Humanoid Robots Go Global: From 'Actors' to 'Workers'

06/15 2026

06/15 2026

460

460

Author|Tang Fei

Editor|Li Xiaotian

On June 11 (local time), the 2026 FIFA World Cup officially kicked off.

This World Cup not only features the largest-ever lineup with 48 participating teams but also serves as the largest real-world testing ground for artificial intelligence and robotics in human sports history. FIFA has officially announced that Boston Dynamics' Atlas humanoid robots and Spot quadruped robot dogs will be deployed across multiple World Cup venues for practical tasks, including event operations support, fan interactions, and security patrols.

The first batch of customized Boston Dynamics Spot robots has been deployed at three core venues—the Dallas International Broadcast Center, New York Stadium, and New Jersey Stadium—to perform autonomous patrols and real-time venue monitoring.

Robots transforming into 'workers' has become a new trend in the humanoid robot sector in 2026. It's not just overseas companies; domestic robots are already seen 'handling cargo' in the loading zones of Tokyo's Haneda Airport, 'screwing components' on production lines at Texas Instruments' U.S. factories, and 'making coffee' in foreign supermarkets.

Traditional industrial robotic services have been evolving for decades, yet the global annual installation volume remains stagnant at just over 500,000 units. The issue isn't that robotic arms (manipulators) are immature—rather, traditional automation is too rigid, expensive, and lacks flexibility. Truly decentralized flexible tasks in factories—such as agile sorting, complex assembly, and intelligent quality inspection—are difficult for robotic arms to complete fully autonomously and still heavily rely on manual labor.

These processes may seem simple but are challenging to cover cost-effectively with traditional automation systems. The increasingly mature AI and embodied intelligence technologies have largely resolved these adaptation challenges across various scenarios.

As a result, we see that in 2026, more and more humanoid robots are transitioning from being 'actors' on stages to 'workers' in factories.

The 'Qualitative Shift' Behind the Data

Customs data provides the most direct evidence.

In the first four months of 2026, China exported a cumulative total of 8.145 million robots of various types, with a total value of 15.79 billion yuan, setting new historical highs in both export volume and trade value. Products were shipped to over 150 countries and regions worldwide.

The pace of humanoid robot exports is particularly remarkable. In the first quarter of 2026, Chinese humanoid robot exports surged by 210% year-on-year, with Europe, Southeast Asia, and the Middle East serving as the primary markets. Morgan Stanley projects that Chinese humanoid robot sales will double to 28,000 units in 2026.

Judging from the mass production plans announced by several domestic companies, this year marks a critical juncture for capacity expansion and shipments.

Unitree Technology plans to ship 10,000–20,000 units in 2026; Zhiyuan Robotics aims to achieve a production capacity of 10,000 units in 2026, with revenue expected to double if deliveries proceed smoothly; UBTECH's humanoid robots secured nearly 1.4 billion yuan in total orders for 2025, with production capacity reaching ten thousand units in 2026; Deep Robotics anticipates robot shipments to exceed ten thousand units in 2025, with further capacity increases in 2026.

Meanwhile, successful financing rounds have further accelerated production and deployment.

Looking at the financing side, data shows that in the first quarter of 2026, there were over 100 financing events across China's humanoid robot industry chain, with the largest single funding round reaching 2.5 billion yuan and 15 deals exceeding 1 billion yuan.

On the other hand, since January, over 20 embodied intelligence companies have announced listing plans. In addition to Unitree Technology, which has already passed regulatory reviews, the listing tutoring (listing coaching) registrations of RoboTech, Fourier Intelligence, and Deep Robotics have been accepted. Zhiyuan Robotics, Yinhe General, Zhongqing Robotics, Xinghaitu, and Songyan Power have completed their corporate restructuring.

Cao Wei, a partner at BlueRun Ventures, judges that the embodied intelligence industry is currently in the tail end of a typical expansion phase. Once leading companies go public, a clear valuation benchmark will form in the secondary market, putting significant valuation pressure on second- and third-tier companies and accelerating industry consolidation.

From Stages to Factories

If the data represents quantitative change, then the evolution of deployment scenarios constitutes true qualitative change.

UBTECH exemplifies this transformation most vividly.

According to UBTECH's annual report, its revenue from Hong Kong and overseas markets reached 475 million yuan in 2025, with products entering over 50 countries and regions. Rather than 'selling hardware first,' UBTECH appears to focus on building 'overseas recognition' before gradual expansion. Its Walker C model served at the China Pavilion during the Expo 2025 Osaka and was deployed in public settings like Paris Charles de Gaulle Airport, essentially establishing 'overseas public recognition' first.

After building recognition, UBTECH's products began transitioning into 'worker roles.' Global semiconductor giant Texas Instruments purchased UBTECH's humanoid robot Walker S2 and deployed it on its semiconductor production lines for debugging and applications. ROSSMANN, one of Europe's largest pharmacy chains, procured dozens of UBTECH's full-sized humanoid robots for deployment in retail stores and logistics centers. Recently, Japanese motor manufacturing giant Hitachi introduced UBTECH's Walker S2, primarily for elevator manufacturing and assembly.

Figure Caption: Unitree G1 Robot

Unitree Technology follows a similar path to UBTECH, targeting both public venues like airports and industrial deployments. In May 2026, the Unitree G1 robot, wearing a blue vest with the GMO logo, appeared at Tokyo's Haneda Airport as a newly hired 'ground crew' member, primarily handling baggage loading/unloading, cargo transfer, and conveyor belt coordination. In April, Warsaw, Poland, officially introduced the Unitree G1 robot, named 'Edward,' to help drive away wild boars overrunning the city's streets. Earlier in 2023, Unitree Technology established an exclusive strategic partnership with Saudi Arabia's QSS, deploying its industrial quadruped robot B2 at facilities of the Abu Dhabi National Oil Company (ADNOC) for high-temperature, high-risk environmental inspections and gas detection.

Dobot has emerged as a dark horse in the collaborative robotics sector. Its 2025 performance report shows a 31.7% year-on-year increase in annual revenue, with collaborative robot shipments ranking first globally. Serving over 80 Fortune 500 companies worldwide, including BYD, CATL, Mercedes-Benz, and Samsung, its business spans 15 major industries and over 200 niche scenarios, including automotive new energy, 3C electronics, semiconductors, surgical robotics, and new retail.

In the commercial services sector, coffee robots equipped with Dobot's Nova series collaborative robotic arms have operated stably in over 20 venues, including airports, high-speed rail stations, and supermarkets, setting a record of hundreds of thousands of fault-free cups. Coca-Cola's unmanned beverage stations along the Mediterranean coast, the UAE's 45-second coffee dispensing mobile stations, and unmanned food trucks in Singaporean malls all feature Dobot robots.

Geek+, another listed company, has set its sights on Europe. In 2025, Geek+ partnered with SEC Group to create an intelligent warehouse project for a leading UK electrical distributor; collaborated with AMH Material Handling to launch a UK intelligent warehousing center for Nisbets, a European catering equipment leader; and deployed large-scale shelf-to-person robot solutions with Watsons Group in the Benelux region. By year-end, its robot solutions were successfully implemented at Coolshop's intelligent warehouse in Denmark and global logistics provider Arvato's facility in Poland.

Figure Caption: Navigator 2 NAVIAI

In addition to these companies, the 'Navigator 2 NAVIAI' from Zhejiang Humanoid Robot Innovation Center entered the production base of European home appliance giant BEKO in Turkey. Zhiyuan Robotics partnered with automotive parts manufacturer Minth Group, aiming to enter the supply chains of Mercedes-Benz, BMW, and other automakers by deploying robots directly in factories. Wujie Power collaborated with global automotive parts giant ZF LIFETEC, focusing on precision assembly and soft object manipulation for automotive passive safety components. Paxini partnered with South Korean listed robotics company Neuromeka to launch a 'tactile + visual' bimodal dexterous hand capable of handling 3C electronics assembly, logistics sorting, and other precision operations. RoboTech's humanoid robots entered German automotive parts factories, working over 12 hours daily per unit and helping reduce workplace injury rates by 60%.

These cases paint a clear picture: Chinese humanoid robots are going mainstream—from airports to factories, logistics to manufacturing, services to production—embedding themselves as 'workers' across all segments of the global industrial chain.

Zhang Zhengtao, a researcher at the Institute of Automation, Chinese Academy of Sciences, provides a clear judgment on the commercialization scenarios for humanoid robots over the next three years. He believes that industrial and household applications will advance in tandem, but industrial manufacturing and warehousing logistics are relatively easier to implement.

For a long time, the humanoid robot industry seemed distracted by various 'stunts'—backflips, dancing, marathon running—which easily garnered attention. However, what truly defines industry milestones is not video view counts but who first enters real-world scenarios, especially industrial ones.

'Being able to screw in ten thousand screws repeatedly without error matters more than performing a hundred different movements. Industrial scenarios primarily demand load capacity, precision, and endurance from hardware, while algorithms require strong generalization and visual servoing capabilities. Warehousing logistics emphasize endurance, mobile stability, and navigation/obstacle avoidance, needing long-duration autonomous operation and dynamic environmental adaptation,' Zhang explains.

In reality, overseas demand for robots has consistently outpaced domestic needs. IFR (International Federation of Robotics) data shows that as of 2023, South Korea (1,012 units) and Singapore (770 units) had the highest robot densities in manufacturing globally, followed by China, the EU, and the U.S.

These figures indicate that South Korea, Singapore, the EU, and other countries have stronger demand and more mature deployments of robotic labor. With global population aging intensifying, demand for robots continues to grow across more nations and enterprises.

However, it's worth noting that the most valuable manufacturing scenarios—automotive, aviation, digital appliances—are already closely monitored by industry giants. Manufacturing behemoths like Tesla, Toyota, BYD, XPeng, and Xiaomi are all developing their own robots. Even Foxconn has deployed its self-developed humanoid robots at its Houston factory. These giants' closed-loop ecosystems of 'scenarios-data-algorithms' offer greater imagination.

This means the largest and most urgent industrial application scenarios may close doors to 'outsiders' like Unitree.

On the other hand, cost-effectiveness and reliability remain key bottlenecks for large-scale deployment.

Data from Gaogong Robot Industry Research Institute shows that the average cost of humanoid robots dropped to 100,000 yuan per unit in the first quarter of 2026, but this only reflects base model procurement prices. After deployment in specific production processes, the total cost of ownership (including operation and maintenance) can double or more compared to the purchase price. A robot capable of 'working' in a factory may have an actual total cost approaching 500,000–600,000 yuan.

Assuming a 500,000-yuan robot replaces a worker earning 100,000 yuan annually, payback takes five years.

Goldman Sachs' China Robotics Company Research Report describes the lengthy and complex typical deployment process. Generally, POC (Proof of Concept) validation requires 3–6 months and averages 2–3 rounds; small-batch testing follows, with initial factory orders usually under 50 units; another ~12-month validation period ensues; only at the pilot deployment stage do order volumes begin to scale to 50–100 units per customer.

This means that from a client's first serious consideration of a solution to stable deployment, two years or even longer may pass.

Most industry players believe the window for large-scale deployment will open between 2027 and 2029. Thus, the deployment news we see today functions more as 'showcases' with greater demonstration value than actual monetization capability.

A New Elimination Round Begins

Behind the differences in deployment scenarios lie variations in technological approaches, which ultimately manifest in business models.

Currently, humanoid robot companies primarily pursue three monetization paths.

The first path is the 'hardware sales model.' Represented by Unitree Technology, these companies focus on standalone unit sales, with pricing ranging from tens of thousands to hundreds of thousands of yuan. Their core competitiveness comes from extreme supply chain cost control. The advantage is rapid capital turnover without reliance on a few major clients; however, the drawback is that overall revenue must be supported by shipment volumes, and building/maintaining after-sales systems represents a long-term investment.

Yet Unitree has validated the viability of this approach, achieving a 60% gross margin and 600 million yuan in net profit (excluding non-recurring items) in 2025—a rare profitable example in the industry.

The second path is the 'Holistic Solution Model'. Companies like UBTECH, Dobot Technology, and RoboBusiness are the main players in this category. Their target customers are primarily automotive OEMs and large manufacturing enterprises. While these orders are substantial in value, they come with long delivery cycles, high levels of customization, and significant fluctuations in gross profit margins.

In other words, this is a traditional B2B business. The key to how far these companies can go lies in their ability to secure benchmark customers and replicate successful cases across more scenarios.

The third path is the 'Position-Based Subscription Service'. For this model to truly succeed, the economic calculations must work out. It requires robots to operate continuously in specific roles for a sufficient duration to amortize the initial investment. The core of this approach lies in deeply binding to specific scenarios, forming a long-term data feedback loop, and enabling robots to continuously create quantifiable and trackable value in their assigned roles.

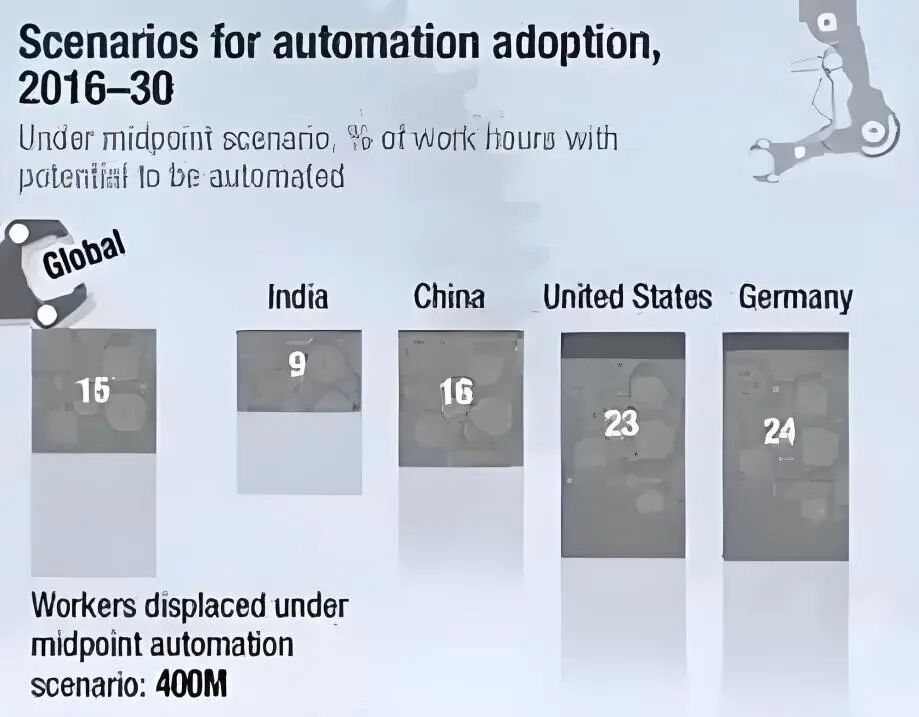

This is the much-feared issue of 'machines replacing humans,' but it also represents the most promising direction. Liberating human hands and improving efficiency have been fundamental themes of scientific development over the past few centuries. According to a recent report by the McKinsey Global Institute, by 2030, the global average ratio of labor replaced by robots is projected to be 15%. In developed countries like the United States and Germany, this ratio could reach as high as 23% and 24%, respectively. In other words, ordinary workers in developed countries will face a higher risk of being replaced by robots.

Image source: McKinsey

Of course, this 'elimination race' is not limited to humans; it is also unfolding within the robotics sector itself.

Data from Qichacha shows that as of May 13, 2026, there are 1,025 humanoid robot-related companies in China. As industry enthusiasm rises, the gap between winners and losers is widening dramatically.

According to the '2026 In-Depth Analysis Report on the Intelligent Robot Industry' released by China Investment Consulting, international robot manufacturers have already formed a distinct tiered landscape. The first tier, represented by UBTECH and ZhiYuan Robotics, is at the stage of technological leadership and commercialization initiation. The second tier, represented by Unitree Robotics and Fourier Intelligence, is at the stage of differentiated positioning and rapid catch-up. The third tier includes companies like LimX Dynamics, Xingdong Era, and RoboBusiness.

However, judging by the trajectory of the story, this elimination race is far from a simple case of 'industry infighting.' Robot companies must face off against larger, all-encompassing giants that already have foundational application scenarios, such as Tesla, which has algorithmic expertise and automotive manufacturing needs; Xiaomi, which has an ecosystem and application channels; and Foxconn, which possesses both robot production capacity and usage scenarios.

Peter Thiel's famous quote from 'Zero to One' sums it up perfectly: 'Competition is for losers.' The real winners do not engage in overt head-to-head battles; instead, they leverage their existing industrial foundations to launch dimensionality-reducing strikes from a higher vantage point.

As Professor Zhao Mingguo from the Department of Automation at Tsinghua University recently stated in a media interview, 'My judgment is that 2026 may be the year for filter (screening) application scenarios. Only by deeply embedding in scenarios and listening to market feedback can companies survive.'

-

AI Asset Spin-offs at Tech Giants: Is Kling Paving the Way for ByteDance and Alibaba?

-

![]()

Why Zhang Xue? Why HONOR?

-

![]()

Exclusive! Tencent’s ‘Tencent Drive’ with AI-Powered Asset Backup in the Works—A Game-Changing Move

-

![]()

Internal Upheaval in Initial Listing Days: SpaceX's AI Division Faces Accelerated Talent Loss, with 50+ R&D Staff Exiting in 2026

-

![]()

Price War Fails, Chinese Automakers Have No Retreat

-

![]()

Still in the Red but Outpacing Tesla: What Lies Behind SpaceX's $2.1 Trillion Valuation?

-

![]()

Humanoid Robots Go Global: From 'Actors' to 'Workers'

-

![]()

Still Incurring Losses Yet Outpacing Tesla: What Does SpaceX's $2.1 Trillion Valuation Signify?