Xiaomi's Lost Trillion-Yuan Market Cap: All Picked Up by Zhipu

06/23 2026

06/23 2026

434

434

PART01 Carnival

166 days after its listing, Zhipu joined the trillion-yuan market cap club in Hong Kong stocks.

Previous regulars here include Tencent, Alibaba, HSBC, and five banks. Some visitors, such as CATL and Xiaomi, were once on the list but dropped out after a pullback. Among all residents and visitors, Zhipu is undoubtedly the youngest and least accessible to the public.

It is also the most controversial.

The keyword is bubble. In just over five months, Zhipu's stock price has surged more than 20 times compared to its IPO price, peaking at 25 times on today's (June 22) intraday high. Additionally, with revenue of only 700 million yuan in 2025 and substantial losses, even without a visible path to profitability, its market cap now equals 2 Xiaomis and 4 Baidus.

After the stock price continued to fall and lost public favor, Lei Jun, who would be ridiculed even for eating a bowl of noodles on the street, what reasoning could he possibly offer?

The pinnacle of celebrated joy once also befell Xiaomi and Lei Jun in June 2025. On the 27th, Xiaomi's intraday stock price exceeded HK$61, with its market cap once surpassing HK$1.5 trillion. Investors who profited fully embraced Xiaomi's narrative of a "human-vehicle-home ecosystem" and Lei Jun, who rose to fame through short videos.

But just a few months later, Lei Jun went from doing everything right to doing everything wrong. Currently, Xiaomi's market cap has evaporated HK$977 billion compared to its peak. By calculation, the trillion-yuan market cap Xiaomi lost has all gone to Zhipu.

The joys and sorrows of this world are indeed not shared.

The new energy track (translated as "sector" for clarity) where Lei Jun strives is a bloodbath.

The AI sector where Zhipu operates is a sea of bubbles.

Earlier this year, Bridgewater Associates founder Ray Dalio warned that the current AI bubble fervor has reached about 80% of the levels seen before the 1929 Great Depression or the 2000 dot-com bubble.

He spoke too soon and conservatively.

The scent of the AI bubble grew stronger in the first half of 2026. Over the past few months, fervent AI believers and speculators have banded together, repeatedly pushing Zhipu's stock price and price-to-sales (PS) ratio to new highs. The pattern of surging, retreating, surging again, and retreating again has left onlookers thrilled.

Based on the June 22 intraday peak stock price of HK$2,980, its PS ratio reached an all-time human high: 1,499 times. Before Zhipu, SpaceX, mocked as the biggest bubble in human history with a 150x PS ratio, can only call itself a younger brother now.

However, this was a pulsed surge, followed by a plunge. By the day's close, Zhipu's stock price fell back to HK$2,410, with a market cap of about HK$1.07 trillion.

Two weeks earlier, Zhipu's stock price also experienced a short-term halving. In the internet era, we talked about "30 turbulent years," but in the AI era, it has become "100 turbulent days," "24 turbulent hours," or even "10 turbulent minutes."

PART02 Absence

The frenetic surge is both a product of the times and Zhipu's proactive choice.

When OpenAI was hot, it told the story of "China's OpenAI." When Anthropic gained momentum, it switched to the narrative of "China's Anthropic."

The greatest convenience of being a follower is not having to strenuous (translated as "bother" for clarity) explaining to the capital markets.

Fortunately, whether in terms of B-end DNA or product ethos, Zhipu is closer to the latter, making this transition seem less abrupt. When Anthropic became the world's highest-valued AI company, Zhipu also reaped the benefits.

But no one knows where the inflection point of this frenetic surge lies—and it must be so. From a longer-term perspective, all surges are phased (translated as "phased" for clarity).

The first lock-up expiration in July may serve as a bellwether, though this round involves a limited proportion of shares, mostly held by state-owned shareholders, with unlikely significant reductions. The lock-up expiration in January 2027, involving over 60% of shares held by non-controlling shareholders, may truly reveal the market's true colors and test its resilience.

After the frenetic surge ends, Zhipu still needs a safety cushion, like the thick mats placed at climbing gym landing zones to ensure climbers descend safely from heights. Historically, many star companies saw their market caps plunge over 90% after bubbles burst, and only those landing safely had a chance to take off again.

Currently, Zhipu has technological leadership, government-enterprise relationships, Tsinghua-affiliated talent reserves, and some policy dividends, but these "safety cushions" are not thick enough.

A safety cushion capable of weathering a bubble burst could be business buffers—when the core business hits a bottleneck, other businesses can sustain the company; it could be cash flow—sufficiently strong internal or external funding; or it could be core resources—such as computing power, data, and clients that constitute a moat.

What about Zhipu?

Business buffers. Not enough.

A single (translated as "singular" for clarity) revenue structure is its longstanding issue. Local deployment is the absolute revenue mainstay, accounting for nearly 74% of 2025 revenue despite efforts to control it.

It is also accelerating efforts to increase the revenue share from cloud-based APIs, which offer higher profit margins but are relatively more unstable due to low user migration costs, making it easy for users to switch providers—akin to the always-fluctuating membership revenues of long-form video sites.

Cash flow. Not enough.

Zhipu's earnings lag far behind its spending: 2025 R&D expenditure was 3.18 billion yuan, 4.4 times annual revenue; adjusted net loss was 3.182 billion yuan, up 29.1% year-on-year. Once market confidence collapses, it will face a hard landing.

While OpenAI is expected to lose $14 billion in 2026, it boasts 900 million weekly active users, over 50 million paying users, and 9 million enterprise users, with ChatGPT becoming an operating system-like presence. Additionally, it has received over $13 billion in cumulative investment from Microsoft, $40 billion in financing led by SoftBank, and Oracle's participation in the Stargate project, forming deep ties with multiple giants.

Core resources. Not enough.

GLM has not become an irreplaceable underlying capability, and Zhipu remains just a startup with an ultra-high market cap, lacking a sufficiently deep moat. In contrast, Anthropic's Claude Code and other Agentic products are deeply embedded in the workflows of over 500 major companies, making users unable to leave.

If Zhipu is seen as a climber, its current situation is roughly this: the person has climbed Over ten meters (translated as "over ten meters" for clarity) up the rock face, but only a thin yoga mat awaits below. This won't prevent the climber from continuing upward but cannot catch a sudden fall.

Looking around, the climber also notices:

If OpenAI and Anthropic jump down, a host of major companies, big clients, and a massive user base will catch them;

If DeepSeek jumps down, fear not—its low-cost structure is inherently lightweight, and magic square (translated as "Fantasia Square" for clarity, though a proper noun may require verification) will catch it;

ByteDance, Alibaba, and Baidu need no mention—their large model products come with built-in "safety cushions" in their factory settings. In this AI competition, where the direction has become consensus, major firms will provide their core AI business units with a steady stream of talent, computing power, and as much patience as possible.

Thus, "bolstering the cushion" becomes a compulsory course (translated as "mandatory task" for clarity) for Zhipu, now a trillion-yuan market cap company.

While the joy of upward exploration is undeniable, only a safe landing completes the challenge and allows for the next ascent.

Currently, its best opportunity lies in infrastructure development. By leveraging technological advantages to make GLM a true infrastructure in certain industries and scenarios, Zhipu will gain a relatively robust "safety cushion."

What is indispensable holds the most value.

The "infrastructure route" has saved many companies before. After Amazon was "ambushed" by the dot-com bubble, its market cap evaporated by over 90%, but it later flourished again through AWS's infrastructure role.

However, a key cost is time. AWS took nine years from its 2006 launch to its first profit in 2015, relying entirely on Amazon's e-commerce business for support during that period.

For Zhipu, which lacks stable support, such a nine-year journey is clearly too expensive.

PART03 Essence

Zhipu may have one more special safety cushion.

Founder Tang Jie.

With Zhipu's stock price surge on June 22, Tang Jie's shareholding value once neared HK$80 billion. Yet, his public image remains that of a technical expert.

While internet companies busy themselves with "market cap management" and bosses seek fame, Tang Jie rarely makes public appearances.

He serves only as the company's chief scientist, not even standing at the center during the listing bell-ringing ceremony. His Weibo self-introduction lists only Tsinghua University professor and AMiner founder as his identities. AMiner is a big data mining system for scientific and technological intelligence led by Tang at Tsinghua's KEG team, with Zhipu chairman Liu Debing and CEO Zhang Peng as longstanding members.

A Zhipu employee once told me that Tang often remains "invisible" in client meetings but strictly oversees technical details, having once fired a frontline employee for a technical mistake he detected.

He is also highly low-key on social media. Apart from a recent discussion with Elon Musk on X about "when GLM-5.2 will reach Fable's level," he mostly gentle (translated as "gently" for clarity) promotes or explains technical issues without sharp edges.

Tang Jie's recent "friendly interaction" with Musk on X

In most cases, a founder directly shapes a company's style. Tang's low-key and technology-focused approach may help Zhipu avoid fatal errors, such as pursuing technical routes mismatched with its capabilities or over-marketing leading to user disappointment.

But this is also a double-edged sword.

Infrastructure development requires technology, government relations, ecological operation capabilities, and even more so, "ambition." Amazon's rise to a "behemoth" today stems from Bezos's pursuit of infinite expansion. If Tang's interest remains solely in research and technological academic achievement, his role as Zhipu's "safety cushion" must be reconsidered.

Tang's social media avatar is a front-facing photo with pure eyes, set against a backdrop of snow-capped mountains, lakes, and a cabin. Judging by the background, this is likely Wolfgang Lake in Salzburg, Austria, possibly taken during an early international academic conference on AI and data mining Tang attended there.

Tang Jie's Weibo homepage and self-introduction

Clearly, his avatar signals that he sees himself as a scientist, not a businessman or tycoon.

Now, it faces new tensions. The snow-capped mountains represent nearly a scientist's ideal world: quiet, distant, pure, and with clear boundaries, but the real AI sector is almost its opposite: crowded, noisy, complex, and full of variables every moment.

It seems, for now, the snow-capped mountains can only exist in Tang's dreams.

-

![]()

When AI Dominates 618, Is Human Live Streaming the Ultimate Challenge?

-

![]()

Behind SpaceX's IPO: Musk, Boasting a Trillion-Dollar Net Worth, Still Grapples with a Severe 'Cash Crunch'

-

![]()

【OFweek Weike Cup】CASTECH Nominated for 2026 Optics Industry Outstanding Component Supplier

-

![]()

【OFweek Weike Cup】Accelink Technologies Competes for 2026 Outstanding Optical Component Supplier in Optical Industry

-

![]()

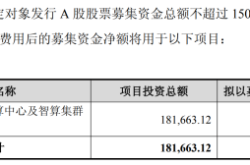

A Leading Computing Power Provider Secures 1.5 Billion Yuan in Private Placement, Expands Smart Computing Center to 12,000 Racks

-

![]()

【OFweek Weike Cup】Sundek Officially Enters for the 2026 Outstanding Contribution Award for Optical Industry Application Solutions

-

![]()

Geely's Three Strategic Cards for Future Layout Unveiled at Hong Kong Auto Show

-

![]()

GAC Toyota’s Sales Boom: Forging Vehicles with Enduring Value for the Long Haul