SRC Empowers SEER Intelligence to Reach a Market Cap of Tens of Billions, Yet Fails to Sustain Profitability

06/24 2026

06/24 2026

497

497

What is the true value of the 'first robot brain stock'?

As the gates of Chapter 18C of the Hong Kong Stock Exchange slowly open, another technology-driven company steps into the spotlight.

On June 24, SEER Intelligence (06106.HK) officially listed on the main board of the Hong Kong Stock Exchange, claiming the title of the 'first robot brain stock.' With an issue price of HKD 101.60 per share, its IPO market capitalization reached HKD 11.227 billion. Eight cornerstone investors collectively subscribed to HKD 462 million, accounting for 43.34%, with Hillhouse leading the pack with a HKD 118 million subscription. The Hong Kong public offering saw an overwhelming oversubscription of approximately 5,934 times, demonstrating the market's enthusiasm for this 'brain' at least during the IPO phase.

However, when we strip away SEER Intelligence's glossy exterior, we find that this company, which defines its market position through its 'brain,' is forced to sustain itself through its 'body.'

01 From Hardware Base to Data Flywheel: The Three-Tiered Technical Foundation of SRC

At 9:30 a.m. on the 24th, SEER Intelligence opened flat at HKD 101.6. The stock price surged to a high of HKD 136.2 during the session, marking a 34.06% increase, before retreating.

By the close of trading that day, SEER Intelligence stood at HKD 106, up 4.33% from its issue price, with a turnover of HKD 673 million. For a new stock oversubscribed nearly 6,000 times, this debut was not spectacular but managed to hold the line on the issue price.

Yet, beyond the first-day stock performance, a more pressing question arises: What justifies the company's HKD 11.7 billion valuation?

The prospectus provides a clear answer: SEER Intelligence is an intelligent robot company centered around its self-developed robot control system. Building on the market position and leading technology of its 'robot brain'—the robot control system—it develops and sells robots, controllers, software, and accessories, offering one-stop intelligent robot solutions for real-world scenarios, encompassing development, acquisition, and use.

So, what is the technical foundation of this highly sought-after 'brain'?

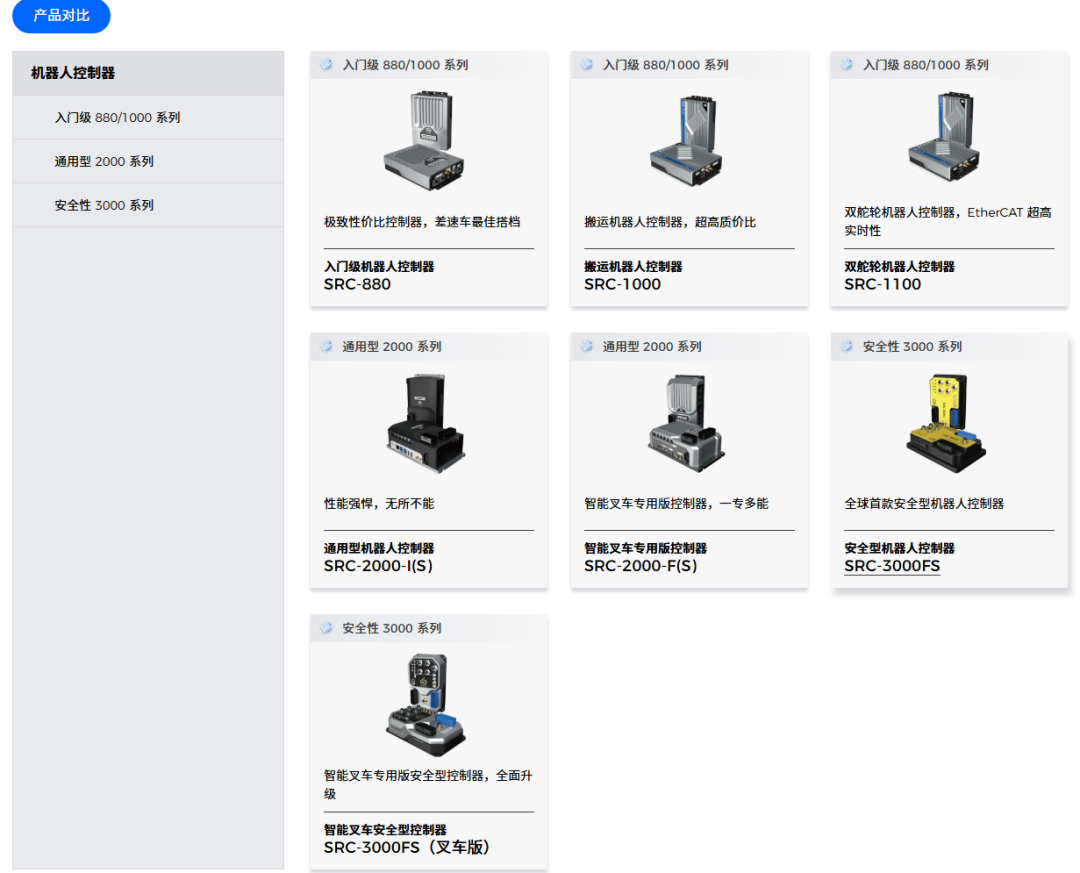

To understand this, the core entry point lies in SEER Intelligence's self-developed 'decision-making hub'—the SRC series controller.

Installed within the body of intelligent robots, it integrates three core modules: perception and localization, intelligent decision-making, and motion control. This is not a simple circuit board but a 'software-hardware integrated' technological base for mobile robots.

At the hardware level, the SRC integrates various computing cores such as CPUs, GPUs, and MCUs, along with industrial-grade communication interfaces. At the system software level, it includes a fully self-developed real-time operating system kernel and middleware by SEER Intelligence. More importantly, at the algorithmic level, it incorporates a hierarchical technical architecture of vision-language-action (VLA), reinforcement learning, end-to-end navigation, and simultaneous localization and mapping (SLAM). Through multi-interface connections with various sensors and actuators, it enables autonomous operation of intelligent robots.

For example, in forklift controller applications, it achieves positioning accuracy of ±2mm and supports dynamic obstacle avoidance and high-precision stacking. As a technological base, the SRC encapsulates all the underlying hardware, operating system, core algorithms, and safety capabilities required to transform an industrial vehicle into an autonomous mobile robot within a single controller.

If the SRC is the 'brain,' then the open ecosystem built around it by SEER Intelligence is the key to making this brain 'user-friendly.'

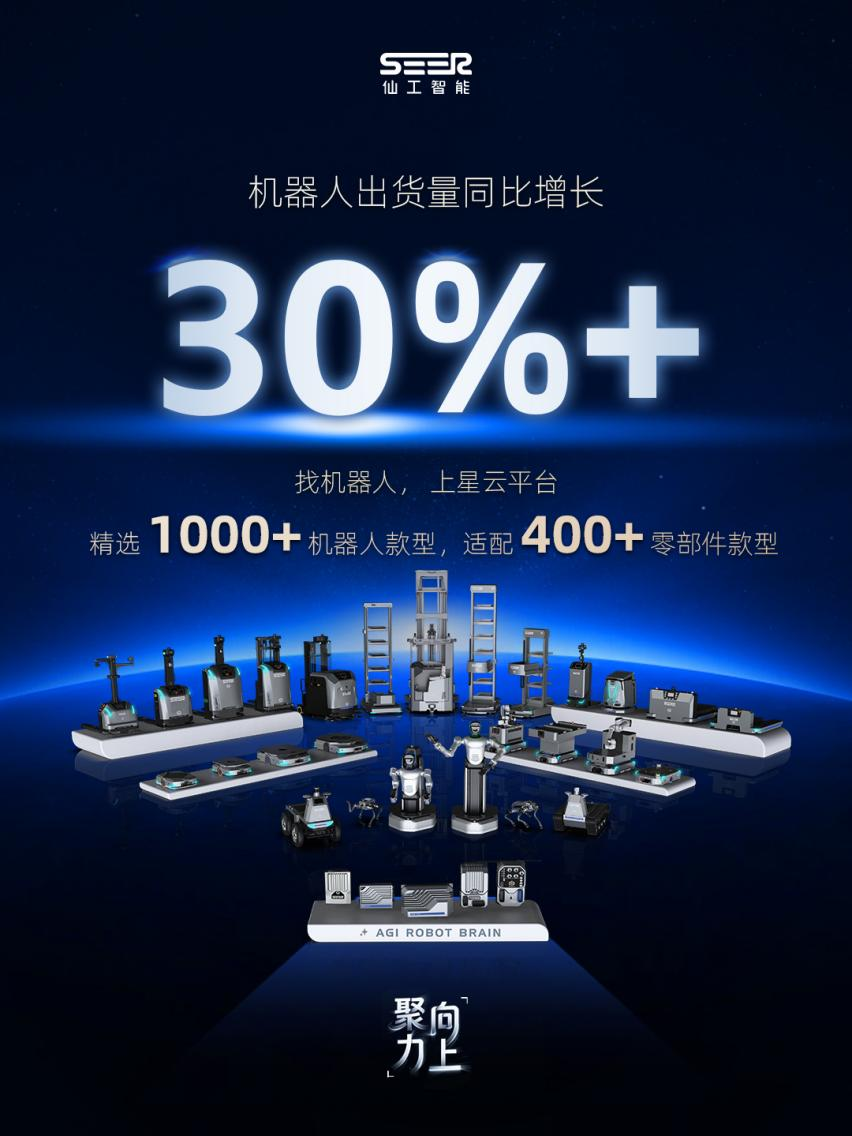

By the end of 2025, the SRC series controllers had been adapted to over 400 types of components, allowing customers to build their own robots 'like LEGO bricks' without requiring in-depth knowledge of hardware compatibility or robotics engineering. This 'plug-and-play' capability significantly lowers the barrier to robot development.

Furthermore, SEER Intelligence's Nebula system further scales this open ecosystem. The system has selectively integrated over 1,000 intelligent robots equipped with SRC series controllers, covering intelligent forklifts, lifting robots, tote robots, all-terrain robots, cleaning robots, and multi-legged robots. Customers can submit customized requests and configure options online through the Nebula platform, enjoying end-to-end transparent services from intention confirmation to offline delivery.

Relying on the plug-and-play controller architecture and the open ecosystem of Nebula, SEER Intelligence has achieved rapid delivery of over 2,000 robot SKUs.

However, a true robot brain is not just about a single model's capabilities but about an embodied intelligence system composed of data closed loops, real-world scenarios, and multimodal models.

At the data level, SEER Intelligence adheres to a real-machine data approach, having shipped tens of thousands of different types of intelligent robots, including humanoids, robot dogs, embodied forklifts, composite robots, and cleaning robots. These robots have accumulated over 60 million hours of operation, generating vast amounts of cross-entity and cross-scenario real-world data.

At the scenario level, robots equipped with SEER Intelligence's 'brain' have been deployed in over 1,000 factories, covering more than 20 industries such as 3C, automotive, new energy, semiconductors, and biopharmaceuticals.

At the model level, the company has applied edge-side E2E models and VLA models to its embodied intelligent robot products, enabling direct mapping from sensor data to control instructions across the entire link .

This demonstrates that SEER Intelligence has established a data flywheel system of 'deployment → data feedback → closed-loop training → model iteration → expanded deployment.'

From the SRC controller encapsulating perception, decision-making, and motion control into a standardized base, to the open ecosystem enabling rapid deployment of over 2,000 robot SKUs, and to the data flywheel continuously iterating through 60 million hours of real-machine operation, these three layers of capabilities together form the true technical foundation of this 'brain.'

02 A 'Brain-Selling' Company That Relies on 'Body-Selling' for Revenue

Selling 'brains' sounds glamorous but may not necessarily be profitable.

Across the tech industry, most companies relying on 'brains' are still struggling with losses. For example, Cambricon, a leading domestic AI chip company, incurred eight consecutive years of losses before going public, with cumulative losses exceeding RMB 5.4 billion, only achieving annual profitability in 2025. Enflame Technology saw cumulative losses exceeding RMB 4.3 billion from 2023 to 2025, with an expected loss of RMB 577 million to RMB 608 million in the first half of 2026. Even globally renowned OpenAI reported revenue of USD 13.07 billion in 2025 but an operating loss of USD 20.92 billion. Losses among 'brain-type' companies have become an industry norm.

Thus, SEER Intelligence can only sustain itself through its 'body.'

In its early stages, SEER Intelligence leveraged its controller technology to extend downstream into complete machine manufacturing, quickly penetrating the end market through standardized forklifts, tote robots, and mobile robotic arms.

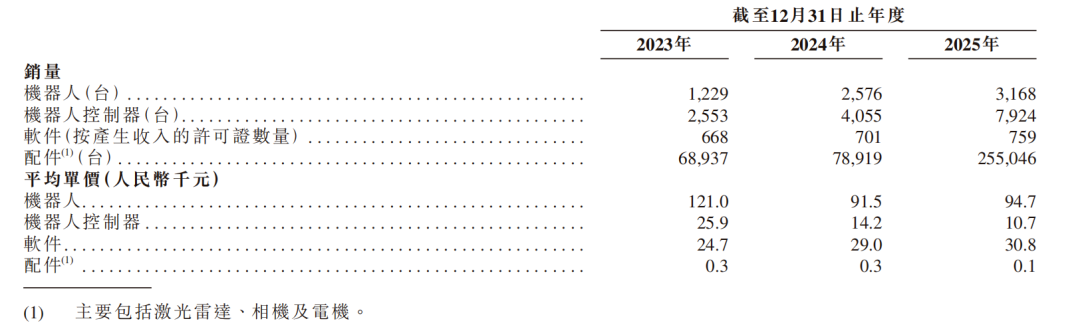

Robot sales surged from 1,229 units in 2023 to 3,168 units in 2025, a 157.8% increase over three years. The true value of the complete machine business lies not in profit but in 'volume deployment.' Sold machines serve as data acquisition terminals equipped with SRC controllers, validating scenarios, accumulating data, and driving controller and software sales.

This strategy is not inherently flawed—without sufficient terminal deployments, the data flywheel cannot spin. However, it may not be a sustainable long-term approach, as the complete machine business is dragging the company into a deeper quagmire.

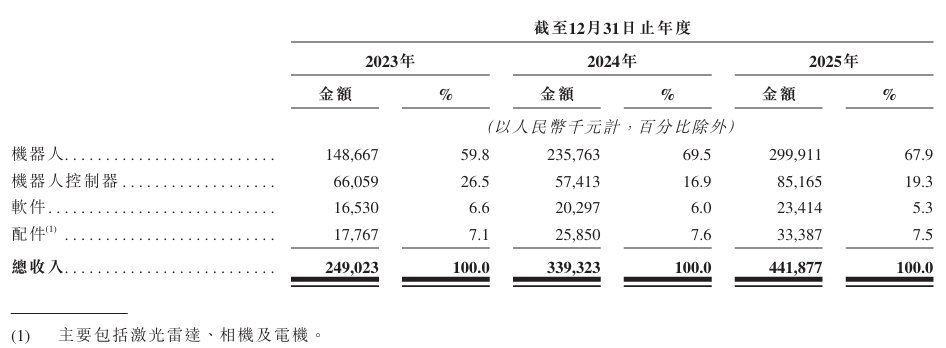

The most immediate impact is a severely inverted revenue structure, with high-margin 'brains' shrinking in proportion while low-margin 'bodies' dominate.

From 2022 to 2025, SEER Intelligence's revenue from complete robot machines rose from 55.6% to 67.9%, while controller revenue fell from 25.5% to 19.3%. In 2025, complete machine revenue reached RMB 299 million, whereas controller revenue was only RMB 85 million.

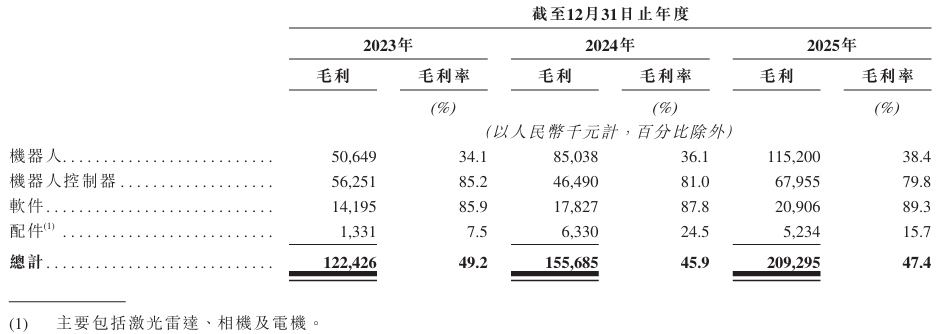

Even more striking is the profit margin disparity. Controller gross margins reached 79.8%, and software margins hit 89.3%, while complete machine margins stood at just 38.4%, yet accounted for nearly 70% of revenue. The most profitable business sells the least, while the least profitable sells the most.

More alarming than the financial data is the strategic misalignment.

The valuation logic for a 'robot brain' in the capital market differs sharply from that of a 'robot complete machine manufacturer.' The former is valued based on platform effects, ecological barriers, and software revenue with marginal costs approaching zero, while the latter is evaluated on production capacity, supply chains, and scale effects.

By controller sales volume in 2025, SEER Intelligence ranked first globally and in China, with market shares of 24.8% and 45.2%, respectively. However, by revenue in the industrial intelligent robot market, it ranked only seventh globally and third in China, with market shares of just 1.1% and 2.5%. Thus, while the complete machine strategy has expanded SEER Intelligence's market presence, the narrative of the 'robot brain' is being diluted by the reality of the 'robot body.'

In summary, when the technological premium of the 'brain' fails to manifest in the revenue structure, market confidence in the 'first robot brain stock' narrative is bound to waver.

03 How Long Can the 'Misaligned' Model Last?

After the listing bell rings, the capital market will not pay solely for a 'number one in controller sales' label. It cares more about whether this 'brain' can truly become the company's profit engine rather than relying forever on 'body' support. If the 'body' cannot translate the 'brain's' technological premium into a profit pillar, the foundation of this business model may begin to crumble.

So, is this 'misalignment' a temporary growing pain in the early stages of listing, or a long-term structural dilemma? To answer this, let's dissect the issue through three dimensions.

First, with controller unit prices declining rapidly, can 'volume growth' truly offset 'price declines'? This is the first challenge SEER Intelligence faces.

The prospectus shows that the average controller unit price dropped from RMB 25,900 in 2023 to RMB 14,200 in 2024 and further to RMB 10,700 in 2025, a 58.7% decline over three years. SEER Intelligence attributes this to falling upstream component costs, scale effects, and increased sales of the entry-level SRC-880 series.

This means that while the controller business maintains relatively high gross margins, it faces product mix changes and downward pricing trends. Whether this business can offset hardware price declines through increased sales volume, expanded application scenarios, and enhanced software system stickiness remains a critical test for SEER Intelligence.

Second, SEER Intelligence has yet to reach its profit inflection point and faces sustained cash flow pressure.

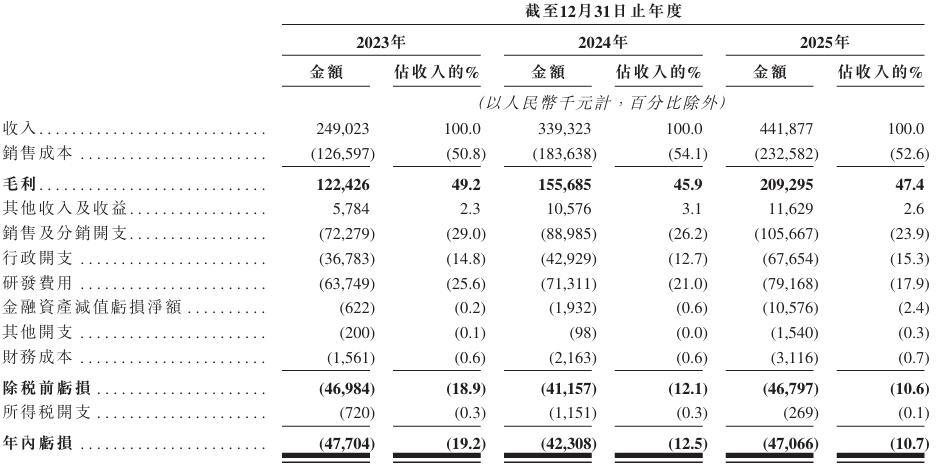

From 2023 to 2025, SEER Intelligence's revenue grew from RMB 249 million to RMB 442 million, a three-year CAGR of 33.2%, but cumulative net losses reached RMB 137 million over the same period. Operating cash flow turned from RMB 10.32 million in 2023 to -RMB 24.96 million in 2024 and -RMB 27.80 million in 2025, with negative outflows continuing for two years. Losses are expected to persist in 2026.

More concerning is that receivables turnover days increased from 61 in 2023 to 111 in 2025, with trade receivables and bills rising to RMB 170 million in 2025, accounting for 38.4% of annual revenue. This means that for every RMB 100 in products sold, over RMB 38 remains as 'IOUs' on the books, eroding the 'quality' of revenue through prolonged collection cycles.

Finally, as competition intensifies, even in the 'champion track' of controllers, SEER Intelligence's moat is far less impenetrable than imagined.

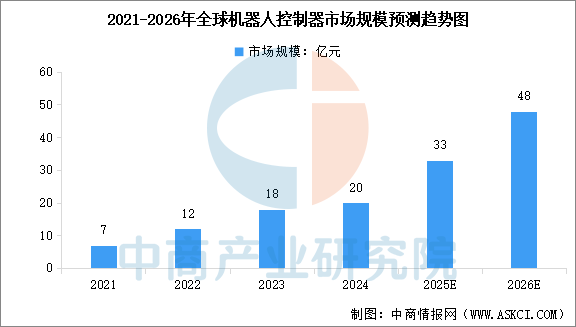

Take Geek+, an industry leader, as an example. Its revenue had reached RMB 3.171 billion by 2025, more than seven times that of SEER. In the controller market, although SEER leads with a 24.8% global market share, according to data from the China Business Research Institute, the global controller market size was only about RMB 3.3 billion in 2025, indicating that this is a market with a relatively low ceiling.

As more players enter the market and product homogenization intensifies, coupled with the inherently limited market size, it remains uncertain whether SEER can sustain its high gross margins for controllers over the long term.

In the short term, SEER's misaligned model of 'nourishing the brain with the body' may barely sustain itself through scale expansion. However, in the long run, the underlying structural contradictions are pushing this business logic toward an increasingly narrow corner.

Perhaps what SEER truly needs is not just a 'sales champion' title that exists only in its prospectus, but rather a shift in its value focus from the 'body' to the 'brain'.

* Image sourced from the internet. Please contact us for removal if there is any infringement.

-

![]()

Total Investment Hits Nearly 3.28 Billion! Goertek Launches Mass Production of 12-Inch Transparent Substrate Wafer for AR Glasses’ Micro-Nano Optical Components

-

![]()

Why Is This Precision Optical Film Leader Worth Reevaluating with a Tens of Millions Procurement?

-

![]()

AI Costs Plummet by 90% Over Nine Years: Key Insights from Davos You Shouldn’t Miss

-

Doubao, Your Late-Night AI Companion, Now Eyes Profitability

-

![]()

SRC Empowers SEER Intelligence to Reach a Market Cap of Tens of Billions, Yet Fails to Sustain Profitability

-

![]()

China’s Embodied AI Industry Faces Fierce Domestic Competition, Making Overseas Expansion Essential for Survival

-

![]()

32.8 Billion Yuan Investment! Goertek’s 12-Inch AR Glasses Optical Wafer Base in Lingang Begins Operations

-

![]()

How Far is the All-New Li Auto L8 from Being the Best Five-Seat SUV with In-House Full-Stack Development?