth rate. Both revenue and adjusted net profit exceeded market expectations. Revenue in the fourth fiscal quarter surged by 27.1% year-on-year to RMB 149.5 billion, marking the fastest quarterly growth in nearly 20 quarters (five years).

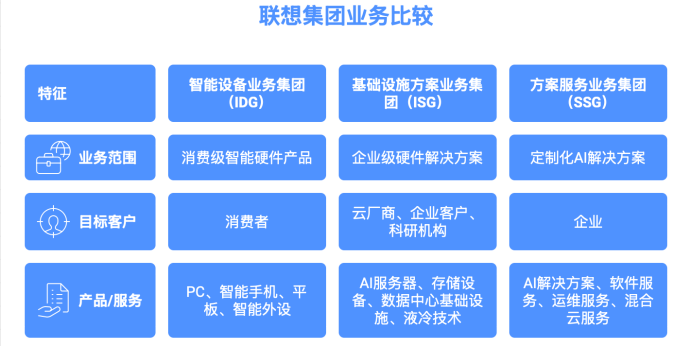

All three of the company's business groups—IDG (Intelligent Devices Group), ISG (Infrastructure Solutions Group), and SSG (Services & Solutions Group)—achieved double-digit growth.

The Intelligent Devices Group (IDG) contributed the most to revenue. Annual revenue reached RMB 418.5 billion, up 17% year-on-year. Revenue in the fourth fiscal quarter hit RMB 101.2 billion, up 24% year-on-year. Lenovo maintained a leading market share in PCs at 24.2% annually and 24.4% in Q4, with high-end PC shipments accounting for 50% of total PC shipments in Q4, up 29% year-on-year, indicating a shift toward premium product lines.

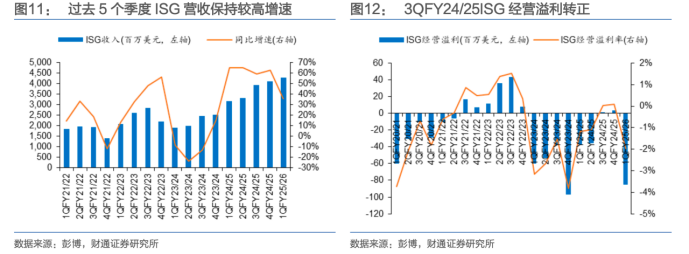

The Infrastructure Solutions Group (ISG) achieved the fastest growth, turning historically profitable and setting new records. Annual revenue exceeded RMB 136 billion, up 32% year-on-year. Revenue from AI servers surged by 50% year-on-year, with year-end order backlog exceeding RMB 140 billion.

As AI applications move from technical exploration to commercialization, revenue from industry-specific AI solutions has soared. Lenovo's Services & Solutions Group (SSG) revenue surpassed $10 billion for the first time, up 19% year-on-year. In Q4, revenue from operational services and project solutions accounted for 62% of the total.

Over the past year, Lenovo Group has indeed delivered an impressive performance: revenue "off the charts," all three business groups growing simultaneously, and double-digit high-speed growth. The efforts and preparations behind this achievement are worth examining.

Stockpiling to Navigate the Storage Super Cycle

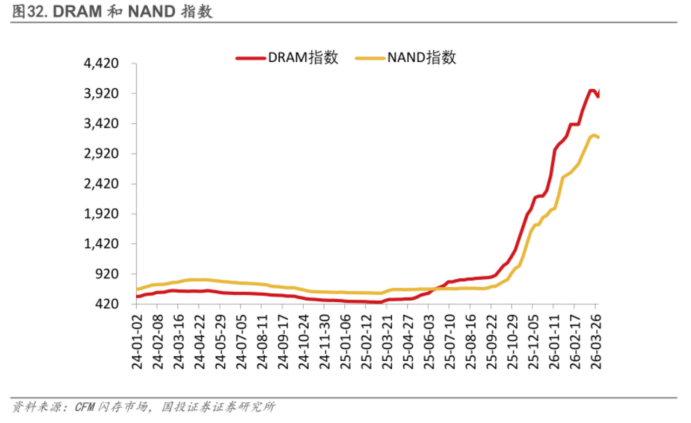

To understand the quality of Lenovo's recent performance, it's essential to clarify the "storage super cycle," a critical variable currently impacting the consumer electronics industry.

For the broader storage market, this super cycle is not a typical inventory restocking cycle but a structural price hike driven by AI computing infrastructure. Currently, Samsung, SK Hynix, and Micron have shifted over 80% of their advanced production capacity to high-bandwidth memory (HBM) for the lucrative AI market, causing severe shortages of traditional storage chips like NAND Flash and DRAM for the consumer market. This structural supply-demand gap has triggered the sharpest price surge in recent years, with DRAM price increases revised upward from ~150% to 250%-280% in 2026, and NAND price forecasts raised from ~100% to 200%-250%.

The sharp rise in storage costs has imposed widespread cost pressures on the global smart device industry, squeezing profit margins for complete machine (complete devices). For laptops, storage costs are expected to rise from 10%-18% to over 20% of the total BOM cost. Facing industry-wide price hikes, major OEMs have begun raising prices. Lenovo, leveraging its strong brand influence, market clout, and pricing power, has demonstrated exceptional ability to pass on upstream cost increases to downstream consumers.

In interviews with Shenzhen Business, it was found that Lenovo began consecutive price hikes in May 2025, with mainstream models rising by RMB 800-1000 and some high-end models exceeding RMB 1000. In contrast, HP's PC prices increased by RMB 200-300, relatively smaller, offering higher cost-performance at similar configurations.

Lenovo CFO Wong Wai Ming revealed in an interview that to counter the "unprecedented" price surge driven by AI demand, the company has stockpiled memory sufficient for all of 2026, with component inventory levels ~50% higher than usual. Lenovo's proactive inventory strategy has become a key tool for mitigating cost pressures and stabilizing profitability.

The early stockpiling strategy can translate into cost advantages during price hikes. By the end of Q3, Lenovo's storage inventory covered 7-8 months of usage, far exceeding the industry average of 2-3 months. However, this also means significant capital tied up in inventory, raising risks of inventory write-downs if prices decline. Can the company maintain its current gross margins? For now, this strategy has shown advantages in financial reports. Industry sources indicate that a consumer electronics company faced severe gross margin pressures due to inventory issues.

Explosive Growth in AI Server Business

Financial reports show that Lenovo's annual AI-related revenue skyrocketed by 105% year-on-year, accounting for nearly 33% of total group revenue, and rising to 38% in Q4. Chairman and CEO Yang Yuanqing predicted boldly on the earnings call that AI PCs would account for over 50% of total PC sales in the new fiscal year. Additionally, strong server demand, driven by increased cloud investments from key clients and enterprise market expansion, boosted revenue. Supported by a robust product lineup and leading liquid cooling technology, AI server revenue more than doubled year-on-year. AI is rapidly becoming Lenovo's core growth engine.

Amid the AI computing infrastructure boom, Lenovo continues to expand high-end server capacity, accelerating its shift toward high-value-added AI infrastructure. The company's annual server manufacturing capacity now exceeds 70,000 racks, including over 11,000 liquid-cooled racks. It plans to deliver next-generation Rubin AI server racks in H2 2026, focusing on core computing needs for AI data centers—a key battleground in the industry.

Product mix upgrades have significantly boosted average selling prices (ASPs). In high-end AI servers, Lenovo's models priced above $250,000 saw ASPs surge from ~$576,000 in Q2 last year to $1.4 million in the previous fiscal quarter, reflecting its strategic shift toward high-end AI training servers. However, competition in the server market remains fierce. According to IDC, in China's 2025 x86 server market, Inspur, Super Micro, H3C, Lenovo, and ZTE ranked top five with market shares of 31.3%, 12.7%, 12.5%, 10.7%, and 8.5%, respectively.

During the global AI infrastructure boom, overseas hardware leader Dell also delivered explosive results. In Q1 2027, Dell reported revenue of $43.8 billion, up 88% year-on-year; adjusted EPS reached $4.86, up 214% year-on-year, outpacing industry profit growth. Dell's AI system-related revenue surged by 757% year-on-year to $16.1 billion, with total AI orders hitting $24.4 billion and year-end backlog at $51.3 billion. Serving over 5,000 AI server clients, Dell holds a significant edge in industry layout (positioning).

Both Lenovo and Dell are classified by capital markets as traditional hardware cycle stocks, but their valuations and market perceptions differ sharply. Dell, with earlier AI server commercialization and faster revenue realization, enjoys a higher valuation premium. Lenovo, relying on upgrading traditional hardware with AI features, struggles to shake off the "hardware assembler" bias in capital markets.

In the consumer market, while Lenovo remains a global PC leader, a perception gap persists with its high-tech brand positioning. The productivity redefinition of AI PCs in this tech wave may help reshape its brand image.

At CES 2026, Dell, a veteran in AI PC marketing, shifted AI to the functional layer, refocusing PC efforts on product line updates, design, reliability, and commercial needs. Similarly, Luca Rossi, president of Lenovo's IDG, stated in media interviews that users explicitly choosing AI PCs for AI features remain a minority of professionals. Most consumers prioritize device thinness, battery life, and future upgradability over AI capabilities.

This implies that consumer PC revenue growth relies more on storage cycle-driven price hikes than genuine AI application demand, leaving AI PCs in a commercialization debate between "structural improvement" and "market share replacement." Only sales growth driven by real end-user demand can sustain long-term corporate performance.

Lenovo's $100 billion revenue target for the new fiscal year is both a confidence declaration to capital markets and a double-edged sword. Whether AI can truly come to the rescue will determine the blade's direction.

The Challenge of Transitioning from "Assembly Thinking" to "Full-Stack AI"

Lenovo's AI transformation benefits from years of accumulation and M&A preparations.

Liquid cooling technology exemplifies this. The company's Neptune liquid cooling achieves 98% efficiency, reducing data center PUE to below 1.1. With a decade-plus leadership in global HPC Top500 rankings, Lenovo boasts industry-leading technical application prowess.

In AI storage, Lenovo acquired Infinidat, a global provider of high-end enterprise storage solutions, filling a critical gap in ISG's high-end enterprise storage and improve (completing) its computing-storage integration layout.

Beyond acquisitions, the company invested in AI chip startups, from Cambricon and Hygon to Moore Threads and MetaX, becoming the only investor heavily backing all four leading domestic AI chip firms, achieving full coverage of mainstream domestic computing chips.

Meanwhile, Lenovo deepened strategic partnerships with global chip leaders like NVIDIA. According to financial reports, the GB300 NVL72 rack solution has entered mass production, and the next-gen Rubin architecture platform for AI computing will launch in H2 2026, further strengthening high-end AI server capabilities.

However, Lenovo's deep ties with NVIDIA and AI chip investments still differ fundamentally from "proprietary technology." Lenovo acts more as a "financial investor + supply chain integrator" than a core technology owner. This AI development model, built on "proprietary capacity + invested technologies," struggles to establish long-term irreplaceable competitive barriers.

Under the influence of geopolitical frictions, compared to Huawei, which has formed an ecological closed loop through its full-stack self-developed Ascend AI chips, Lenovo relies heavily on external chip supply chains, posing persistent supply chain security risks.

Epilogue: What Has the Cyclical Dividend Concealed?

Lenovo's impressive financial results and mature AI strategic narrative are essentially phased (phased) outcomes driven by the combined effects of the storage supercycle and the surge in AI computing power demand. These do not fully confirm that Lenovo has completed a fundamental transformation from a traditional hardware assembler to an AI technology enterprise.

For Lenovo, short-term AI concept iterations and cyclical dividends are insufficient to support long-term growth. The true breakthrough in transformation lies in achieving a profound leap from supply chain integration capabilities to independent technological capabilities, thereby fundamentally reevaluating the company's value. Looking ahead, with its solid foundation in end-user hardware and computing infrastructure, Lenovo is poised to continue benefiting from the industrial resonance of differentiated collaborative development between Chinese and U.S. hybrid AI systems, opening up new avenues for growth in the commercialization and inclusive AI sectors.

- XINLIU -

-

AI Asset Spin-offs at Tech Giants: Is Kling Paving the Way for ByteDance and Alibaba?

-

![]()

Why Zhang Xue? Why HONOR?

-

![]()

Exclusive! Tencent’s ‘Tencent Drive’ with AI-Powered Asset Backup in the Works—A Game-Changing Move

-

![]()

Internal Upheaval in Initial Listing Days: SpaceX's AI Division Faces Accelerated Talent Loss, with 50+ R&D Staff Exiting in 2026

-

![]()

Price War Fails, Chinese Automakers Have No Retreat

-

![]()

Still in the Red but Outpacing Tesla: What Lies Behind SpaceX's $2.1 Trillion Valuation?

-

![]()

Humanoid Robots Go Global: From 'Actors' to 'Workers'

-

![]()

Still Incurring Losses Yet Outpacing Tesla: What Does SpaceX's $2.1 Trillion Valuation Signify?