Stop the Involution! Unusual Signs from Four Automakers

06/23 2026

06/23 2026

396

396

Introduction

The era of rapid, expansive growth in China's domestic new energy vehicle (NEV) industry is drawing to a close.

If one were to inquire about the bellwether of China's NEV sector, my vote would undoubtedly go to 'NIO, XPeng, Li Auto, and Leapmotor.' Having been established for over a decade, these companies have navigated through both triumphs and setbacks, embodying the evolution of China's NEV industry.

Over the past few years, China's NEV sector has followed a classic trajectory of linear growth: transitioning from fuel vehicles to electrification → advancing technology → reducing costs → expanding the market → achieving dominance.

New car manufacturers, leveraging the dual advantages of electrification and intelligent upgrades, could swiftly scale their market presence through continuous product innovation. However, this 'linear' path is now fracturing.

As the industry matures, the underlying competitive dynamics are undergoing a profound transformation. Persistent price wars, rampant product homogenization, and diminishing profit margins have emerged as the defining characteristics of the current market landscape.

The entire market is embroiled in fierce competition, yet struggles to generate profits or signs of sustainable growth.

Data reveals that from January to May, cumulative domestic passenger vehicle retail sales reached approximately 7.10 to 7.15 million units, marking a year-on-year decline of 19% to 19.5%. In May alone, retail sales stood at 1.51 million units, a 22.1% decrease from the previous year. It is no exaggeration to say that this impact extends beyond the NEV sector, affecting the entire automotive industry, including supply chains for power batteries, chips, and electric motors.

From the perspective of vehicle manufacturers (original equipment manufacturers), core technologies such as the three-electric systems (battery, motor, electric control), intelligent cockpits, and advanced driver-assistance systems (ADAS) have achieved near-universal adoption. The simple model of hardware stacking is losing its efficacy and can no longer establish enduring competitive barriers for enterprises.

When competition on the product front reaches its zenith, relying solely on the traditional business model of car manufacturing and sales is insufficient to sustain long-term enterprise development, making survival a formidable challenge. Thus, new questions arise:

In this low-margin, hyper-competitive phase of industrial development, can automotive companies afford to adhere solely to the 'pure car manufacturing' track and 'wait' for hope?

01 Li Auto and XPeng: Two Expressions of Intelligence and Technology

Faced with the new industry landscape characterized by diminishing industrial dividends and intensifying competition for existing markets, XPeng and Li Auto have responded in what could be considered the most 'aggressive' manner among the four new car-making forces. Both are betting on the transformative potential of technology and intelligence, albeit with significantly different approaches.

In early June, XPeng CEO He Xiaopeng issued an internal letter announcing his assumption of the CEO role for the robotics business, personally spearheading the advancement of related operations. He stated in the letter that this move represents not merely a business upgrade but a pivotal step in XPeng Group's transformation from a 'smart car company' to a 'physical AI company'.

Clearly, XPeng is leveraging technology to 'diversify outward,' thereby deploying a comprehensive terminal ecosystem for physical AI. Its objective is to transcend the automotive industry's boundaries and expand the long-term growth prospects for the enterprise through physical AI technology.

In XPeng's strategic vision, smart cars are no longer the endpoint of enterprise development. Their advantage lies in their high ceiling, effectively hedging against cyclical fluctuations in the automotive market and the relentless pressure of involution.

However, the shortcomings are equally pronounced. A parallel layout (deployment) across multiple sectors will continuously disperse R&D, financial, and human resources. How to achieve convergence and synergy across multiple businesses, ensure efficient technology implementation, and balance with commercial profitability are all core challenges XPeng must address next.

In contrast to XPeng's outward expansion, Li Auto leans more toward 'inward convergence'.

Five days after He Xiaopeng's internal letter, Li Auto further solidified its positioning at 'Livis Day,' showcasing its strengths in AI, software, hardware, and embodied intelligence technologies. It defined cars as 'embodied intelligent terminals,' emphasizing the deep integration of AI with the vehicle system.

Indeed, Li Auto is also delving into AI, embodied intelligence, and other technologies.

However, Li Auto has not embarked on side projects but has converged on the main body of 'embodied intelligent vehicles.' Relying on precise positioning for mid-to-high-end family users, a stable product iteration rhythm, and an integrated intelligent solution for the entire vehicle, it attempts to redefine the product attributes of the entire vehicle.

Admittedly, this focused strategy has brought Li Auto a clear commercial closed loop and stable profitability, helping it establish a firm foothold in the mid-to-high-end market amidst homogenization.

However, the highly focused scenario positioning also locks in the enterprise's growth boundaries; the bet on intelligent technologies requires time to take effect. Thus, as numerous automakers enter the home range extender and family intelligence sectors, Li Auto's exclusive scenario barriers are weakened, and pressure begins to mount.

02 NIO and Leapmotor: Different Paradigms of System and Efficiency

Of course, this does not imply that NIO and Leapmotor do not pursue intelligence or technology. Rather, it underscores that NIO's continuously demonstrated system capabilities and Leapmotor's high efficiency and low costs highlight their unique characteristics.

NIO's core is not just 'cars' but 'relationships' with users. It has constructed a comprehensive long-term system, encompassing battery swap networks, user communities, service systems, and brand identity. The essence of its business model is a long-term subscription model rather than a one-time transaction.

This asset-heavy, service-intensive operational model has enabled NIO to completely break free from the low-margin involution of the mid-range market. Leveraging stable brand premium and high user stickiness, it has built unique barriers in the high-end market.

However, the asset-heavy model also harbors inherent structural shortcomings. Continuous investment in battery swap infrastructure, offline service networks, and high-end operational systems has driven up fixed costs and operational pressures for the enterprise. This business model relies on sustained user payments, repurchases, and ecosystem consumption.

In response, NIO is not unprepared. The deployment of its second brands, Leo and Firefly, helps NIO achieve 'scale' goals more swiftly and further amortize the costs of system construction. Going forward, NIO only needs to focus on selling cars, maintaining product tone, and enhancing the value of its system capabilities to remain invincible.

In contrast, Leapmotor has adopted a distinct approach. It does not rely on grand narratives or boundary-pushing imaginations but continuously focuses on one thing: transforming cars into standardized industrial products.

With a background in Dahua, Zhu Jiangming, Leapmotor's founder, possesses a deep understanding of how to succeed in industrial manufacturing. Thus, Leapmotor has chosen the development path most aligned with physical manufacturing, leveraging extreme cost control, vertical integration, and scale efficiency. With robust industrial capabilities, it has transformed itself into a 'manufacturing efficiency model' capable of continuous cost optimization.

It is reported that 65% of Leapmotor's vehicle costs stem from core components that are self-developed and produced, with a target of reaching 80% by 2026; the self-research rate for the three-electric core components is 92%. Within the same platform models, the commonality rate of vehicle components is 88%; even across different platform models, the underlying electronics, software, and three-electric modules can be shared.

You see, Leapmotor's full-domain self-research and offering high-quality products at affordable prices have been pushed to the extreme under the 'manufacturing efficiency model.' Thanks to its sufficient focus on the mass-market segment, Leapmotor has maintained a stable delivery scale and cash flow level amidst fierce price wars.

This is the confidence behind Leapmotor's goal of 'selling one million units annually.' However, it should not be overlooked that extreme cost orientation makes it difficult to cultivate brand premium. In this regard, Leapmotor's upcoming second brand may be the key to breaking the mold!

03 What Will the Industry's Final Outcome Look Like?

A comprehensive analysis of the strategic layouts of the four new car-making forces reveals that, despite their vastly different development paths, the core logic of transformation is highly unified: to break free from the low-margin involution trap of traditional vehicle manufacturing and seek sustainable long-term growth logic by redefining corporate identities and iterating business models.

XPeng anchors technological boundary expansion, Li Auto delves deep into vertical scenario value, NIO operates a high-end user ecosystem, and Leapmotor pursues extreme industrial efficiency. There is no absolute superiority or inferiority among these four business models; they all represent strategic choices made by enterprises based on their unique genes amidst the industry's transformation cycle.

Currently, China's domestic NEV industry is still in a chaotic phase of dynamic transformation. AI technology iteration, the implementation of autonomous driving systems, the overseas market landscape, and enterprise profit models have not yet fully taken shape.

Thus, the harsh reality is that the current enterprise differentiation is merely a phased exploration of the NEV industry, not its final outcome.

However, one fact must be clear: the era of rapid, expansive growth in China's domestic NEV industry is indeed coming to an end; the new battle has already been initiated by NIO, XPeng, Li Auto, and Leapmotor.

In this brand-new transformation, enterprises that cling to traditional car-making thinking and rely on product involution and price wars will gradually be eliminated by the market. In contrast, those that actively break free from fixed operational models, redefine their core corporate identities, and build new business systems will become the new core players.

In other words, the future of the NEV industry may no longer feature traditional automotive companies in the purest sense. The long-term path forward for all automakers requires completing the iterative upgrade of their traditional car-making identities and achieving rebirth amidst the new cycle of AI technology and industrial transformation.

Editor-in-Chief: Shi Jie Editor: He Zengrong

THE END

-

![]()

When AI Dominates 618, Is Human Live Streaming the Ultimate Challenge?

-

![]()

Behind SpaceX's IPO: Musk, Boasting a Trillion-Dollar Net Worth, Still Grapples with a Severe 'Cash Crunch'

-

![]()

【OFweek Weike Cup】CASTECH Nominated for 2026 Optics Industry Outstanding Component Supplier

-

![]()

【OFweek Weike Cup】Accelink Technologies Competes for 2026 Outstanding Optical Component Supplier in Optical Industry

-

![]()

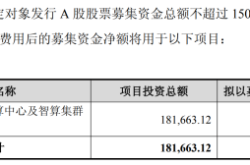

A Leading Computing Power Provider Secures 1.5 Billion Yuan in Private Placement, Expands Smart Computing Center to 12,000 Racks

-

![]()

【OFweek Weike Cup】Sundek Officially Enters for the 2026 Outstanding Contribution Award for Optical Industry Application Solutions

-

![]()

Geely's Three Strategic Cards for Future Layout Unveiled at Hong Kong Auto Show

-

![]()

GAC Toyota’s Sales Boom: Forging Vehicles with Enduring Value for the Long Haul