China’s Embodied AI Industry Faces Fierce Domestic Competition, Making Overseas Expansion Essential for Survival

06/24 2026

06/24 2026

440

440

By 2026, the embodied AI industry will transcend the stage of “trade show buzz” and “lab prototypes,” fully entering a pivotal phase of testing, validation, and small-scale commercial rollout.

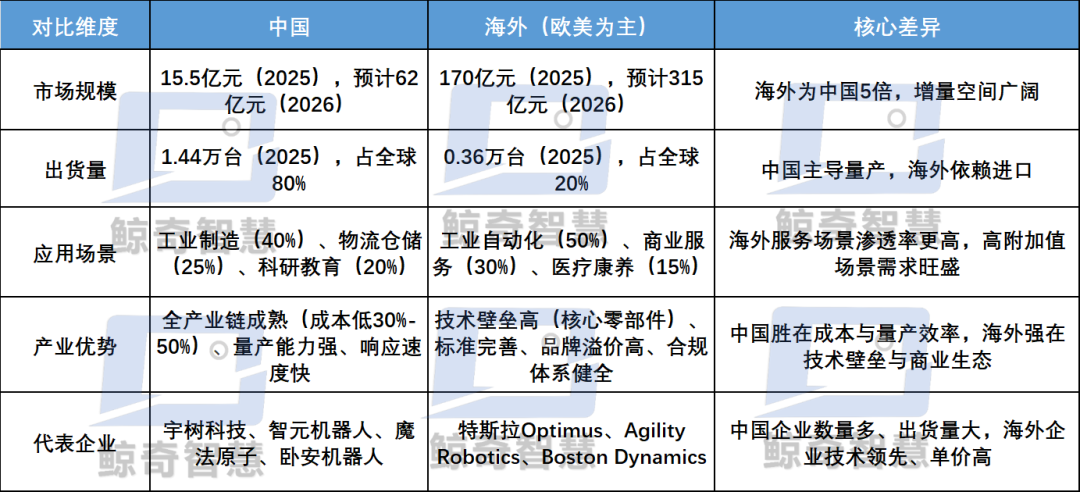

China, responsible for 74% of global shipments and leveraging unparalleled cost advantages, has emerged as the global hub for embodied AI growth. However, the domestic market is plagued by intense price competition and product homogenization, while overseas markets offer untapped “blue ocean” opportunities characterized by labor shortages, strong purchasing power, and inelastic demand.

For Chinese embodied AI companies, overseas expansion has transitioned from a strategic “option” to a survival “necessity.” Success no longer hinges on hype-driven funding or valuation bubbles but on overcoming structural challenges in scenario selection, delivery reliability, after-sales networks, compliance, and data-driven iteration. The goal is to establish sustainable commercialization pathways—spanning industrial logistics to service applications and evolving from single-point validation to large-scale replication.

From Domestic Homogenization to Global Incremental Markets

Data indicates the embodied AI industry will achieve a critical leap between 2025–2026, with global shipments surging from 18,000 to over 50,000 units (+700% YoY). Chinese firms will account for >74% of shipments, with leaders like Unitree and ZhiYuan Robotics achieving annual mass production exceeding 5,000 units.

China boasts the world’s only fully integrated embodied AI supply chain, covering core sensors, servo motors, final assembly, and algorithm adaptation, with costs 30–50% lower than overseas competitors. This creates irreplaceable advantages in large-scale manufacturing.

The industry’s focus is shifting from “parameter competition” and “prototype demonstrations” to “real-world testing” and “small-batch commercial delivery.” Industrial manufacturing and logistics warehousing are the primary application scenarios, accounting for >60% of deployments.

Meanwhile, domestic markets face severe homogenization and price wars. Humanoid robot prices plummeted from >500,000 RMB in 2024 to 100,000–150,000 RMB in 2026, with some quadrupedal robots dropping below 50,000 RMB. Gross margins universally fall below 20%.

In contrast, overseas markets grapple with accelerating global aging, labor shortages in manufacturing across Europe, Japan, South Korea, and the U.S., and rising labor costs. Traditional automation cannot meet flexible production needs, making embodied AI robots the optimal solution for cost reduction and efficiency gains. The global inelastic-demand market is expanding, with the market size projected to exceed 100 billion RMB by 2028.

Another authoritative report predicts the 2026 overseas embodied AI market will reach 31.5 billion RMB (+450% YoY), with high premium potential and gross margins of 40–60%.

At this global industrial inflection point, “going overseas” is no longer a strategic choice but a survival imperative for Chinese embodied AI firms. However, globalization is not a simple replication of traditional hardware exports’ “price-for-volume” model.

Breakthroughs face deep structural contradictions: mismatches between domestic mass-production advantages and highly fragmented overseas scenario demands; the “wooden barrel effect” of hardware cost advantages offset by software generalization shortcomings; and short-term pressures to close commercial loops and secure orders versus long-term ecosystem building.

Five Key Capabilities for Embodied AI Overseas Breakthroughs

Over half of Chinese embodied AI firms expanding overseas remain stuck in “product selling,” neglecting deeper overseas demands for long-term operations, localization, data compliance, and scenario adaptation.

This results in industry-wide issues like “easy pilots but hard scaling” and “easy contract signing but hard repurchasing,” forming the core bottleneck to scaled overseas expansion.

Beyond capital noise, the true competitiveness of embodied AI overseas expansion lies in structural hard power across scenario definition, stable delivery, after-sales networks, compliance adaptation, and data loops.

(1) Scenario Definition: Prioritize high-value inelastic-demand scenarios. Given the short-term hurdles for general-purpose humanoid robots in achieving large-scale commercialization, firms must abandon blind pursuit of “universal scenario generalization.”

Currently, priority should go to vertical scenarios like automotive manufacturing, 3C electronics, e-commerce logistics, and retail services. These offer high demand certainty, standardized processes, agile deployment, and quantifiable ROI—the optimal path to commercial viability.

(2) High-Reliability Delivery: Overseas markets demand 7×24 continuous operation, <0.5% failure rates, and >5,000-hour MTBF (Mean Time Between Failures). Delivery stability is not just factory parameters but a litmus test for long-term real-world reliability. It directly determines overseas customer trust and repurchase willingness, forming the core defense for scaled overseas expansion.

(3) After-Sales Networks: Localized responsiveness underpins scaled deployment. Embodied AI robots feature tightly coupled hardware-software systems, requiring complex deployment, frequent maintenance, and strong spare parts dependency. Industry baselines demand stringent SLAs: “48-hour onsite response, 72-hour fault resolution, and >90% local spare parts inventory.”

Building a three-dimensional operations network—“local teams, regional spare parts centers, remote maintenance platforms”—is the essential ticket for crossing commercialization thresholds and achieving global expansion.

(4) Compliance Capabilities: Safety and data governance red lines form rigid overseas entry barriers. Currently, Europe and the U.S. markets are erecting strict regulatory walls for embodied AI products. Compliance has evolved from a baseline requirement to an indispensable core defense for overseas firms.

For physical and system safety, the EU mandates CE certification (aligned with ISO 10218 mechanical safety standards) and includes it in the AI Act’s high-risk category for strict review. The U.S. enforces FCC and UL safety norms.

For data governance, frameworks like GDPR mandate localized data storage, require special approvals for cross-border transfers, and impose “high-wall” controls on biometric and multimodal data critical for embodied AI development.

(5) Data Loops: The competitive foundation of embodied AI lies in continuous iteration through real-world scenario data. Overseas scenario data (industrial conditions, logistics flows, service interactions, etc.) differ significantly from domestic data. Without localized data loops, models hit generalization bottlenecks, stalling product iteration.

Chinese firms must accelerate overseas data reflow and training pipelines under compliance, transforming cross-scenario data into irreplaceable technological moats for sustainable global competitive advantage.

Ultimately, these five capabilities determine whether firms can progress from “one-time orders” to “scaled repurchases” and drive ecological shifts from “hardware manufacturers” to “global full-stack scenario solution providers.”

Value Pathways for Embodied AI Overseas Expansion

After overcoming “capability building,” global layout becomes the industry’s next focus.

The embodied AI value chain comprises four links: hardware, models, data, and services. In reality, firms cannot simply export this “full package” overseas.

With varying “home court advantages”—some rely on hardware sales, others on “brains” (AI models)—firms must leverage core strengths to explore differentiated overseas pathways amid complex markets.

1. Hardware-First Approach: From “Lab Tools” to “Production Mainstays”

This path emphasizes ultimate cost-performance, first penetrating universities and research institutions. Unitree’s >70% market share in educational research exemplifies this.

However, true commercialization requires organizational transformation: firms must shift from “serving teachers and students” to “engaging procurement managers” and endure rigorous 6–12-month POC (Proof of Concept) trials by industrial clients. This marks not just a customer shift but the key leap to scaled deployment.

2. Scenario-Closed-Loop Approach: Deep Integration of Technology and Scenarios

Firms no longer sell hardware alone but deploy self-developed large models and full-stack solutions directly into high-value overseas domains like factories and power inspection, transitioning from “finding nails” to “taking deep root.”

Examples include UBTECH empowering Airbus production lines and Fifth Era Robotics achieving 24/7 autonomous handling in Germany. While this “deep embedding” creates high competitive barriers, it is constrained by industrial scenarios’ fragmentation, making scaled replication a “marathon.”

3. Model-Ecosystem Approach: Aiming to Collect “Ecosystem Taxes”

This typifies a “light-model, heavy-capital” strategy. Firms often establish R&D hubs in overseas tech frontiers like Silicon Valley, using open-source world models and VLA (Vision-Language-Action) large models to attract global developers, aiming to build a flywheel of “real-machine scale → data repatriation → model leadership.”

The core challenge is “cold start”: ecosystem stickiness depends heavily on physical deployment scale, which in turn relies on the ecosystem’s attractiveness. Breaking this “chicken-and-egg” deadlock is key to this model’s success.

4. Components Warfare Approach: “Hidden Champions” Embedded in Supply Chains

These firms operate discreetly but occupy the deepest links in the embodied AI supply chain. Examples include domestic dexterous manipulation platforms quietly integrated into Cambridge, Stanford, and Siemens systems, and precision component makers like Leader Harmonic Drive and Wuzhou New Spring leveraging overseas OEM giants’ capacity expansions to “ride the wave.”

Though low-profile in end-brand markets, their hardcore technical barriers and deep ecosystem bindings secure foundational supply chain profits.

Embodied AI overseas expansion is returning to commercial rationality, reflecting overseas markets’ core logic: customers demand “production tools” that create value, not “tech toys” for concept display.

Meanwhile, the global market landscape shows “Europe and the U.S. anchoring value highlands, emerging markets driving scale dividends.” Chinese firms are adopting a phased strategy—“easy-to-hard, application-first-then-technology”—to systematically explore global markets.

Phase 1: Southeast Asia & Middle East—Overseas “Foot in the Door” and Commercial Closed-Loop Testbeds. These regions focus on service, inspection, and retail applications, offering low entry barriers and policy friendliness—ideal for Chinese firms to validate commercial models.

Phase 2: Europe—A “Litmus Test” Market Combining High Value and High Barriers. Stringent CE certifications and GDPR data compliance create steep entry hurdles, forcing Chinese firms to abandon “quick-profit” mentalities and commit to long-term localization, making it a battleground for industrial-grade embodied AI commercialization.

Phase 3: North America—Overseas Frontier and Compliance Risk Zone. Home to global top-tier R&D and algorithm ecosystems, the region poses high compliance risks from geopolitical tensions, tariff barriers, and export controls. Chinese firms currently adopt a “lightweight” strategy—“Silicon Valley model nodes + targeted scientific research client outreach”—to bypass compliance minefields of whole-machine exports via “algorithm-first” approaches.

This tiered breakthrough strategy will help firms escape domestic “inventory competition” traps and unlock trillion-RMB incremental blue oceans. By 2035, China is projected to capture 55% of the global embodied AI market.

China’s embodied AI industry holds core strengths in full-supply-chain cost control, agile mass production, and flexible services. Weaknesses lie in algorithm generalization, overseas ecosystem building, and compliance governance experience.

With 2026 half over, Chinese embodied AI overseas expansion is moving beyond sporadic trials into a phase of scaled, quality-driven growth. This is not mere “Made in China” capacity overflow but the prelude to “Intelligent China Ecosystem” leading the globe.

*Editor's Note: Original content is hard-earned; please respect authors. For reprints, contact us.

-

![]()

Total Investment Hits Nearly 3.28 Billion! Goertek Launches Mass Production of 12-Inch Transparent Substrate Wafer for AR Glasses’ Micro-Nano Optical Components

-

![]()

Why Is This Precision Optical Film Leader Worth Reevaluating with a Tens of Millions Procurement?

-

![]()

AI Costs Plummet by 90% Over Nine Years: Key Insights from Davos You Shouldn’t Miss

-

Doubao, Your Late-Night AI Companion, Now Eyes Profitability

-

![]()

SRC Empowers SEER Intelligence to Reach a Market Cap of Tens of Billions, Yet Fails to Sustain Profitability

-

![]()

China’s Embodied AI Industry Faces Fierce Domestic Competition, Making Overseas Expansion Essential for Survival

-

![]()

32.8 Billion Yuan Investment! Goertek’s 12-Inch AR Glasses Optical Wafer Base in Lingang Begins Operations

-

![]()

How Far is the All-New Li Auto L8 from Being the Best Five-Seat SUV with In-House Full-Stack Development?