Samsung Doesn't Make Money the Hard Way

06/26 2026

06/26 2026

484

484

The home appliance and smartphone sectors, once the cornerstone businesses supporting the 'Samsung Empire,' have reached a turning point. Samsung's response requires not just a simple market exit or retreat but a fundamental strategic overhaul.

Cover image source: Unsplash

Samsung is further distancing itself from the home appliance industry.

According to foreign media reports, Samsung Electronics held a global strategy meeting in mid-June to conduct a comprehensive review and planning of its current key business issues, including accelerating the restructuring of its DX division (covering consumer electronics and mobile businesses).

Notably, a major adjustment to its home appliance product line was announced: Samsung plans to discontinue or outsource certain low-margin products while concentrating departmental resources on high-end offerings and more competitive businesses.

Just over a month earlier, Samsung had already announced the cessation of sales for all home appliance products—including TVs and monitors—in the Chinese mainland market. Recently, netizens observed that Samsung Electronics' official WeChat public account appears to be frozen, Suspected cancellation (presumably deactivated).

These consecutive developments indicate that Samsung is not merely adjusting its layout (market layout translates better as 'market positioning' or 'market strategy') in a single market but is undertaking a radical transformation of its entire home appliance business.

As the global home appliance industry enters an era of thin profits, Samsung's strategic pivot reflects not just a corporate reorientation but also the collective anxiety of traditional home appliance companies amid the wave of intelligence: supply chains grow increasingly mature, markets become more competitive, and profit margins shrink. The question is how to survive this major reshuffle.

1. Samsung Refuses to 'Earn Meager Profits'

As early as April this year, South Korean media reported that Samsung was restructuring its home appliance production system, including outsourcing some low-priced product lines to overcome growth bottlenecks and ensure profitability.

Around the same time, news emerged that Samsung had decided to shut down its TV factory in Slovakia and microwave oven factory in Malaysia, with plans to fully outsource production of low-margin products like dishwashers and microwaves while retaining in-house manufacturing for high-margin categories such as refrigerators, washing machines, and air conditioners.

The reason behind Samsung's abandonment of self-research and production for mid-to-low-end home appliances is simple: the sector is no longer profitable.

Throughout 2025, Samsung's Visual Display (VD) and Digital Appliances (DA) divisions—responsible for TV operations—collectively incurred losses of KRW 200 billion (approximately RMB 945 million), marking their first annual loss since establishment.

In Q4 2025, Samsung intensified price cuts to reverse declining trends, but results fell short of expectations. Revenue increased by a mere 2.3% YoY, while operating profit margins further declined to -4.1%—meaning even price wars failed to boost appliance sales.

By Q1 2026, conditions had not improved. Revenue for the two divisions reached KRW 14.3 trillion, with operating profit of just KRW 200 billion (approximately RMB 882 million), yielding a profit margin of around 1.4%.

Meanwhile, Samsung's semiconductor division told a different story.

In 2025, Samsung's Device Solutions (DS) division reported total revenue of KRW 130.1 trillion (approximately RMB 610.17 billion) and operating profit of KRW 24.9 trillion (approximately RMB 109.85 billion), representing a 64.9% profit increase.

By Q1 2026, Samsung Electronics achieved record quarterly revenue of KRW 133.9 trillion and operating profit of KRW 57.2 trillion. The DS division contributed approximately KRW 53.7 trillion in operating profit, accounting for 94% of the company's quarterly operating profit and surpassing its total 2025 annual profit in a single quarter.

The data comparison tells all: with HBM memory and enterprise SSD profits surging, over 90% of Samsung's profits now come from semiconductors, rendering the meager profits from home appliances negligible.

This profit disparity transcends financial reports, triggering internal divisions—profitable businesses grow dominant while unprofitable ones face neglect.

In May, Samsung experienced a large-scale company-wide strike, with employees protesting unfair bonus distribution and demanding 15% of annual operating profit as bonuses.

Ultimately, Samsung and the Samsung Electronics Labor Union reached a consensus on profit distribution, but new issues arose:

Semiconductor division employees received average bonuses of KRW 513-626 million (approximately RMB 2.8 million) each, while DX division employees (responsible for phones, TVs, and appliances) received just KRW 6 million (approximately RMB 28,000) per person. The stark bonus gap led non-semiconductor employees to file a court injunction to block the voting process for the agreement.

Behind the 'wealth gap' between Samsung's two major business divisions lies not just a question of profit distribution but a strategic dilemma in the AI era: how should Samsung pivot?

The home appliance and smartphone sectors, once the cornerstone businesses supporting the 'Samsung Empire,' have reached a turning point. Samsung's response requires not just a simple market exit or retreat but a fundamental strategic overhaul.

Only by breaking free from past dependencies can Samsung's home appliance business not just 'survive' but 'thrive.'

2. Home Appliances Enter an Era of Thin Profits

Samsung has long dominated global markets through vertical integration, covering memory, panels, chips, and finished devices. This model once made Samsung unbeatable in global consumer electronics.

Take TVs as an example: before the 1980s, Japanese brands like Sony and Panasonic led in technology with superior image quality.

In the 1990s, South Korea's first LCD panel production line went operational. Subsequently, Korean brands like Samsung and LG eroded Japanese market share in display panels through production line expansions.

After 2000, Samsung and LG began leading the LCD market, with their display technology advantages reflecting in TV market share. By 2005, Samsung claimed nearly 20% of China's TV market, becoming the champion.

However, Samsung's decline began in 2015. Aowei Cloud Network data shows Samsung's home appliance market share in China plummeted from 12.3% to 1.5% between 2015-2025.

Meanwhile, Chinese TV brands rose in the display panel industry.

TCL and other leading TV brands, through acquisitions of panel production lines and self-built high-generation lines, dealt a dimensionality-reducing blow to Korean production lines, becoming the new 'LCD overlords.' By 2025, Chinese companies accounted for over 70% of the global LCD market.

The history of TV development shows that mastering the full industrial chain closed loop (closed loop) grants control over global resources and adaptability, enabling superior yield, stability, and cost compression—key advantages in fierce competition.

The problem is that Samsung is losing this advantage.

On one hand, Chinese brands like TCL and Hisense are catching up, transitioning from LCD to LED and even Micro LED technologies, achieving leapfrogging from 'followers' to 'leaders' in high-end displays.

Sigmaintell data shows Chinese brands held over 60% of the global Mini LED TV market share in 2025, eroding Samsung's former technological moats.

On the other hand, as global home appliances enter an era of thin profits, Samsung seems disinterested in continuing traditional display panel battles. It has shut down LCD lines and decided to phase out LED businesses.

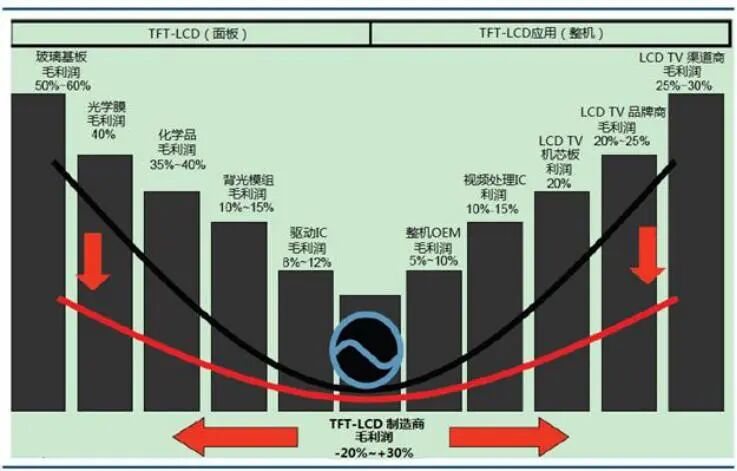

To understand this, one must recognize that display panels occupy the 'bottom' of the 'smiling curve' in the TV supply chain—the lowest-value segment.

Take LCD panels: upstream suppliers of glass substrates, optical films, and other materials enjoy 20-60% gross margins; downstream integrators, brand owners, and distributors also command brand premiums. Meanwhile, mid-chain LCD panel and module manufacturers earn just 15-20% margins.

Worse, recent years have seen intensifying price wars in home appliances, further compressing profit margins across the TV supply chain.

In 2025, about 60% of the ~60 A-share home appliance companies reported YoY declines in net profit attributable to shareholders, meaning even Samsung's full supply chain advantages could not squeeze profits in a saturated market.

Thus, Samsung's abandonment of self-research and production for mid-to-low-end home appliances reflects proactive adaptation to market changes, concentrating resources on semiconductors, AI, high-end healthcare, and other cutting-edge fields—escaping the mid-to-low-end price war quagmire to pursue high-quality growth.

3. Will Chinese Manufacturers Seize the Opportunity?

Samsung is transforming from a consumer electronics giant into a high-end, intelligent, and diversified tech brand.

Note that Samsung is not entirely exiting mid-to-low-end home appliance businesses but considering outsourcing low-margin manufacturing to contract manufacturers. Samsung products will remain on the market.

Moreover, Samsung is not alone. LG, Sony, Toshiba, Panasonic, and other brands have already exited China through equity sales and brand licensing, retaining only their most valuable 'brand' assets.

This 'retreat' by leading global brands has created vast growth opportunities for Chinese companies.

However, seizing this opportunity is no simple task. This is not just a zero-sum game but a reshuffling of the global home appliance value chain.

First, contract manufacturing remains a low-margin business. If Chinese companies merely accept mid-to-low-end OEM orders, they will continue earning 'hard-earned money' without fundamentally altering their position in the global value chain.

Thus, Chinese OEMs must escape the 'manufacturing trap' of thin profits not by quantity but by quality—leveraging supply chain synergies and smart manufacturing efficiencies to activate capacity and scale production, transforming OEM profits from 'sweat money' to 'technology money.'

For example, Changhong's Changhong Jijia built southwest China's largest 2000T stamping flexible production line last year, producing a TV backplate every 6 seconds to meet explosive demand for ultra-large-screen electronics.

Second, China's home appliance industry must develop clearer brand tiers: high-end players should pursue brand premiums, overseas expansion, and technological innovation to protect profit pools; low-end players can scale production to reduce costs and compete globally on quality.

To some extent, Samsung's 'disengagement' provides a reference model for Chinese brands:

Instead of crowding into mid-to-low-end markets, Chinese companies should voluntarily cede some mid-to-low-end capacity, allowing 'high-end brands to ascend and low-end brands to scale'—each earning their share and defending their turf to collectively drive industry upgrades.

For Chinese home appliances, Samsung's market exit presents opportunities, but how much they can seize and sustain depends on Chinese companies' own choices and capabilities.

In the global home appliance era of thin profits, Chinese brands must make strategic choices—not just targeting what Samsung abandons but understanding why Samsung pursues its new directions.

-

![]()

NIO Maintains Brand Premium: Onvo Sets Minimum Price at 150,000 Yuan, Avoids Direct Competition with Leapmotor and BYD | MJ Pro

-

![]()

“From a 5-minute escape window to a zero-fire baseline, I finally feel confident driving an electric vehicle”

-

![]()

Profits Skyrocket! From Leasing to Construction: A Storage Enterprise with Hundred-Billion-Yuan Revenue Plans 1.175 Billion Yuan Investment in New Headquarters

-

![]()

Discounts Now on Offer: Is Xiaomi No Longer Grappling with Vehicle Shortages?

-

![]()

Samsung Doesn't Make Money the Hard Way

-

![]()

Japanese Media Acknowledges: China's Engine Technology Outstrips That of Japanese Firms

-

![]()

Japanese Media Concedes: China’s Engine Technology Outpaces Japanese Firms

-

![]()

Doubao Professional Version Unveiled! China Now Boasts Its Own National-Level Professional AI Agent