Hong Kong Stock IPO 丨 HiLight Semiconductor: 7.5x Revenue Growth in Three Years, Leading Domestic Silicon Photonics Interconnect Provider Launches IPO

06/23 2026

06/23 2026

394

394

Design 丨 Tian

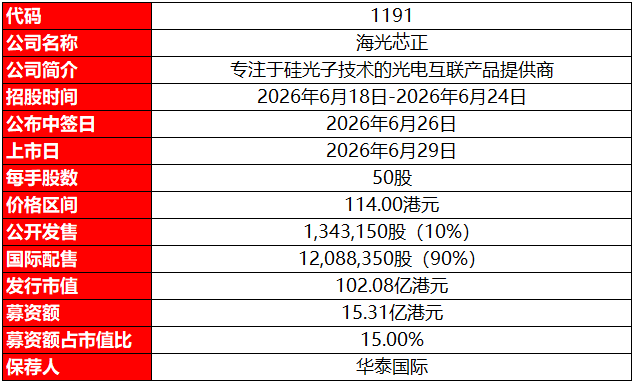

Issuance Details

Source: Prospectus

Financial Performance

HiLight Semiconductor is a rapidly growing domestic core vendor in AI optoelectronic interconnects, with three major product lines covering optical modules, Active Optical Cables (AOC), and Active Electrical Cables (AEC) across full-speed series from 100G to 800G. All 400G+ single-mode optical modules adopt proprietary silicon photonics solutions. The company is deeply positioned in AI computing and data center core sectors, partnering with leading domestic cloud providers like Xiaomi and Alibaba, AI server brands, and telecom equipment leaders. According to Frost & Sullivan, it is one of the few global enterprises with full-chain capabilities from silicon photonics chip design, packaging/testing to optical module manufacturing. Ranked 8th among Chinese AI optical module providers with 1.6% market share by 2025 revenue.

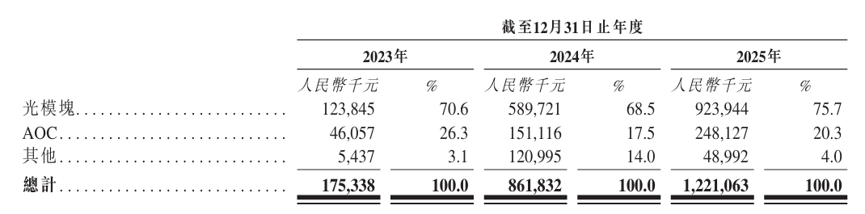

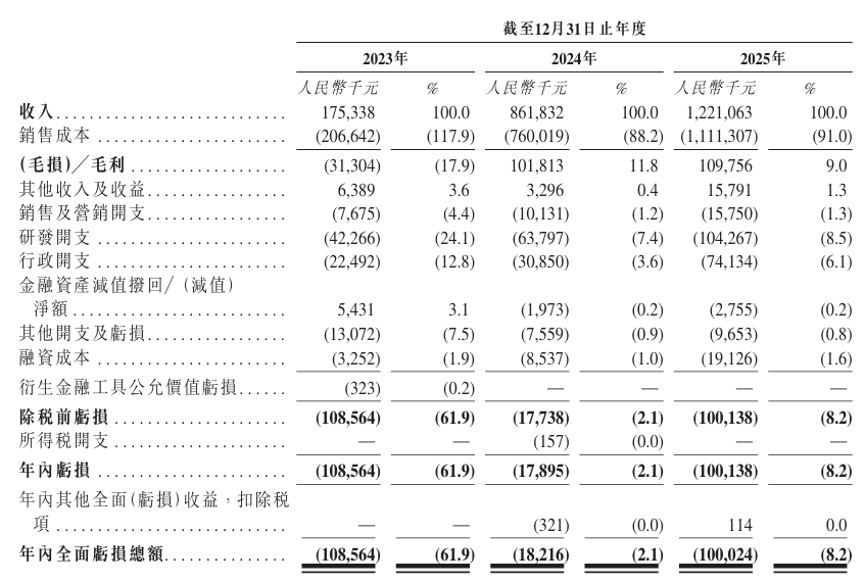

Revenue surged from RMB 175 million in 2023 to RMB 1.221 billion in 2025, achieving a 164% CAGR driven by explosive global demand for high-speed optical interconnects amid AI computing infrastructure expansion. By product structure: Optical modules dominated revenue, contributing RMB 924 million (75.7%) in 2025 with 7.5x growth in three years; AOC as the second growth engine generated RMB 248 million (20.3%) in 2025, rapidly penetrating AI server interconnects and short-distance data centers; other ancillary products/services accounted for 4.0%, creating synergistic cross-selling opportunities.

Source: Prospectus

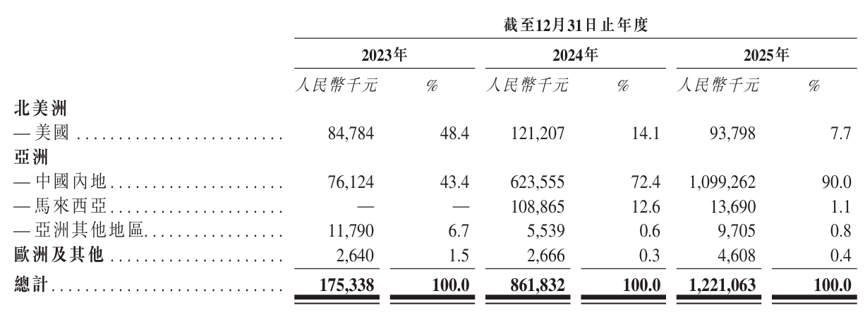

Geographically, the domestic market drove revenue growth, with mainland China's share expanding from 43.4% in 2023 to 90% in 2025, benefiting from accelerated AI computing infrastructure construction and surging optical module orders from core cloud/server vendors. North America remained a key overseas market, peaking at RMB 121 million in 2024 before declining to RMB 94 million in 2025 due to customer procurement cycle adjustments, though long-term expansion potential persists.

Source: Prospectus

Source: Prospectus

The company maintains deep partnerships with top-tier cloud computing and AI infrastructure clients, featuring strong order momentum but high customer concentration: Top two clients accounted for 21.0% and 20.6% of 2025 revenue respectively, with top five clients contributing over 70%. Demand fluctuations and procurement rhythms from these key clients significantly impact short-term performance, with any core customer strategy shift materially affecting results.

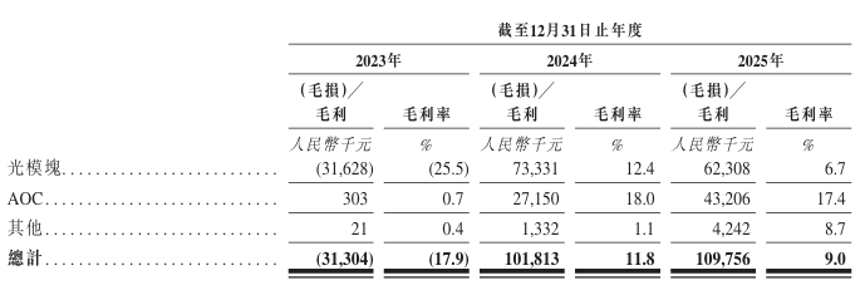

Gross margin improved markedly from -17.9% in 2023 to 11.8% in 2024 and 9.0% in 2025. The 2023 negative margin resulted from early-stage capacity building and product certification, with high fixed costs. The 2024 rebound to 11.8% was driven by mass production of 400G AOC and data center interconnect products, unlocking scale economies. The 2025 dip to ~9.0% reflected intensified high-speed optical module price competition, accelerated product iteration pressures, and initial yield/cost challenges in scaling 800G production.

Source: Prospectus

Source: Prospectus

Net loss narrowed from RMB 109 million in 2023 to RMB 18 million in 2024 before widening to RMB 100 million in 2025, with net margin improving from -61.9% to -2.1% then -8.2%. Despite increased R&D investment in 800G/1.6T/CPO next-gen products, R&D expense ratio optimized from 24.1% to 8.5% through scale effects. However, administrative expenses and share-based compensation rose with organizational expansion, suppressing profitability during rapid scaling. Long-term, sustained high-speed product mix upgrades, cost advantages from proprietary silicon photonics, and deeper scale economies will drive profitability recovery.

Source: Prospectus

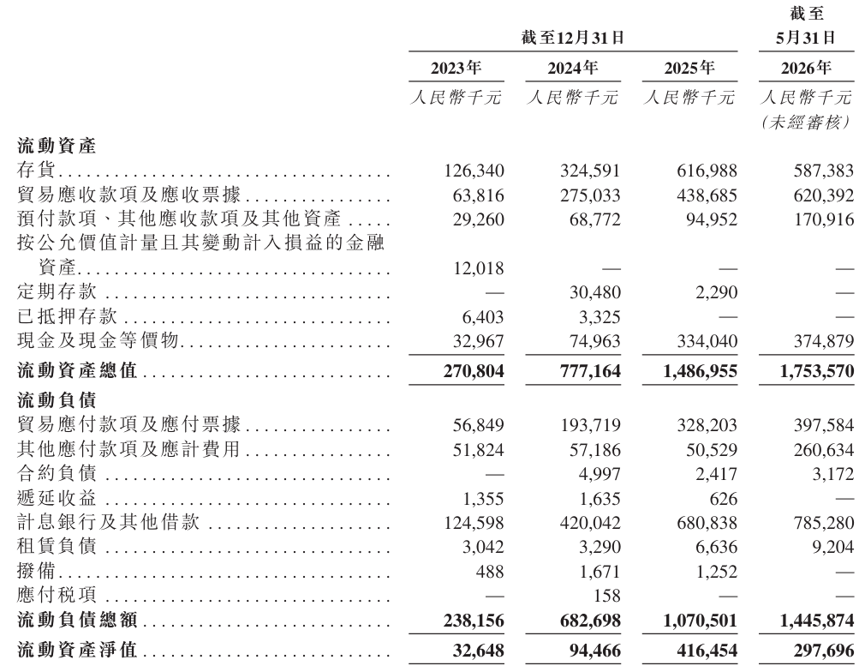

Asset-liability-wise, HiLight Semiconductor, as a technology-intensive and manufacturing-heavy optical component enterprise, concentrates assets in inventory, accounts receivable, production equipment, and construction in progress, with core capital allocations to capacity expansion, R&D equipment upgrades, and supply chain stockpiling. Total assets ballooned from RMB 437 million in 2023 to RMB 1.83 billion in 2025, with net assets growing from RMB 161 million to RMB 586 million, driven by industry upcycle and equity financing. Liabilities primarily comprise bank loans and operating payables, with bank borrowings surging from RMB 160 million at end-2023 to RMB 828 million at end-2025 to support capacity expansion and inventory buildup. The asset-liability ratio first rose (63% in 2023 → 79% in 2024) then fell to 68% in 2025 after Pre-IPO equity financing, remaining relatively high.

Source: Prospectus

Source: Prospectus

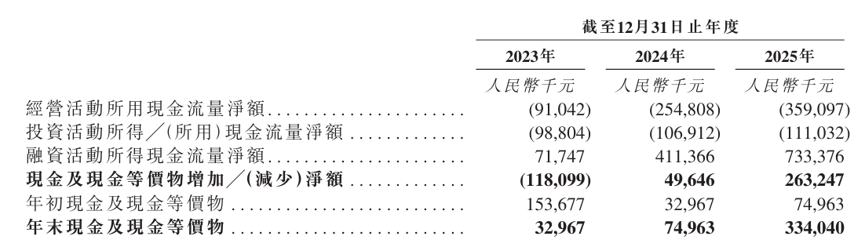

Cash flow remained negative for three consecutive years, with net operating cash outflows widening from RMB 91.04 million in 2023 to RMB 359 million in 2025 as revenue growth drove accounts receivable expansion (RMB 64 million → RMB 439 million) and inventory stockpiling surged (RMB 126 million → RMB 617 million) to meet order fulfillment demands. Investing cash flow also stayed negative, consuming over RMB 300 million in three years for 800G production line equipment and R&D capitalization. The company remains highly dependent on external financing, with net financing inflows reaching RMB 733 million in 2025 alone. As of December 31, 2025, cash balances stood at ~RMB 334 million, insufficient to cover one year's funding needs. This IPO will provide critical capital for high-speed optical module capacity upgrades, silicon photonics R&D, and global market expansion.

Source: Prospectus

Source: Prospectus

Comprehensive Assessment

Market Capitalization

HKD 10.208 billion.

Valuation

This analysis selects Accelink and Eoptolink as comparable companies for HiLight Semiconductor.

Accelink

A leader in high-speed optical interconnects and silicon photonics, Accelink has built full-chain capabilities from core optical chips, high-speed optical components to premium optical modules, with exceptional high-speed signal simulation R&D, precision optical packaging, and large-scale smart manufacturing. Its portfolio spans all generations of high-speed data center optical modules (100G/400G/800G/1.6T/3.2T) while proactively deploying cutting-edge interconnect solutions like CPO, silicon photonics integration, and XPO. It serves AI computing clusters, hyperscale data centers, cloud computing, and 5G telecom networks globally, providing core optical interconnect products and customized solutions to NVIDIA, Microsoft, Google, Amazon, and other global AI/cloud giants.

Eoptolink

A core global provider of high-speed optical interconnect solutions, Eoptolink has established a three-pronged full-stack technology framework covering full-speed product R&D, low-power innovation, and global capacity delivery. It owns proprietary technologies including LPO linear direct drive, silicon photonics chip design, and all-optical switching systems. Its products extend to 12.8T full-series optical modules, encompassing pluggable modules, LPO, CPO optical engines, and other formats, meeting full-scenario demands across data centers, telecom, and enterprise networks. Customers include NVIDIA, Meta, Amazon, and other global tech leaders, with deep overseas market penetration. Eoptolink is a key player combining technological iteration efficiency with global delivery capabilities in the optical module sector.

Source: iFinD, Zhenyan Factory

Note: 1 HKD = 0.8629 RMB; PS = Market Cap / 2025 Revenue; PE = Market Cap / 2025 Net Profit

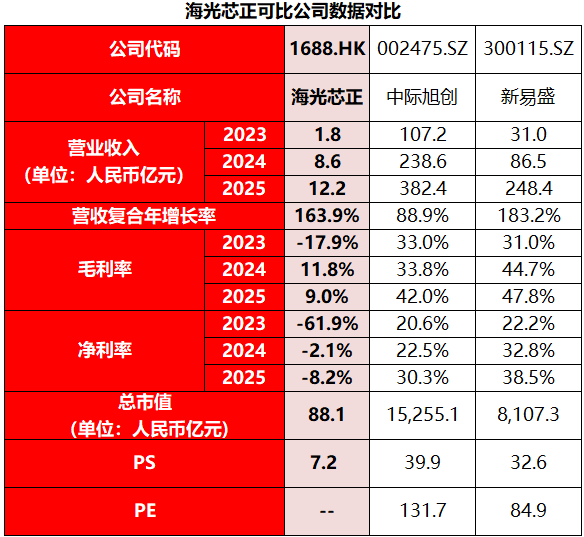

In terms of revenue scale and growth trajectory, HiLight Semiconductor's 2025 revenue of RMB 1.221 billion remains significantly smaller than global leader Accelink (RMB 38.24 billion) and domestic peer Eoptolink (RMB 24.84 billion), reflecting a smaller revenue base. However, its 164% CAGR ranks among the industry's highest, driven by unprecedented expansion in global AI data center capital expenditures, which triggered non-linear demand surges for optical modules and cables. As an early entrant in this niche segment, HiLight Semiconductor is in the initial "0-to-1" phase of customer certification and capacity ramp-up, exhibiting extremely steep growth elasticity. In contrast, Accelink and Eoptolink have completed multiple technology and customer validation cycles, entering a mature harvest phase with synchronized revenue/profit growth through 800G mass production and 1.6T early commercialization, creating significant revenue moats compared to HiLight Semiconductor's early stage. Nevertheless, all three benefit from industry boom dividends with strong growth momentum.

Profitability diverges significantly: Accelink and Eoptolink have sustained upward gross margin trends (benefiting from rising 800G/1.6T product mix and silicon photonics cost optimization), entering accelerated profit release phases. HiLight Semiconductor's gross margin turned positive from -17.9% in 2023 to 11.8% in 2024 but dipped slightly in 2025, reflecting early-stage volatility in product certification, yield improvement, and cost amortization. The company currently focuses on AOC cables and customized optical interconnect systems (JDM/ODM), lacking proprietary optical chip technology barriers, resulting in weaker bargaining power, product value-add, and profit structure stability compared to the two leaders.

At the net margin level, Accelink and Eoptolink both achieved over 10 percentage point improvements, demonstrating the optical module industry's excellent profit-generating capacity amid AI computing dividends. HiLight Semiconductor remains in net loss, though losses narrowed overall before widening again in 2025 due to R&D intensification, IPO expenses, and heightened competition. Profitability inflection and commercialization closed loop (closed loop) require further validation.

Valuation-wise, based on 2025 revenue of RMB 1.221 billion, HiLight Semiconductor's IPO valuation of HKD 10.208 billion (RMB 8.809 billion) implies a PS of ~7.2x, significantly below comparable companies' average, reflecting valuation discounts due to its unprofitable status and weaker earnings certainty compared to industry leaders. Additionally, its smaller revenue base and high customer concentration result in weaker risk resistance than Accelink/Eoptolink. Future Valuation upside potential (valuation upside) will open as 1.6T/3.2T high-speed optical modules and silicon photonics products scale, driving revenue growth and gross margin expansion, shifting valuation logic from growth narrative to earnings delivery.

Listing Team

Source: Prospectus

The company's listing sponsor is Huatai International.

Historically, Huatai International has participated in 74 projects as a sponsor, with 40 gains, 31 losses, and 3 draws in the grey market, resulting in a grey market break rate of 41.89%. On the first trading day, there were 37 gains, 29 losses, and 8 draws, with a break rate of 39.19%, indicating a generally moderate win rate.

Source: Chipbaba

Over-Allotment Option

This issuance includes an over-allotment option, with Huatai International serving as the stabilizing agent.

Offer Size Adjustment Option

This issuance does not include an offer size adjustment option.

Clawback Mechanism

This IPO adopts Mechanism B for issuance.

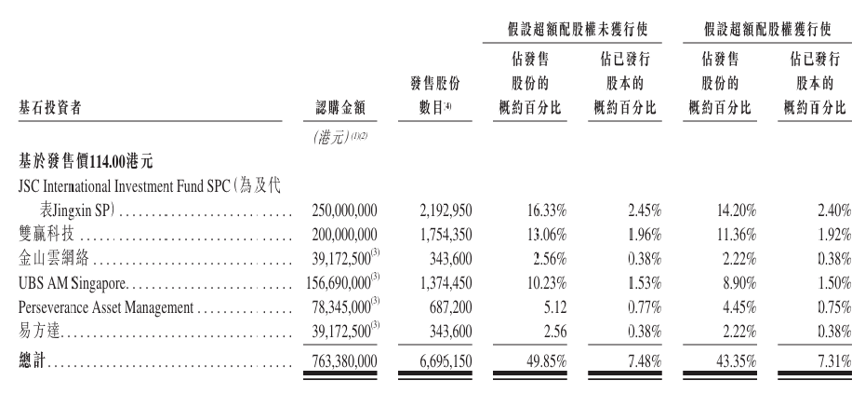

Cornerstone Investors

There are six cornerstone investors: Beijing SASAC, Shuangying Technology, Kingsoft Cloud Network, UBS, Gaoyi Assets, and E Fund, collectively subscribing for HK$763.38 million worth of shares. Based on an offer price of HK$114, this represents 49.85% of the total global offering and 7.48% of the total issued shares immediately following the global offering (assuming the over-allotment option is not exercised).

Source: Prospectus

Pre-IPO Financing

Since its inception, the company has completed over 10 rounds of financing, raising a cumulative total of approximately RMB 885 million. It has attracted well-known investors including Xiaomi, Alibaba, Yunshan Capital, Zhongtian Technology, and Oriza Holdings. In August 2025, the post-money valuation in the final F+ round reached RMB 2.66 billion. Compared to the offering's market capitalization of HK$10.208 billion, the valuation has more than tripled in less than a year.

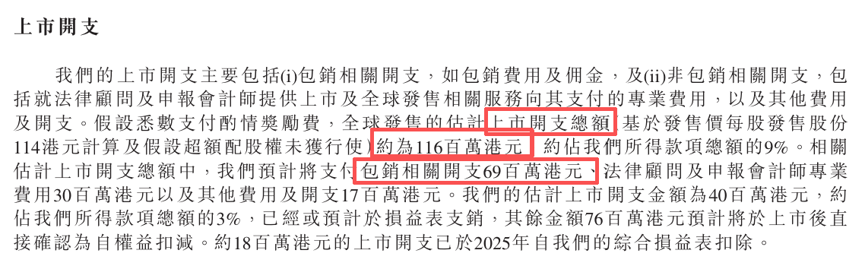

Listing Expenses

The total estimated expenses for this IPO by Haitong Xinzheng are approximately HK$116 million. Based on an offer price of HK$114, expenses account for approximately 9.0% of the proceeds. This includes underwriting-related expenses and fees of HK$69 million, accounting for approximately 5.4% of the proceeds.

Source: Prospectus

Analysis of New Share Subscription

Haitong Xinzheng is a rapidly growing domestic core manufacturer of AI optoelectronic interconnects, with deep coverage in the core sectors of AI computing power and data centers. It has established three core product lines: optical modules, active optical cables (AOC), and active copper cables (AEC), covering the full range of 100G to 800G speeds. It is a core optical interconnect supplier for leading domestic cloud providers such as Xiaomi and Alibaba, AI server brands, and telecommunications equipment leaders. From 2023 to 2025, driven by the explosion in global AI computing power construction and the resulting surge in demand for high-speed optical interconnect devices, the company's revenue soared from RMB 175 million to RMB 1.221 billion, achieving a three-year CAGR of 163.9%. During the performance period, gross margins were -17.9%, 11.8%, and 9.0%, respectively. Affected by intensified industry competition, price competition in high-speed optical modules, and yield ramp-up challenges during the initial scaling production of next-generation products, margins turned positive after three years before experiencing a slight decline. Net profit margins closely mirrored gross margins, with figures of -61.9%, -2.1%, and -8.2% during the performance period, showing a significant trend of narrowing losses and approaching the breakeven point. The revenue surge led to a substantial increase in accounts receivable and inventory levels, continuously increasing working capital requirements. Operating cash flow has seen large net outflows for three consecutive years, with the scale continuously expanding, indicating that the core business has not yet achieved self-sufficiency. Investing cash flow has also consistently seen net outflows, with cumulative investments of over RMB 300 million in high-speed optical module production line equipment and R&D capitalization over three years. The company currently relies heavily on external financing for operations. As of the end of 2025, cash on hand was approximately RMB 334 million, insufficient to meet capacity expansion and R&D needs. This Hong Kong listing will provide the company with essential capital, enhancing financial flexibility.

In terms of the offering structure, this IPO adopts Mechanism B, with an initial public allocation of 10%, totaling 153 million shares or 26,863 lots. The share volume is moderate, with a one-lot entry fee of over HK$5,700, representing a moderate participation threshold. However, the likelihood of successful allocation is not low. As of 13:40 on June 23, Futu's one-lot allocation rate was predicted to be 3.56%. The sponsor, Huatai International, has a moderate historical performance with an average win rate. The cornerstone investor lineup is solid, with Beijing SASAC, E Fund, Gaoyi, and UBS collectively subscribing for nearly 50%, indicating high institutional confidence. The offer price is HK$114, with a market capitalization of HK$10.208 billion (RMB 8.809 billion), essentially at the threshold for inclusion in the Stock Connect. With a PS ratio of 7.2x, the valuation is relatively cheap compared to comparable companies, showing a significant discount.

From a market sentiment perspective, the timing of Haitong Xinzheng's IPO is suboptimal, as there are currently eight other new listings also in the subscription phase. Based on the timeline, funds freed up from the first batch of subscriptions (ending on the 25th) can participate in the third batch of new listings (also ending on the 25th), while the second batch, including Haitong Xinzheng, will be caught in between and unable to participate in either. This results in significant fund diversion. Recently, as multiple cross-border brokers have responded to regulatory adjustments, trading and fund deposits in some mainland investors' accounts have faced restrictions, directly impacting overall activity in the new share subscription market. As of 13:40 on June 23, Haitong Xinzheng's subscription was over 329 times oversubscribed. Interested investors are advised to continue monitoring subscription activity in the coming days.

Disclaimer:

1. This article is based solely on publicly available information and aims to provide factual observations and industry research references. It does not constitute any form of investment advice or offer to buy or sell securities. Data related to companies, stock prices, valuations, market share, etc., mentioned herein are sourced from publicly disclosed documents by the issuer, HKEX disclosures, public news reports, and third-party research. This account makes no explicit or implicit guarantees regarding the completeness or accuracy of such data.

2. Any investment decisions made by readers based on this information are at their own risk. Regulatory requirements differ between the Hong Kong and mainland markets, and cross-border investments require attention to policy, exchange rate, liquidity, and compliance risks.

3. Investment involves risk; decisions should be made cautiously.

For reprints and collaborations, please contact us.

-

![]()

Over 50% of Revenue Hinges on Yutong Optics! This Optical Equipment Manufacturer is Charging Towards an IPO

-

![]()

YOCO Optics Finalizes Industrial and Commercial Registration Update Post 160 Million Yuan Investment in Jiangfeng Biology, Securing 20% Stake to Emerge as Second-Largest Shareholder!

-

![]()

Google Market Value Plummets by $1.5 Trillion Overnight Following the Loss of Two Key Figures

-

![]()

Put an End to the EV 'Weight Gain Race'! Can Your Car Still Be Driven Under the New National Standards?

-

![]()

In 2026, 'AI Upstarts' Collectively Bet on World Models

-

![]()

【OFweek Weike Cup】Phoenix Optics Officially Participates in the 2026 Optical Industry Annual Innovation Product Award

-

![]()

Ford Ditches Mach-E: Will Its Billion-Dollar Electrification Drive Have to Start All Over Again?

-

![]()

【OFweek Weike Cup】Shuangli Hepu Officially Participates in the 2026 High-Growth Enterprise Award in the Optical Industry