Trillion-Yuan Zhipu: A Fleeting Capital Sentiment or an Early Pricing of the Ultimate Market for General AI Infrastructure?

06/23 2026

06/23 2026

516

516

Editor's Note:

In June 2026, Zhipu's market capitalization exceeded HK$1.07 trillion during trading, surging over 19-fold in the six months since its listing. On one hand, there is the financial reality of just RMB 724 million in annual revenue and a net loss of RMB 4.718 billion. On the other hand, there is a capital valuation comparable to internet giants, sparking a fierce debate across primary and secondary markets regarding the valuation of domestic large models. Some claim this is a thematic bubble detached from fundamentals, echoing the internet frenzy of two decades ago. Others assert that the trillion-yuan market cap marks the official starting point of the general artificial intelligence industry cycle.

Amid the controversy, the market tends to simply compare Zhipu to the former 'AI Four Little Dragons,' overlooking its unique three-tiered competitive barriers: Tsinghua-affiliated native technology foundation, high-stickiness government and enterprise cash flow foundation, and rapidly expanding open-source ecosystem foundation. Setting aside emotional narratives, dissecting the true moat behind the trillion-yuan valuation answers the core question: Is the high valuation a capital bubble or an early realization of long-term industrial value?

Tsinghua's Technical Talent: 452 Shareholding Employees Build an Irreplicable R&D Foundation

It is widely acknowledged in the industry that the most difficult long-term barrier for companies to replicate is a stable scientific research talent system that competitors would struggle to establish even with a decade of effort and billions in investment. In the realm of general large models, this precisely highlights Zhipu's core foundation—distinguishing it from most AI companies. Its technical genes, nurtured in Tsinghua University's KEG Knowledge Engineering Lab, combined with a company-wide employee shareholding mechanism covering half of its staff, jointly establish an industry-hard-to-replicate talent barrier.

Most AI startups in the market temporarily assemble their R&D teams with high salaries, experiencing a core talent turnover rate exceeding 30% annually. In contrast, Zhipu has been tied to Tsinghua's NLP field since its inception, benefiting from over a decade of accumulated scientific research expertise. Co-founder Professor Tang Jie, a fellow of IEEE, ACM, and AAAI and the original architect of the GLM large model, leads a team deeply engaged in knowledge graphs and pre-trained models for over ten years. In 2022, they launched China's first open-source large model with hundreds of billions of parameters, positioning themselves at the forefront of domestic foundation models. Unlike the outsourced R&D approaches of large corporations or the commercial focus of companies prioritizing implementation over foundational research, Zhipu naturally retains a long-termist R&D logic from the lab, investing over 400% of its annual revenue into R&D (2025 data), with R&D expenditures reaching RMB 3.18 billion in 2025, all directed towards foundational model iteration and self-developed computing frameworks, without chasing short-term To C traffic gimmicks.

More crucial than technical pedigree is a shareholding system that binds core R&D personnel. According to Zhipu's Hong Kong IPO prospectus, as of late June 2025, the company employed 883 people, with 452 holding shares through two major shareholding platforms, Huihui and Zhideng, accounting for 51.2% of total employees. These two platforms collectively hold nearly 15% of the company's equity. Breaking down the data, the Huihui platform accommodates 426 mid-level researchers and engineers, while Zhideng focuses on 25 core scientific research executives. Based on a trillion-yuan market cap, ordinary shareholding employees generally hold paper assets worth tens of millions, with core R&D personnel exceeding HK$200 million each.

In contrast, some traditional AI companies concentrate equity among founding teams before listing, leaving grassroots R&D personnel largely excluded from equity incentives. Frequent industry layoffs and salary cuts lead to ongoing talent attrition. Zhipu's mechanism of 'shared prosperity for all researchers' addresses the large model industry's biggest pain point—the scarcity and high turnover cost of top algorithm talent. The AI industry is fundamentally intelligence-intensive; GPU computing power can be procured, and industry projects can be replicated, but a stable R&D team deeply engaged in foundational models for a decade and committed to the company's long-term development cannot be hastily assembled with money.

In essence, while computing power can be procured in bulk and algorithms quickly replicated, a decade-old scientific research echelon (Chinese term meaning 'echelon' or 'tier') and a talent mechanism binding interests represent a technological moat that capital cannot rapidly construct.

Government and Enterprise Service Commercialization: Stable Cash Flow Hedging Against Industry Loss Cycles

The core argument against Zhipu's trillion-yuan valuation in capital markets always revolves around a stark contrast: annual revenue of RMB 724 million, net losses of RMB 4.718 billion, and a price-to-sales ratio exceeding 500 times, far surpassing overseas leading large model companies in the same period. However, dismissing value based solely on losses fundamentally confuses the valuation logic of traditional software companies with that of general large model enterprises.

An AI company recorded RMB 5.015 billion in annual revenue in 2025, nearly seven times Zhipu's volume its, yet market cap stood at just HK$71.7 billion, less than a tenth of Zhipu's. The core issue lies in its business structure's inherent flaws: early bets on fragmented smart city and security projects led to long delivery cycles, low renewal rates, scattered clients with weak data security demands, and a lack of stable cash flow to support its later transition to general large models, resulting in years of large negative operating cash flow. In contrast, Zhipu targeted high-value clients such as central SOEs, finance, energy, and government sectors from its inception, adopting a 'dual-wheel approach' of 'private localized deployment as the foundation and cloud-based MaaS for rapid scaling,' forming an industry-unique stable cash foundation.

Authoritative 2025 annual report data shows Zhipu's total revenue at RMB 724 million, with localized government and enterprise deployment contributing RMB 534 million (73.7% of total revenue), serving over 12,000 enterprise institutions. Government and enterprise clients boast a project renewal rate as high as 95%. Industries like government and finance have stringent policy requirements for local data storage and autonomy, naturally rejecting internet public cloud large models. Leveraging Tsinghua's academic endorsement and compliant implementation experience, Zhipu firmly occupies the core share of the domestic government and enterprise large model sector. Although this business involves heavy delivery and lower gross margins, its stable payment collection and predictable orders serve as a 'cash flow ballast' for the company's sustained high-cost R&D investments.

An even more critical second growth curve is the explosive growth of cloud-based MaaS (Model as a Service) business. Financial reports disclose that MaaS deployment revenue reached RMB 190 million in 2025, soaring by 292.6% year-on-year—more than double the overall revenue growth rate of 131.9% (36Kr). The MaaS platform's annual recurring revenue (ARR) hit RMB 1.7 billion, a 60-fold increase year-on-year. Even after proactively raising API call prices by 30% and eliminating first-purchase discounts in early 2026, paid subscription packages still sold out immediately upon release, with the paid developer base surpassing 242,000, showcasing a typical 'volume and price surge' pattern of supply scarcity.

This model of 'locking cash flow through government and enterprise privatization while earning scalable increments via cloud-based MaaS' perfectly avoids the two fatal flaws of traditional AI companies: first, it does not rely solely on scattered custom projects, as MaaS cloud services enjoy declining marginal costs and internet-platform-like scaling compounding effects; second, high-stickiness government and enterprise orders offset industry cycle fluctuations, eliminating the need for continuous reliance on financing to sustain R&D. While peers still depend on financing to fill operational gaps, Zhipu has achieved a mature business stratification: short-term stability through government and enterprise privatization, and medium-to-long-term growth via the MaaS developer ecosystem, opening up hundred-fold growth potential.

While traditional AI remains trapped in 'project-based internal competition,' Zhipu breaks free, using government and enterprise cash flow to support R&D and relying on the MaaS platform to deliver scale effects. This is the commercialization moat hidden beneath the surface of losses.

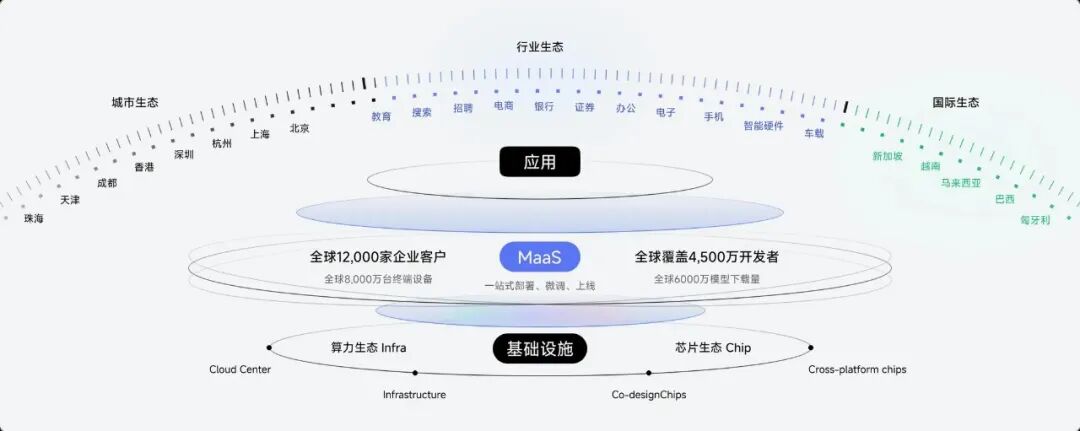

Open-Source Ecosystem: 3 Million Developers Building an Industry-Unique Network Effect Moat

Metcalfe's Law states that the value of a network is proportional to the square of its user base. In the general large model track (Chinese term meaning 'track' or 'arena'), the open-source ecosystem determines the ultimate long-term victory, and Zhipu, with a community of nearly 3 million registered developers, has established China's most complete foundational model open-source ecosystem, forming an insurmountable network effect moat for other players.

Many investors focus solely on revenue and market cap figures, underestimating the long-term value of open-source ecosystems: the large model industry ultimately hinges not on a single vendor's solo efforts but on ecosystem competition involving foundational models, industry developers, and end enterprises. Internet giants largely rely on their proprietary cloud businesses, confining developers to their own cloud ecosystems. Overseas, OpenAI's closed-source strategy raises industry usage barriers. In contrast, Zhipu has adhered to a permanent open-source approach for foundational models since the GLM's initial iteration, forging a virtuous cycle of 'openness attracting developers, who in turn feed model iteration.'

As of Q1 2026, Zhipu's MaaS platform registered over 3 million developers across 218 countries and regions, with cumulative global downloads of open-source models exceeding 45 million. Nine of China's top ten internet companies have integrated GLM series models for secondary development, while countless small-to-medium software vendors and independent developers have built industry-specific large models and intelligent agent tools based on open-source GLM.

The logic of the ecosystem flywheel is clear and irreversible: the more developers use open-source GLM, the more they continuously feed back industry scenario defects and provide fine-tuning data, driving model iteration and optimization. Stronger model capabilities attract more enterprises and developers to the platform, with API call volumes climbing and MaaS revenue growing in tandem. Zhipu's open-source strategy freely provides tools to the entire industry, exchanging openness for scale networks. Once the ecosystem forms, customer migration costs become prohibitively high—after building entire business systems based on GLM, enterprises would need to rewrite all code and readjust compatibilities to switch foundational models, incurring time and financial costs sufficient to lock in most clients.

The capital market's debate over whether the trillion-yuan valuation is a bubble essentially measures general AI ecosystem assets using traditional manufacturing and software industry valuation benchmarks. Throughout internet history, Amazon endured two decades of losses, facing early bubble question (Chinese term meaning 'doubts') about its market cap. However, capital markets priced not current profits but the monopoly value of its ecosystem's endgame. Today, Zhipu's ecosystem network of 3 million developers represents the far-sighted asset supporting its high valuation: while open-source generates no immediate profits, it will continuously convert into MaaS paid services and privatization custom orders, forming a steady stream of long-term monetization channels.

Short-term open-source represents cost investment; long-term, it serves as an ecosystem ticket. The network effect forged by millions of developers constitutes the AI sector's most difficult long-term moat to replicate with capital.

Conclusion

Determining whether Zhipu's trillion-yuan market cap is a bubble or an industry starting point hinges on distinguishing two dimensions: short-term stock prices may carry emotional premiums, but the long-term industrial value fortified by three major moats is not a bubble. In the short term, the company remains in a high R&D investment cycle, with losses likely persisting for years. The price-to-sales ratio in the hundreds includes market speculation over the scarcity of domestic large model targets, with objective correction risks. However, over a five-to-ten-year horizon, the triple barriers of Tsinghua's stable R&D team, government and enterprise cash flow stability, and a million-strong open-source ecosystem simultaneously hold, appearing unique among domestic independent large model vendors.

Merely possessing algorithms cannot navigate industry cycles; blindly piling money into computing power only leads to sustained losses. Zhipu's uniqueness lies in simultaneously holding technological, commercial, and ecological barriers. Its trillion-yuan valuation is not a pricing of its current RMB 700 million in revenue but an early pricing of the ultimate market for domestic general AI infrastructure. While bubbles represent fleeting capital sentiment, a starting point signifies long-term industrial transformation. Zhipu's trillion-yuan market cap essentially signals that China's large model industry has officially entered maturity.

-

![]()

Over 50% of Revenue Hinges on Yutong Optics! This Optical Equipment Manufacturer is Charging Towards an IPO

-

![]()

YOCO Optics Finalizes Industrial and Commercial Registration Update Post 160 Million Yuan Investment in Jiangfeng Biology, Securing 20% Stake to Emerge as Second-Largest Shareholder!

-

![]()

Google Market Value Plummets by $1.5 Trillion Overnight Following the Loss of Two Key Figures

-

![]()

Put an End to the EV 'Weight Gain Race'! Can Your Car Still Be Driven Under the New National Standards?

-

![]()

In 2026, 'AI Upstarts' Collectively Bet on World Models

-

![]()

【OFweek Weike Cup】Phoenix Optics Officially Participates in the 2026 Optical Industry Annual Innovation Product Award

-

![]()

Ford Ditches Mach-E: Will Its Billion-Dollar Electrification Drive Have to Start All Over Again?

-

![]()

【OFweek Weike Cup】Shuangli Hepu Officially Participates in the 2026 High-Growth Enterprise Award in the Optical Industry