86% Gross Margin, Revenue Hits 48-Year High: Micron Warns of Prolonged Supply Tightness Beyond 2027

06/26 2026

06/26 2026

341

341

Following the close of the U.S. stock market on June 24, global memory chip behemoth Micron Technology (NASDAQ: MU) unveiled an earnings report that will be etched in semiconductor history.

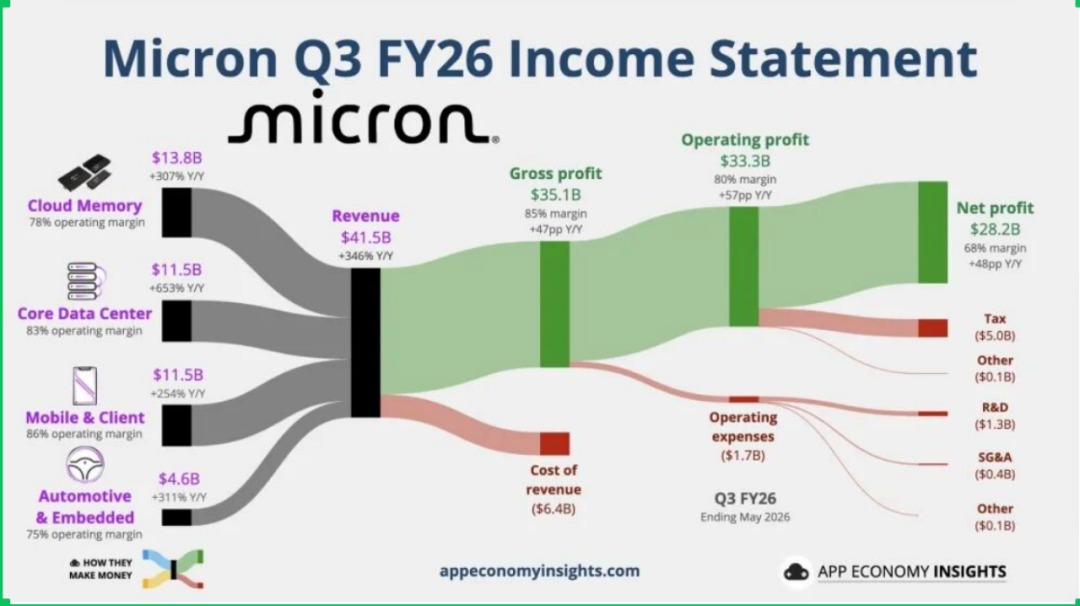

In the fiscal third quarter of 2026, which concluded on May 28, 2026, Micron reported revenue of $41.46 billion, marking a staggering 346% year-over-year surge and a 74% quarter-over-quarter increase. This achievement represents the fifth consecutive quarter of record-breaking revenue. Under GAAP, net profit soared to $28.24 billion, with diluted earnings per share (EPS) reaching $24.67. On a non-GAAP basis, net profit climbed to $28.86 billion, with EPS of $25.11.

What truly captivated the market was Micron's fourth-quarter outlook: revenue is projected to approach $50 billion (±$1 billion), with a gross margin of approximately 86% and EPS around $31 (±$1)—all poised to shatter the company's 48-year records once again.

However, the true gem of this earnings report lies not in the explosive data from the past three months but in Micron's management's forward-looking vision for the industry landscape: AI-driven memory demand represents not a cyclical rebound but a structural transformation.

From "Commodity" to "AI Infrastructure": The Pricing Power Revolution Behind an 84.9% Gross Margin

The most groundbreaking revelation in Micron's earnings report is not the revenue growth but the qualitative shift in profitability.

The consolidated gross margin soared to 84.9% in the third quarter, up 10 percentage points sequentially and doubling year-over-year, setting a new company record. All four business units maintained high margins: the Cloud Storage Business Unit (CMBU) at 83%, the Core Data Center Business Unit (CDBU) at 87%, the Mobile & Client Business Unit (MCBU) at 87%, and the Automotive & Embedded Business Unit (AEBU) at 79%.

(Image source: Micron's earnings report)

This profitability surge underscores the memory chip industry's metamorphosis from a "cyclical commodity" to an "AI core infrastructure." Micron CEO Sanjay Mehrotra stated candidly during the earnings call: "The strategic value of memory in the AI era is being redefined, and industry supply constraints will persist beyond 2027."

The data center boom is the primary driver. In the third quarter, Micron's annualized revenue run rate for data center-related businesses exceeded $100 billion, with data center SSD revenue doubling sequentially to surpass $5 billion. Fueled by dual demands for AI training and inference, high-bandwidth memory (HBM) has become an even scarcer "hard currency" than GPUs—Micron's HBM capacity for 2026 is fully booked.

HBM4 Ramp-Up and HBM4E Readiness: Technological Iteration Defines Market Leadership for the Next Three Years

In the AI computing race, high-bandwidth memory (HBM) is the decisive factor. Micron confirmed in its earnings report that HBM4 memory chips, based on 1-beta-generation DRAM technology, have entered mass production for key customer platforms, with multiple other clients receiving validation samples. The next-generation HBM4E is under development, with mass production expected in 2027.

This timeline is crucial. Currently, SK Hynix leads the HBM market with a 56.4% global share in Q1 2026 and has filed for a U.S. IPO. Samsung, grappling with HBM3E yield issues, has temporarily shifted capacity to HBM4.

Micron's HBM4 mass production solidifies its position in the next product cycle. The 2027 HBM4E mass production timeframe reserves ammunition for its technological competition in 2027–2028.

Given that the HBM market is projected to reach $100 billion by 2028—two years earlier than previously forecast—whoever maintains technological leadership in HBM4 and HBM4E will secure the largest slice of the "$100 billion AI memory cake."

Supply Bottlenecks: "No Sign of Relief Before 2028"

While earnings data answer "how profitable now," supply-side judgments determine "how long this profitability will last."

Mehrotra shocked the market with his assessment: Even if industry supply improves gradually by 2028, there is "no visibility on when memory supply can catch up with surging demand." He noted that memory supply growth hinges on massive greenfield fab expansions, which are "enormous, complex, and time-consuming."

Micron CBO Sumit Sadana revealed that current DRAM and NAND demand significantly outstrips supply, with Micron meeting only 50–67% of key customers' needs.

Behind this "structural shortage" lies exponential growth in AI computing demand. Micron's third-quarter data center business annualized revenue run rate exceeded $100 billion, with data center SSD revenue surpassing $5 billion in a single quarter, more than doubling sequentially. Future AI adoption in smartphones, high-end PCs, automotive, industrial applications, and robotics will further amplify memory demand. Management highlighted that robotics and humanoid robots are expected to drive growth over the next two decades, requiring significant memory capacity.

Capital Expenditure Surge: $27 Billion Bet on Future Capacity

To sustain this "super cycle," Micron is expanding capacity at an unprecedented pace. Fiscal 2026 capital expenditures are estimated at $27 billion, including $10 billion in Q4.

The company had already raised its annual capex from $18 billion to over $25 billion, with projects including a mega-fab in New York built in partnership with Bechtel and leveraging up to $6.4 billion in CHIPS Act subsidies for large-scale U.S. manufacturing.

However, capacity ramp-up takes time. Micron expects new fabs to contribute meaningfully to earnings starting in fiscal 2028. This implies that supply-demand tightness in the memory market will remain largely unchanged in 2026–2027, with strong price support.

For Micron, this $27 billion gamble bets that AI memory demand is not a flash in the pan but a long-term boom lasting at least five years.

A-Share Market Reaction: "Beta Rally" in Memory Sector and Accelerated Domestic Substitution

Micron's "legendary earnings" quickly reverberated in the A-share market. On June 25, the A-share memory chip sector gapped higher, with Biwin Storage and Longsys rising over 5%, GigaDevice hitting the 10% daily limit with a market cap nearing 500 billion yuan, Wuxi Taiji Industrial sealing a 10% limit up, Yoke Technology up over 6%, and HuiCheng Technologies and GigaDevice sealing 20% limit up.

This rally reflects synchronized global memory industry sentiment. Domestically, memory module makers like Longsys, Biwin Storage, and Demingli have been early beneficiaries of price hikes and inventory revaluations. Design-side players like GigaDevice and Montage Technology continue to break through in NOR Flash and memory interface chips. Yangtze Memory's market share has risen to 13%, tying with Micron and SanDisk as the world's fourth-largest, with its IPO process accelerating.

More critically, overseas giants like Micron and Samsung are prioritizing capacity for HBM and advanced DRAM, further tightening supply of commodity DRAM, NAND, and enterprise SSDs, with lead times extending beyond six months. This opens a window for domestic memory module and chip design firms to accelerate substitution. Customer adoption driven by shortages is shifting from "optional" to "mandatory."

Conclusion

Micron's earnings report is not just a corporate update but a manifesto revaluing the memory industry in the AI era. With gross margins exceeding 85%, SCA locking in $100 billion-plus RPOs, and data center revenue hurtling toward an annualized $100 billion, memory is no longer the fragile sector that investors "fear cyclicality."

For China's semiconductor industry, this is both the worst and best of times—giants are erecting higher barriers with capital and agreements, but AI demand's certainty provides unprecedented substitution opportunities. Whether Chinese memory firms can achieve technological leaps before the 2027 supply gap narrows will determine if they join this "super cycle" or merely serve as a backdrop to Micron's capital feast.

END

Special Disclaimer: This content is sourced from publicly available internet channels. Please contact us for removal if copyright infringement occurs. This article does not constitute any investment advice, guidance, or commitment and is solely for industry exchange and discussion. Market risks exist; invest cautiously!

-

![]()

Profits Skyrocket! From Leasing to Construction: A Storage Enterprise with Hundred-Billion-Yuan Revenue Plans 1.175 Billion Yuan Investment in New Headquarters

-

![]()

Discounts Now on Offer: Is Xiaomi No Longer Grappling with Vehicle Shortages?

-

![]()

Samsung Doesn't Make Money the Hard Way

-

![]()

Japanese Media Acknowledges: China's Engine Technology Outstrips That of Japanese Firms

-

![]()

Japanese Media Concedes: China’s Engine Technology Outpaces Japanese Firms

-

![]()

Doubao Professional Version Unveiled! China Now Boasts Its Own National-Level Professional AI Agent

-

![]()

ByteDance and Alibaba Both Step Back from the Gaming Arena

-

Xiangeo International Clears BSE Review: Setting a Global Standard for the ‘Chinese Sound’ | A-Share Financing Brief