Industry Insights | Electronic Fabric Prices Double, Fueled by AI Demand as a ‘Critical Resource’

06/23 2026

06/23 2026

468

468

According to Wind data, early June 2026 saw the fifth price increase this year for commonly used electronic fabrics in the market, reaching an average price of 7.4 yuan per meter—a 100% rise from the low point in Q3 2025. As a key raw material for copper-clad laminates (CCLs), this price surge has seamlessly transferred to the CCL market. On June 16, Kingboard Laminates, a leading CCL manufacturer, announced its fifth price hike of the year, raising prices for all FR-4 CCLs and PP semi-cured sheets by 15%, just 20 days after its previous adjustment. Previously, price increases occurred every 24-30 days with hikes around 10%. This time, CCL prices rose more sharply and rapidly, with the announcement highlighting sustained price increases and tight supply of glass fabric as the direct causes.

Figure: Price of Standard 7628 Electronic Fabric (yuan/meter)

Data Source: Ping An Securities

Shifts in computing architecture are the main driver behind the surge in electronic fabric prices. According to Founder Securities, as of April, the price of AI-specific Low-Dk second-generation electronic fabric reached 160 yuan per meter—25 times that of standard 7628 fabric. Founder Securities notes that changes in computing architecture due to upgrades in AI server and switch speeds are transforming electronic fabric into a critical resource.

The global computing race demands certainty, supporting an industry cycle that far exceeds previous booms in electronic fabrics. TrendForce data indicates that global cloud giants such as Google and AWS are expected to spend $830 billion on capital expenditures in 2026, with a compound annual growth rate (CAGR) of 63.7% from 2023 to 2025. AI server shipments are projected to grow from 2 million units in 2024 to 6.5 million units in 2030. When AI server PCB layers increase from 10 in traditional servers to 16-24, electronic fabric usage per server becomes 3-8 times higher than in traditional servers, providing strong demand-side support.

Figure: Global AI Server Market Size

Data Source: Aj Securities

Capital market trends confirm the likelihood of a prolonged industry boom. Jujie Microfiber, a microfiber products company with revenue of just 577 million yuan in 2025, is investing up to 150 million yuan to purchase air-jet looms from Toyota and raising up to 1.1 billion yuan through a private placement to invest in high-end electronic fabric. Meanwhile, Jushi Group announced a 4.431 billion yuan investment to build a production line capable of producing 50,000 tons of electronic yarn and 320 million meters of electronic fabric annually.

With industry leaders expanding production, new entrants joining the market, accelerating prices, and constrained supply, electronic fabric is experiencing not just a typical price hike cycle but a transformation from a 'cost item' to a 'critical resource' driven by AI computing.

Prices Rise Sharply as AI Demand Intensifies

According to Founder Securities, from February to May, prices for 7628 electronic fabric increased by 0.5 yuan per month; in June, the increase expanded to 0.7 yuan, with monthly hikes rising from around 10% to even higher levels. Kingboard Laminates' price hike notices followed a similar pattern, previously raising prices by 10% every 24-31 days, but on June 16, the fifth round directly increased prices by 15% with the interval shortened to 20 days. Price increases are not only accelerating but also transmitting smoothly. From electronic fabric to CCL to PCB, the entire supply chain's price transmission has not faced obstacles but instead formed a 'CCL-electronic fabric price spiral' mechanism, as described by GF Securities.

However, data on product price tiers reveals deeper industry changes beyond the speed of price hikes. Founder Securities' survey shows that standard 7628 thick fabric is quoted at 6.2-6.5 yuan per meter, 2116 thin fabric at 7.6 yuan per meter, 1080 ultra-thin fabric at 7.9 yuan per meter, and AI-specific Low-Dk second-generation fabric at 160 yuan per meter. There are three price gaps: around 1.1 yuan per meter between standard and thin fabric, about 0.3 yuan per meter between thin and ultra-thin fabric, and approximately 152.1 yuan per meter between ultra-thin and AI-specific fabric. The closer to the AI core, the steeper the jump in added value. As Founder Securities judges, the electronic fabric product matrix has shifted from a single-layer pricing based on standard thick fabric to a steep premium curve defined by AI computing demand density. Sinolink Securities judges that 7628 fabric prices will rise 78% this year, with about 18% room left to reach the previous high of 8.75 yuan per meter in 2021, while Low-Dk second-generation fabric has already doubled this year. Different product tiers are in completely different price hike stages, which is the true meaning of 'transitioning from a cyclical product to a growth product' at the price level.

The Emergence of Critical Resources: Capacity Struggles to Keep Pace with Demand

Three factors limit electronic fabric capacity. The first is technological barriers. Shenwan Hongyuan believes that high-end electronic fabric capacity cannot be easily or quickly replicated. Producing specialty electronic fabric is highly challenging, with capacity difficult to duplicate. The main difficulties lie in: 1) the physical limits of front-end melting and drawing, requiring high-purity raw materials, high-temperature precision drawing, and control over ultra-fine monofilament strength and uniformity; 2) the equipment and process limits of back-end weaving, including the brittleness and tension control of quartz/ultra-fine yarns, delivery times and efficiency bottlenecks of high-end air-jet looms; and 3) post-treatment/surface chemistry and formula matching, including desizing damage control and treatment agent compatibility. Additionally, bottlenecks in loom equipment, high-purity quartz sand supply, crucible and furnace ramp-up, and stringent and lengthy customer certifications all limit the expansion pace of specialty electronic fabric.

The second factor is competition for loom capacity. Sinolink Securities believes that loom competition is the core micro-mechanism behind this round of supply tightness. AI specialty fabric, with the highest profitability, prioritizes the use of newly added Toyota JAT910 looms, with Toyota supplying a limited number of looms to the mainland each year; specialty fabric capacity expansion crowds out (displaces) ultra-thin and extremely thin fabric's existing looms; ultra-thin and extremely thin fabrics further displace 7628 thick fabric looms. This layered loom shortage limits the supply of all types of glass fabric, leading to a shortage across all categories. Founder Securities emphasizes that to secure high-margin AI orders, leading companies actively convert standard looms to produce high-end fabric, meaning the supply gap for standard fabric will further widen during the expansion period.

The third factor is the time required for new capacity to come online. According to Shenwan Hongyuan, capital expenditure growth for glass fabric companies was only 36% in Q1 2026, while growth in the CCL and PCB segments exceeded 100%. Downstream expansion is rapid, but upstream glass fabric is constrained by an 18-24 month equipment delivery cycle. Founder Securities also emphasizes that high-end loom delivery cycles are 18-24 months, with stringent and lengthy customer certification cycles.

Quartz Electronic Fabric: The Technological Path Forward for Electronic Fabric in the AI Era

Four factors support quartz electronic fabric becoming the physical inevitability for high-speed transmission in the AI era. The first is that the 224G transmission rate requirement eliminates traditional electronic fabric categories. According to Changjiang Securities, NVIDIA's Rubin architecture supports a 224Gbps transmission rate, and 224Gbps high-speed interconnect technology requires CCLs to reach the M9 level, which traditional electronic fabric cannot meet.

The second factor is the shift of bottlenecks from chips to PCB materials. Changjiang Securities believes that enhancing computing power is essentially about improving data transmission speed. While chip processes can continue to shrink to 1nm or 0.7nm, if PCB materials cannot upgrade synchronously, signal attenuation will physically limit computing efficiency.

The third factor is that quartz fabric offers the best engineering feasibility. Changjiang Securities analyzes that while PTFE's Df limit can reach 0.0001, it is 'difficult to process, soft, prone to deformation, has poor copper adhesion, and is costly.' Quartz fiber, with a Df of 0.0001 at 1MHz and a thermal expansion coefficient of just 0.55ppm/K, can use traditional PCB processes, maintaining structural stability and compatibility with the CCL system. Quartz fabric achieves an engineering balance of performance, process, and cost.

The fourth factor is that two application curves open up growth space for quartz fabric. Huajin Securities analyzes that in AI servers, NVIDIA's Rubin architecture defines quartz fabric as a core bottleneck material. When switch speeds increase to 1.6T, the electronic fabric's Df value should be less than 0.001, which ordinary low-dielectric glass fabric struggles to achieve, making quartz fabric a better solution. In consumer electronics, the iPhone 17 in 2025 will be the first to adopt LowCTE glass fabric for closed-body heat dissipation. If smart terminals gradually replace materials with LowCTE glass fabric, it could become another growth driver for LowCTE demand.

Two Fronts of Domestic Substitution

The global high-end electronic fabric market has long been dominated by Japanese manufacturers. According to Founder Securities, Japanese companies like Nitto Boseki and Asahi Kasei collectively hold over 70% of the high-end market share, with Taiwan's TaiGlass Group and Fujiho Industry forming the second tier. China's Jushi Group, International Composite Materials, Sinoma Science & Technology, Honghe Technology, Philly Quartz, and Linzhou Guangyuan are the pursuing group. Domestic substitution is advancing on three fronts.

Large-scale substitution: Jushi Group. According to Ping An Securities, Jushi Group ranks first globally in glass fiber capacity, with annual glass fiber yarn capacity exceeding 3 million tons, a 30% global market share and 40% of the Chinese market. The company plans to invest 4.431 billion yuan to build new capacity for 50,000 tons of electronic yarn and 320 million meters of electronic fabric, with a construction period of 1.5 years. Its net profit attributable to shareholders is expected to reach 6.223 billion yuan in 2026, up 89.4% YoY, with the gross margin jumping from 33.1% to 43.4%.

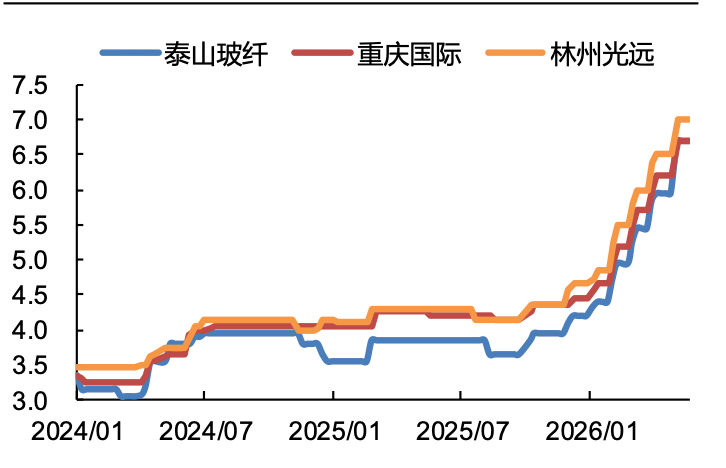

Technological substitution: International Composite Materials, Philly Quartz, and Taishan Fiberglass. Changjiang Securities analyzes that International Composite Materials leads domestically in Low-Dk second-generation fabric shipments, with excellent yield and stability, deep strategic cooperation with domestic CCL leaders, and full benefits from the NVIDIA supply chain, increasing its domestic market share. Philly Quartz targets Japanese monopolies in M9-grade substrate materials with its quartz fabric. Taishan Fiberglass is the domestic leader in Low-Dk fabric, the only one achieving full coverage of three generations, with its second-generation product featuring Dk 3.7 and Df 0.0007, approaching Nitto Boseki's performance.

Industry profit realization data provides fundamental support. According to Zhongtai Securities and TF Securities, in 2025, sample glass fiber companies' net profit excluding non-recurring items grew 127% YoY, with Q1 2026 growth at 70.9% YoY and full-industry net profit surging 72% YoY in Q1 2026.

Research Report Sources:

1. Changjiang Securities' 'How to View Quartz Electronic Fabric at This Juncture?'

2. Huajin Securities' 'How to View the Explosive Demand for Electronic Fabric Driven by AI Infrastructure Upgrades?'

3. East Money Securities' 'Electronic Fabric Prices Rise Again, Q1 2026 Consumption Building Materials Turn Upward'

4. Huayuan Securities' 'Jujie Microfiber: Profitability Improves Quarter-on-Quarter, Electronic Fabric Business Opens Growth Space'

5. Founder Securities' 'Electronic Fabric: The Key PCB Substrate in the Computing Era, Transitioning from a Cyclical to a Growth Product'

THE END

Copyright and Disclaimer

1. Content Copyright: Except for quoted public data, policies, and cases, all content is original. Professional data is sourced from authorized databases and government websites, with cases compiled from real events.

2. Image Licensing: Some images are proprietary or officially licensed, with others AI-generated; for network images with unclear copyright, ownership remains with the original authors, and unauthorized images will be removed upon notification.

3. Reprint Guidelines: Unauthorized reprinting is prohibited; reprints must retain the full source and author.

4. Liability Disclaimer: This article is a commercial observation and industry commentary compiled by the author based on public information. Content is for reference only and does not constitute professional advice. Risks arising from use are borne by the user. The Industrial Internet Alliance reserves the final interpretation rights.

-

![]()

Over 50% of Revenue Hinges on Yutong Optics! This Optical Equipment Manufacturer is Charging Towards an IPO

-

![]()

YOCO Optics Finalizes Industrial and Commercial Registration Update Post 160 Million Yuan Investment in Jiangfeng Biology, Securing 20% Stake to Emerge as Second-Largest Shareholder!

-

![]()

Google Market Value Plummets by $1.5 Trillion Overnight Following the Loss of Two Key Figures

-

![]()

Put an End to the EV 'Weight Gain Race'! Can Your Car Still Be Driven Under the New National Standards?

-

![]()

In 2026, 'AI Upstarts' Collectively Bet on World Models

-

![]()

【OFweek Weike Cup】Phoenix Optics Officially Participates in the 2026 Optical Industry Annual Innovation Product Award

-

![]()

Ford Ditches Mach-E: Will Its Billion-Dollar Electrification Drive Have to Start All Over Again?

-

![]()

【OFweek Weike Cup】Shuangli Hepu Officially Participates in the 2026 High-Growth Enterprise Award in the Optical Industry