Alipay Builds a City, JD.com Paves the Road, WeChat Guards the Gate: The Three-Way Battle of AI Payments

06/23 2026

06/23 2026

520

520

Authorization is harder than payment, and trust is scarcer than technology.

AI payment is not a product of impulsive decision-making by major companies, not a meaningless battle for entry points, and certainly not a "pseudo-demand" that users do not need. It is an infrastructure upgrade driven by both technology and user habits, marking an inevitable evolution in the payment industry from "transaction processing" to "intelligent services."

Of course, it is still imperfect today. There will be security issues, limitations in scenarios, and competition among major companies.

But if we criticize it for its imperfections, we may miss out on an era where payments truly become "seamless."

Advancing AI to Complete the "Last Mile" of Transactions

Recently, WeChat, Alipay, JD.com, and UnionPay have intensively launched AI payment products, prompting many to ask: Are the major companies competing in payments again? However, a closer look reveals that these products are not even in the same race.

Alipay addresses how AI can truly complete tasks. WeChat focuses on how AI can spend money safely on behalf of users. JD.com tackles the issue of accountability when AI makes incorrect payments. UnionPay ensures how AI can integrate into existing payment networks and gain trust.

Overseas, Visa, Mastercard, and Stripe are vying for the underlying protocols and infrastructure of future intelligent agent commerce.

While they all appear to be working on AI payments, they are actually filling different gaps in the transaction chain of the Agent era.

Alipay is the most aggressive. According to LatePost, Alipay initiated the "Bao Plan" internally in the second half of 2023 to explore intelligent transformation. In September 2024, it launched the standalone app "Zhixiaobao," but its impact remained limited due to fragmented access. By March 2025, the team made a crucial adjustment, abandoning the standalone app route and returning to the main Alipay app.

The key judgment behind this shift is that AI should not become a new entry point outside the payment system but should be an integral part of the payment system itself.

Abao, launched in June this year, is a brand-new AI interface connected to Alipay's long-accumulated service network.

On the one hand, Alipay is promoting the opening of MCP interfaces to enable merchants' services to be directly invoked by AI. On the other hand, it ensures compatibility with mini-programs and service ecosystems that have not yet been upgraded through screen-reading operations.

Abao attempts to enable AI to complete a full closed loop from demand understanding to service invocation and then to payment settlement.

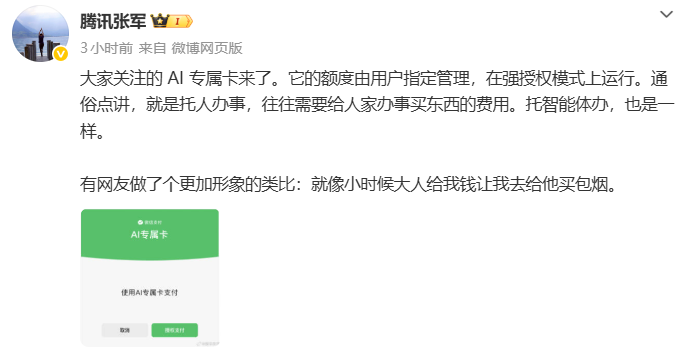

Compared to Alipay's reconstruction of underlying infrastructure, WeChat is more concerned with how to grant intelligent agents limited spending capabilities while ensuring security.

In early June, WeChat opened its AI platform, with Meituan, JD.com, Didi, and Ctrip among the first to integrate. Subsequently, WeChat Pay integrated with Tencent's self-developed desktop intelligent agent, WorkBuddy.

Users can make requests to the AI on their PC, such as finding nearby group-buying deals. The intelligent agent completes recommendations, filtering, and ordering, while the payment is confirmed via the mobile app.

The entire process seems simple but hides WeChat's most important design principle: enabling AI to spend money, but not recklessly.

Currently, AI-exclusive cards adopt an independent authorization mechanism. First-time use requires binding an account and authorizing payment capabilities, with strict limits on spending scope and amounts.

It first completes full verification of "recommendation, decision-making, payment, and redemption" in closed scenarios, addressing how AI can pay securely.

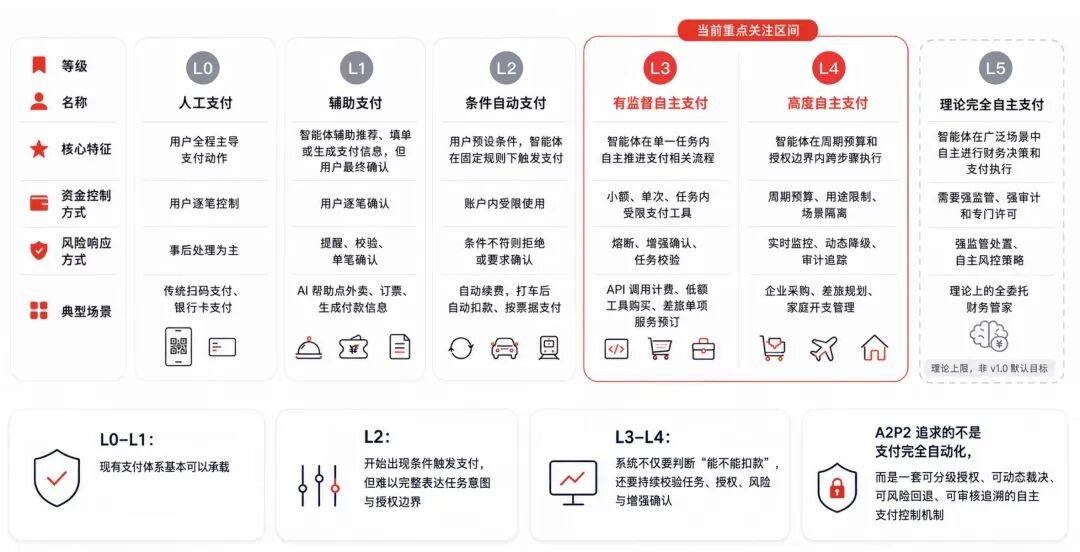

JD.com takes a longer-term view, considering how responsibility should be divided when AI starts spending on behalf of users, leading to mispurchases, overspending, or even fraud. JD.com proposes the A2P2 (Agent to Payment Protocol), outlining a six-level autonomous payment system from L0 to L5, along with task delegation credentials and ARI identity authentication mechanisms. JD.com aims to establish a standard framework describing AI spending permissions, responsibility attribution, and risk boundaries.

Compared to Alipay and WeChat, which directly target users, JD.com is more like paving the road.

UnionPay and UnionPay Commerce are upgrading traditional merchant acquiring systems into transaction networks that AI can directly invoke. In April this year, China UnionPay released the Agent Payment Open Protocol (APOP) framework and completed multiple real transaction verifications. From booking flights and hotels to purchasing coffee via in-car assistants, APOP addresses how intelligent agents can gain trust in payment networks.

Who is the user? Who is the intelligent agent? Who initiated the payment? Is the payment consistent with the user's intent? These questions require a new trust mechanism to answer.

UnionPay Commerce further extends these capabilities to real-world commercial scenarios such as campus meal ordering and utility bill payments. If UnionPay sets the rules, UnionPay Commerce verifies them.

Looking overseas, similar developments are occurring simultaneously. Mastercard launched Agent Pay, Visa released the Trusted Agent Protocol, Stripe began building payment capabilities for AI agents, and Google collaborated with industry partners to promote the Agent Payments Protocol.

Almost all global payment giants are striving to establish new transaction infrastructures for the AI era. They recognize that when AI starts performing tasks on behalf of users, payment is no longer just the final step of a transaction but a key link for intelligent agents to gain actionable capabilities.

In this light, the term "AI payment" itself is inaccurate. Alipay reconstructs service networks, WeChat verifies consumption closed loops, JD.com formulates responsibility frameworks, UnionPay establishes trust rules, while Visa and Mastercard compete for global protocol standards.

They all start from different points but converge on the same question: After AI performs tasks on behalf of humans, can it spend money safely and trustworthily?

Why Now?

AI large models have been popular for three years, and mobile payments have been widespread for over a decade. Why have they suddenly become a hot topic for all giants?

The answer lies in the transformation of AI's role.

Previously, large models operated on a "you ask, I answer" basis. No matter how capable, they remained at the information level, not handling money or tasks. But in the Agent era, AI starts booking tickets, ordering food, hailing rides, and reserving hotels. AI transitions from "talking" to "acting," and the next step after acting is spending money.

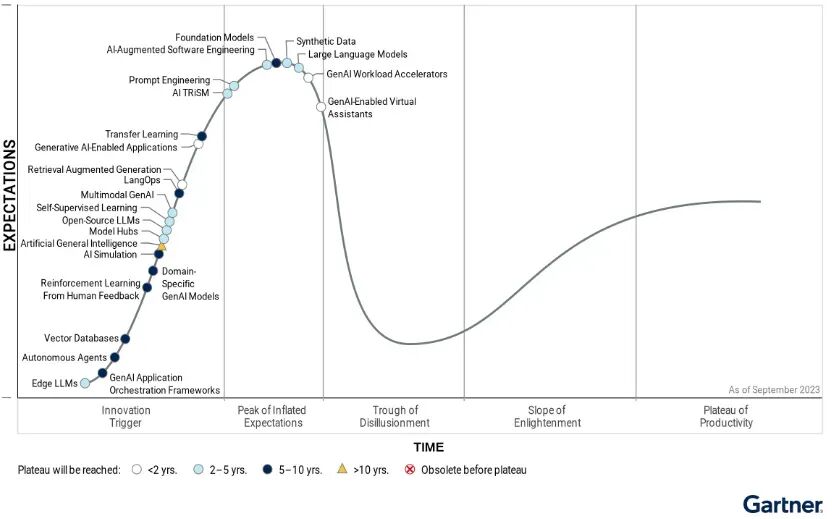

The technological turning point is first evident. Gartner predicts that by 2026, over 80% of enterprises will use generative AI (GenAI) application programming interfaces (APIs) or models or deploy GenAI-supported applications in production environments, up from less than 5% in 2023.

IDC data shows that the global number of active AI agents is expected to grow rapidly from about 28.6 million in 2025 to 2.216 billion in 2030, an nearly 80-fold increase in five years.

These numbers sound grand, but in the specific context of payments, they boil down to one sentence: AI can not only help you find information but also make decisions for you.

From QR code payments in 2011 to facial recognition payments in 2018, palm payments in 2023, NFC taps in 2024, and glance-to-pay in 2025, payment methods have continuously evolved to seek more seamless interaction forms.

However, the fundamental difference between AI payments and previous iterations is that QR codes, facial recognition, and NFC optimize how humans complete payments, while AI payments redefine who decides to pay.

The former enhances interaction efficiency; the latter shifts the decision-making main body .

Mastercard explicitly lists AI-driven agent commerce as the top global payment trend in its 2026 Trend Report, arguing that this is not a side feature but a fundamental shift where AI agents, not humans, initiate and complete transactions.

Moreover, mobile payments themselves have limited growth potential, with users and markets reaching a ceiling.

iResearch data shows that China's personal mobile payment market reached RMB 205.2 trillion in 2024 but is expected to decline by 3.7% year-on-year to RMB 197.5 trillion in 2025, with transaction volume growth at only 1.1%. High-frequency scenarios like offline micro-businesses and life services are already fully penetrated. In other words, QR code payments have peaked, and it's time to explore new avenues.

The maturity of user habits is another driving force. During the 2026 Spring Festival, major companies invested over RMB 4.5 billion in red envelopes and subsidies to acquire new users and educate them on using AI assistants. This RMB 4.5 billion was not for payments but for capturing user intent. Users have become accustomed to booking tickets, ordering food, finding guides, and grabbing red envelopes by chatting with AI.

When users are already comfortable expressing needs to AI, letting it pay on their behalf faces much less psychological resistance than a year or two ago.

The final driving factor comes from regulations. Many assume major companies are rushing ahead of regulations. Quite the opposite. The dense release of AI payment products this round indicates that the industry recognizes the need to establish rules before scaling .

JD.com's A2P2 grading system, Alipay's Token Pay, WeChat's AI-exclusive cards, and UnionPay's APOP protocol address questions like how much AI can spend, in what scenarios, and who is responsible if issues arise.

These products may seem to open up payment capabilities, but they actually impose increasing constraints. Amount limits, whitelists, pre-authorizations, identity verifications, and risk gradings—all participants are trying to erect layers of guardrails around AI.

Payment has never been a purely technical issue; trust is the core.

Returning to the original question: Why now? Because AI has gained actionable capabilities for the first time, moving from answering questions to completing tasks. Users have also, for the first time on a large scale, become accustomed to expressing needs in natural language and delegating more tasks to AI.

Meanwhile, mobile payments have matured, and the payment industry needs new growth spaces. The rule frameworks surrounding intelligent agent payments are also moving from conceptual discussions to real-world verification.

When technology, demand, market, and regulations all reach a tipping point, the emergence of AI payments is no longer a choice but an inevitability.

Don't Be Too Critical of AI Payments

Over the past decade, the payment industry has focused on making it easier for humans to complete payments. From online banking to QR codes, from facial recognition to NFC taps, each innovation optimized the payment action itself.

AI payments, however, aim to address how money should be spent when AI starts completing tasks on behalf of humans.

If speed were the only goal, NFC taps would suffice. Alipay's tap-to-pay had already covered over 400 cities nationwide by 2025, with over 10 million merchants and over 100 million users. The true value of AI payments lies in transforming payments from a tool into a service.

Previously, your payment action was the goal; now, it is merely the result.

Imagine a scenario: You tell WeChat AI to book a high-speed train ticket to Shanghai tomorrow morning, preferably not too expensive. The AI invokes Ctrip, compares prices, selects seats, and completes the payment—all without you needing to open the Ctrip app, repeatedly confirm amounts, or manually enter passwords (within your preset limits and rules). The core value of this experience is not having to manage it, shifting from "people seeking services" to "services finding people."

In Alipay's context, this logic goes a step further. You tell Abao to check your investment returns this month. The AI not only completes the query but also offers suggestions based on your historical data and risk preferences: "Your monthly fixed investment outperformed peers, but your bond allocation is relatively high . Would you like to adjust?"

This "payment plus insight" experience cannot be provided by simple QR codes.

Today, the commercial significance of this transformation has already been validated in the B2B sector. Gartner predicts that by 2028, 90% of B2B procurement will be completed through AI agent intermediaries, involving over USD 15 trillion in spending. McKinsey's estimates are even more aggressive: by 2030, intelligent agent commerce coordination revenue in the U.S. B2C retail market alone could reach USD 1 trillion, with the global market size reaching USD 3-5 trillion.

When Agents can independently complete transactions and settle accounts among themselves, the entry logic of the traditional internet will be completely restructured.

This logic also holds true on the consumer side, though it manifests in more everyday forms and is less noticeable. But just because you don't perceive changes doesn't mean they aren't happening.

Of course, these scenarios are not yet perfect today. AI payments currently cover only small-value, standardized, and high-frequency transactions. For large transfers or complex financial decisions, AI still dares not—and cannot—make final decisions on your behalf. However, it is precisely because things are imperfect today that continuous investment, iteration, and standardization are needed, rather than harsh criticism.

When Alipay was launched in 2004, online transactions still required bank transfers. When QR code payments emerged in 2011, many people thought they were unnecessary—after all, online banking was already sufficient.

WeChat's AI scheduling center leverages its social ecosystem with 1.47 billion monthly active users, while Alipay relies on the depth of financial services for its 1.04 billion monthly active users. JD.com is attempting to establish industry standards with A2P2, while overseas players like Stripe and Mastercard are vying for global infrastructure. What they are competing for is whose ecosystem can more comprehensively meet your needs when AI becomes the entry point.

Ultimately, this competition will translate into lower prices, more precise recommendations, and a seamless experience. Ordinary people don't need to understand AI payments—they just need to enjoy the convenience they bring.

Another often-overlooked aspect is the friendliness of AI payments to digitally vulnerable groups. Voice interaction, natural language commands, and automated execution can enable visually impaired individuals, the elderly, and those unfamiliar with smartphone operations to regain payment capabilities, which they might have been excluded from due to digital payment barriers.

According to data from the People's Bank of China, as of the end of 2024, there were still approximately 280 million elderly people and over 17 million visually impaired individuals in China. For them, the process of QR code payments—finding an app, opening the scanner, aligning the code, and confirming the amount—is not much simpler than cash payments.

The interaction logic of AI payments is: speak, confirm, and complete. This is the essence of inclusive payments. You might think scanning a code is simple, but for the elderly, speaking is a hundred times easier than scanning.

Many also worry that letting AI handle spending could lead to loss of control, but the opposite is true. While this may sound counterintuitive, AI payment designs actually give users finer-grained control. In traditional payments, your authorization is often one-time and coarse-grained—binding a card or enabling password-free payments means the platform can continuously deduct funds within agreed limits.

However, in AI payment designs, users must authorize each agent separately, set spending limits, and can revoke permissions at any time.

This distributed authorization design is theoretically more secure than traditional payments because it shifts risk control from 'post-event remediation' to 'pre-event authorization,' giving each transaction clearer boundaries.

But as authorization becomes more granular, a new question arises: How well must AI understand you to complete a transaction on your behalf?

Take JD.com's A2P2 task authorization credentials as an example. They were originally designed to address liability issues. The system not only records 'what was bought' but also 'why it was bought,' 'on whose behalf,' and 'in what context.'

From a payment security perspective, this is necessary. Only by understanding user intent can the system determine whether the agent accurately executed the authorization.

However, this leads to a chain reaction of 'overexposure.' A medication order may record not just the purchase but also family health needs; a birthday cake order may reveal not just the transaction but also a relationship and an important moment. With mobile payments, platforms hold transaction data; in the AI payment era, platforms have access to intent data.

This information may not be actively used by platforms, but for the first time, it enters the transaction system in a structured form. The question then arises: When AI not only knows what you bought but also begins to understand why you bought it, where should the boundary between humans and systems be drawn?

Today, this change not only affects users but also transforms merchants and the entire acquiring industry. In the past, the core action for acquiring institutions was merchant onboarding—verifying merchant identity, business operations, and settlement accounts. Once approved, merchants gained payment acceptance capabilities.

For agent payments, merchant onboarding alone is insufficient. For AI to assist users in completing transactions, it must know what merchants sell, their prices, inventory levels, how to apply discounts, how orders are generated, and how refunds and after-sales are handled. Thus, agent payments may drive the acquiring industry beyond merchant onboarding to include product onboarding, order onboarding, and transaction capability onboarding.

UnionPay Business's MCP Server, public product library, and order capabilities are all responses to this change.

In the future, when you tell AI to buy breakfast, it will not only need to know which stores are open but also what buns they offer, their prices, and how many are left. Without an AI-understandable product library, truly implementable agent payments cannot exist.

Payment institutions will not only process payments in the future but also begin organizing transactions. This change is fundamental and will have far-reaching impacts.

Conclusion

AI payments are not impulsive products from tech giants, not meaningless entry-point battles, and certainly not 'pseudo-needs' that users don't want. They represent an infrastructure upgrade driven by both technology and user habits, an inevitable evolution of the payment industry from 'transaction processing' to 'intelligent services.'

Of course, they are still imperfect today. There will be security issues, scenario limitations, and competition among tech giants. But if we criticize them for their imperfections, we may miss an era where payments truly become 'effortless.'

Today's caution is not cowardice. Rather than rushing to debate whether AI payments will replace QR code payments, we should first consider how much power you are willing to delegate to AI as it increasingly understands and makes decisions for you.

This is why all participants proceed with restraint—they know they are building not just a new payment system but also a new order of trust, authorization, and responsibility.

The broader the scope, the more important it is to take root step by step. What must be held steady is not just technology but also the courage to entrust. Such steadiness is the most profound form of progress.

Editor: Muren Reviewer: Zhang Wenxin Producer: Rui Zong

-

![]()

Over 50% of Revenue Hinges on Yutong Optics! This Optical Equipment Manufacturer is Charging Towards an IPO

-

![]()

YOCO Optics Finalizes Industrial and Commercial Registration Update Post 160 Million Yuan Investment in Jiangfeng Biology, Securing 20% Stake to Emerge as Second-Largest Shareholder!

-

![]()

Google Market Value Plummets by $1.5 Trillion Overnight Following the Loss of Two Key Figures

-

![]()

Put an End to the EV 'Weight Gain Race'! Can Your Car Still Be Driven Under the New National Standards?

-

![]()

In 2026, 'AI Upstarts' Collectively Bet on World Models

-

![]()

【OFweek Weike Cup】Phoenix Optics Officially Participates in the 2026 Optical Industry Annual Innovation Product Award

-

![]()

Ford Ditches Mach-E: Will Its Billion-Dollar Electrification Drive Have to Start All Over Again?

-

![]()

【OFweek Weike Cup】Shuangli Hepu Officially Participates in the 2026 High-Growth Enterprise Award in the Optical Industry